CA - The Smead International Value Fund Q1 2023 Shareholder Letter

2023-04-27 05:09:00 ET

Summary

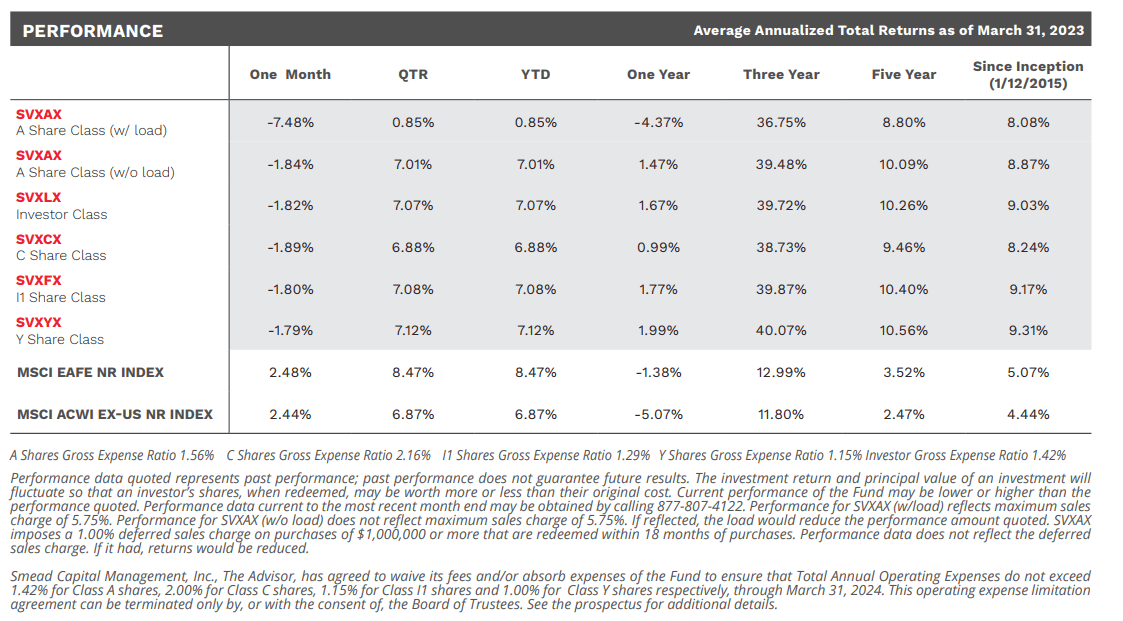

- We are pleased to report that the Smead International Value Fund had an absolute return of 7.07% for the quarter.

- The shareholders of the Smead International Value Fund have invested alongside us but aren’t adding strings to the investment discipline that we use to build wealth.

- We believe the marvel is found in the unspectacular businesses that give investors good pricing and good capital structures with growing consumer markets as their allies.

{kind=link}

Dear Shareholder

Our job is to create wealth for our investors, and we are always happy to post a positive return.

We are pleased to report that the Smead International Value Fund ( SVXLX ) had an absolute return of 7.07% for the quarter. Our job is to create wealth for our investors, and we are always happy to post a positive return. At the same time, we acknowledge that we are judged on a relative basis and the Fund underperformed the MSCI EAFE Index, which gained 8.47%. Our biggest contributors to performance for the quarter were UniCredit ([[UNCFF]], [[UNCRY]]) (UCG IM), MEG Energy ([[MEGEF]], [[MEG:CA]]) (MEG CN), and Frontline ( FRO ) (FRO NO). Our holdings in Cenovus Energy ([[CVE]], [[CVE:CA]]) (CVE CN), Bankinter ([[BKIMF]], [[BKNIY]]) (BKT SM), and BAWAG Group ([[BWAGF]], [[BAWAY]]) (BG AV) were the largest detractors in the quarter. Isn’t it ironic that our biggest contributors and detractors came from similar industries? The market continued to experience the quarter-to-quarter volatility we mentioned in our last letter. This provided us with an opportunity to increase our exposure to wonderful companies that are well-positioned to compound wealth for our investors.

Buying Unwanted Assets

To kick off the beginning of 2023, there continues to be a bias we see in equity investor portfolios. These portfolios have many of the traits investors see at the endpoints of the economy like software, consumer products, and computer chips. What they often don’t own or under-own are the building blocks of the economies of the world. These tangible products drive construction, power transportation or enhance production. We believe this is particularly true in producers of oil, for the movement of goods, and the production of commodities that create most of the electricity like natural gas and coal. We get excited for the prospects surrounding this phenomenon because there is nothing better than a lack of competition in the ownership of economically-needed products. Our investors are buying unwanted assets.

