BMO:CC - The Ultimate 7%-Yielding SWAN Bargain Buys

2023-10-24 07:10:00 ET

Summary

- Clickbait articles promoting financial apocalypse are designed to maximize panic but can be easily debunked.

- These articles will throw out many plausible reasons that stocks, bonds, and cash are all in trouble, but their facts are wrong.

- I explain why the housing market isn't crashing; cash is a safe place for conservative investors, and evidence from 134 financial metrics that another financial crash isn't coming.

- Risk management, not the elimination of risk, is the key to retiring rich. Rating agencies like S&P are able to accurately measure fundamental risks using over 1,000 risk metrics.

- This article highlights five world-beater blue-chips with risk management in the top 4% of all global companies, A-credit ratings, and an average yield of 7.2%. They are 28% undervalued and offer almost 100% total return potential over the next two years, 4.5X more than the S&P 500. And they could more than quadruple over the next decade, delivering twice the return potential as the market but with 5X the much safer yield.

It's a scary world out there, and it always has been.

It's just that today, there are websites promoting every crank and doomsday prophet out to generate clicks and sell books about "secret" ways to get rich in the coming financial apocalypse.

The Daily Doom

This weekend, I got a panicked message from a member in our chat room asking about the above article posted on "The Daily Doom."

Here is a quick explanation of how these panic-inducing articles work and why you should ignore them.

The Anatomy Of Panic

This article is a perfect example of what is called "The Gish Gallop" in debate strategy.

It takes headlines from credible sources, such as CNBC or Bloomberg, and then spins them into a completely wrong conclusion designed to maximize panic.

For example, no less than Howard Marks has said that the return of historically normal interest rates is a likely sea change.

But this article spins a return to historically normal interest rates as the harbinger of the ultimate financial collapse, from which there will be no safe harbor.

Not bonds, stocks, or even cash will be safe from the coming hyper-inflation collapse.

This article just goes on and on, throwing out over a dozen claims, sometimes no more than "Here is another terrifying headline I found."

The reason the Gish Gallop is used in debate is that there is no way to debunk all the arguments without devoting way more time than any credible expert has.

It would take 6 hours to go point by point debunking every claim in this doomsday prophet article, and obviously, I have better things to do with my time.

Rest assured, reading through this article, I instantly saw the holes in their logic and knew what charts and data I could use to disprove the panic-inducing clickbait claims.

Here are just 3 of the biggest claims and how I know they are wrong.

Cash Can't Protect You!

The Fed is not going to let inflation get above the Fed funds rate again, they have made this very clear.

{kind=link}

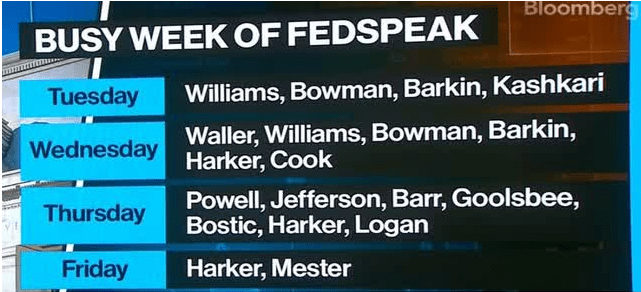

Last week, there were 22 Fed speakers: the presidents of each of the Fed regional banks and Chairman Powell himself.

The very reason interest rates are soaring is because the bond market is starting to believe the Fed's "higher for longer" strategy.

In fact, last week, President Waller sent long-term rates spiking 0.1% simply by saying that QT might be $1 trillion higher than initially expected, running through mid-2026 and hitting $3.5 trillion.

Effectively the Fed started out trying to suck $2.5 trillion out of the economy and is now considering sucking out $3.5 trillion.

The Fed's official dot plot shows no rate cuts until November of next year after one more hike this year.

Goldman Sachs thinks inflation MIGHT rebound to 5% by January before starting another gradual decline.

If that happens, the Fed will be hiking steadily and cash yields, especially T-bills track the Fed funds rate.

So, if CPI goes to 5%, the Fed is going to 6%, and cash will go above 6%.

If CPI keeps rising due to an accelerating economy, then the Fed keeps hiking, and cash stays above inflation.

Right now the real rate on cash, short-term T-bills minus inflation is 2% to 3% depending on what inflation metric you look at.

So no "there is no place to hide" is absolutely wrong. Cash now pays you a 2% real rate.

Another Housing Crisis Is Right Around The Corner! Except It's Not

One of the favorite things for doomsday prophets to do is claim that another housing crisis is right around the corner.

Higher for longer rates = bond losses for banks! That's true.

And bank bond losses killed SVB! That's also true.

And now bond losses are going to crash the housing market and that's what caused the Great Recession! So another Great Recession (or worse) is imminent!

Absolutely not.

{kind=link}

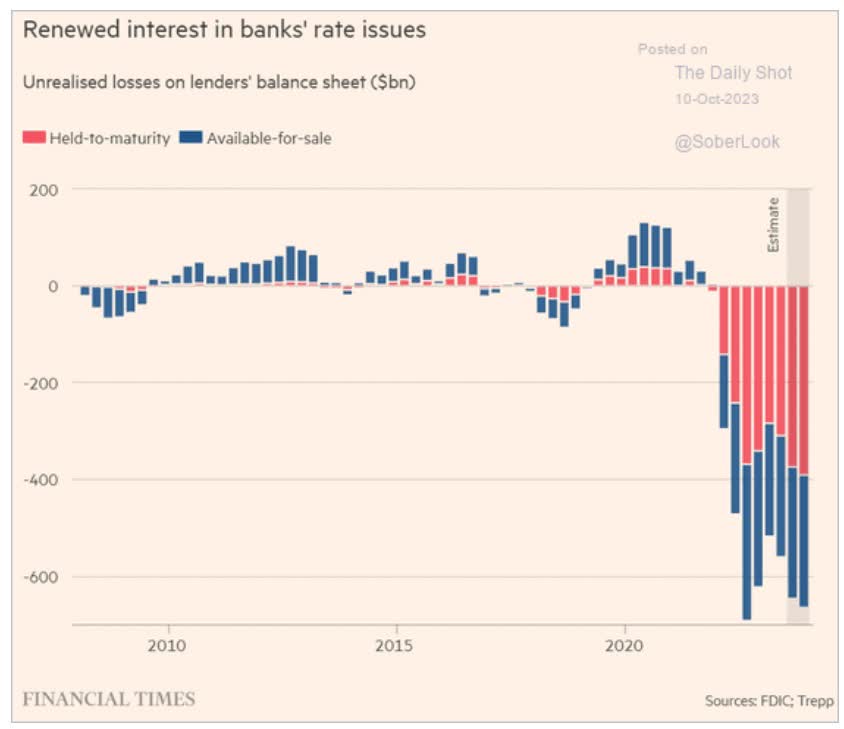

Yes bond losses at banks are over $600 billion. But these are "held to maturity" U.S. treasury bonds.

Unless the banks are forced to sell at those losses they are fine.

SVB Financial Group (SIVBQ) was forced by a bank run to sell everything at any price, and that's what killed it.

The big banks have seen deposits go up during the regional banking crisis and regional bank deposits have also started rising again.

The Fed's new lending facility offers 100% of face value on bonds, for 12 months at 5.4% interest rates.

In other words, even if a bank had bought 100% 30-year U.S. bonds at record low yields and is down almost 60%, the Fed will lend it for 100 cents on the dollar.

Are some regional banks likely to fail if rates stay this high for long enough? Yes, up to 200, according to Stanford.

- 200 small regional banks out of 4,000

- none close to the size of First Republic and SVB.

What about another housing crisis?

