XLU - There Are CEF Premiums To NAV And Then There Is GUT At 107%

Summary

- Gabelli Utility Trust is a closed-end fund focused on utilities.

- GUT is now trading at an all-time high premium to NAV of 107%.

- Never in the fund's history has the market value of its shares been this high versus the market value of its assets.

- We feel both the underlying sector (Utilities) and the premium to NAV for GUT are overbought.

Thesis

Gabelli Utility Trust ( GUT ) is a closed end fund focused on utilities. As per its literature:

The Fund's primary investment objective is long term growth of capital and income. The Fund will invest 80% of its assets, under normal market conditions, in common stocks and other securities of foreign and domestic companies involved in providing products, services, or equipment for (i) the generation or distribution of electricity, gas, and water and (ii) telecommunications services or infrastructure operations.

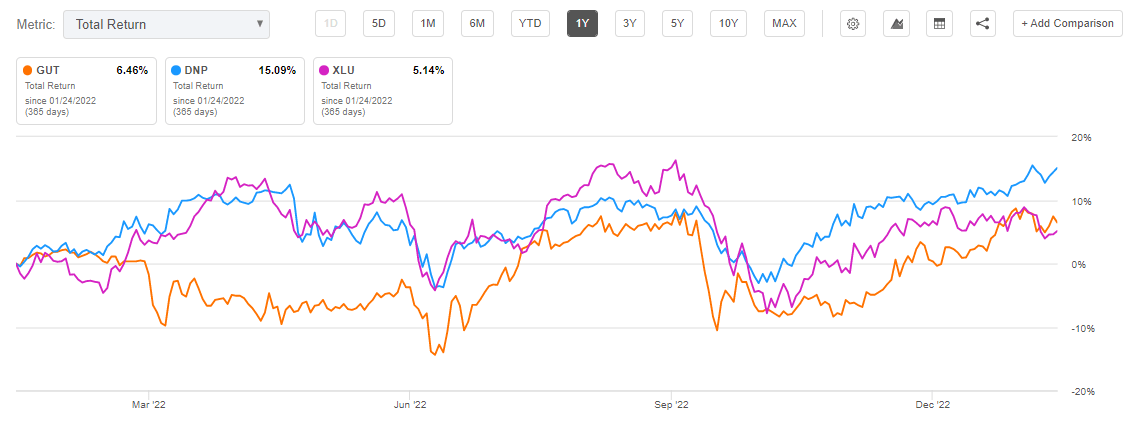

It is no secret the Utilities sector is a defensive one, that has fared particularly well in the past year on the back of market participants moving into defensive assets. This shift has resulted in GUT posting a positive performance on a 1-year trailing period, with its total return in excess of +6%. The CEF's total return is in line with what we have seen from the Utilities Select Sector SPDR Fund ( XLU ), but trails the results of another premier Utilities CEF, namely DNP Select Income Fund Inc ( DNP ) which came in at +15%.

Let us just set the stage here - GUT is a very good fund with an enviable track record in a defensive sector of the equity market. The CEF has successfully managed to transform equity market returns into dividends in the past decade and has been rewarded handsomely by shareholders. However, there are limits and overbought conditions in any financial asset, and we are observing such a situation for GUT. Just think about the following for a second:

- GUT is trading at a historic high premium to NAV of 107%

- Never in the fund's history has the market value of its shares been this high versus the market value of its assets

- If GUT were to liquidate today, investors would only get 50 cents/$ for what they currently own

- If you buy outright the top ten holdings in the fund, you can replicate to a large extent GUT's performance at only half the cost

- You are not only paying management fees here, but actually another 100% of net asset value for having your money managed by Gabelli

The current set-up is just untenable, with only downside in our minds here. There is substantial downside from the fund's premium to NAV reverting to a more palatable historic norm, and there is substantial downside from the asset class itself, which is currently overvalued:

P/E Ratio (Yardeni)

GUT simply takes Utilities equities and transforms them into dividends. When Utilities are overvalued fundamentally, GUT is in the same position. As we can see from the graph above, courtesy of Yardeni, the Utilities sector displays one of the highest P/E ratio observed in the past 20 years. This P/E ratio is not sustainable either.

Premium/Discount to NAV

GUT is now trading at an all-time high premium to NAV of 107%:

Looking back on a decade long basis, we can see the CEF is now trading at an astounding 107% premium to NAV! We have benchmarked the fund versus DNP, another well-known name in the sector, and we can see both vehicles having large premiums, but GUT dwarfs DNP.

