INDT - This Time Is Different

2023-03-14 09:00:00 ET

Summary

- Amid intensifying concerns over the potential fallout from several major tech-focused bank failures, this report examines high-level REIT fundamentals to chart the likely path forward for the real estate industry.

- Real estate equities have been slammed particularly hard as investors draw parallels to the early stages of the 2008 financial crisis when locked-up credit markets created a cascade of distress.

- Owing to the harsh lessons from the Great Financial Crisis, however, most REITs have been exceedingly conservative with their balance sheet and strategic decisions, ceding ground to higher-levered private-market players.

- With commercial property values now 15-20% below 2022 highs, and with interest rates doubling from last year, distress will become ever-apparent from private-market firms and lenders that pushed leverage limits. Most public REITs are prepared to weather the storm.

- With the exception of office, malls, and some sub-sectors of healthcare and mortgage REITs, fundamentals across the REIT industry are stronger than before the pandemic. REIT FFO is 10% above pre-pandemic-levels while dividend coverage remains historically strong.

State of the REIT Nation

Amid intensifying concerns over the potential fallout from several major tech-focused bank failures, this report examines high-level real estate industry fundamentals to chart the likely path forward for the publicly-traded real estate industry utilizing recently-released NAREIT T-Tracker data.

{kind=link}

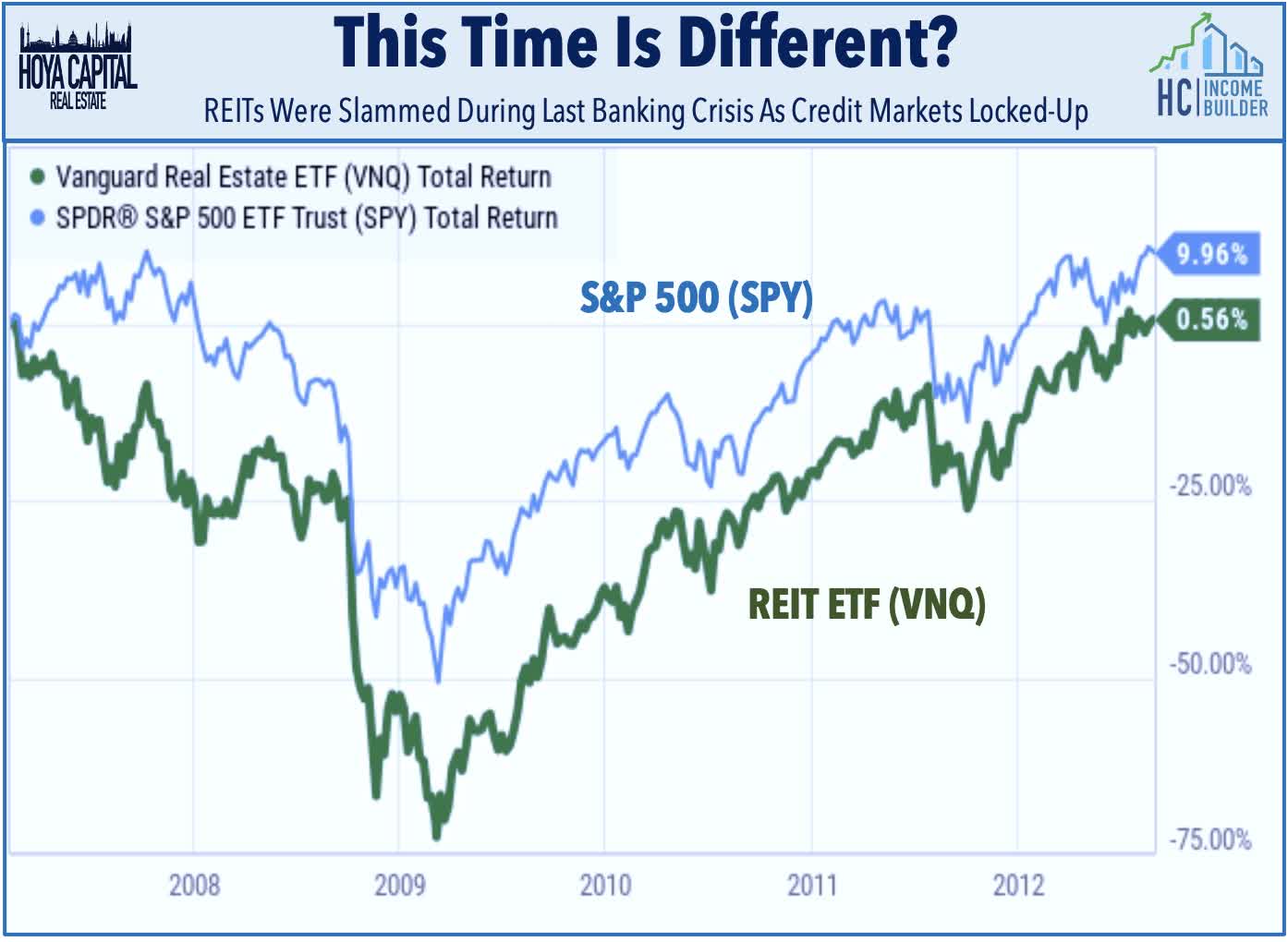

Real estate equities have been slammed particularly hard over the past week erasing all of their 2023 gains which were as high as 10% in early February - as investors draw parallels to the early stages of the 2008 financial crisis when locked-up credit markets created a cascade of distress across the more highly-levered and credit-sensitive industry groups. The broad-based Equity REIT ETF ( VNQ ) plunged by nearly 75% from its peak in February 2007 to its trough in March 2009 as seizing credit conditions caught over-extended REITs flatfooted, forcing many real estate companies to issue equity at firesale valuations simply to stay afloat. By comparison, the S&P 500 ( SPY ) dipped roughly 50% from peak-to-trough and returned to its pre-GFC levels by early-2011, nearly two years before the real estate index fully recovered.

