WEN - The Wendy's Company: Scaled Market Penetration Drives Systemwide Sales Growth

2023-05-19 05:13:59 ET

Summary

- Over the past year, Wendy's (WEN: +32.92%) has experienced superior share price growth to both the general market (SPY: +1.69%) and the restaurant industry (EATZ: +15.68%).

- While the impressive growth of both Wendy's and the restaurant industry reflects the broader COVID recovery theme, unlike most of the industry, Wendy's has seen record revenues.

- This is in line with the firm's aim of growth and scale at all costs, with a tripartite strategy of expanding the firm's footprint, digital acceleration, and supporting SRS momentum.

- The firm also retains a disciplined capital deployment strategy, enabling resilience and reducing risk of poor investment.

- Combined with a general undervaluation, I believe WEN stock is a 'buy'.

Wendy's ( WEN ) is an Ohio-based global fast-food restaurant franchiser with operations concentrated on burgers, sandwiches, milkshakes, and more. As of 2023, there are 5,994 Wendy's restaurants in the US and 1,101 across 31 foreign countries.

These activities have enabled TTM revenues to approach $2.14bn and a net income of $179.79mn, alongside a free cash flow of $206.61mn. The firm additionally pays out an annualized dividend yield of 2.21%.

Introduction

The Wendy's Company has developed a restaurant model focusing on three primary strategies to enable scale and margin growth; building same-restaurant sales momentum; promoting the digital acceleration and access; and expanding the footprint of the company at all levels.

{kind=link}

The company principally derives revenue from two sources; sales at company-operated restaurants and royalties, fees, and advertising fund collections from franchised restaurants. Additionally, Wendy's segments its sales between its American operations, international operations, and global real estate and development portfolios.

