ACTV - This Is Another Ideal Jobs Report

2023-03-10 09:45:39 ET

Summary

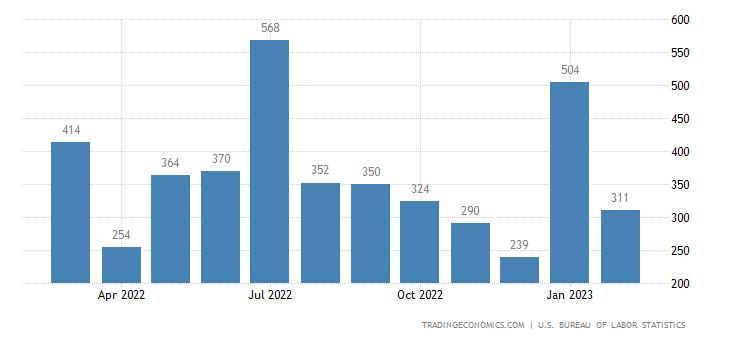

- The economy added another 311,000 jobs in February, but downward revisions lowered the net by 34,000.

- Wage growth fell short of expectations and the length of the workweek shortened, which are more important datapoints.

- We continue to see the best of both worlds as disinflation ensues, while the labor market remains healthy.

- This report should begin the process of reversing the selloff in risk assets that started a month ago.

The jobs report for February is the first of two pivotal data points that will likely determine whether the Fed continues with another 25-basis-point rate increase at its upcoming meeting or ratchets up the percentage to 50 basis points in what most view will be a higher terminal rate that lasts longer. The fear of a higher-for-longer terminal rate has elevated recessions fears, which is why we have seen longer-term interest rates fall this week, the yield curve further inverts, and stocks continue to correct from their February highs.

Markets have been repricing risk assets and raising expectations for short-term rates ever since last month's jobs report, which estimated that the economy added 517,000 jobs in January. Yet that jobs report and the stronger-than-expected economic data for January that followed were clearly influenced by several one-time factors, which included seasonal adjustments. The real economy was simply not that strong, and it has been my expectation that February's data would show more moderate growth, which should start to reverse the repricing or risk assets that took place over the past month and reduce rate-hike expectations. I think today's jobs report affirms that.

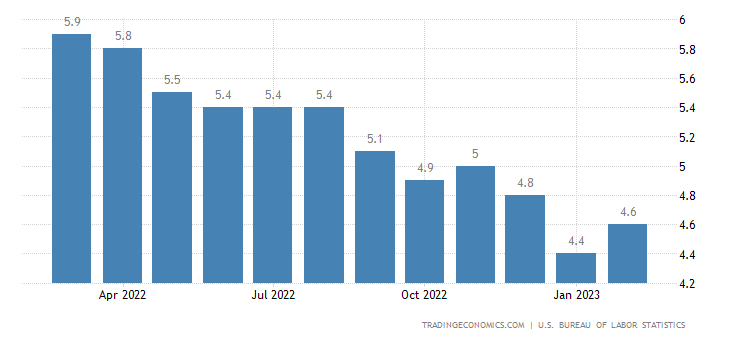

The economy added 311,000 jobs in February, which was modestly higher than expectations, but the prior two months saw downward revisions of 34,000. I expect we will see additional downward revisions, as the establishment survey always overestimates job growth at turning points in the economy. The leisure and hospitality sector continues to lead all sectors in creating jobs with a gain of 105,00 last month, while the unemployment rate rose from 3.4% to 3.6%.

{kind=link}

The quality of the jobs being created is far from spectacular, which is one reason we saw wage growth fall short of expectations at just 0.2% for the month. That results in a year-over-year growth rate of 4.6%, which was short of the 4.8% expected. Additionally, the length of the workweek fell by 0.1%. These two factors more than offset the modestly higher job numbers, which is exactly what the Fed wants to see. This report should take pressure off the Fed to raise interest rates any more than 25 basis points at its next meeting.