{kind=link}

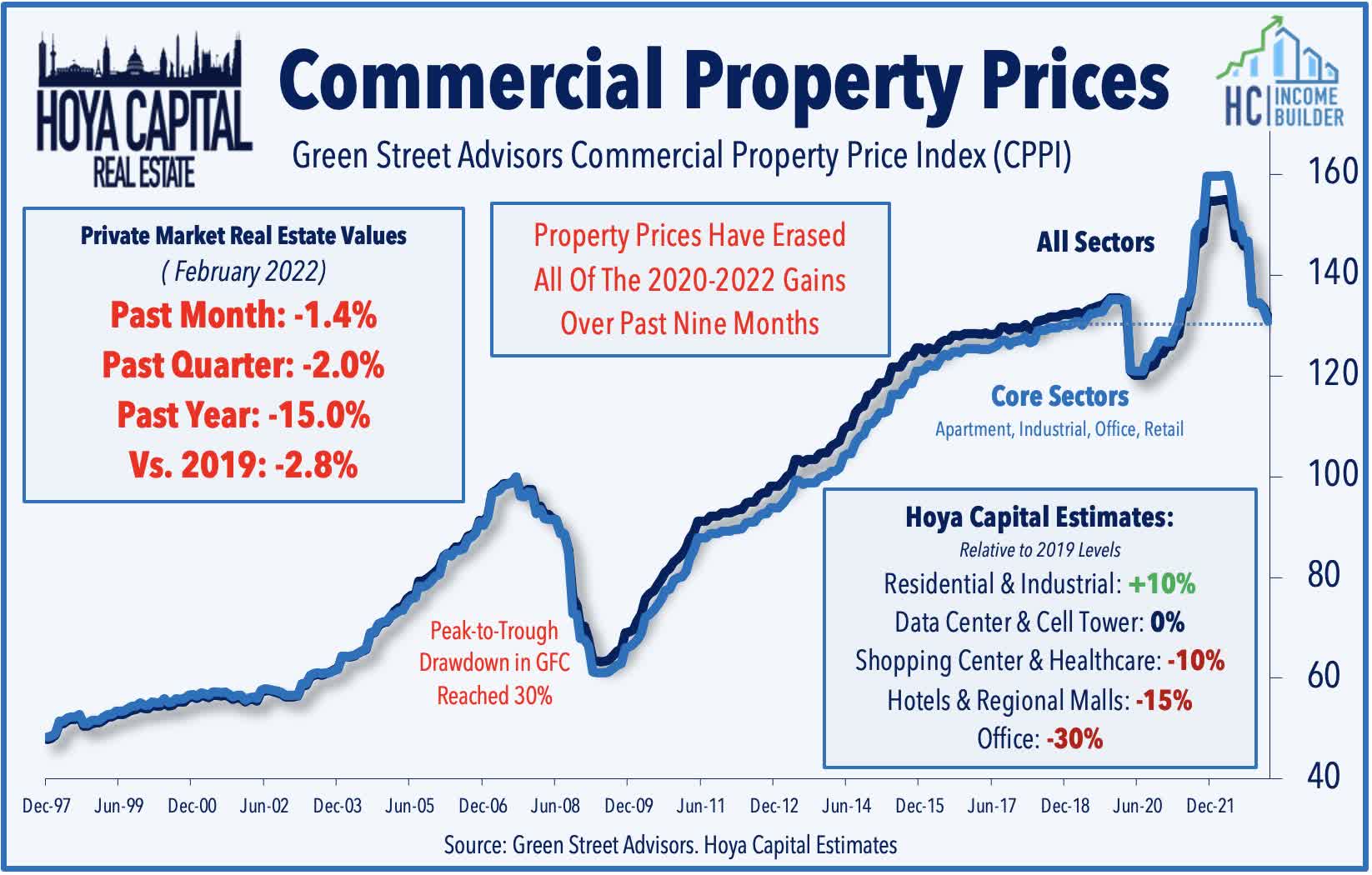

It took several quarters, but private real estate markets are finally "catching up" to the reality of sharply higher interest rates - and expectations that rates may be "higher for longer" - conditions have been reflected in public real estate markets since early 2022. Green Street Advisors' data shows that private-market values of commercial real estate properties have dipped nearly 15% over the past year and have now given back all of their pandemic-era gains. By comparison, the peak-to-trough drawdown in this valuation index during the Great Financial Crisis was 30%. Far more than the prior crisis, however, we've seen a greater divergence between property sectors over the past several quarters, with office valuations now about 30% below 2019-levels, which has sparked a wave of mega-sized loan defaults from Pimco , Brookfield , and RXR. On the upside, residential and industrial property valuations are above 2019-levels as significant property-level Net Operating Income ("NOI") growth has more than offset the uptick in cap rates.

{kind=link}

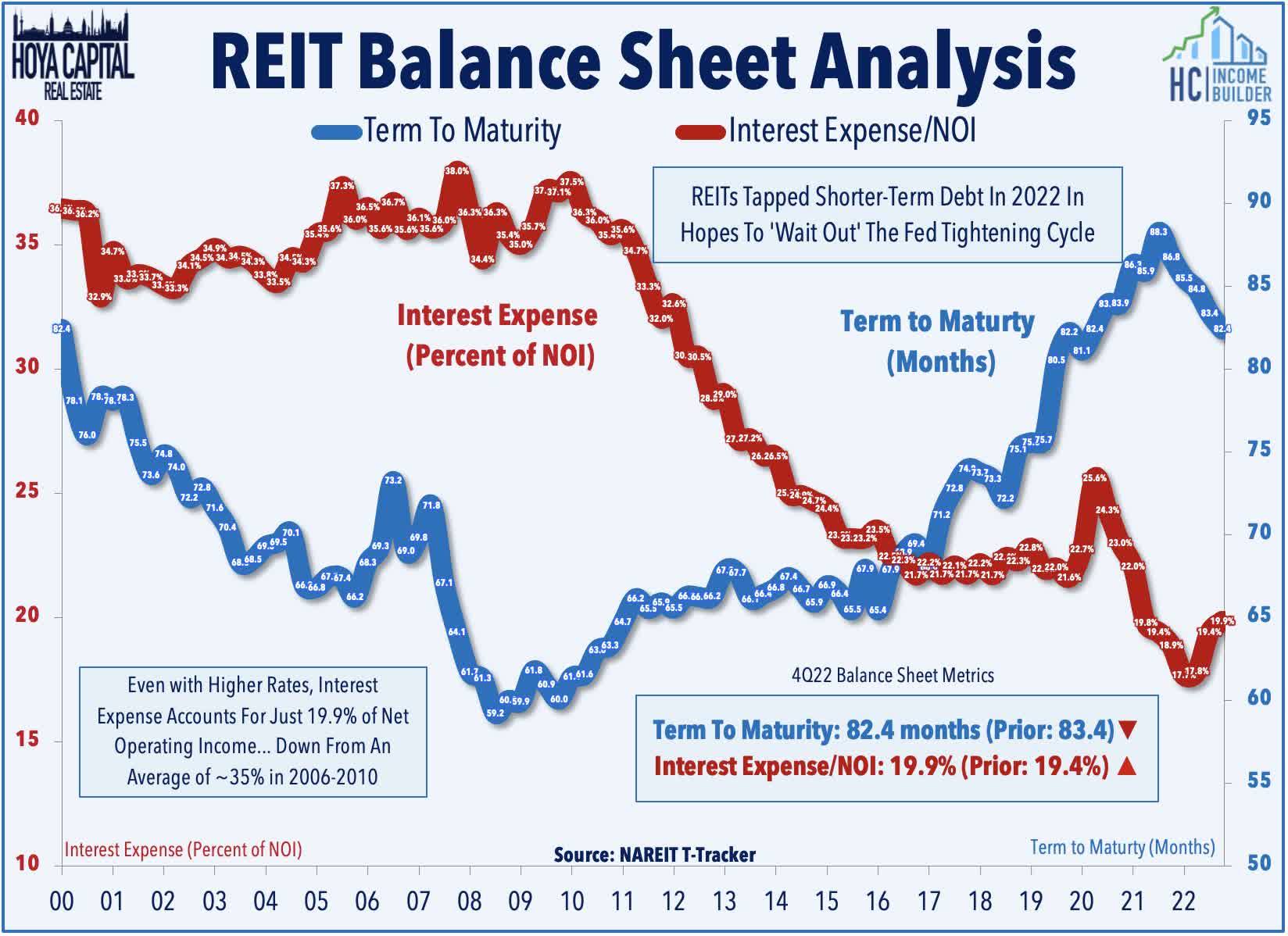

Is this time different? With the scars of the Great Financial Crisis still visible enough to be reminders of more dismal times, most public REITs have been "preparing for winter" for the last decade, perhaps to the frustration of some investors that turned to higher-leveraged and riskier alternatives in recent years - a theme that is certainly not unique to the real estate industry. In doing so, REITs ceded some ground to private market players and non-traded REIT platforms that were willing to take on more leverage and finance operations with short-term debt. Publicly-traded REITs have had far greater access to longer-term, fixed-rate unsecured debt that has allowed REITs to lock-in fixed rates on nearly 90% of their debt while simultaneously pushing their average debt maturity to nearly 7 years, on average, thus avoiding the need to refinance during these highly unfavorable market conditions.