Valuation & Financials

General Overview

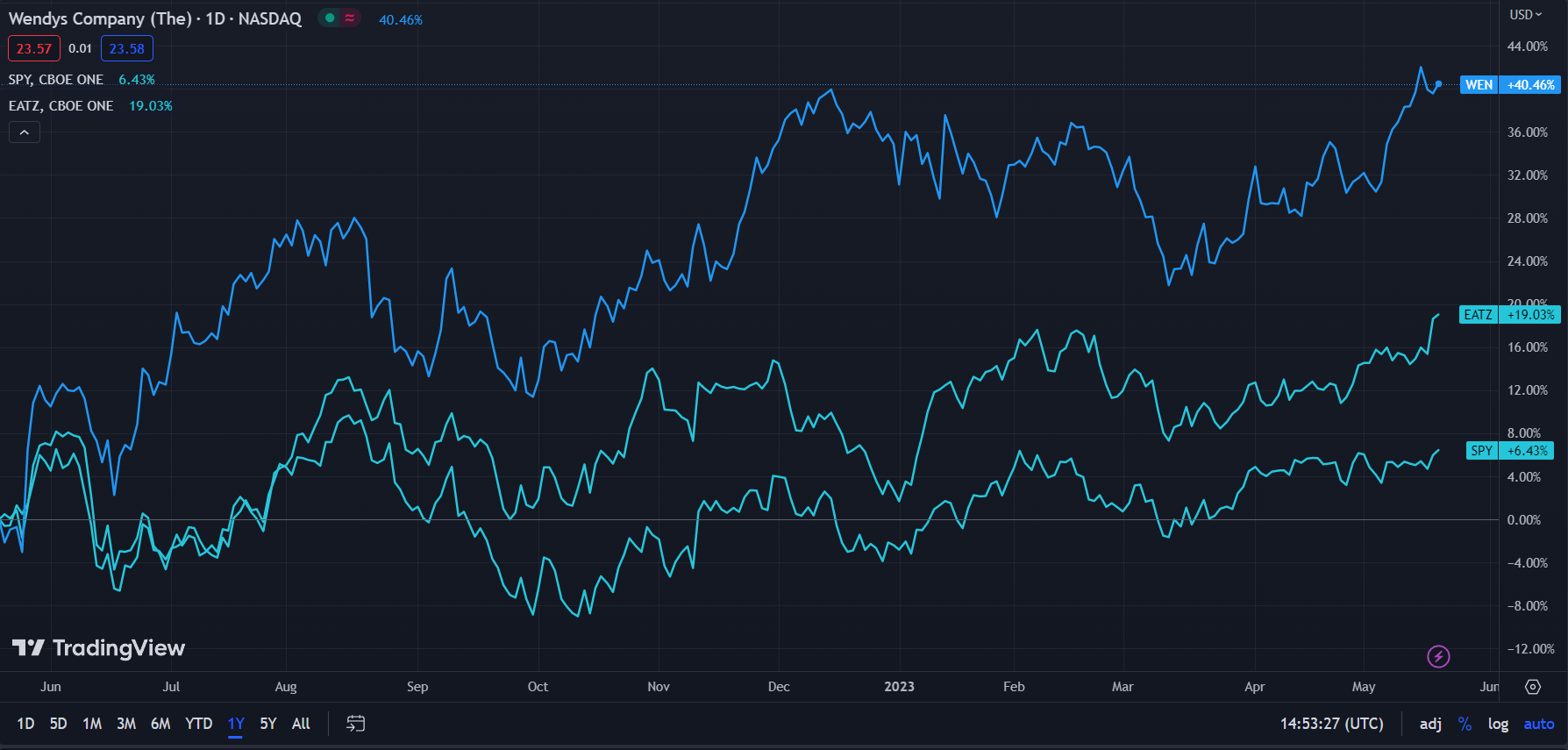

In the TTM period, Wendy's - up 40.46% - has experienced greater stock price growth than both the broad market, represented by the S&P 500 ( SPY )- up 6.43%, and the restaurant industry ( EATZ )- up 19.03%.

{kind=link}

This growth recovery reflects the conclusion of the COVID-recovery theme as well as material reductions in inflationary pressures, much less pervasive than a year prior.

On the other hand, WEN stock's superior price performance represents its chronic undervaluation and the company's operational advantages.

Comparable Companies

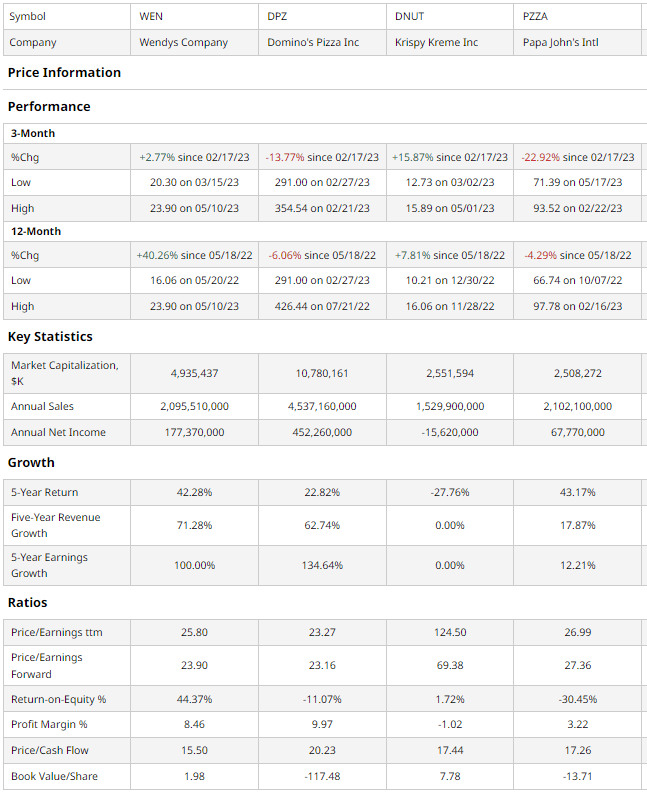

The restaurant industry remains one of the industries with the highest levels of competitive intensity, from mega-cap leaders such as McDonald's ( MCD ) to various mom-and-pop shops. As such the best comparable peers for Wendy's are mid-cap firms with similar operational capacities, rather than firms with similar offerings, as they can range wildly in size. Such companies with similar size to Wendy's include; Domino's Pizza ( DPZ ), the world's largest pizza chain; Krispy Kreme ( DNUT ), a premier donut firm; and Papa John's International ( PZZA ), a pizza chain with nearly identical revenue levels to Wendy's.

{kind=link}

As demonstrated above, Wendy's has experienced markedly greater 1Y share price growth than all peers and the second-best quarterly price growth. This emphasizes that, in spite of recent rallies, Wendy's remains a value company, with future growth not yet fully priced in.

This is further expanded upon by Wendy's multiples, maintaining the second-best trailing and forward P/Es and book value per share while sustaining the lowest price/cash flow.

Additionally, Wendy's ability to make prudent investments for forward growth is exemplified by its 44.37% ROE, by far the best of all peers, and the company's rapid scale growth, with the fastest revenue growth of all firms. And Wendy's has not neglected margin growth either; the firm has experienced the second-best earnings growth alongside its revenue growth.