No There Isn't Another Housing Crisis Coming

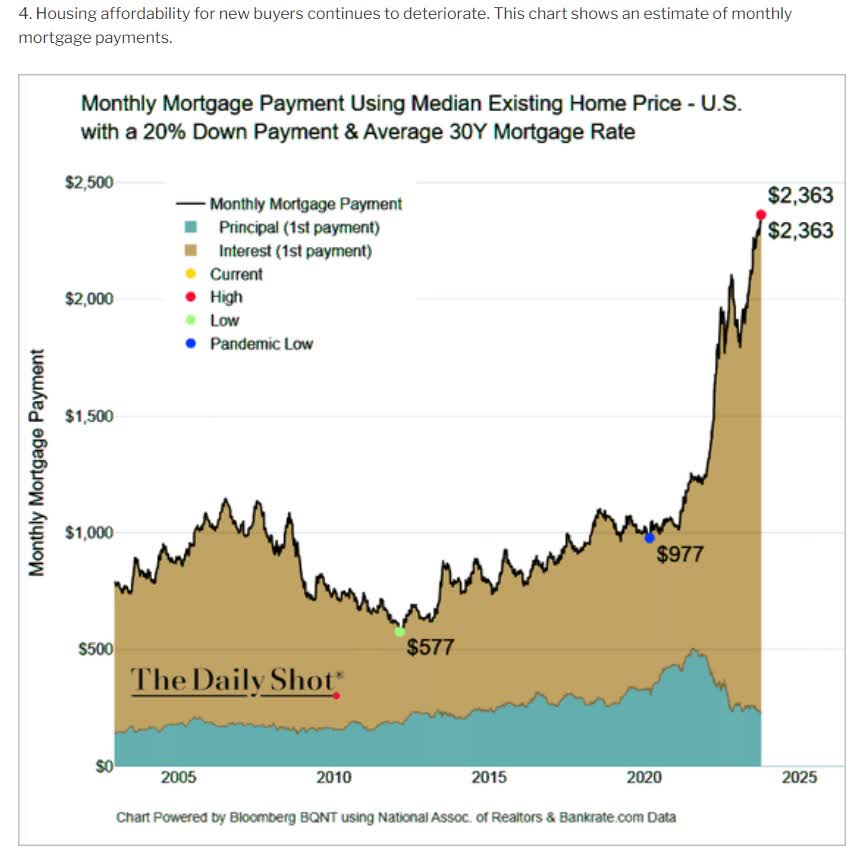

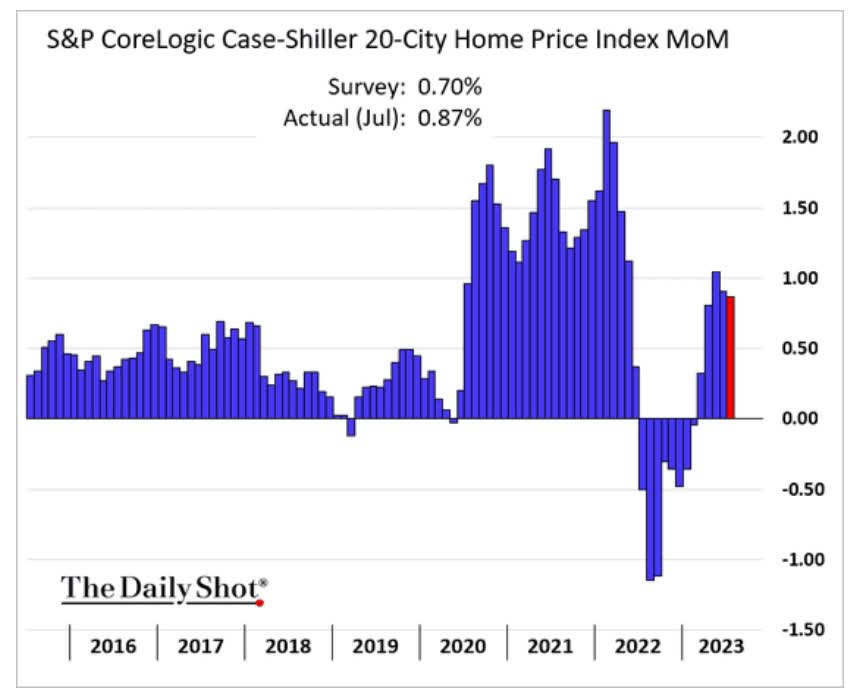

Mortgage rates just hit 8%! The housing market is frozen! Home prices are going to crash! And the last time that happened the global financial system melted down!

{kind=link}

Median mortgage costs have quadrupled in 4 months! Doom, gloom, and boom! Everyone buy my book which has been predicting cataclysm and calamity for a decade!

Guess what? The housing market isn't melting down.

{kind=link}

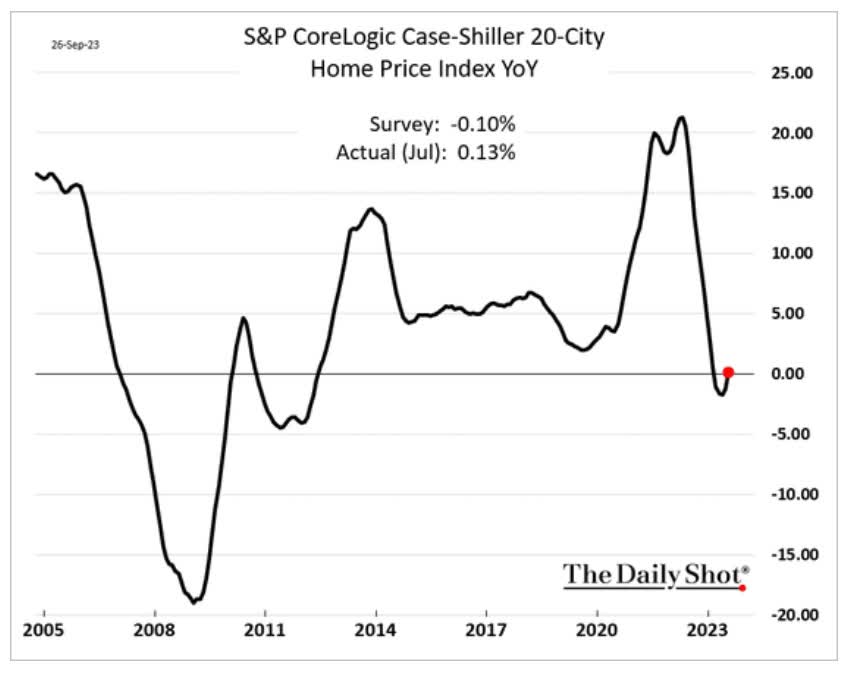

Year-over-year home price changes are not cratering. Not even close.

{kind=link}

In fact, they are going back up.

How on earth can home prices not crash when mortgage rates are 8%? Because of the frozen housing market.

Imagine you refinanced your home during the Pandemic at 3%.

- 2.6% was the record-low 30-year mortgage rate.

Can you sell your home knowing you have to buy another one but this time the mortgage rate is 8% and home prices have soared? Nope.

That's why existing home sales have fallen to the lowest level in a quarter century.

That leaves home builders as the only new source of home supply.

{kind=link}

America's supply of new homes has been lagging population since at least 1995, and this is why home prices are going up, not crashing.

And even if home prices fall up to 10% (the highest decline estimate from a blue-chip economist team, Morgan Stanley), that isn't going to crash the economy.

In 2008 banks like Citigroup were 40X leveraged to toxic mortgage-backed bonds via credit default swaps.

Today Bank of America's average FICO score on new loans is over 800.

Big banks, the ones that if they failed would destroy the financial system, have no exposure to toxic mortgages.

The Great Financial Crisis caused by home prices collapsing simply can't happen again.