{kind=link}

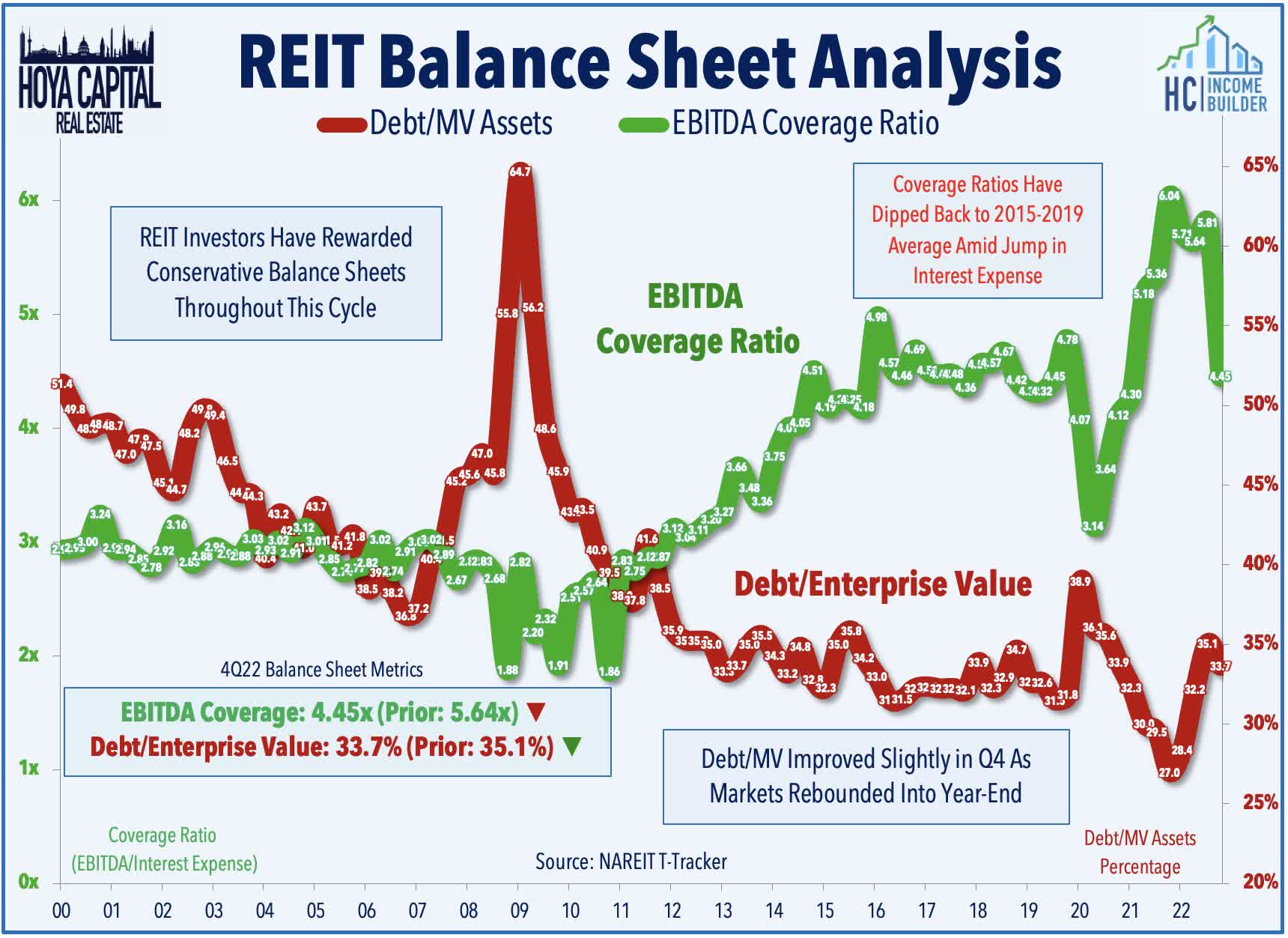

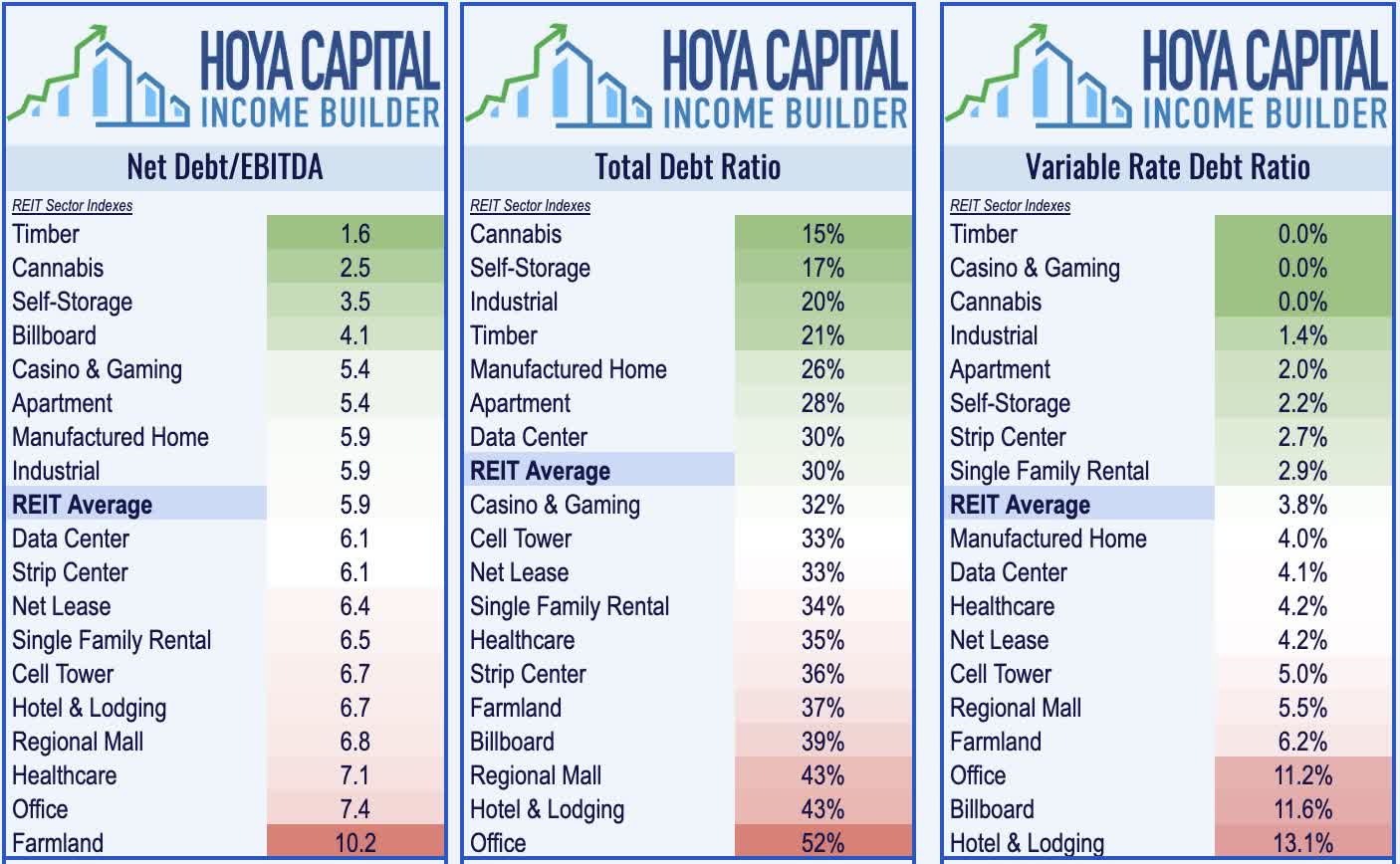

Even as benchmark interest rates doubled from a year earlier and even with market values of REITs lower by 20-30% during that time, REITs balance sheets remain very healthy by historical standards, merely giving back the incremental pandemic-era improvement. Debt as a percent of Enterprise Value still accounts for less than 35% of the REITs' capital stack, down from an average of roughly 45% in the pre-recession period - and substantially below the 60-80% Loan-to-Value ratios that are typical in the private commercial real estate space. Interest coverage ratios (calculated by dividing EBITDA over interest expense) have seen a shaper erosion over the past several quarters from its all-time highs set last year, but still stands at 4.45x, which roughly matches the coverage ratio at the end of 2019 and compares very favorably to the 2.75x average in the three years before the Great Financial Crisis.

