IVT - The Virtuous Cycle: Why I Love 'Expensive' REITs

2024-01-13 08:35:00 ET

Summary

- Investing in REITs primarily for high income can be risky as higher yields often correspond with higher risk.

- REITs with a low cost of capital can buy higher quality properties, while those with a higher cost of capital are often caught in a vicious cycle of declining quality.

- Several net lease REITs show the dangers of getting caught in the Vicious Cycle as well as the rewards that flow from achieving the Virtuous Cycle.

- I discuss some of my favorite "expensive" REITs with strong costs of capital, high-quality portfolios, and modest leverage.

All the time, over and over again, when I pitch a high-quality real estate investment trust ("REIT") here on Seeking Alpha, I will inevitably receive comments to the tune of:

Solid REIT, but too expensive for me. The yield is too low. I invest in REITs for the income!

Now, I don't begrudge any investor, especially retirees, for seeking to maximize the current income from their portfolio. I do that myself by allocating a portion of my investment capital to high-yield securities like midstream energy companies, high-yielding closed end funds ("CEFs"), and preferred stocks.

But there is an often overlooked danger embedded in the idea that one should invest in REITs primarily to find sources of high income.

The market may not be perfectly efficient, but it isn't stupid either. Higher yields generally correspond with higher risk. Some investors think that higher yield simply implies lower expected growth . That can be true in some cases, but most often, higher yield correlates with higher risk .

In fixed income, the terms "high yield" and " junk " are used interchangeably. And yet, in the realm of equities, investors often buy the 8%-yielding stock instead of the 4%-yielding stock believing that the only tradeoff is higher income today in exchange for lower growth tomorrow. Often, they don't understand the elevated risk they are taking.

In the REIT space, especially for net lease REITs as I'll discuss below, there are two self-reinforcing cycles that can play out:

- The Virtuous Cycle

- The Vicious Cycle

In case it isn't obvious, REITs want to attain the former and avoid the latter.

It isn't bad to seek sources of high income, but doing so in the realm of REIT common stocks is frequently a bad idea that will cause investors to own only low-quality REITs caught in a vicious cycle of becoming even lower quality.

I've made this mistake multiple times myself, so I won't be the first to cast the stone. But these mistakes have led me to a greater and greater appreciation of and concentration in high-quality, "expensive" REITs.

Let me lay some groundwork before I get to discussing some winners and losers in the realm of net lease REITs as well as a group of my favorite "expensive" REITs.

The Groundwork

Everyone has heard the classic phrase that the three most important factors in real estate investing are location, location, location .

In REITdom, however, I'd argue the most important factors are cost of capital , cost of capital , cost of capital .

According to Green Street Advisors, the industry-leading commercial real estate research and advisory firm in the US, there are four pillars of REIT excellence.

{kind=link}

I would argue that the most important of these, the one to which the rest are ultimately in service, is capital allocation.

And strong capital allocation requires a strong cost of capital.

No one has ever found a money tree that magically grows an unlimited supply of $100 bills, so no source of capital is truly free. Capital always has a price; investors always want a return on their capital.

Since REITs typically pay out most of their cash flow, their business model almost always relies on issuing or raising fresh capital in order to buy or develop properties and thereby expand their portfolios.

The best REITs are the ones that can consistently convince investors to part with their capital at a low cost. Investors are only willing to part with their capital at a low cost when they believe they will be sufficiently rewarded for doing so.

On the fixed-income side, lenders give low-cost capital to a REIT because they're convinced of the REIT's safety and ability to service and repay the debt. On the equity side, investors give low-cost capital to a REIT because they're convinced that they'll ultimately see a sufficiently high return on that capital in the form of higher cash profits (i.e. adjusted funds from operations, or AFFO, per share) with low risk of permanent capital loss.

The way REITs increase their AFFO per share over time is to consistently invest in real estate at higher cash yields than their overall cost of capital .

Actually, this is how all business models work.

Raise capital at X cost, then invest it into something that returns greater than X. The difference is profit.