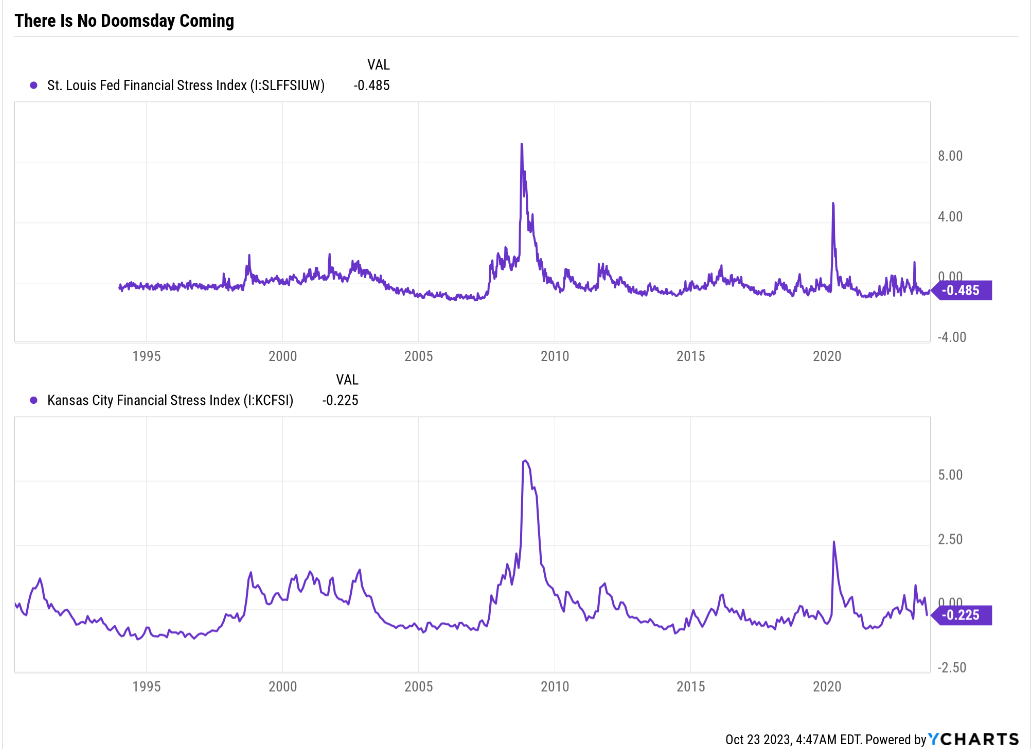

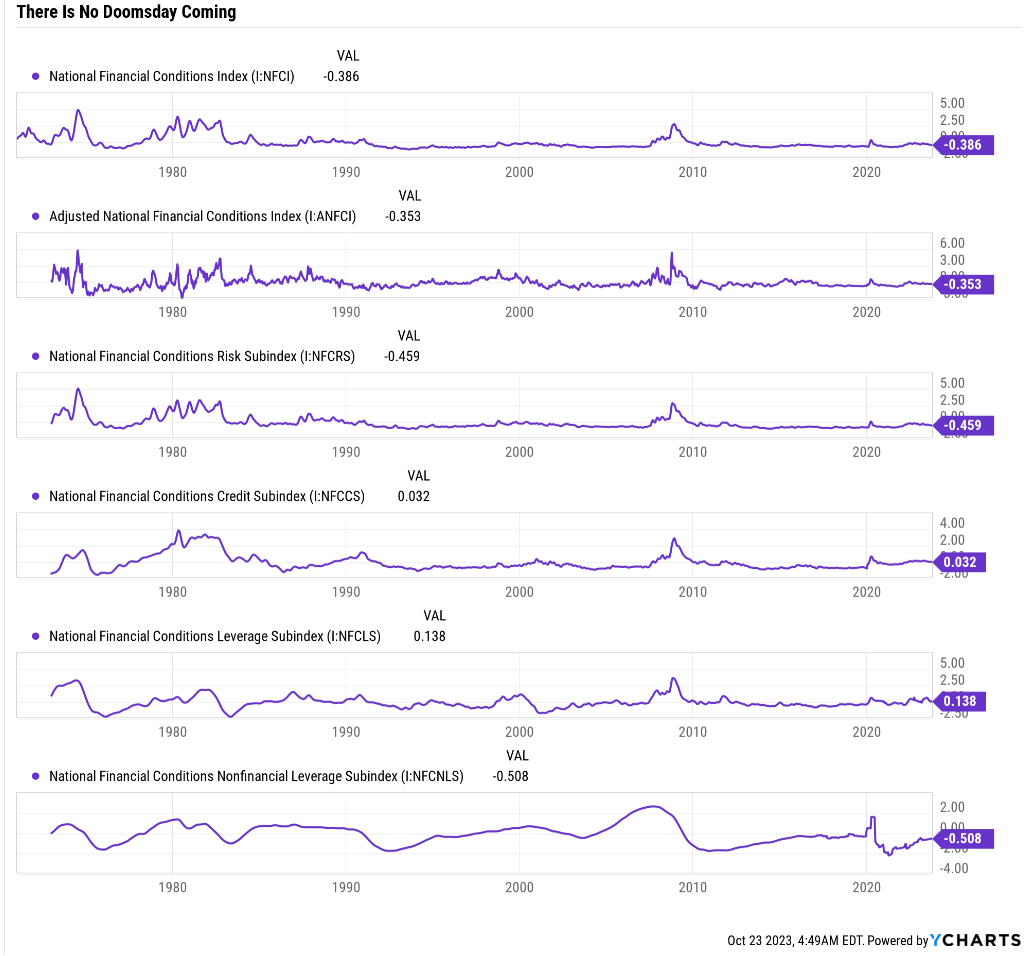

Proof The World Isn't Ending

Ultimately there are 2 charts that disprove all the doomsday prophets claiming that the biggest crash in history is beginning. Predictions that make for shocking headlines but are always laughably wrong.

{kind=link}

{kind=link}

{kind=link}

The St. Louis Fed, Kansas City Fed, and Chicago Fed track 134 weekly financial indicators covering every part of the economy, including bank default rates and loan losses.

{kind=link}

Zero is calibrated to be the average since each metric began which is over 30 years.

{kind=link}

Chicago's financial stress model has over 50 years of data to work with.

And out of these 3 models covering 134 financial metrics updated weekly with the best financial data in the world, right from the Fed itself, there is zero sign of any kind of financial catastrophe coming.

This is how the entire article was. Claim after claim, of cherry-picked data, extrapolated to absurd conclusions.

It was all anecdotes and scary headlines.

Well, here's an anecdote that I think you might appreciate and help you sleep well at night.

I watch about 15 hours of Bloomberg throughout my week. There are about 100 world-class analysts, the blue-chip economist teams that Bloomberg's own data says are the most accurate in the world.

Each week those 100 experts give their takes on what's going on with the financial system, the world of geopolitics, D.C. government shutdown risk, etc.

They have a very wide range of opinions. For example, the year-end estimate for the 10-year yield ranges from 3% to 6%.

And how many of these blue-chip experts believe a severe recession much less a catastrophe from which "there is no way out" is coming? None.

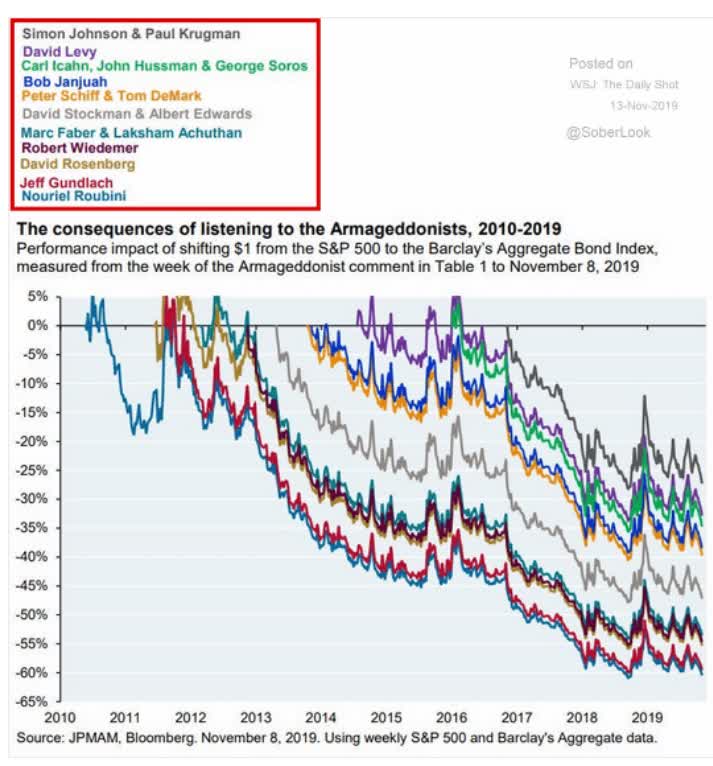

Unless all the best data we have today, and all the best experts are 100% wrong, this article is pure clickbait, designed to peddle a book that's over a decade old.

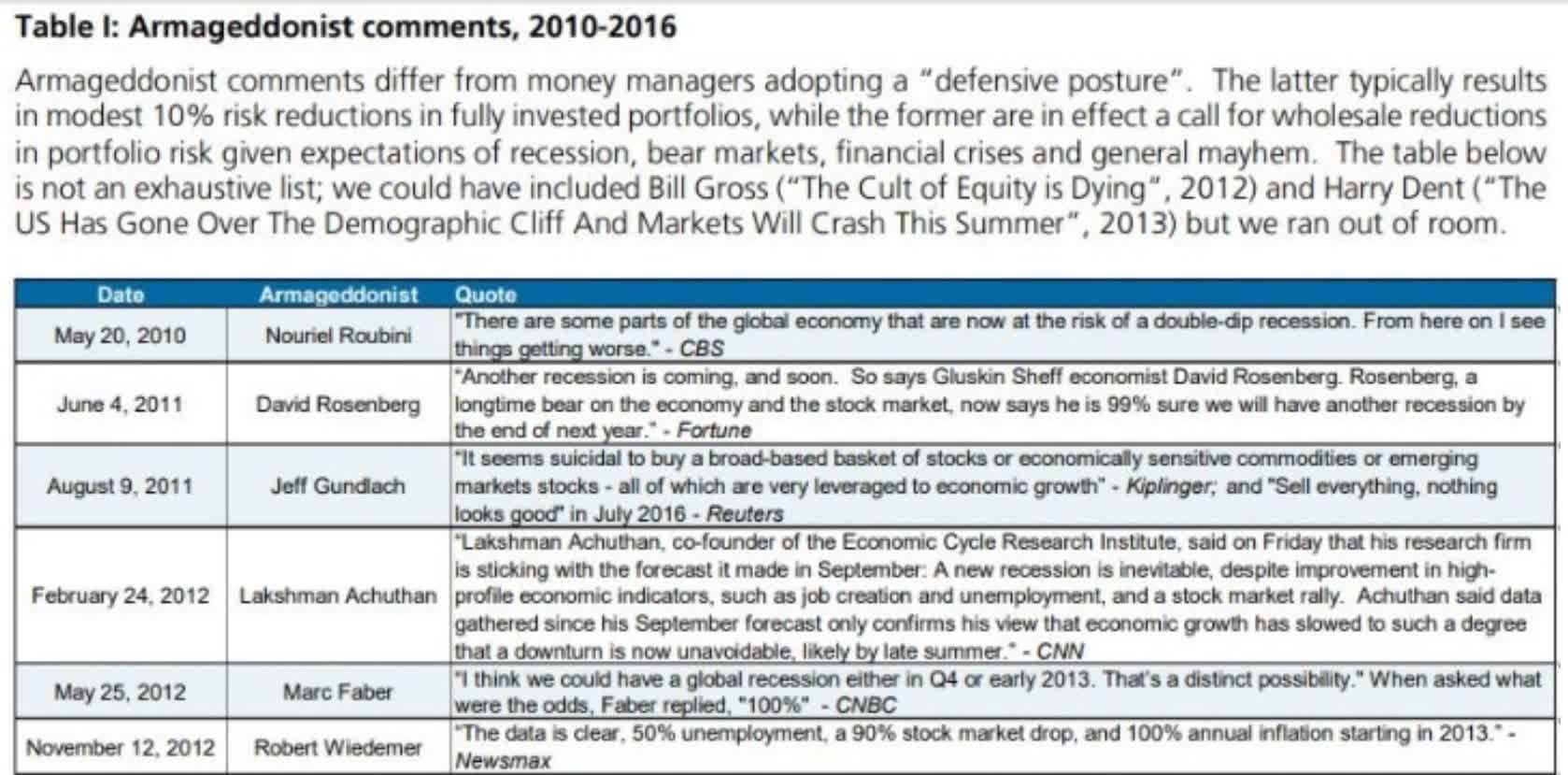

For over a decade, this author has been predicting doom and gloom and he's hardly alone.