{kind=link}

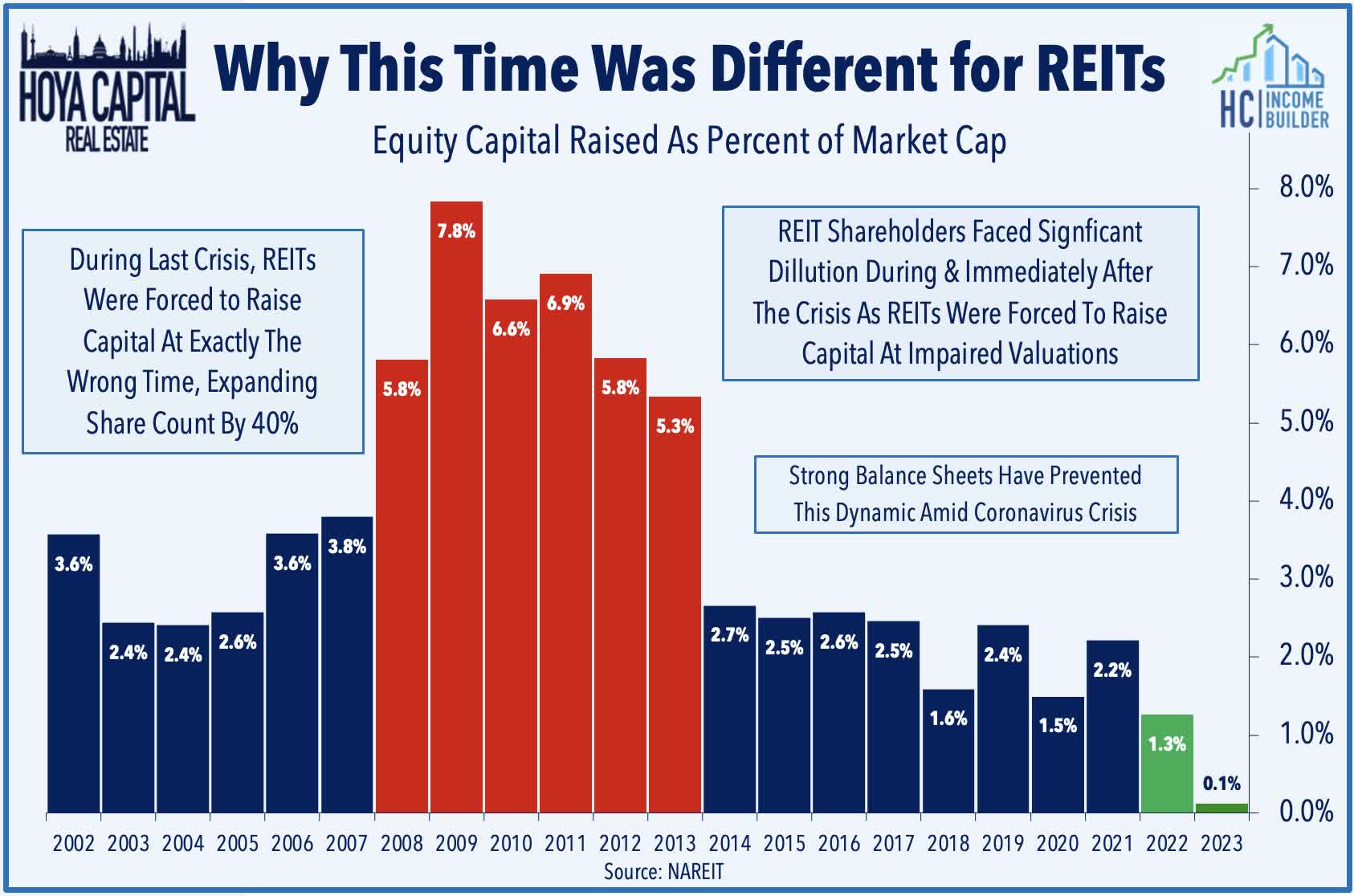

The ability to avoid "forced" capital raising events has been the cornerstone of REIT balance sheet management since the GFC - a time in which many REITs were forced to raise equity through secondary offerings at "firesale" valuations just to keep the lights on, resulting in substantial shareholder dilution which ultimately led to a "lost decade" for REITs. While REITs enter this period on very solid footing with deeper access to capital, the same can't necessarily be said about many private market players that rely on more short-term borrowing and continuous equity inflows to keep the wheels spinning. Much the opposite of their role during the Great Financial Crisis, we believe that many well-capitalized REITs are equipped to "play offense" and take advantage of compelling acquisition opportunities if we do indeed see further distress in private markets from higher rates and tighter credit conditions.

{kind=link}

That said - not all REITs are created equal, and the broad-based sector average does mask some of the intensifying issues in several of the more at-risk sectors and among REITs that have been more aggressive in their balance sheet management. Office REITs are back in the "danger-zone" with a Total Debt Ratio above 50%, while Malls and Hotel REITs have elevated debt burdens above the 40% threshold. As noted in our Losers of REIT Earnings Season report , a significant earnings hit from soaring variable rate interest expense has been the common thread seen across many of these sectors, with a direct earnings hit amounting to 5-10% of Funds From Operations ("FFO") for 2023, and as high as 25% for a small handful of highly-levered REITs.

{kind=link}

REIT Sector Fundamentals

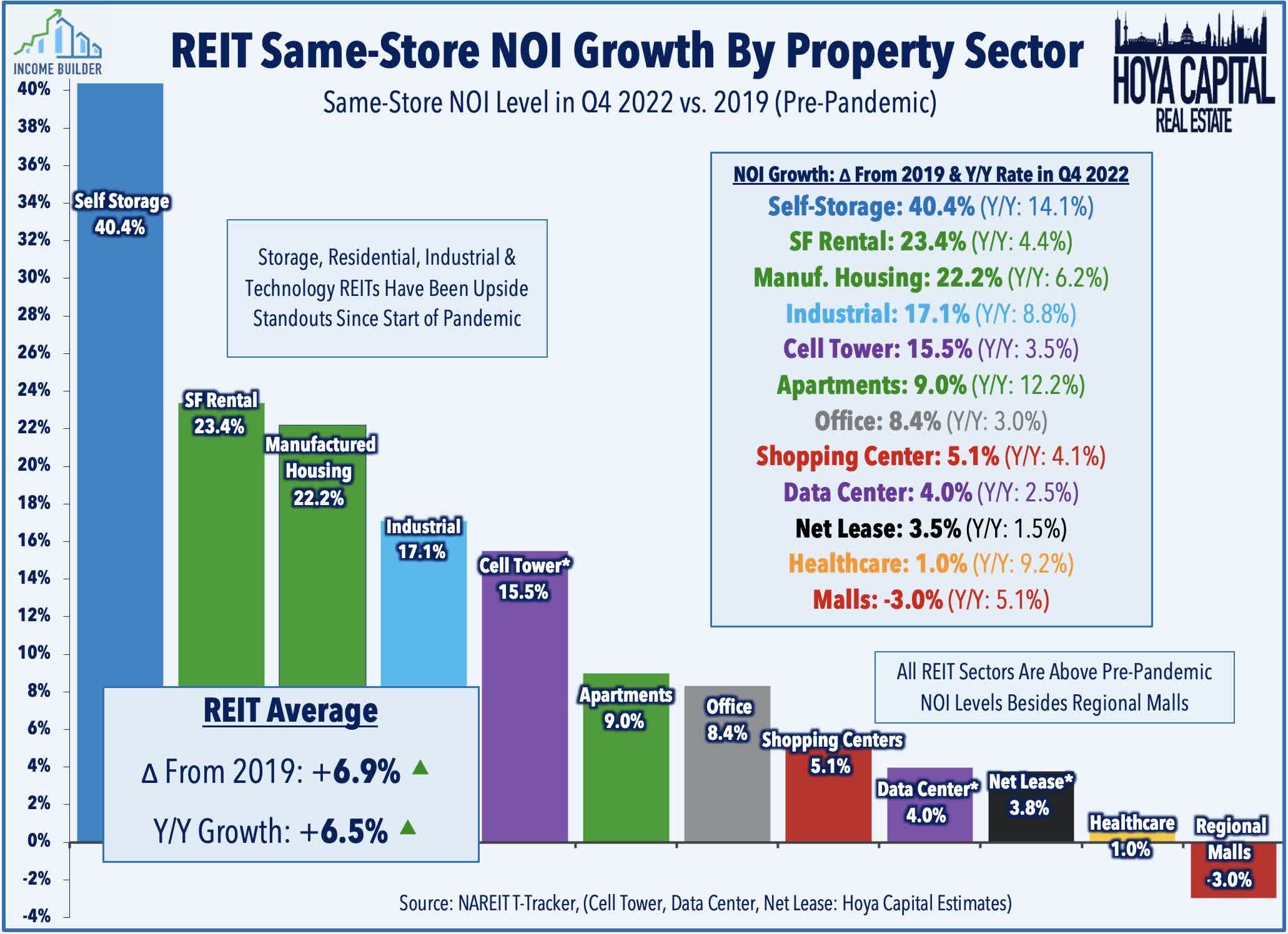

Obscured by the rapidly-shifting macro narrative, REIT property-level fundamentals have been quite strong for most property sectors in recent quarters and - with the exception of office, malls, and some sub-sectors of healthcare and mortgage REITs - entered 2023 with fundamentals that are stronger than before the pandemic. During the depths of the pandemic in 2020, REITs reported a decline in property-level metrics that dwarfed that of the prior crisis, fueled in large part by retail REITs' rent collection woes, but NOI fully recovered by early 2022 and was roughly 7% above pre-pandemic levels in the most recent quarter. The residential, industrial, and technology sectors have been the upside standouts throughout the pandemic with most REITs reporting NOI levels that were 10-30% above pre-pandemic levels.