Valuation

According to my discounted cash flow analysis, the fair value of Wendy's, at its base case, is $27.06, meaning that the stock's current price of $23.53 is undervalued by 13%.

For my DCF, I assume a discount rate of 9%, in line with the company's relatively high debt/assets of 0.78 and the higher cost of capital as necessitated by interest rate hikes. I additionally assume lower revenue growth and SRS due to combined slowed growth in consumer spending and upward pressure on wages.

{kind=link}

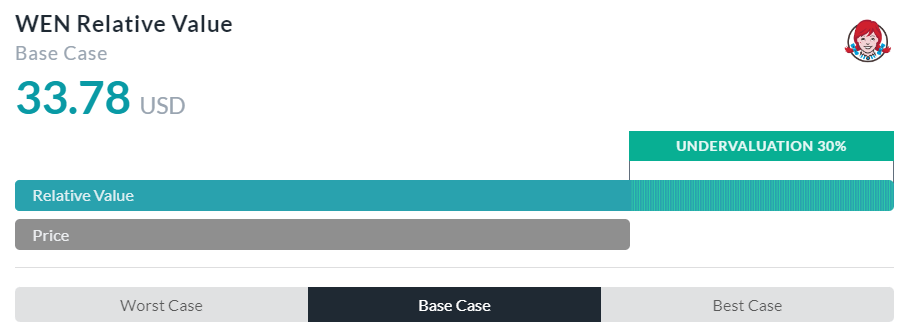

AlphaSpread's multiples-based relative valuation tool more than supports my theory of undervaluation, calculating, at its base case, an undervaluation of 30%, making the true value of the stock $33.78.

Thus taking an average figure between my DCF and AlphaSpread's relative valuation tool, the fair market price for Wendy's is $30.42, with the stock currently undervalued by 21.5%.

Three-Pronged Strategy Centres Around Scale & Margin Expansion

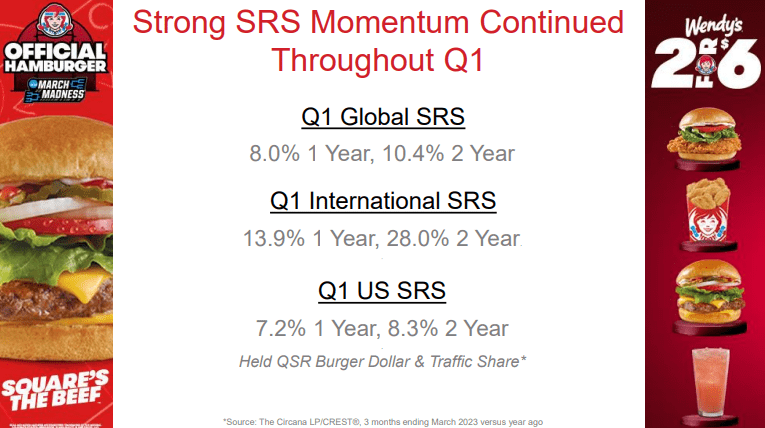

As discussed in the introduction, Wendy's has simplified its strategy around the pillars of scale and margin growth, driven by the three-pronged strategy of continued SRS momentum, greater digital acceleration, and an expanded footprint. Wendy's has mastered the achievement of the first of those objectives, recording 2Y Q1'23 Global SRS of 10.4%, 2Y Q1'23 International SRS of 28.0%, and 2Y Q1'23 US SRS of 8.3%. Such sales have been further driven by Wendy's partnerships, such as becoming the 'official hamburger' for March Madness or value deals such as its '2-for-6' deal.

{kind=link}

The company plans to sustain this SRS momentum through the promotion of products at various price points, properly executing breakfast promotion, and driving late-night business through media deals and social presence.

Regarding its social presence, Wendy's maintains upwards of 3.8mn Twitter followers, close to McDonald's' 4.2mn, a much larger company.

And above all else, to foster scale growth, Wendy's has focused on expanding its physical footprint. While Wendy's has increased its store count, the company has additionally invested in hundreds of 'ghost kitchens', with leaner cost structures and larger margins. Said ghost kitchens leverage the growth of online delivery TAM, which has only grown with the pressures of COVID-19.