{kind=link}

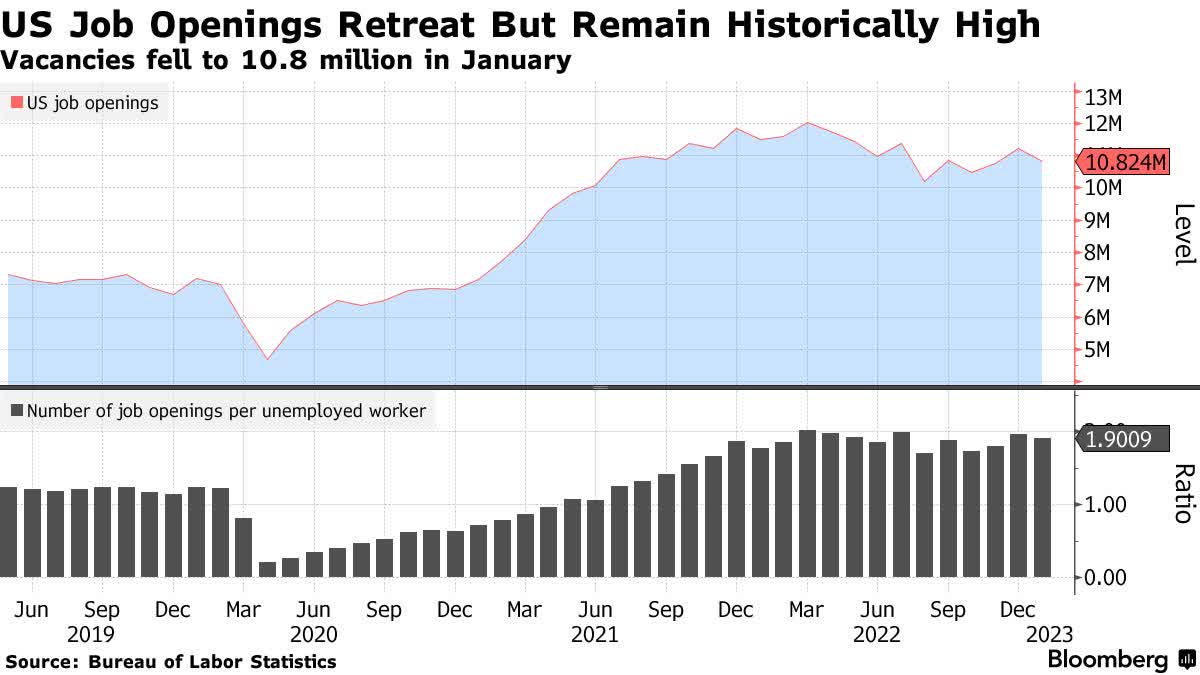

Job openings have been a top concern for the Fed, but vacancies fell by 410,000 in January, led by accommodation and food services companies (-204,000), which is where we have seen the strongest job growth.