{kind=link}

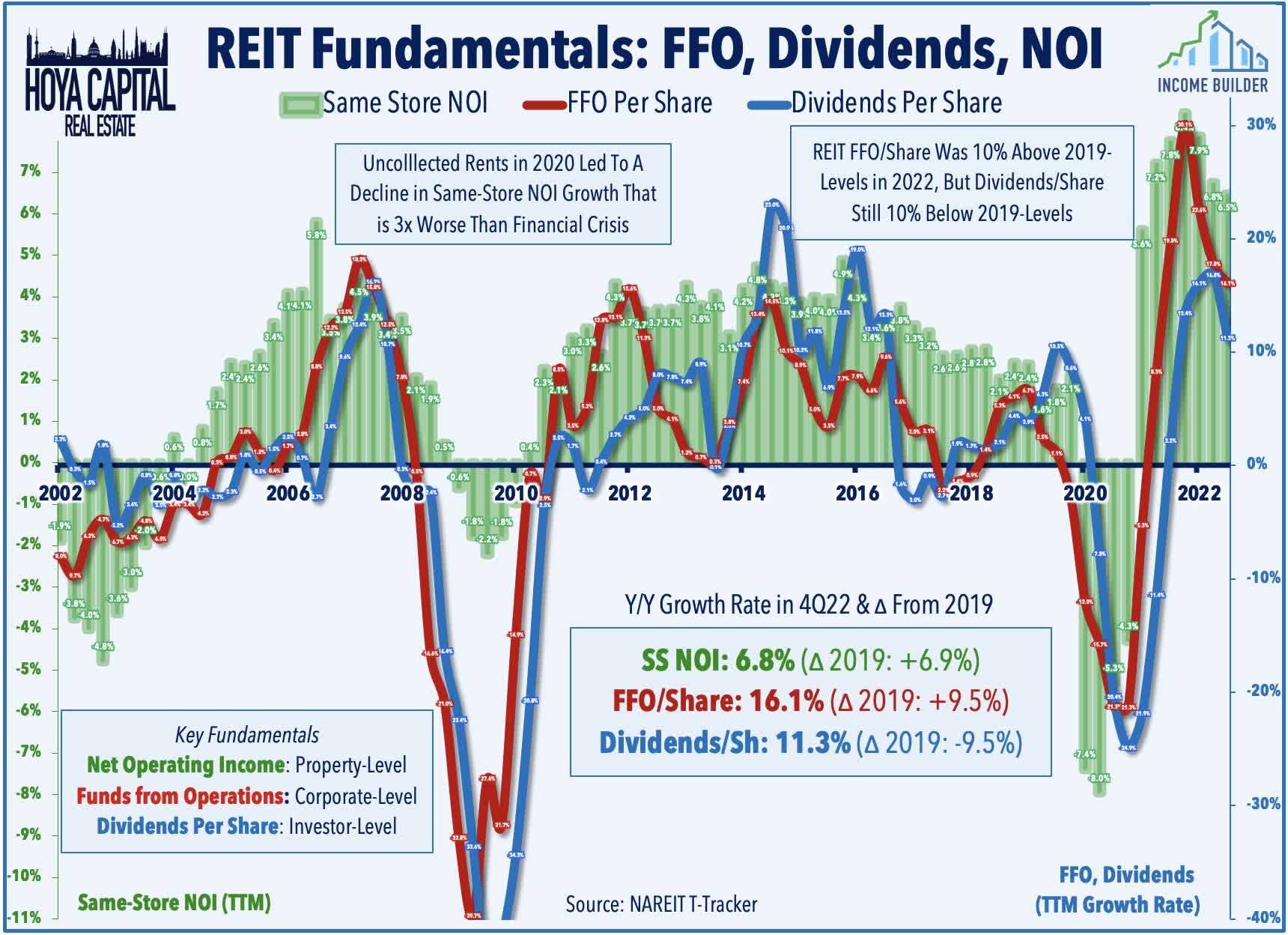

REIT company-level metrics have tracked this rebound in property-level performance closely throughout the pandemic. REIT FFO ("Funds From Operations") has now fully recovered the sharp declines from early in the pandemic and in the fourth quarter, FFO was 25% above its 4Q19 pre-pandemic level on an absolute basis, and 15% above pre-pandemic levels on a per-share basis. Powered by more than 120 REIT dividend hikes in both 2021 and 2022 - and another 38 dividend hikes so far in 2023 - dividends per share rose by 11% from last year in the fourth-quarter. Total dividend payouts remain roughly 10% below pre-pandemic levels, however, as many REITs have been exceedingly conservative in their dividend distribution policy.

{kind=link}

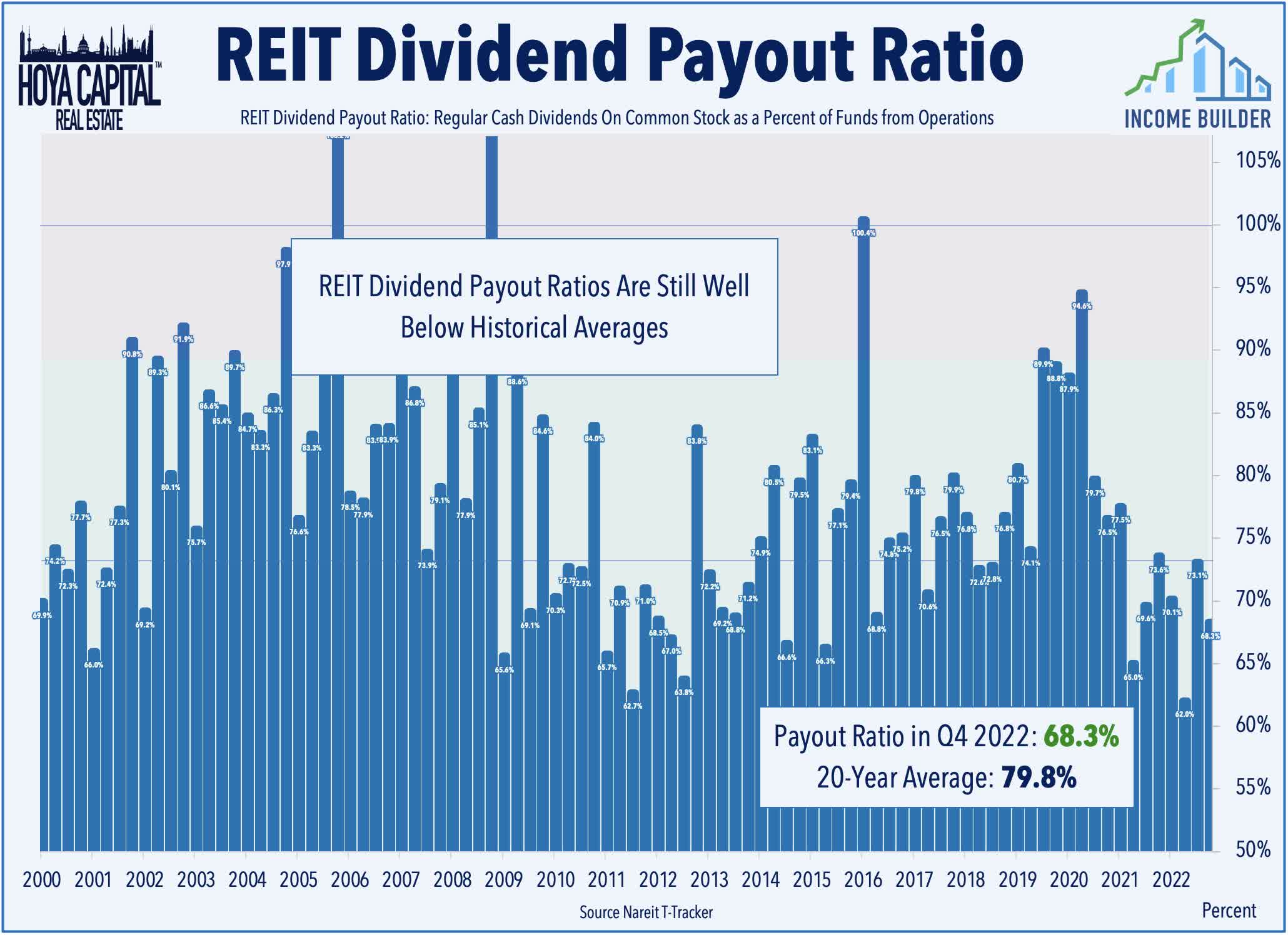

For many generalist investors - the primary question amid the recent market turmoil is: " what does this mean for REIT dividends? " With FFO growth significantly outpacing dividend growth since the start of the pandemic, REIT dividend payout ratios declined to just 68% in Q4 - down from 73% last quarter and still well below the 20-year average of 80%. With a historically low dividend payout ratio, the average REIT has built up a significant buffer to protect current payout levels if macroeconomic conditions take an unfavorable turn. As always, the sector average does mask some elevated payout ratios across several sectors: Mortgage REITs currently pay-out about 95-100% of EPS, on average, while Cannabis REIT payout ratios are also elevated around 85%. Notably, other higher-risk sectors have built-up a larger buffer as office REITs payout just 60% of FFO while hotel REITs payout less than 40%.