{kind=link}

Doomsday prophets sound smart, sometimes. Usually, their arguments sound logical, always ripped from the headlines.

And they are always wrong.

{kind=link}

{kind=link}

{kind=link}

Even Nobel Prize Winners like Paul Krugman have made catastrophic forecasts and been completely wrong.

Ray Dalio, founder of Bridgewater, has admitted that his investing teams never listen to his opinion they stick to their long-term strategies and quant-based investing systems.

If the king of hedge funds says that his company is running almost $200 billion in assets without listening to him, and he's an actual expert, why would you listen to a crank whose facts are completely wrong?

How We Measure Risk Management

Risk is real, and we know how to actually measure it. The Dividend Kings uses a 3,000-point safety and quality model incorporating over 1,000 financial metrics because we include risk ratings from the world's best experts, including all major rating agencies.

DK uses S&P Global's global long-term risk-management ratings for our risk rating.

- S&P has spent over 20 years perfecting its risk model

- which is based on over 30 major risk categories, over 130 subcategories, and 1,000 individual metrics

- 50% of metrics are industry-specific

- this risk rating has been included in every credit rating for decades.

The DK risk rating is based on the global percentile of a company's risk management compared to 8,000 S&P-rated companies covering 90% of the world's market cap.

S&P's risk management scores factor in things like:

- supply chain management

- crisis management

- cyber-security

- privacy protection

- efficiency

- R&D efficiency

- innovation management

- labor relations

- talent retention

- worker training/skills improvement

- occupational health & safety

- customer relationship management

- business ethics

- climate strategy adaptation

- sustainable agricultural practices

- corporate governance

- brand management.

If something can go wrong with a business, S&P has thought of it.

- Fitch and Moody's have been working on their comprehensive risk models even longer, about 30 years each

| Classification |

| S&P LT Risk-Management Global Percentile |

| Risk-Management Interpretation |

| Risk-Management Rating |

| BTI, ILMN, SIEGY, SPGI, WM, CI, CSCO, WMB, SAP, CL |

| 100 |

| Exceptional (Top 80 companies in the world) |

| Very Low Risk |

| Strong ESG Stocks |

| 86 |

| Very Good |

| Very Low Risk |

| Foreign Dividend Stocks |

| 77 |

| Good, Bordering On Very Good |

| Low Risk |

| Ultra SWANs |

| 74 |

| Good |

| Low Risk |

| Dividend Aristocrats |

| 67 |

| Above-Average (Bordering On Good) |

| Low Risk |

| Low Volatility Stocks |

| 65 |

| Above-Average |

| Low Risk |

| Master List average |

| 61 |

| Above-Average |

| Low Risk |

| Dividend Kings |

| 60 |

| Above-Average |

| Low Risk |

| Hyper-Growth stocks |

| 59 |

| Average, Bordering On Above-Average |

| Medium Risk |

| Dividend Champions |

| 55 |

| Average |

| Medium Risk |

| Monthly Dividend Stocks |

| 41 |

| Average |

| Medium Risk |

(Source: DK Research Terminal.)

Just like Ben Graham recommended, we look at the past, present, and likely future.

We use the median analyst consensus forecast, every credit rating, risk management ratings, and the bond market's real-time fundamental risk assessments to judge the safety of companies including their dividends.

Our dividend safety scores are designed to be 95% accurate at catching dividend cuts before they happen.

We are evidence-based, using the best available data available, from FactSet, Bloomberg, Morningstar, Gurufocus, and more.

We don't speculate, we tell you the facts, as best as we know them, based on a risk-management and company safety model that's:

- 8 years in the making

- over 20,000 people hours

- over $1 million in R&D.

I watch Bloomberg and C-span, so you don't have to. And believe me, you don't want too, it's no way to live;)

How To Find The Best High-Yield SWANs In A Scary World

Here is how I have used our DK Zen Research Terminal to find the best 5% yielding blue chips to buy with the best risk management according to S&P.

From 504 stocks in our Master List to the best REIT aristocrats you can buy today.

All in one minute, thanks to the DK Zen Research Terminal. This is how I find all my investment ideas.

| Screening Criteria |

| Companies Remaining |

| % Of Master List |

| 1 |

| BHS Rating "reasonable buy, good buy, strong buy, very strong buy, ultra value buy" |

| 387 |

| 77.40% |

| 2 |

| Blue-Chip Quality (10+ quality score) Or Better |

| 355 |

| 71.00% |

| 3 |

| Non-Speculative (No Turnaround Stocks, investment grade) |

| 306 |

| 61.20% |

| 4 |

| Very Safe Dividend Safety (81%+ = 2% or less risk in severe recession) |

| 215 |

| 43.00% |

| 5 |

| 5+% Dividend Yield |

| 26 |

| 5.20% |

| 6 |

| Add Risk Management Percentile And Rank By Risk Management |

| 0.00% |

| 7 |

| Sort By Risk Management |

| 0.00% |

| 8 |

| Select Top 5 And Include In The "Ticker" watchlist creator |

| 5 |

| 1.00% |

| Total Time |

| 1 Minute |

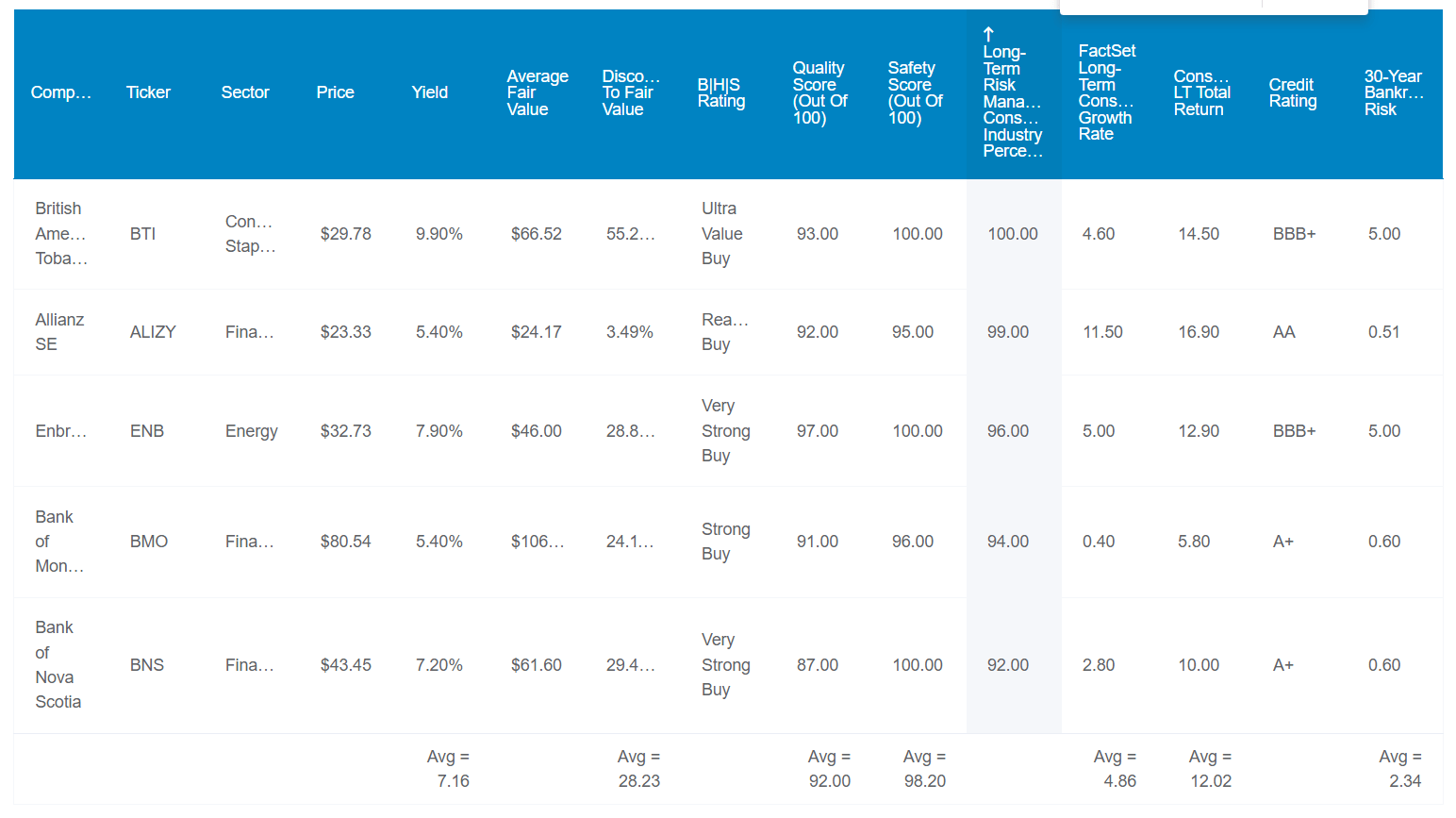

So here they are, the 5 best 5+% yielding Ultra SWANs you can trust to keep their dividends secure and protect your savings, no matter what's coming next with the economy, politics, or the stock market.