4 Reasons Ghost Kitchens Will Succeed in the New Normal (BentoBox)

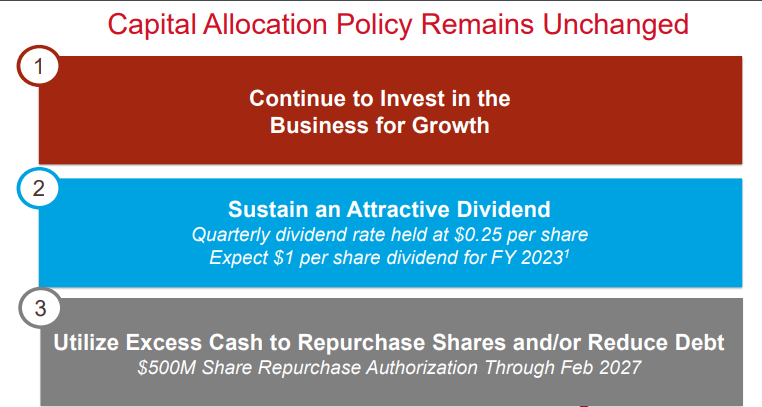

To adequately return this growth to shareholders and ensure a continuation of it, Wendy's sustains a disciplined capital allocation strategy, primarily concentrated upon consistent organic growth, then the maintenance of an attractive dividend- aimed at $1/share for FY23, and the utilization of excess cash flows to opportunistically repurchase shares and reduce debt levels.

{kind=link}

Wall Street Consensus

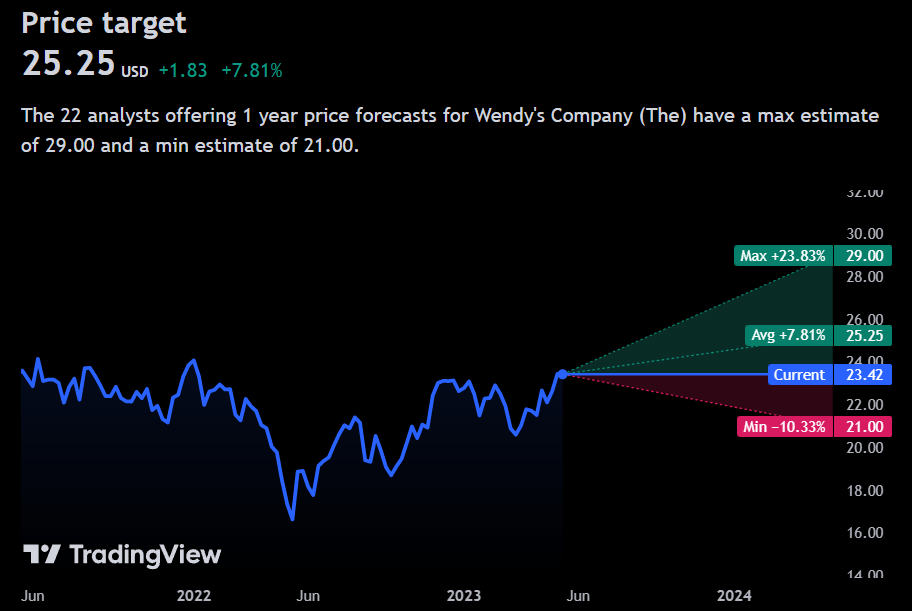

Analysts largely support my positive outlook on Wendy's, projecting an average one-year price increase of 7.77%, to a price of $25.25.

{kind=link}

At the minimum projected price level, however, analysts predict a decline of -10.33% to a price of $21.00. The latter is likely an assessment of analyst anxieties about the worst-case resurgence of inflation or excessive recessionary pressure due to macro headwinds.

Risks & Challenges

High-Levels of Competitive Intensity

The restaurant industry is fragmented at every level, with mega-caps, mid-caps like Wendy's, and small businesses each controlling small segments of the market. As such, Wendy's faces constant downward margin pressure in order to compete with this pressure adequately, and temporary headwinds can lead to permanent loss of market share.

Compressed Discretionary Consumer Spending

With continuous inflationary pressures and increases in interest rates leading to potential recessionary headwinds, consumers are facing a double crisis with the consequence of reductions in consumer sentiment and, by extension, discretionary spending. As such, depressed consumer demand may hinder Wendy's scale growth prospects and materially reduce SRS and overall revenues.

Dependence on Reputation and Perception of Brand

Wendy's has been able to reduce dependence on traditional marketing and advertising with the success of its social media campaigns. However, the success and demand for the company's products still hinge upon its perception, and poor marketing may lead to reductions in demand and subsequent cash flows.

Conclusion

In the short term, I expect Wendy's to revert to fair value and to continue posting scale growth.

In the long term, I project this scale growth will be met with margin growth and Wendy's to become a leaner and more profitable firm.

For further details see:

The Wendy's Company: Scaled Market Penetration Drives Systemwide Sales Growth