{kind=link}

Real Estate Credit Quality

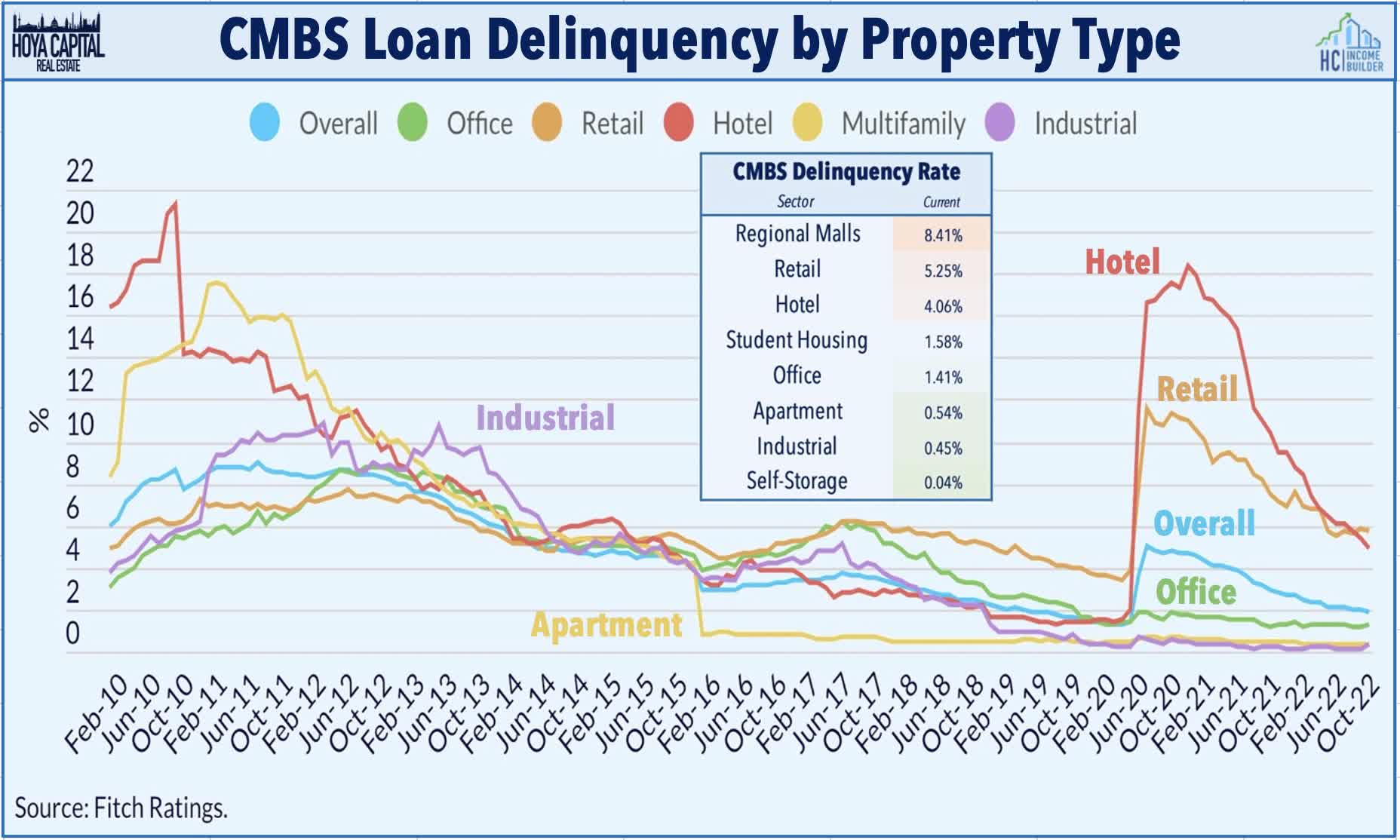

As the Silicon Valley Bank collapse unfolded in real-time, some pundits were quick to point the finger at the banks' real estate exposure as a contributing factor to the firm's failure. But unlike in the 2007-2009 crisis period when real estate-backed loans were considered some of the most "toxic" assets on bank balance sheets, the 15% of firm assets that are real estate-backed are now viewed as some of its strongest collateral during its unwinding process. Ironically, its collapse has fueled a rally in Residential MBS ( MBB ) and Commercial MBS ( CMBS ) valuations as tailwinds from lower benchmark interest rates have more than offset the widening of credit spreads. Importantly, underlying delinquency rates on real estate loans entered this turmoil near historically-low levels. Fitch reported last week that the U.S. CMBS delinquency rate decreased to 1.83% in February - well below the roughly 3% average from 2015-2018 and the 9% peak in 2011. Notably, over 90% of the new delinquencies were office (56%) and retail (35%).

{kind=link}

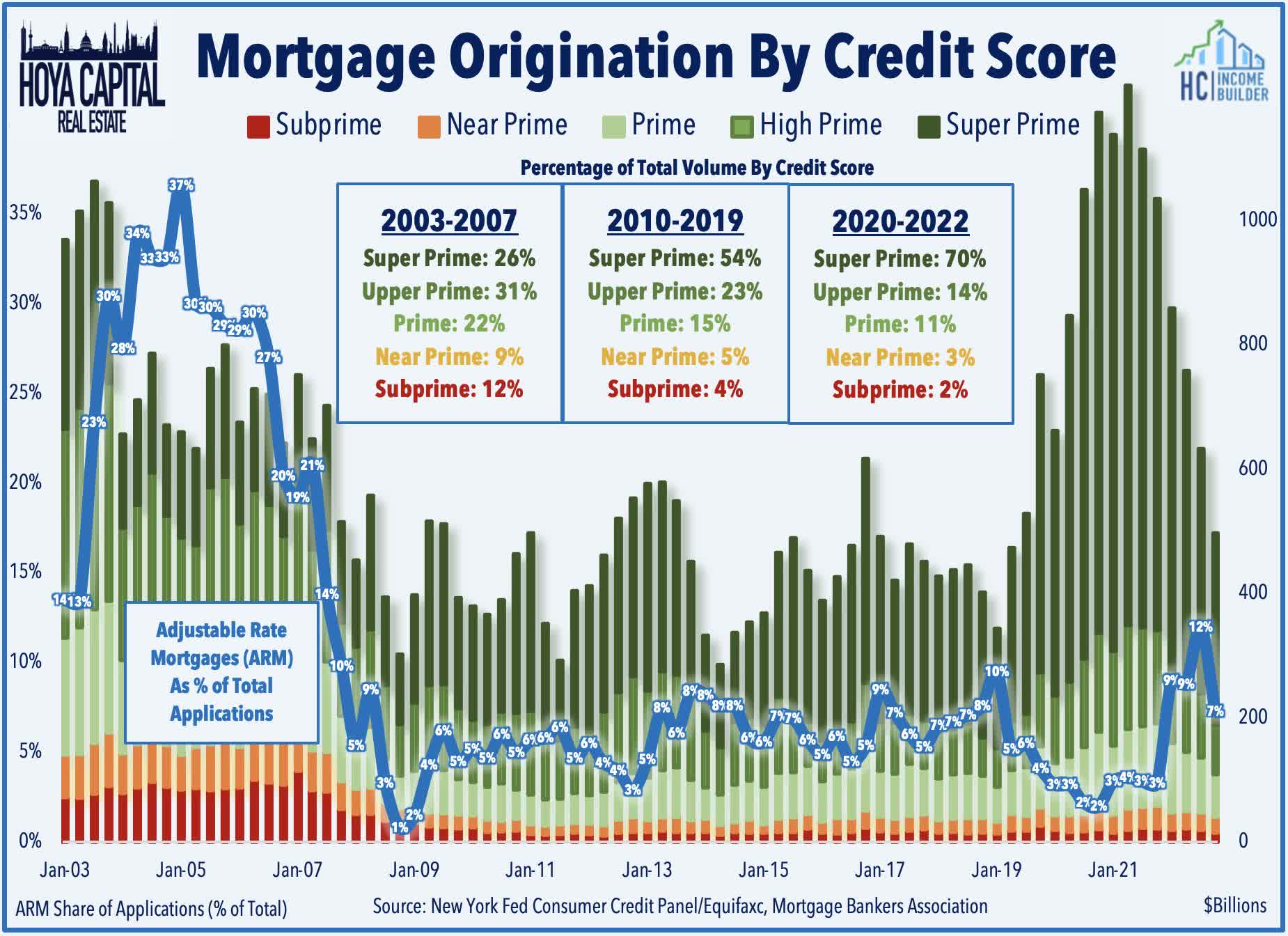

Credit quality is even stronger on the residential side. Owing to years of tight mortgage lending conditions and a generally slow post-recession recovery in homeownership, the residential real estate market has undergone a period of significant deleveraging over the last decade. At the end of 2022, the mortgage debt service payment ratio as a percent of disposable income remained near the lowest level on record at 3.99%. By comparison, this level was at 7.13% in Q4 2007 before the GFC recession. Importantly, subprime loans and adjustable-rate mortgages - the dynamite that led to a cascading financial market collapse in 2008 - have been essentially non-existent throughout this cycle. Adjustable-rate mortgages - which would be most "at-risk" from the surge in rates have accounted for less than 5% of mortgages originated since 2009, down from nearly 30% at the peak in 2005.