If you invest in something at a return lower than your cost of capital, you lose money. You burn cash. Maybe you do it anyway because you believe that thing you invest in will eventually generate a return well above your cost of capital. But if you consistently invest at a lower return than your cost of capital, you lose money.

You see where I'm going with this.

Higher-quality real estate properties typically sell for lower yields. Low-quality properties typically sell for higher yields. Mediocre properties are somewhere in the middle.

REITs with a low weighted average cost of capital ("WACC") are able to buy higher quality and lower yielding properties while still maintaining a positive spread between their WACC and investment yields.

On the other hand, REITs with a higher WACC face a difficult situation. They can do one of five things:

- Buy nothing

- Buy lower quality and higher yielding properties

- Buy higher quality and lower yielding properties

- Sell their higher quality / lower yielding properties in order to recycle capital into lower quality / higher yielding properties

- Rely heavily on issuing debt capital that has a lower cost than equity

Sometimes, they choose a combination of these options.

#1 isn't a great option because it limits growth to organic sources and usually doesn't lead to a lower cost of capital. #2 is a bad option because it progressively increases the overall risk of the portfolio. #3 is a bad option because it probably doesn't generate any growth in AFFO per share. Lastly, #4 often turns out to be a bad option because it also progressively increases the overall risk of the portfolio. #5 is a bad option because it increases leverage, which usually weighs on market sentiment and reinforces a low valuation.

This isn't mere conjecture or spurious logic.

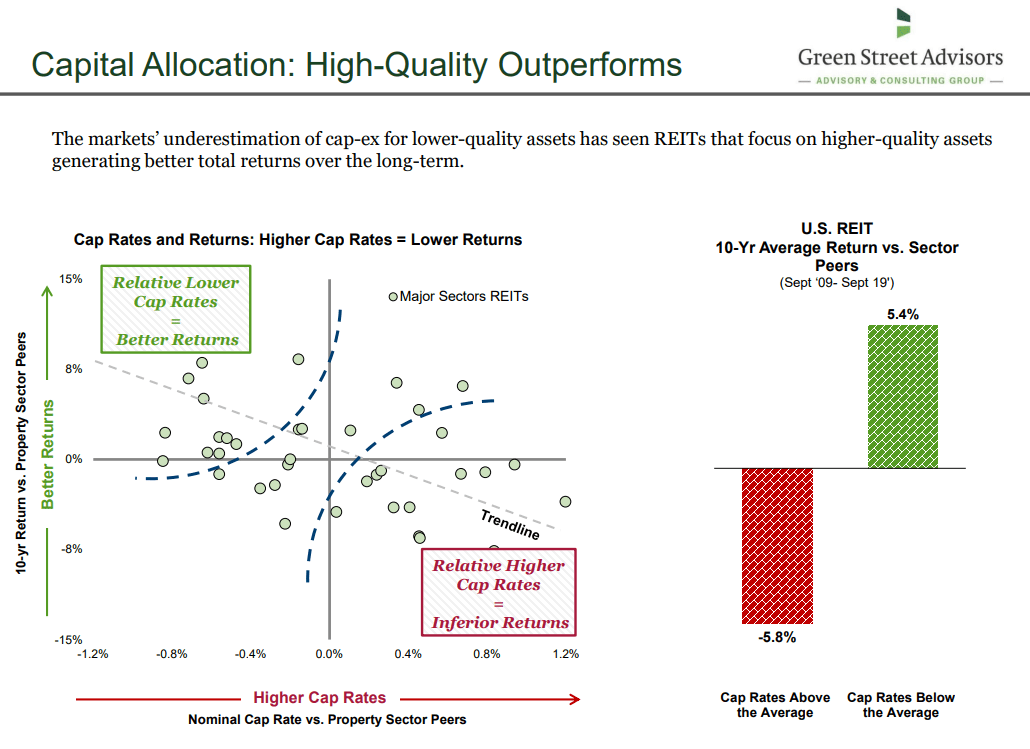

Green Street Advisors looked at US REITs for the decade between 2009 and 2019 and found that REITs focused on higher-quality properties with lower cap rates (investment yields) performed better than REITs focused on higher-yielding but lower quality properties.