The Ultimate 5% Yielding SWAN Bargain Buys

{kind=link}

I've linked to articles highlighting each company's investment thesis. I've ranked them here by S&P's long-term risk management rating.

- British American Tobacco ( BTI )

- Allianz ( ALIZY )

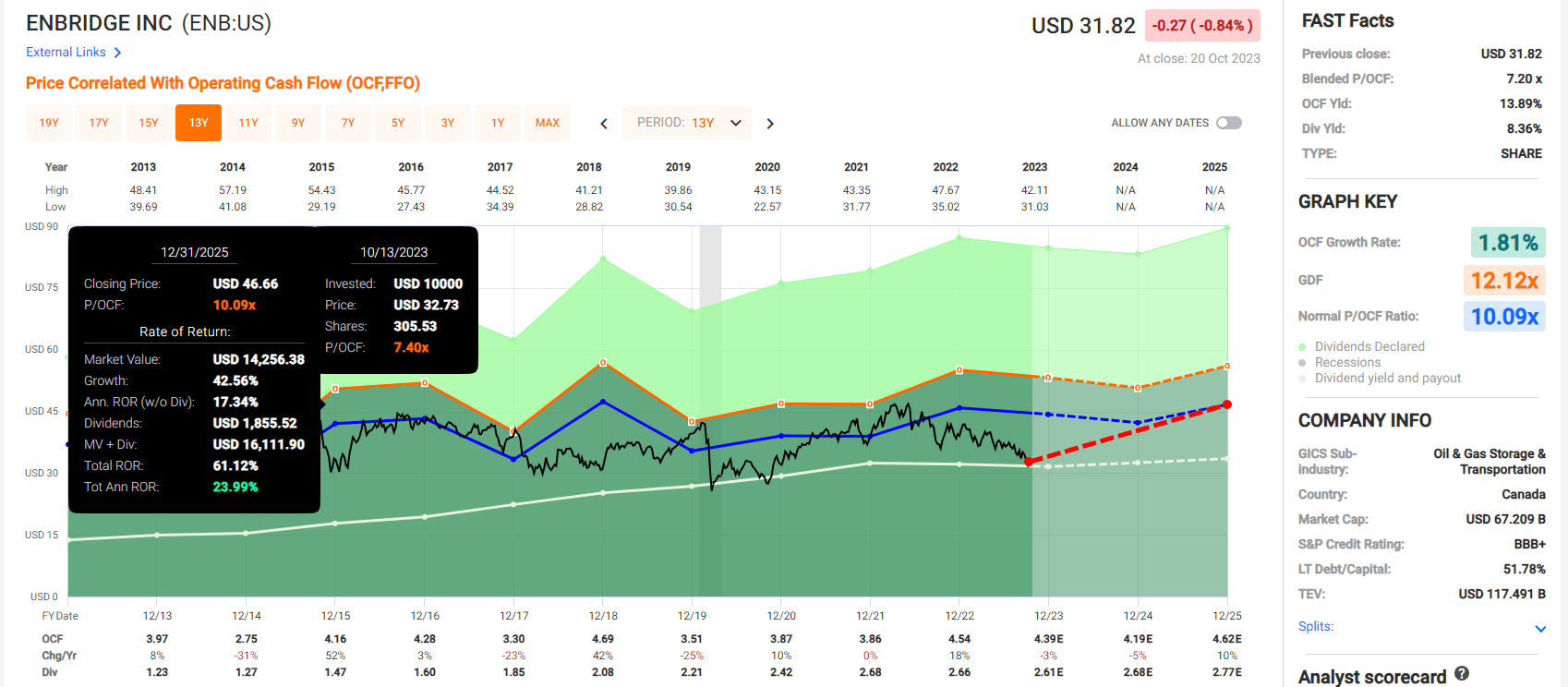

- Enbridge ( ENB )

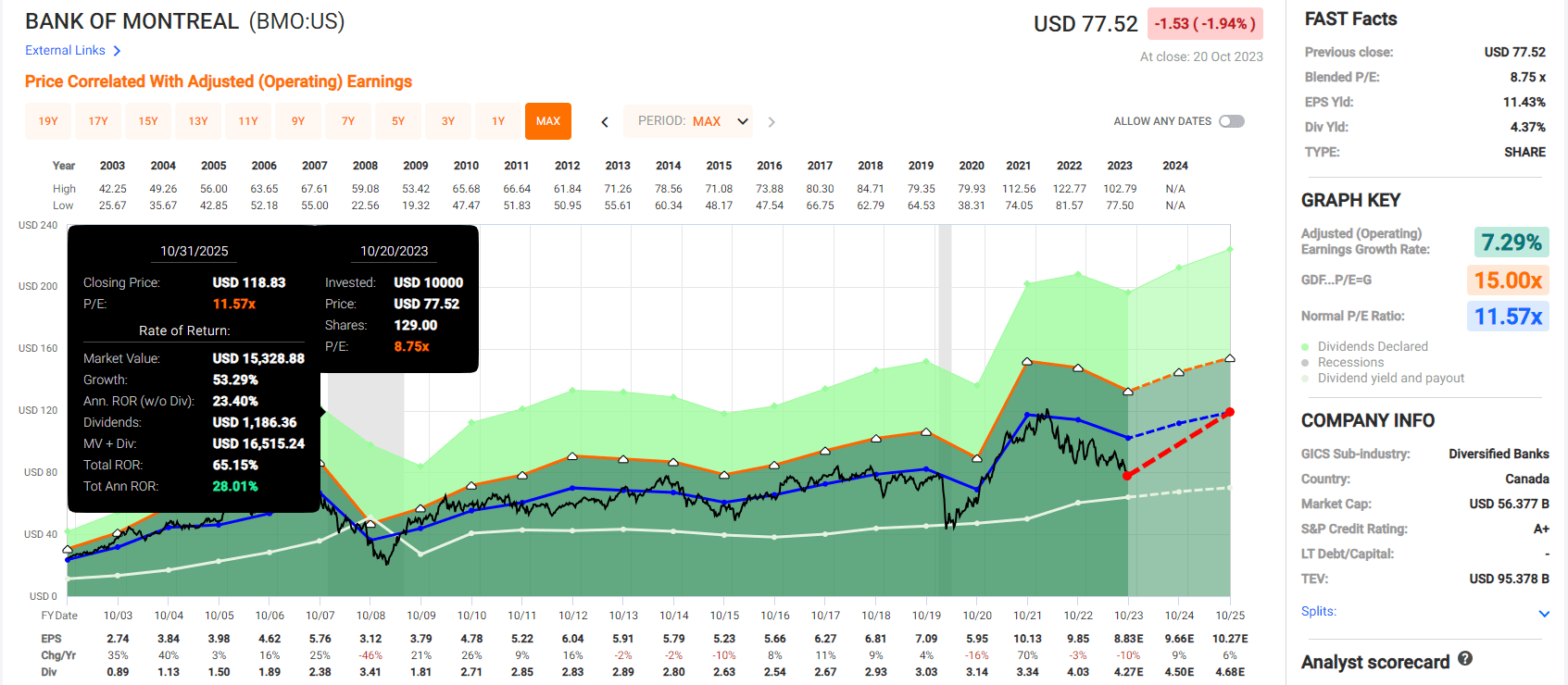

- Bank of Montreal ( BMO )