{kind=link}

REIT External Growth & Public Listings

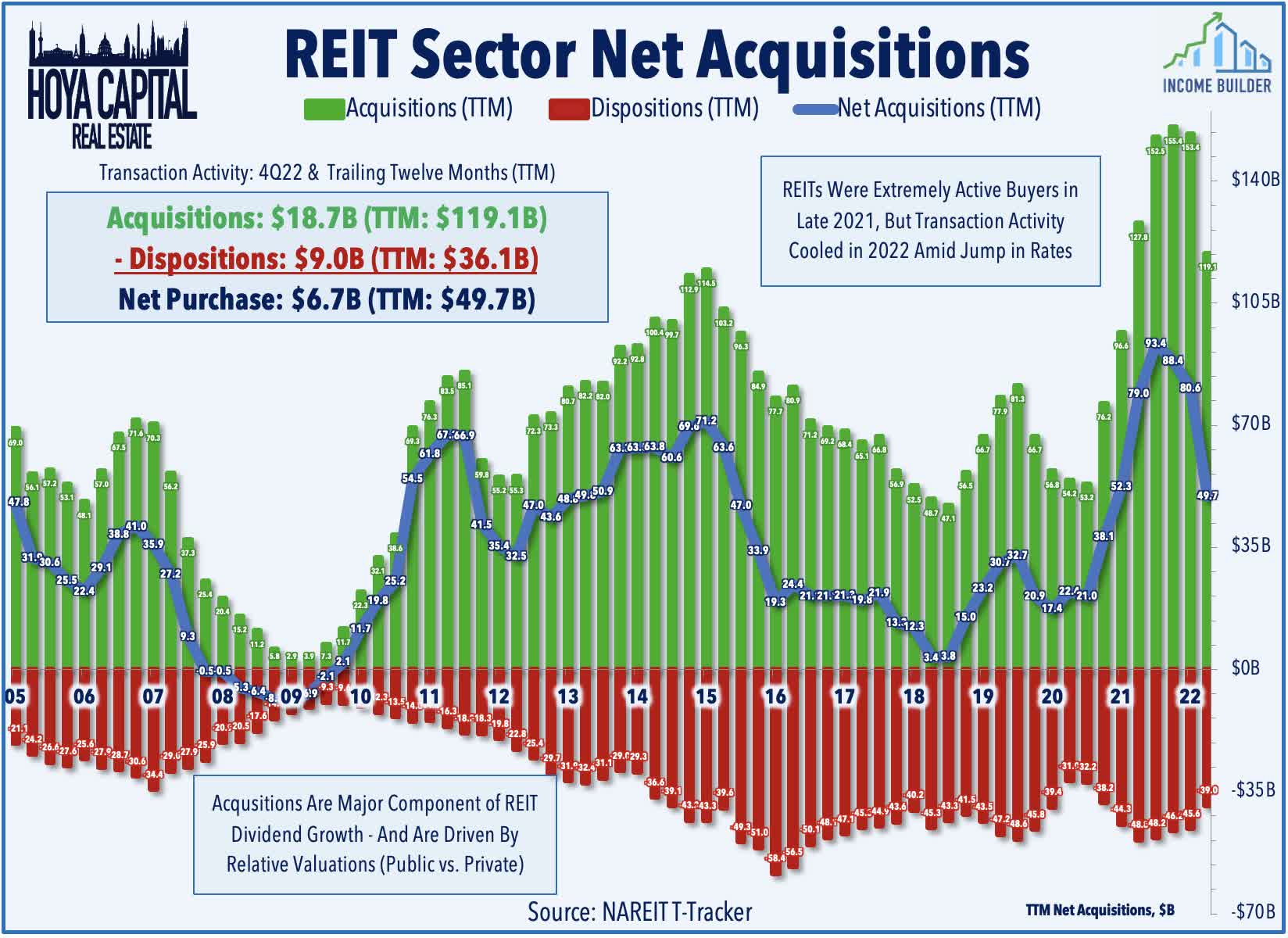

REIT external growth comes in two forms – buying and building. REITs have "hunkered down" in recent quarters amid the surge in interest rates, but we believe that opportunities should emerge over time as private players seek an exit. Acquisitions have historically been a key component of FFO/share growth, accounting for more than half of the REIT sector's FFO growth over the past three decades with the balance coming from "organic" same-store growth and through ground-up development and redevelopment. With a historically large "bid-ask" spread for private real estate assets, REITs have slowed their pace of acquisitions significantly over the past several quarters with net purchases of $6.7B in Q4 - down from nearly $40B in Q4 2022.

{kind=link}

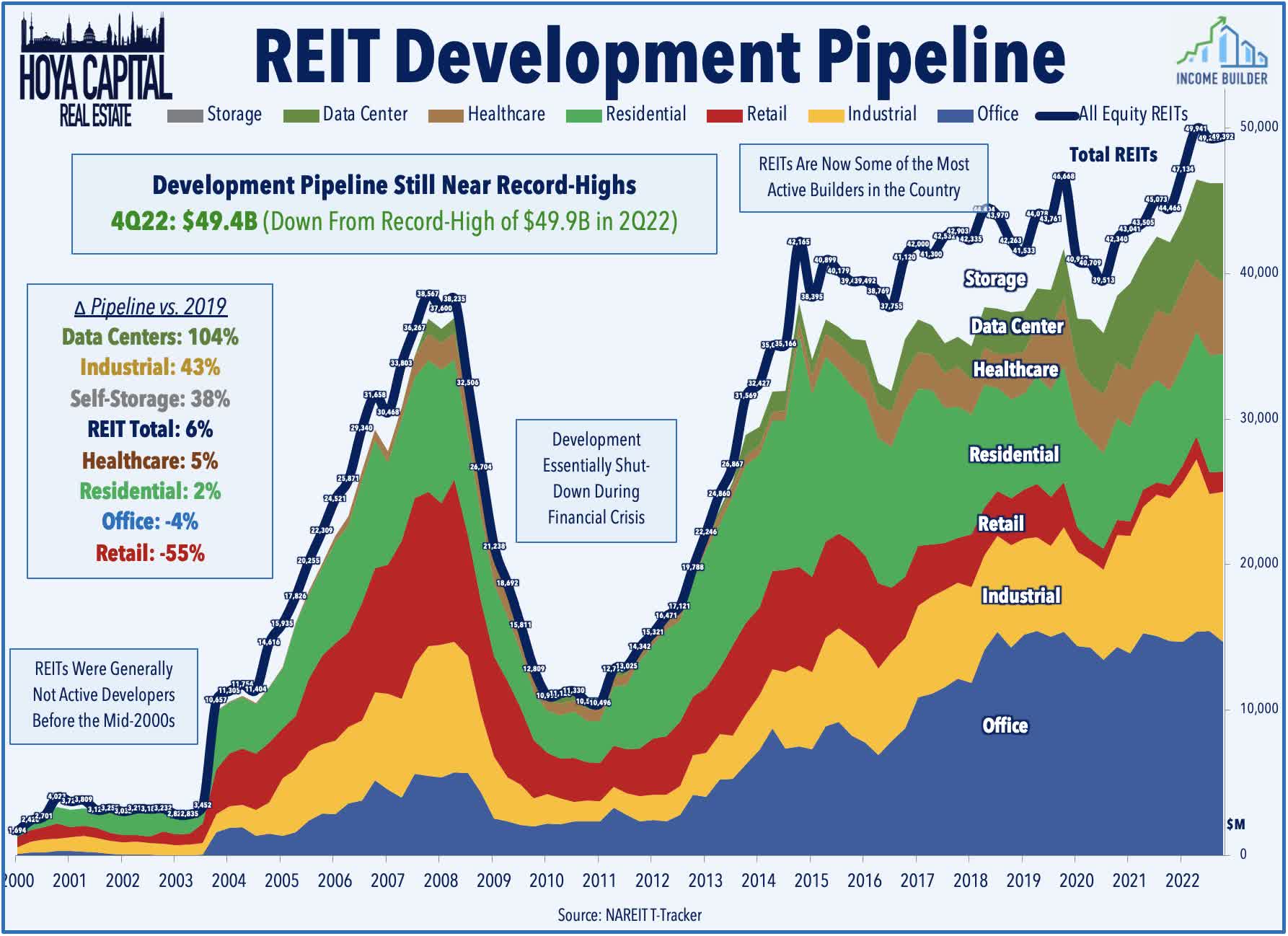

REITs have become some of the most active builders in the country over the past decade and - despite the pressure from higher rates - REITs expanded their pipeline throughout 2022 to levels that exceeded the prior record set just before the pandemic in 4Q19 at $50.4B. Much of this expansion has been fueled by three property sectors - data center, industrial, and self-storage - which have expanded their pipelines by 104%, 43%, and 38%, respectively, since the end of 2019. Retail REITs, on the other hand, have engaged in minimal development activity over the past several years, while the pipeline in residential, office, and healthcare REITs is roughly even with 2019-levels.