{kind=link}

Why? Two reasons:

- High-quality properties enjoy more market rent growth over time.

- Capital expenditures for low-quality properties are consistently higher due to vacancies, required upgrades, maintenance issues, etc.

Of course, another option REITs have is to cut their dividend in order to free up cash for investment, but this has the negative effect of reinforcing the market's view of them as a low-quality REIT. In fact, dividend cuts usually lead to an even lower cost of capital.

This is how the " Vicious Cycle " works.

- Negative market sentiment >>> impaired cost of capital >>> lower investment quality and/or returns >>> more negative market sentiment >>> more impaired cost of capital >>> even lower investment quality and/or returns

The " Virtuous Cycle " works the same way but in the opposite direction.

- Positive market sentiment >>> strong cost of capital >>> higher investment quality and/or returns >>> more positive market sentiment >>> stronger cost of capital >>> even higher investment quality and/or returns

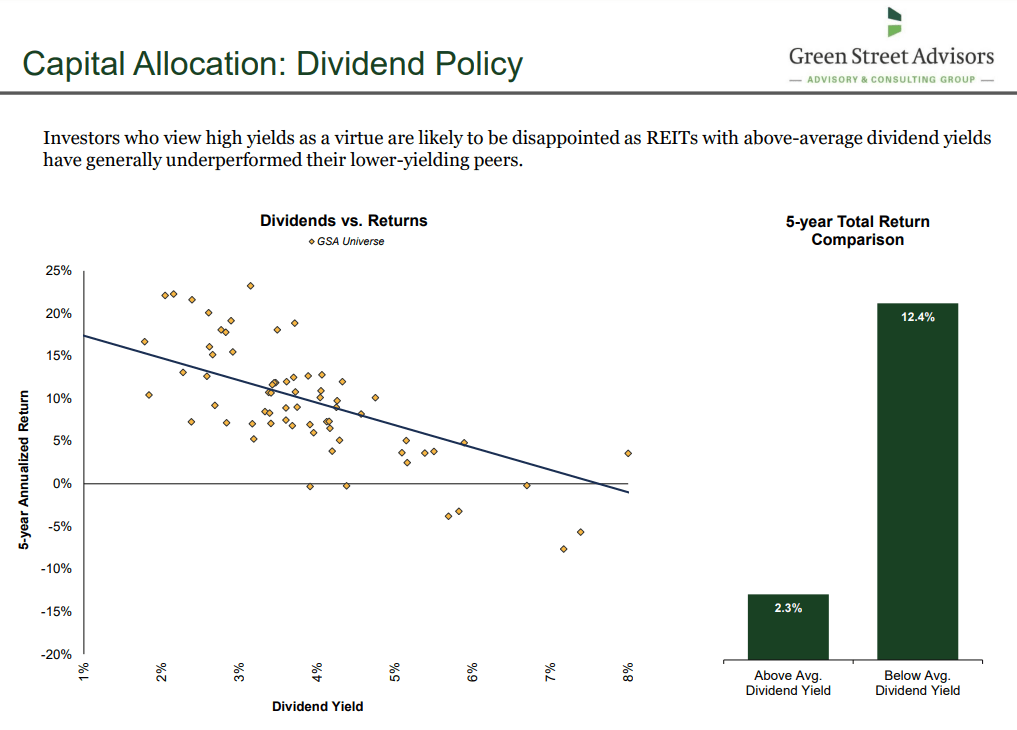

Again, this is not merely conjecture or an interesting thought experiment. This is an observed phenomenon. Low-yielding REITs tend to outperform high-yielding REITs over multi-year time periods.

{kind=link}

There is both a correlative and a causative relationship here.

The market prices lower-quality REITs at a lower valuation (and thus higher yield), hence a correlation between high-yield and less quality/growth.

But that lower valuation, in turn, translates into a higher cost of capital, hence the causation between high-yield and lower quality/growth.