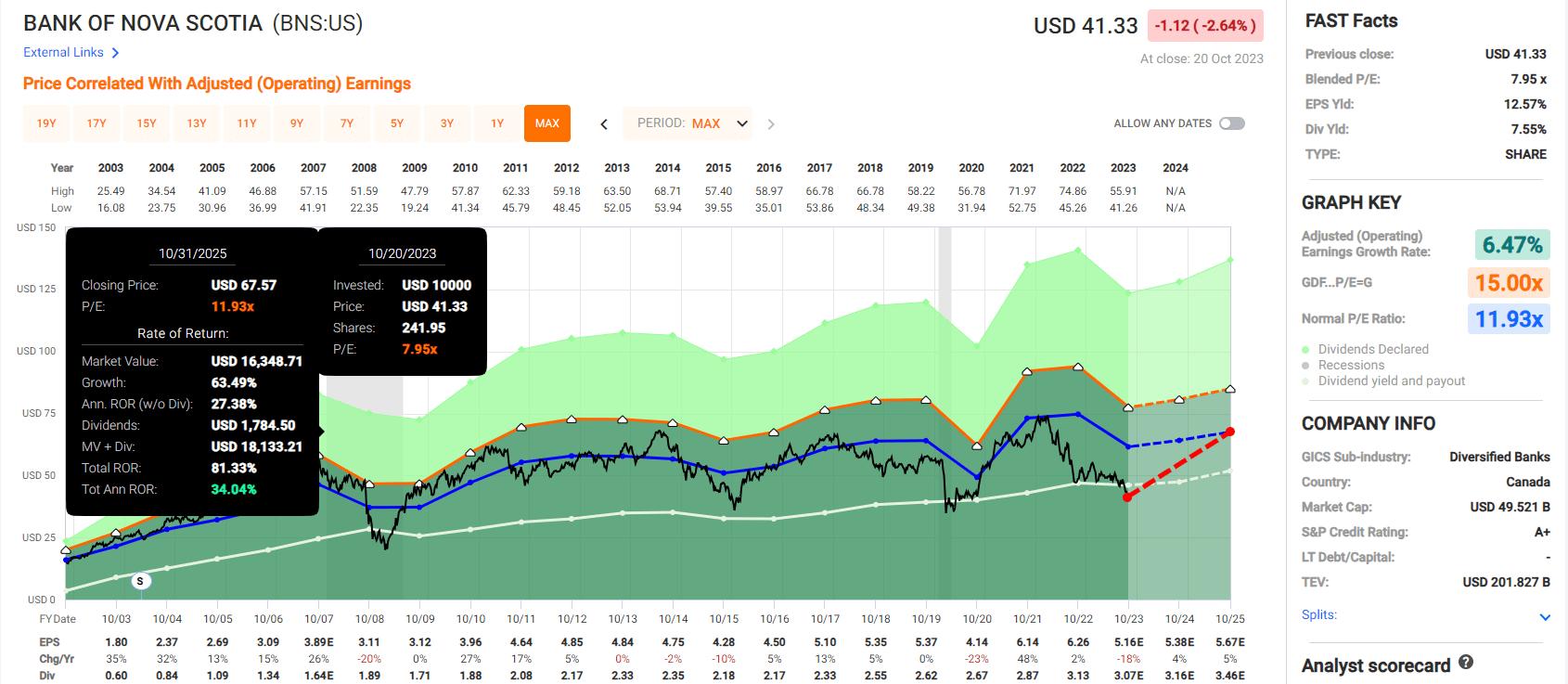

- Bank of Nova Scotia ("Scotiabank") ( BNS ).

Tax Implications

- no tax withholding on dividends from BTI

- 15% withholding on ENB, BMO, and BNS dividends (taxable accounts only)

- 26.375% withholding for ALIZY (German)

- tax credits are available for ENB and ALIZY in the US.

- Own Canadian companies in a retirement account to avoid paperwork

- own ALIZY in a taxable account to qualify for the tax credit

- own Canadian stocks in retirement accounts to minimize tax paperwork

Fundamentals Summary

- yield: 7.2%

- dividend safety: 98% very safe (1.1% dividend cut risk)

- overall quality: 92% very low-risk Ultra SWAN

- credit rating: A- stable (2.34% 30-year bankruptcy risk)

- long-term risk management percentile: 96.2% (top 3.8% of all companies on earth)

- long-term growth consensus: 4.9%

- long-term total return potential: 12.0% vs 10.2% S&P 500

- discount to fair value: 28% discount (very strong buy) vs 6% overvaluation on S&P

- 10-year valuation boost: 3.3% annually

- 10-year consensus total return potential: 7.2% yield + 4.9% growth + 3.3% valuation boost = 15.3% vs 10.1% S&P

- 10-year consensus total return potential: = 315 % vs 160% S&P 500.

Rock solid A-credit ratings, risk management in the top 4% of companies on earth, and a very safe 7.2% yield and double the total return potential of the S&P over the next decade.

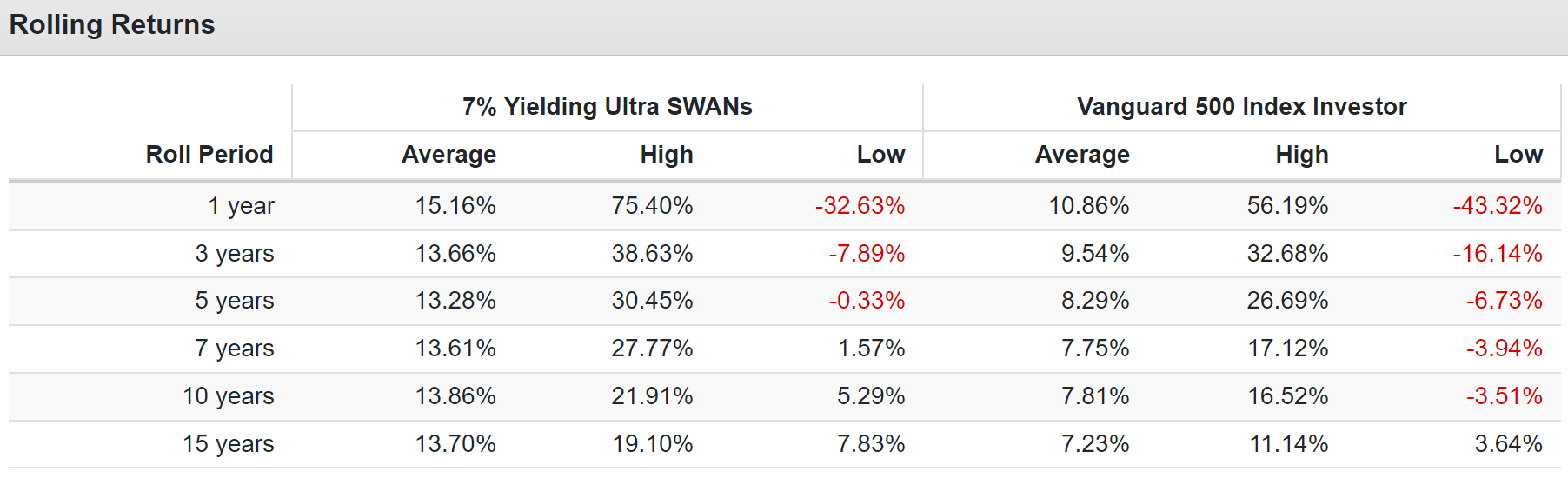

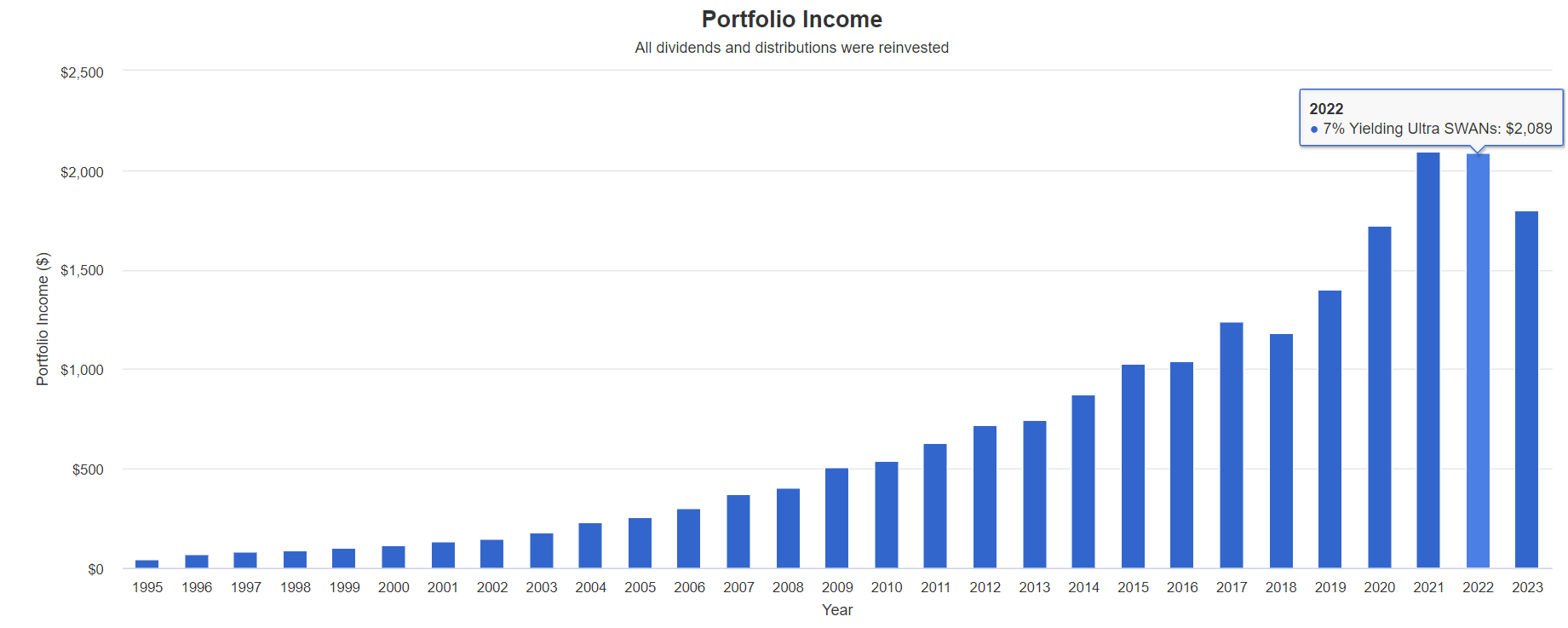

Historical Returns Since 1995

{kind=link}

{kind=link}

{kind=link}

14% annual income growth for over a quarter century.