Charlie Munger explains that ignorance avoidance is one of the easiest ways to have success in life. We agree with Munger and try not to do stupid things. Some investors practice this in reverse. In today’s market, there are some attractive simple risks. Below is the first picture providing information that we care deeply about. The chart below shows the share of coal as a percentage of energy consumption in the respective countries. This explains something that we all know. The US, Germany, and China have reduced their use of coal as a primary consumer. What’s no one saying? India, South Africa, Vietnam, Indonesia, and Japan are at the same place or higher than they were 30 years ago. Remember that each of these countries consumes more total energy today than thirty years ago. So, coal demand has grown despite its declining use as a percentage of total energy consumption.

Don’t pay attention to the developed world’s energy consumption. They are rich. They have the means to pick and choose their energy sources, but where the world’s population is likely to grow the most, coal is “el hefe.”

The UN projects that the world population will close the 21st century with roughly 10.9 billion people.1 Interestingly, 80% of the people in 2100 will live in Asia and Africa. These are not big wind and solar customers. These tend to be economies where a lack of energy impacts economic growth. Again, the West can be picky. These places want economic growth. America didn’t care where its power came from when it was an emerging market. It only cares now when it’s comfortably wealthy and the Bible competes with other religions.

We own a lot of oil and gas assets in OXY ([[OXY]], [[OXY.WS]]) (OXY US & OXY/WS US), MEG Energy (MEG CN), Cenovus Energy (CVE CN) and Whitecap Resources ([[SPGYF]], [[WCP:CA]]) (WCP CN). We also own companies that would like to move oil around the oceans of the world in Frontline (FRO NO). Why are we explaining population growth and the dependence on coal? It’s because we know that many worldwide investors have been trained to hate the oil and gas business. This made them unwanted assets. We believe we are seeing signs with other commodities that are hated more than oil and gas and could be attractive for investors.

ESG investment mandates have caused numerous institutional investors and the marketing arms of money management firms to completely avoid oil, gas, and coal assets. We don’t believe this causes managers to be investors because it’s rules-based investing. The question is whether the rules are wise.

The shareholders of the Smead International Value Fund have invested alongside us but aren’t adding strings to the investment discipline that we use to build wealth. In effect, our investors have become an advantage as they are only seeking to build wealth. They are not trying to build a religion or explain why their view of the world is greater. This puts the Fund at an advantage in pursuit of attractive but unwanted assets. We believe the smartest people in the commodity markets have been the folks at Glencore. We do not own shares in their London listing but pay attention to what they do because they have deep knowledge of what goes on in energy, metal, and mining assets. The King of Oil about Marc Rich is a great resource to understand our view of this.

The unwanted assets today broadly sit in commodity markets. Because of this, there has been a scarcity of new projects started globally. This starving of new investments to find tangible goods like copper, coking coal, and iron ore is only worsened by the Western government’s unwillingness to allow new projects to begin inside their domain.

The investor’s saying never and the government’s doing this likely means a squeeze coming in the price of these goods. The folks at Glencore ([[GLCNF]], [[GLNCY]]) showed their hand with a proposal to buy Teck Resources ([[TCKRF]], [[TECK]], TECK.B:CA ) in Canada at a 20% premium to what they traded for. Teck quickly rejected them. Glencore followed by adding cash to sweeten their prior stock deal on April 11th. Why is a large commodity trading firm stalking a Canadian copper/metallurgical coal business? There are few out there.

Lastly, let’s look at some pricing on these businesses. Below is a chart of the price-to-book (P/B) ratio of the coal mining businesses greater than $3 billion of market capitalization in North America, Europe, Africa, and Developed Asia versus the MSCI EAFE’s price-to-book ratio in red.

Source: Bloomberg. Data from 1/1/1996 - 3/31/2023.

You can buy them at a nice discount to many stocks abroad. What is interesting is that five of these six companies have more cash than debt. It’s hard to go bankrupt with more cash than debt.

It is our suspicion that many investors are looking for some spectacular company to own. We believe the marvel is found in the unspectacular businesses that give investors good pricing and good capital structures with growing consumer markets as their allies. Canadian billionaire Jim Pattison has been asked why he has bought various companies that have made him very wealthy over time. He says, “I buy things that no one else wants.” We seek to compound our money in harmony with what Jim has done while practicing the ignorance avoidance that Munger advocates. This leads us to buy unwanted assets in various energy markets around the world; products that come from the ground, not the cloud. By being excited about this boring approach, we fear stock market failure.

Fear stock market failure,

Cole Smead, CFA, Lead Portfolio Manager

Bill Smead, Co-Portfolio Manager

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

The Smead International Value Fund Q1 2023 Shareholder Letter