This relationship holds whether interest rates are high or low.

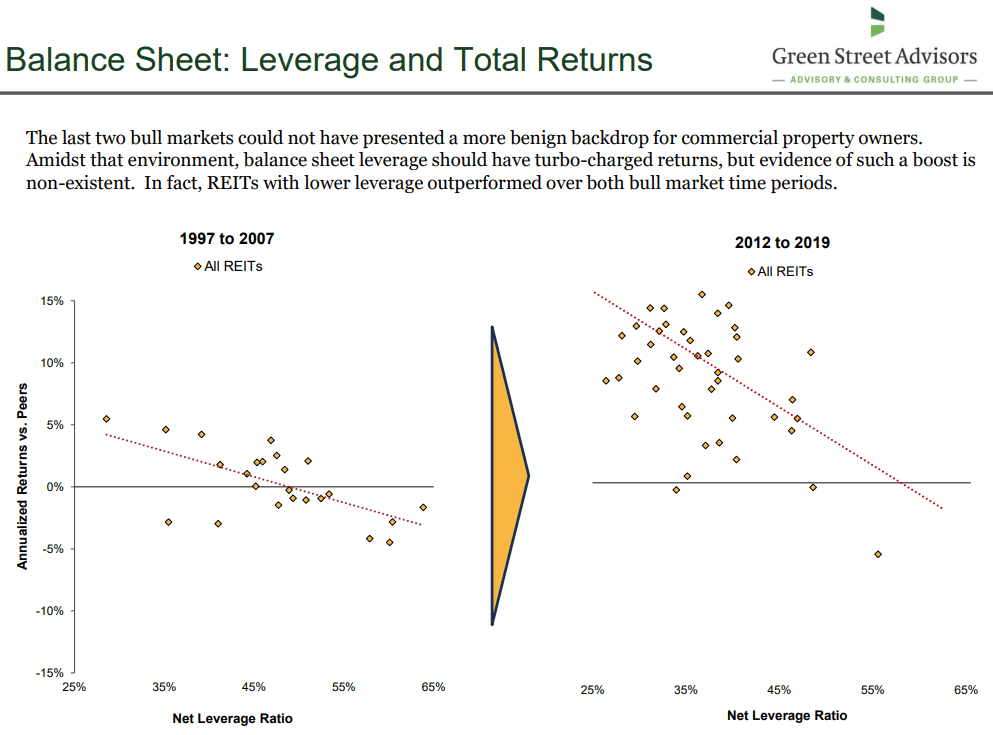

One might think that, during a period of low interest rates, a REIT with high leverage and a weak balance sheet would outperform a peer REIT with low leverage and a strong balance sheet. Not so!

Green Street found that during the 2010s period of low interest rates, REITs generally performed better than they did during the decade of relatively higher interest rates from 1997 to 2007. But during both periods, lower leveraged REITs tended to outperform higher leveraged REITs.

{kind=link}

There are exceptions, of course. There are always exceptions. But this general rule applies more often than not.

"Expensive," low-yielding, low-leveraged REITs that invest in high-quality properties tend to attain the Virtuous Cycle and outperform over long periods of time.

Meanwhile, "cheap," high-yielding, highly leveraged REITs that invest in lower quality properties tend to fall into the Vicious Cycle and underperform.

Net Lease REIT Practicum

We turn now from theory to practice.

The net lease space is both my wheelhouse and a perfect way to illustrate the above line of reasoning. That is because net leases are long contracts, typically with 10-20 year initial periods as well as some 5-year option periods afterward. Rents are contractually fixed for the duration of the lease, often but not always including predetermined rent escalations every year or five years.

The cash yield on investment for a net lease property is very predictable even many years into the future, which makes it important to match this cash yield with a sustainably lower cost of capital.

NNN REIT ( NNN ), formerly called National Retail Properties, is the poster child for conservative financial management and duration-matching its investment yields with its cost of capital.

NNN's weighted average debt maturity is around 12 years at a weighted average interest rate of 3.8%, while its weighted average lease duration is around 10 years.