The yield on cost is now over 200%.

Consensus Total Return Potential Through 2025

- if and only if each company grows as analysts expect

- and returns to historical market-determined fair value

- this is what you will make.

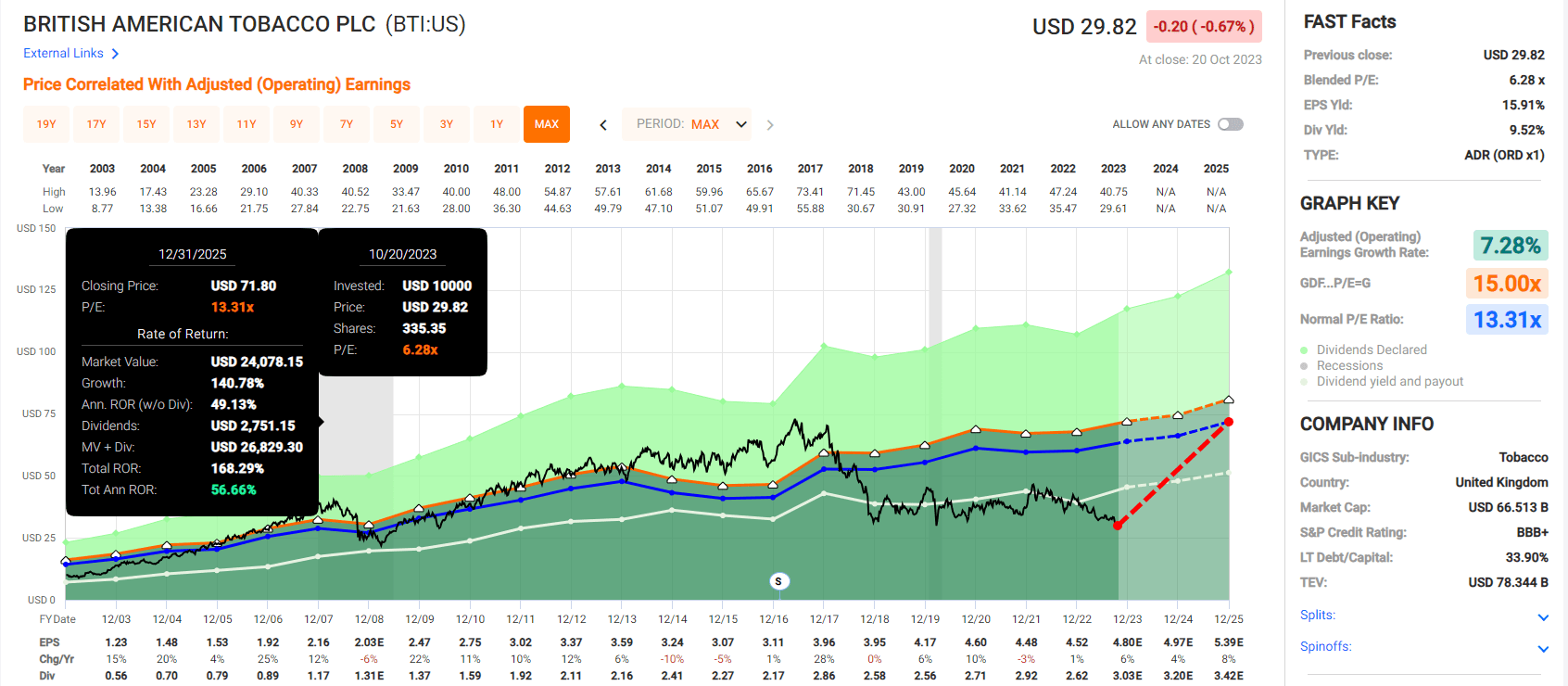

British American Tobacco

{kind=link}

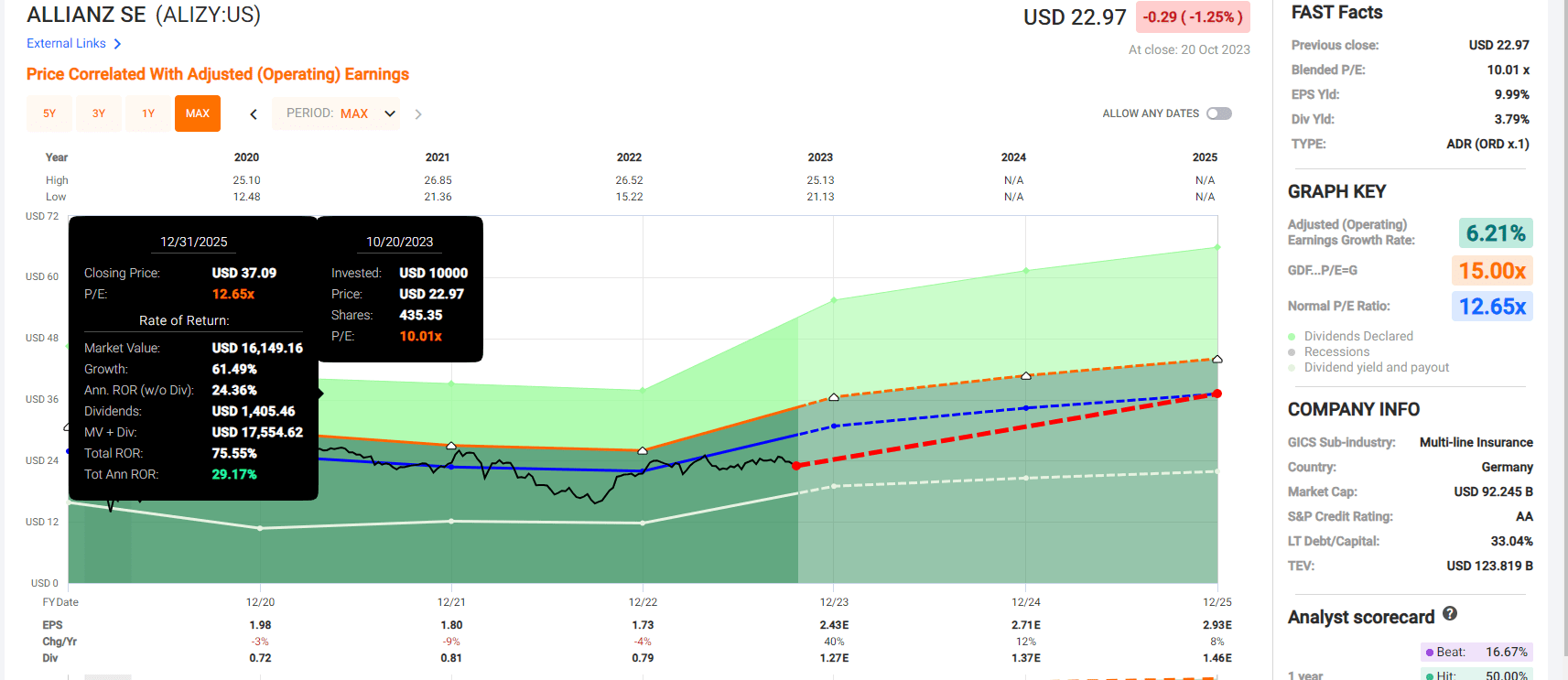

Allianz

{kind=link}

Enbridge

{kind=link}

Bank of Montreal

{kind=link}

Bank of Nova Scotia

{kind=link}

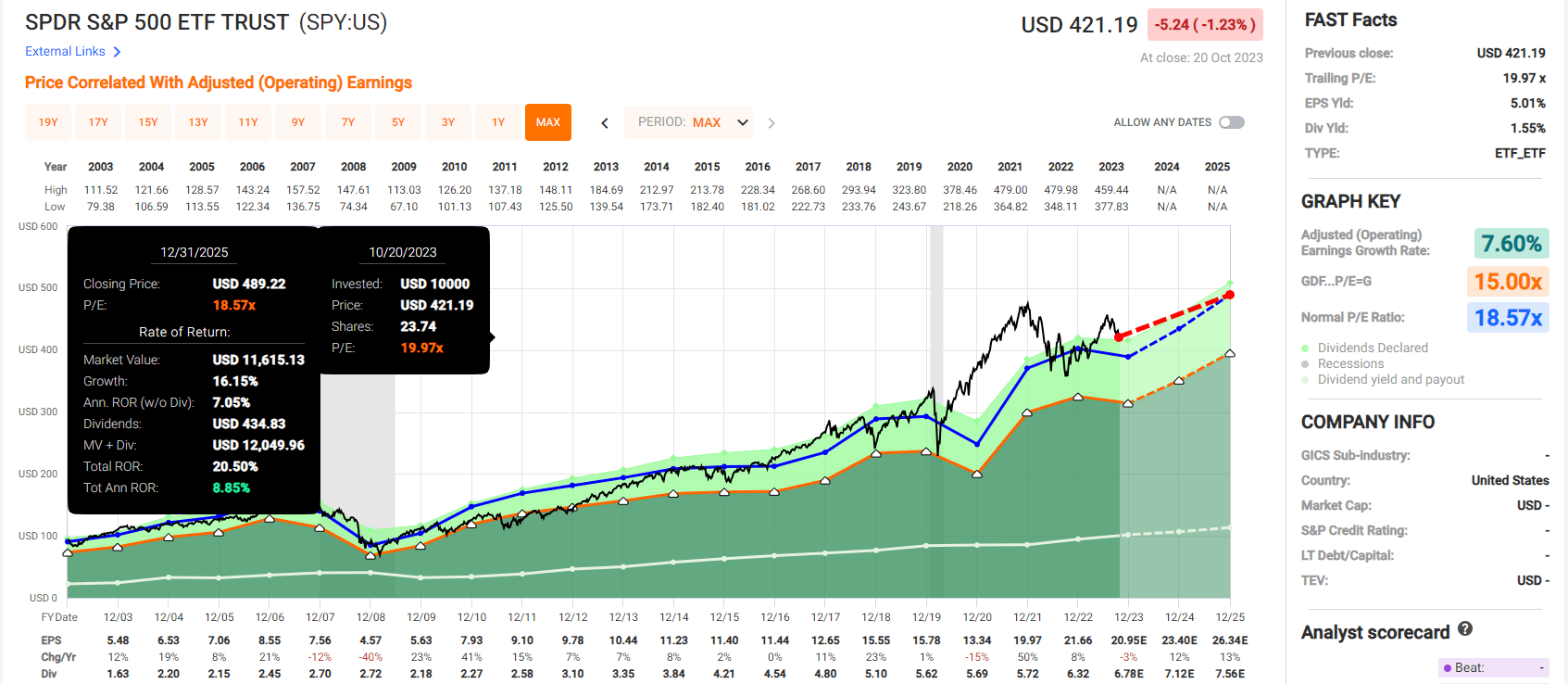

S&P 500

{kind=link}

S&P offering 21% total return potential over the next two years.

These A-rated Ultra SWANs offer 90% two year total return potential, 4.5X more than the S&P 500. That's 34% annualized return potential and a very safe 7.2% yield on day one.

Bottom Line: Trust These 7% Yielding Ultra SWANs To Keep You Safe In Scary Times

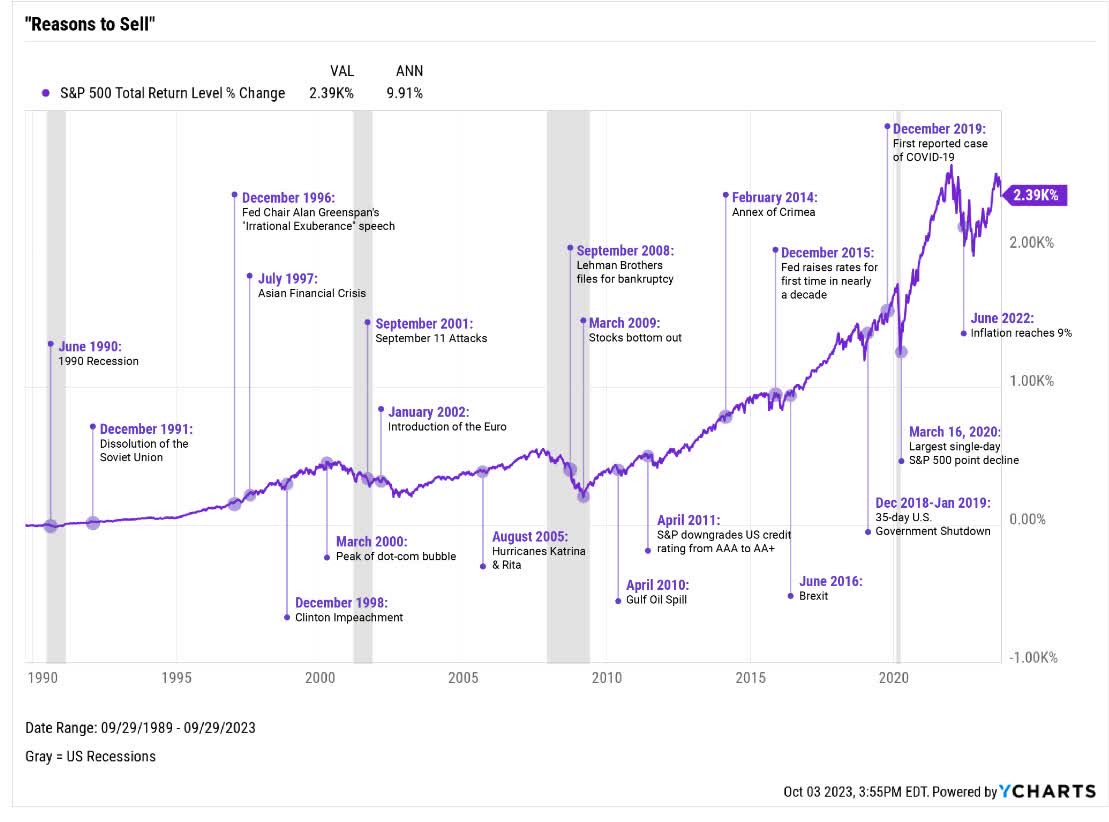

The S&P is down 9% off its record highs and yet...

{kind=link}

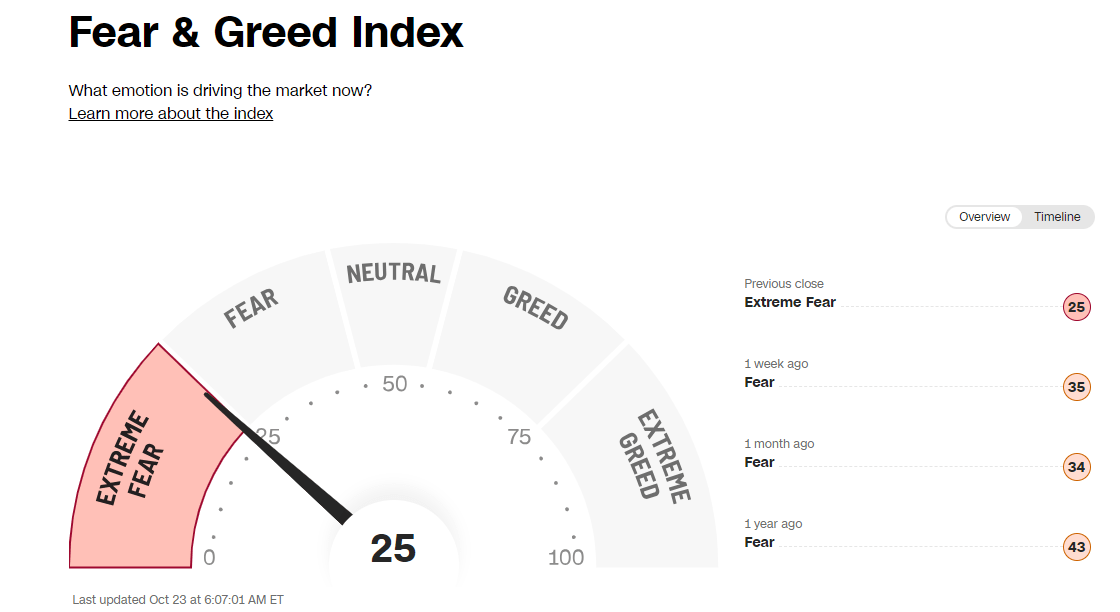

Investor sentiment is tanking and its thanks to scary clickbait doomsday prophecies like what you'll get at the Daily Doom.

While I can only ever be 80% certain about any individual company (Marks/Templeton certainty limit) or 97% confident in the long-term probability of investing success, I can say with 100% confidence that doomsday prophets are safe to ignore.

The man who is bearish on the future of America will always go broke." - J.P Morgan.

No, there is no financial crisis brewing. No, the banks aren't all going to start failing due to bond losses.

There is no housing collapse, and even if home prices fall 10% it won't cause another Great Recession.

5% interest rates are the historical norm and it will take time for corporations to adjust to the return of the old normal.

But the world's strongest companies will be just fine, as they have been through much scarier and trying times.

{kind=link}

Today's best companies have been through interest rates as high as 20%.

They sailed through a 32% GDP collapse in 2020.

They lived through the collapse of financial liquidity in 2008.

They have been rock steady sources of growing income and wealth creation for decades.

When the facts change, I change my mind, but the facts are clear.

No doomsday is coming. A prudently risk-managed diversified portfolio of dividend blue-chips has always been, and will almost certainly always be the lowest risk way to retire in safety and splendor.

Today BTI, ALIZY, ENB, BMO, and BNS are the top five 7% yielding A-rated very low risk Ultra Sleep Well At Night companies you can buy.

Companies whose legendary dividend dependability and rock solid risk management track records is just what you need to keep a cool head when others are losing theirs.

For further details see:

The Ultimate 7%-Yielding SWAN Bargain Buys