{kind=link}

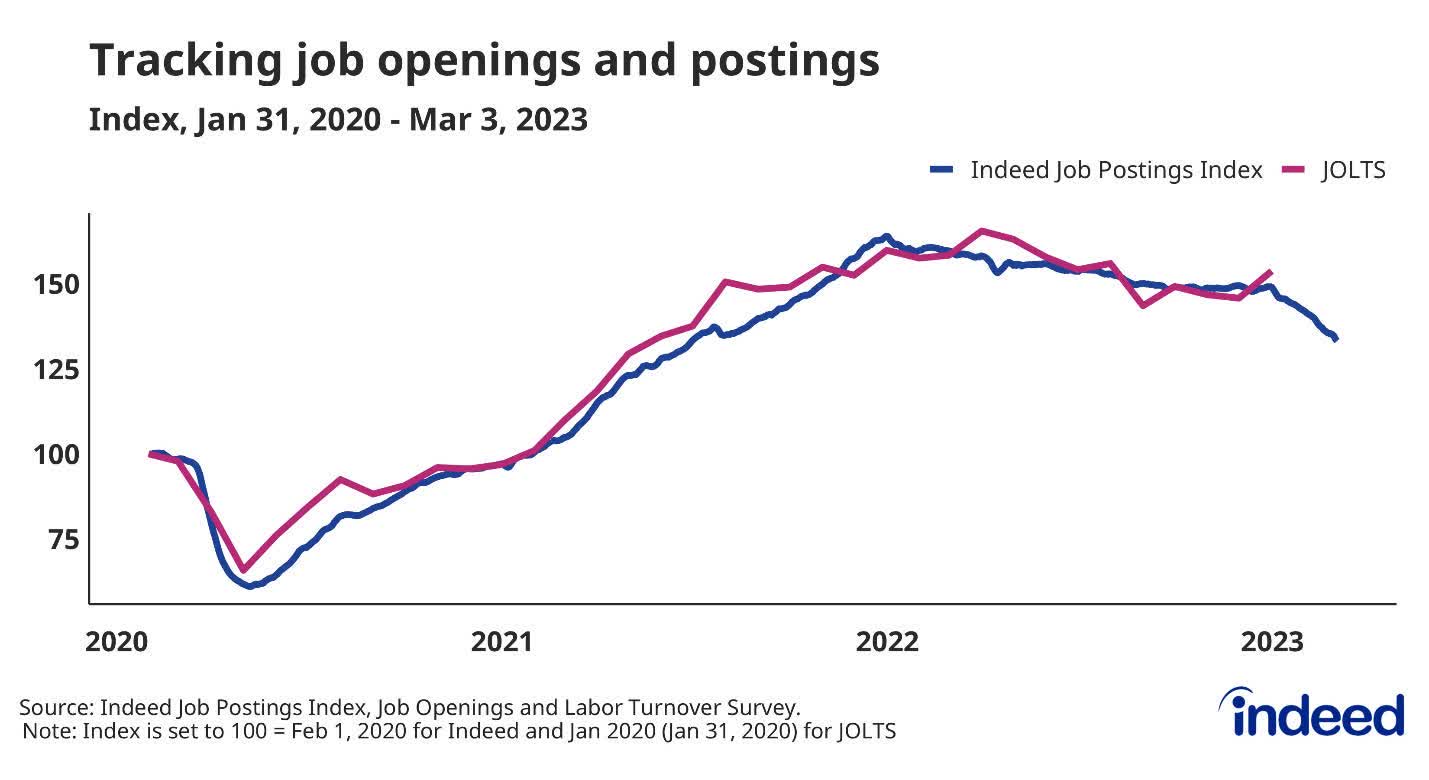

A more real-time indicator for job openings that closely tracks the government's JOLTS report is Indeed's Job Posting Index, which provides data through March 3. This index just posted a sharp decline in vacancies during February, which equates to approximately 9.9 million job openings in the JOLTS report. That would be a decline of over one million jobs in the first two months of the year, but we won't receive an update from JOLTS for February until early April. Fed officials should be paying closer attention to this real-time data to recognize that monetary policy tightening to date, which works with a significant lag, is having its intended impact.

{kind=link}

Additionally, the latest survey from Challenger, Gray & Christmas shows that layoffs for the first two months of this year are substantially above that of the past two years, with the total being the highest since 2009. The layoffs are not all coming from the technology sector, as all 30 industries tracked reported layoffs. Again, this is real-time data that refutes the strength in January's government reports.

Challenger, Gray, and Christmas

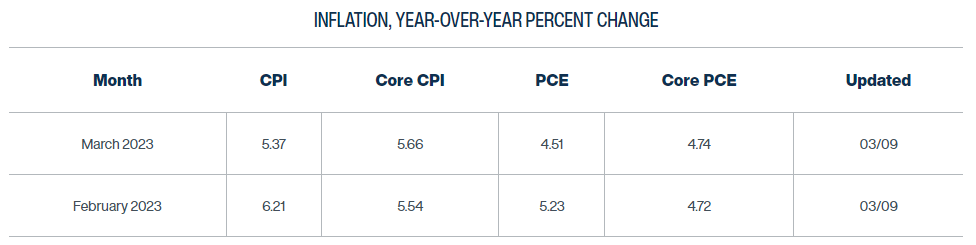

While Fed officials and investors debate the impact labor market strength and wage growth will have on the rate of inflation, the rate of inflation continues to edge lower month after month in a disinflationary period that began last summer. Chairman Powell finally acknowledged it for the first time last month, and January's anomaly of stronger economic statistics does not refute that fact. The Cleveland Fed's "nowcast" for the personal consumption expenditures (PCE) price index, which is the Fed's preferred method of measuring inflation, is expected to fall to 4.5% in March.

{kind=link}

That would be tremendous progress from the peak in June of last year at 7%, as can be seen in the disinflationary trend shown below. Are hawks and bears expecting this rate of fall to 2% overnight? It took 18 months to surge from 2% to 7%. The increase of five percentage points is on track to be cut in half after just nine months. Is it not more than reasonable to allow a full 18 months for it to fall to 2% again? This is happening despite a record-low unemployment rate, strong job growth, and healthy wage gains. It is also happening in advance of the labor market softening meaningfully, which will happen as the interest rate hikes to date have fully worked through the economy.

{kind=link}

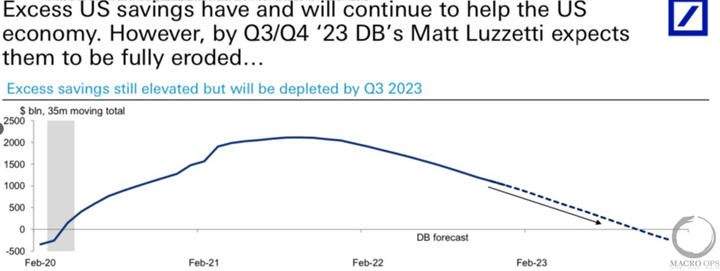

There is another factor, equally as important as jobs and wage growth, which has placed upward pressure on prices in the service sector. That is the tremendous build in post-pandemic excess savings, which is expected to gradually erode back to pre-pandemic levels during the second half of the year. This should temper the demand for services by consumers who have been spending in force at a growth rate just in excess of the rate of inflation. The timing should be perfect in order to see the PCE fall within a range of 2-3% by the end of this year. This factor should be taken into consideration alongside the rate hikes to date, which will both sap demand for goods and services this fall.

{kind=link}

Historically, the Fed has not paused its rate hikes until the Fed Funds rate is at or above the rate of inflation. With the PCE on track to fall below 5% in March, I think the terminal rate should and could ultimately end up being 5%, which would mean we have two more 25-basis-point rate increases ahead in March and May. That is a far cry from the consensus view right now, but there will be a lot of data between now and May, and I am focusing exclusively on the data and ignoring the rhetoric. The stock market should respond well to today's jobs report, as we begin to reverse the February pullback.

For further details see:

This Is Another Ideal Jobs Report