Alexandria Real Estate Equities ( ARE ) is another high-quality REIT that is classified in the "healthcare" subsector but primarily employs net leases. It also employs highly conservative financial management, boasting a weighted average debt maturity of around 13 years and a weighted average lease duration of 7 years.

Aside from duration-matching, the spread between cost of capital and investment yields is all-important for net lease REITs.

When a net lease REIT loses its formerly strong cost of capital and can't quickly get it back, the Vicious Cycle begins.

The Vereit Example

This happened during the 2010s with the former Vereit, the renamed version of American Realty Capital Properties that committed securities/accounting fraud in 2014.

In the early 2010s, ARCP had a decent cost of capital through the combination of CEO Nick Schorsch's sheer marketing prowess and an aggressive use of leverage. The REIT acquired tons of low-quality real estate during those years, increasing its exposure to casual dining restaurants (including Red Lobster) to over 20%.

When the new CEO, Glenn Rufrano, came in, he reconstituted the board, worked tirelessly to deleverage the balance sheet, pruned and upgraded the quality of the portfolio, all while bleeding cash from a litany of settlement payments associated with the ARCP fraud lawsuits.

But, as I explained in " A Eulogy For Vereit ," the REIT never regained its formerly decent cost of capital after losing the market's confidence.

Vereit's stock price never reached the heights enjoyed during Schorsch's reign. Constant portfolio rightsizing for the sake of deleveraging shrank AFFO per share and prevented the stock price from taking off.

The shadow of ARCP persistently loomed over Vereit, and a bad taste lingered in investors' mouths. The REIT has traded at a significant discount to its peer group since 2014.

From 2015 through the announcement of Realty Income's ( O ) acquisition of Vereit in 2021, Vereit never returned to sustained growth, and its stock price remained rangebound.

YCharts, Author's Modification

It was caught in the Vicious Cycle.

To again quote myself:

Here's a sobering fact: at the peak of Schorsch's empire-building days, ARCP shares traded for over $89 on a split-adjusted basis, almost double the acquisition value of Vereit.

Rufrano arguably took all the right steps to regain the market's trust and work back to a decent cost of capital. It didn't work. I held Vereit all the way up until its acquisition, thinking that the market would eventually recognize and reward good behavior. Looking back, however, I doubt it ever would have.

The Spirit Realty Capital Example

Almost the same story could be told about Spirit Realty Capital ( SRC ), albeit with different details.

From the time SRC IPO'd in 2012 through 2015 (and for a portion of 2016), SRC enjoyed a decent cost of capital, being able to accretively issue equity, at least at times. But the market increasingly worried about some of SRC's weaker tenants, especially the largest tenant of (now bankrupt) Shopko. In early 2017, management revealed that a number of retail and restaurant tenants had paid zero rent so far that year.

The former CEO stepped down, and the board installed investment banker Jackson Hsieh as the new head honcho.

Hsieh had a solid plan to improve the quality of SRC's portfolio and balance sheet and regain the market's trust. In 2019, amid a robust REIT rally, it looked like SRC might actually pull itself out of the Vicious Cycle. The REIT spun off its weaker properties into the "Spirit MTA REIT" and subsequently sold the vehicle to another REIT that had (and still has) absolutely no quality controls.

Things looked up for this newly refashioned net lease REIT. It still traded at a discount to peers in 2019, but it was gradually closing the valuation gap.

Then COVID-19 hit.

SRC's AFFO per share grew, but its share price didn't return to its average levels during the 2012-2016 era. Thus, despite a credit upgrade and well-constructed balance sheet, its cost of equity remained stubbornly high, dragging up its overall WACC.

SRC chose to pursue growth largely through capital recycling, selling its higher quality and lower-yielding properties to buy lower quality but higher-yielding properties. On the rare occasions that SRC issued equity, it wasn't at a particularly low cost of equity. The REIT went progressively up the risk curve to find properties with high enough yields to be accretive to AFFO per share.

This reinforced the market's perception of SRC as a low-quality REIT.

SRC couldn't break out of the Vicious Cycle after all.