Historic high premiums to NAV do not tend to last very long. We can see wild swings in the fund's premium in the past year:

We can see how the premium to NAV can swing by 10% to 20% during the course of a year, with a substantial drawdown in April / May 2022. The move is generally correlated with wider markets risk-off sentiment.

Performance

The fund is up on a 1-year basis, but has lagged DNP:

{kind=link}

We can also see from the total return graph above that GUT has experienced a much wider draw-down in 2022 when compared to the wider Utilities sector and to DNP. This means that a substantial part of the move in GUT is driven by its premium during volatile years.

Holdings

The fund contains well-known names in the Utilities space:

Top Holdings (Fund Website)

The CEF's build is a classic one for this sector, with no systemic issues to point out:

Top Sectors (CEFConnect)

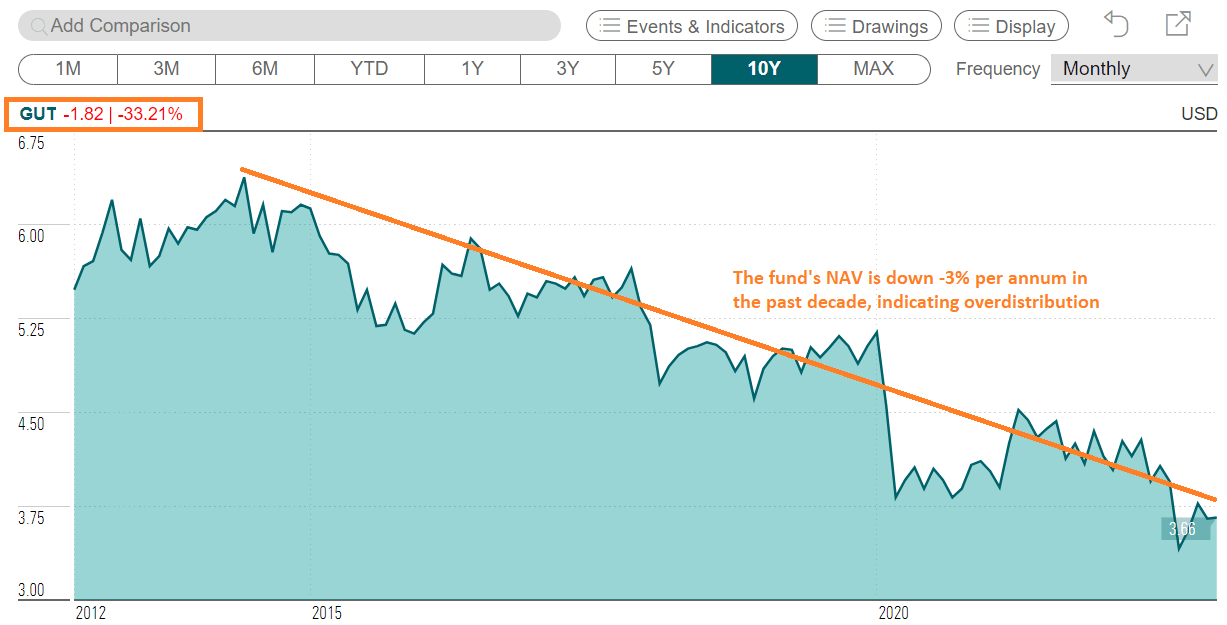

NAV Performance

Despite its ballooning premium to NAV, the fund's net asset value displays a worrying performance:

{kind=link}

We can see from the above graph, courtesy of CEFConnect, that GUT's NAV is actually down -33% in the past decade. We like to see stable NAVs for well-run CEFs, indicating that the fund distribution is supported.

The CEF was able to post a robust total return performance on the back of higher premiums to NAV, when in fact, fundamentally the vehicle shed value via a decreasing pool of assets.

Conclusion

GUT is a Utilities CEF with an enviable track record. The fund has been very successful in the past decade, posting robust performances with shallow drawdowns. The CEF has been rewarded by shareholders, which have bid up the market value of the CEF's shares versus its NAV throughout time. Currently, the premium to NAV is at a historic high level of 107%. Never in the fund's history has such a discrepancy been recorded. Coupled with overbought conditions in the underlying asset class (i.e. Utilities), we feel there is only downside from here for GUT. Despite its ever increasing premium to NAV, the CEF has not managed a stable NAV, witnessing a -33% decrease in net asset value in the past ten years. This is symptomatic of a fund over-distributing (i.e. unsupported yield). Just like the FAANG cohort, which is fundamentally sound, but got overbought in the 2020/2021 time-period, GUT will see its premium decrease from overbought levels on the back of a rotation out of defensive sectors into more aggressive ones as 2023 progresses.

For further details see:

There Are CEF Premiums To NAV, And Then There Is GUT At 107%