That's why I eventually threw in the towel. I explained this in " Why I Sold Spirit Realty And Reinvested In Spirit Realty's Preferred Stock ."

At some point, Jackson Hsieh could see the writing on the wall and hopped on the phone with Sumit Roy, Realty Income's CEO. O inked a stock-for-stock acquisition agreement with SRC in late 2023.

O seems to have become the designated final destination for net lease REITs with an impaired cost of capital.

The Agree Realty Example

I know of only one net lease REIT that has eventually recovered from an impaired cost of capital: Agree Realty Corporation ( ADC ).

In the aftermath of the Great Financial Crisis in 2010-2011, ADC's largest tenant, the bookstore Borders, went bankrupt. This spurred the REIT to cut its dividend and rapidly divest of its Borders properties while expanding and diversifying the portfolio. Then-current CEO Richard Agree, a developer at heart, brought in his son Joey to lead the transformation of ADC from a development-focused REIT to one oriented around growth from external acquisitions.

In 2010-2011, ADC languished with a price to FFO of 9-12x. During this same timeframe, O's price to FFO rose from around 14x up to a peak of about 18x.

But the market eventually recognized and rewarded ADC's relentless commitment to portfolio and balance sheet quality. The REIT's cost of equity rose to roughly par with that of O in the pre-COVID years, and today ADC enjoys a slightly stronger (lower) cost of equity:

| 2023 AFFO Yield |

| ADC |

| 6.3% |

| O |

| 6.8% |

While this half-point difference in AFFO yield may not seem like much, it marks a new era for ADC as the cost of capital leader in the net lease space.

Essential Properties Realty Trust (EPRT) comes in a close second with its 6.4% 2023 AFFO yield, but ADC leads the pack on both the cost of equity side and the cost of debt side.

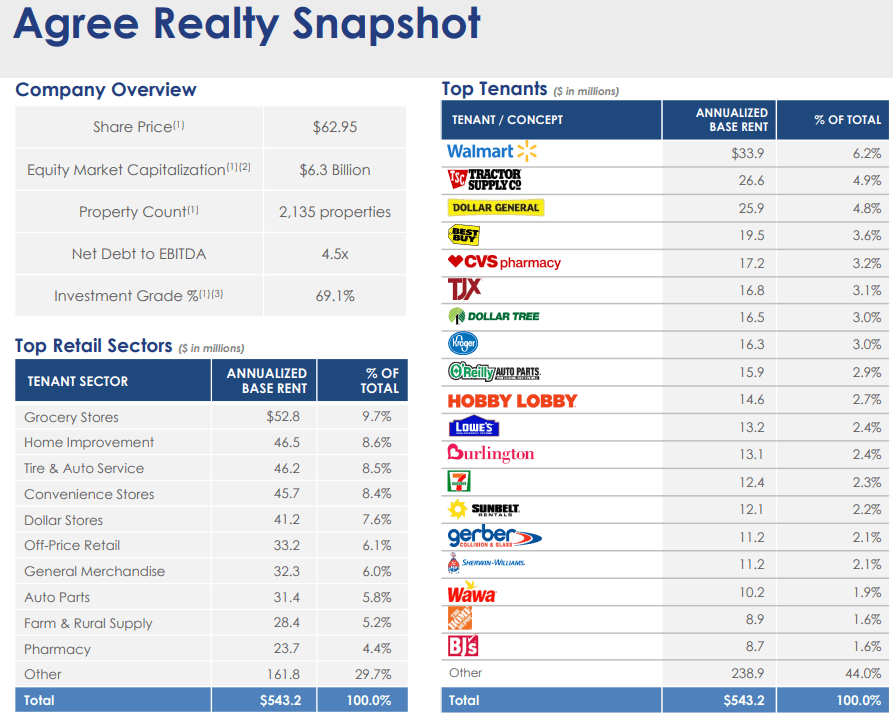

While ADC has only strengthened its portfolio quality with best-in-class retailers in recent years...

{kind=link}

...O's gargantuan size has forced it to throw open its investment criteria in search of adequate-sized investment opportunities.

My fear is that O's veering into investments in casinos, vertical farming, data centers, and all sorts of other assets outside of its traditional wheelhouse will further erode its historical cost of capital advantage. I think the market fears this as well, which may perhaps be why O has slipped out of its status as the net lease cost of capital leader.

It may also be why ADC has outperformed over the last 7 years (and any period of time you want to measure over the last decade).

ADC remains solidly in the Virtuous Cycle, while O appears to be slipping away from it.

Some of My Favorite "Expensive" REITs

I should note at this point that there is such a thing as overpaying for a REIT, even a high-quality one. I'm not advocating throwing out all buying discipline and simply buying the most richly valued REITs you can find.

Even high-quality REITs and cost of capital leaders see their relative valuations ebb and flow. There are still relatively less expensive times to buy their shares.

For example, while ADC is the cost of capital leader in the net lease space, that doesn't mean it isn't cheap relative to its own valuation history. Here's price to cash from operations, directionally the same as its historical price to AFFO:

ADC is cheaper today as measured against its cash flow than it has been for most of the last decade.

There are other REITs like ADC with a moderate dividend yield and a cost of capital advantage.

Here are some of my favorites.

| Dividend Yield |

| Price/AFFO |

| 2023 AFFO Yield |

| Agree Realty ( ADC ) |

| 4.7% |

| 15.9x |

| 6.3% |

| American Homes 4 Rent ( AMH ) |

| 2.5% |

| 21.7x |

| 4.6% |

| Alexandria Real Estate ( ARE ) |

| 4.0% |

| 14.1x |

| 7.1% |

| Extra Space Storage ( EXR ) |

| 4.3% |

| 18.7x |

| 5.3% |

| EastGroup Properties ( EGP ) |

| 2.8% |

| 28.0x |

| 3.6% |

| InvenTrust Properties ( IVT ) |

| 3.4% |

| 15.5x |

| 6.5% |

| Mid-America Apartment Communities ( MAA ) |

| 4.4% |

| 16.3x |

| 6.1% |

| Rexford Industrial Realty ( REXR ) |

| 2.8% |

| 25.4x |

| 3.9% |

| VICI Properties ( VICI ) |

| 5.3% |

| 14.5x |

| 6.9% |

Some of these REITs are temporarily wounded with valuations that are not amenable to accretive acquisitions of their target property types.

For example, ARE has gotten caught up in the office REIT selloff because it gets wrongfully lumped in as a traditional office landlord despite trafficking only in Class A life science lab space in top-tier R&D hubs.

MAA's valuation has slumped because of the magnitude of new apartment supply coming to market in its Sunbelt markets. But new construction has dropped off a cliff, setting up for a far more favorable supply-demand environment in 2025-2026.

Finally, VICI's valuation may not look terribly low, but it does trade at a premium to its sole casino REIT competitor of Gaming and Leisure Properties (GLPI). The latter's price to 2023 AFFO is 12.7x, and its 2023 AFFO yield is 7.9%. GLPI does not have the cost of capital to match a bid from VICI on any given property they may both be interested in.

Bottom Line

There's nothing wrong with seeking out high-income investments, and there are places to look for safe yield in the market.

But I would argue that, when it comes to investing in REIT common stocks, you are far better off hunting for quality , not yield .

Sometimes you'll be able to find those hidden gems that offer both quality and yield, but more often than not, you'll end up with a stinker caught in the Vicious Cycle of declining quality, perpetually high cost of capital, and eventually, dividend cuts.

Anyone wishing to invest in REITs for dividend growth or total returns would do well to seek out those high-quality REITs that enjoy the Virtuous Cycle of rising quality, perpetually low cost of capital, and dividend raises.

Yes, they may look "expensive" at first blush, but this means they also enjoy a strong cost of capital with which to go out and buy the highest quality real estate on your behalf.

Life is just too short to settle for mediocrity.

For further details see:

The Virtuous Cycle: Why I Love 'Expensive' REITs