{kind=link}

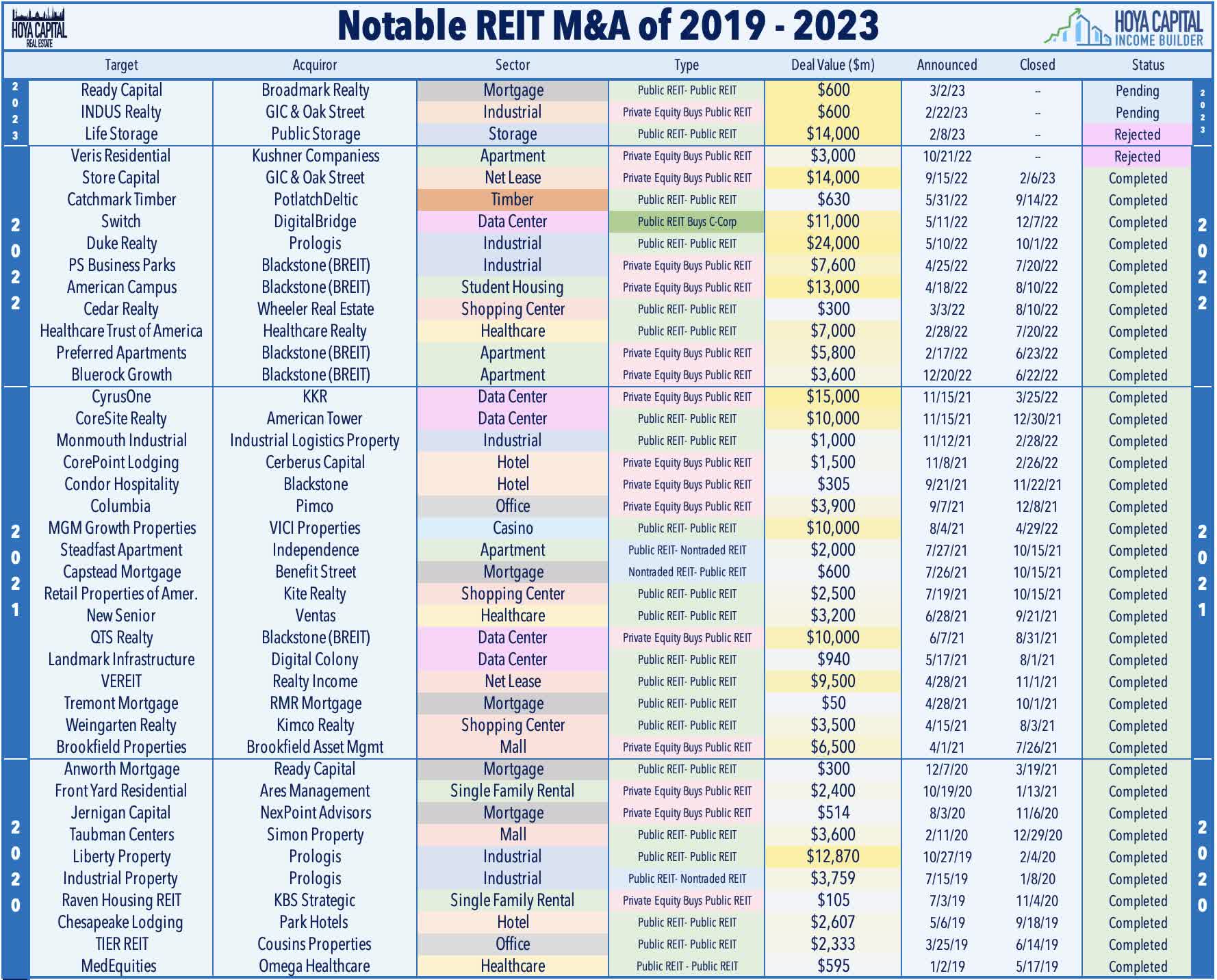

The "animal spirits" - which were very much alive in the REIT world in 2021 and into mid-2022 - have calmed significantly in recent quarters following the spur of activity in early 2022. Blackstone ( BX ) has been quiet since last April following a buying spree that included - student housing REIT American Campus , industrial REIT PS Business Parks , and apartment REIT Preferred Apartment , which followed a pair of deals last year for Bluerock Residential and QTS Realty . Since last May, we've seen just two accepted M&A deals in the equity REIT space - both from private equity firms GIC and Oak Street, which closed on its acquisition of net lease REIT STORE Capital earlier this year and reached a deal to acquire industrial REIT INDUS Realty ( INDT ) in February. In addition to these deals, Veris Residential ( VRE ) rejected a takeout offer from Kushner Companies, while Life Storage ( LSI ) rejected a takeover offer from fellow storage REIT Public Storage ( PSA ).

{kind=link}

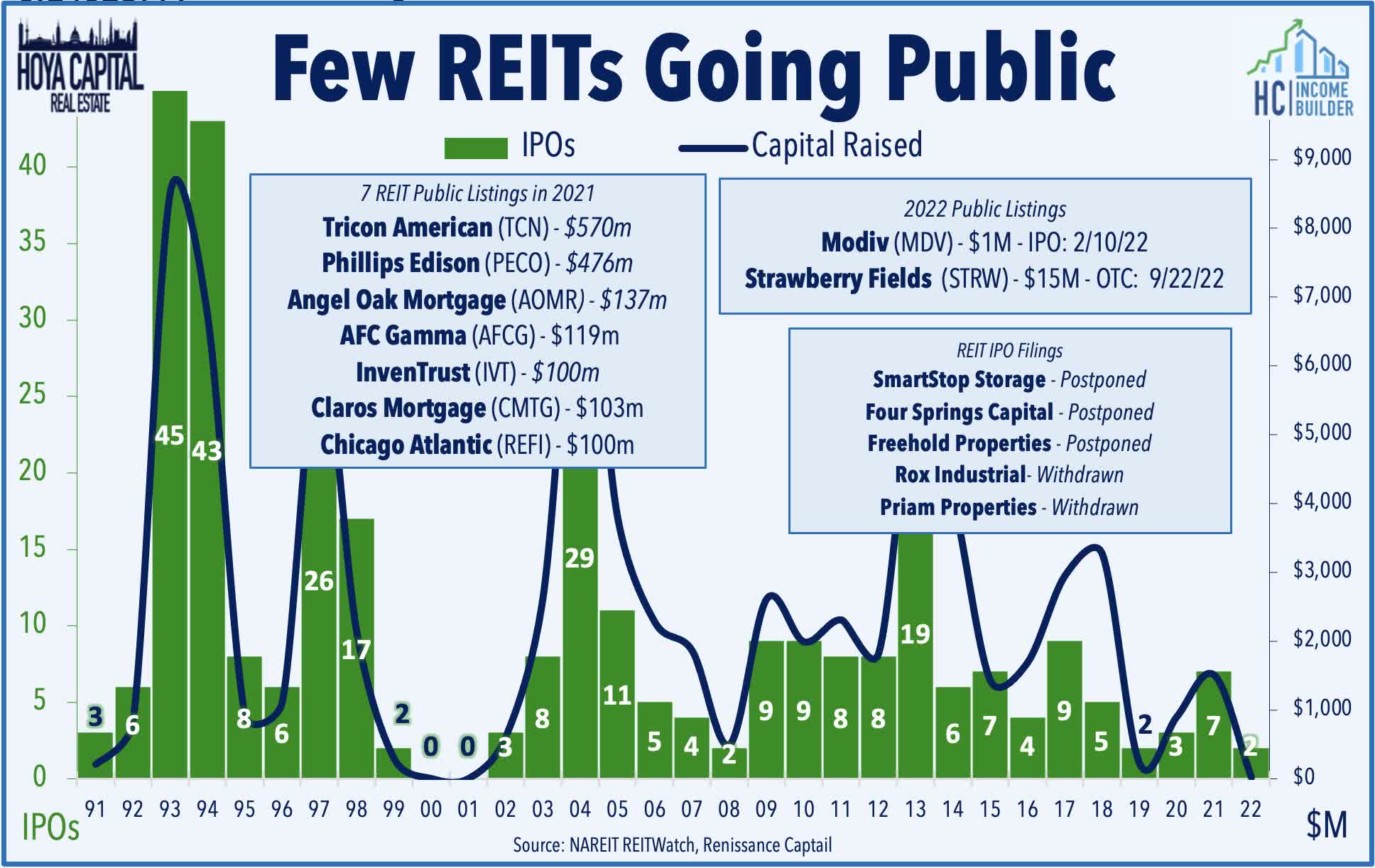

REIT IPOs have also been essentially non-existent over the past year following a notable wave of activity in 2021 - a year that saw seven public listings, the most since 2013. Last September, Strawberry Fields went public through a direct listing and after trading OTC for several quarters, began trading on the NYSE last month. Strawberry Fields is a healthcare REIT with a portfolio of 79 properties located primarily in the U.S. Southeast. A handful of recent REIT IPO filings have been either postponed or canceled, including the listing for office owner Priam Properties , net lease REIT Four Springs Capital , and cannabis-focused Freehold Properties . Notably, past banking crises have led to a subsequent wave of REIT IPOs as private real estate owners that struggled to find debt financing turned to public equity markets to raise much-needed capital. The Savings & Loan Crisis of the early 1990s is generally credited as the catalyst that sparked the Modern REIT Era and many of the largest public REITs trace their lineage back to early 1990s IPOs.

{kind=link}

Takeaways: REITs Prepared For Turmoil

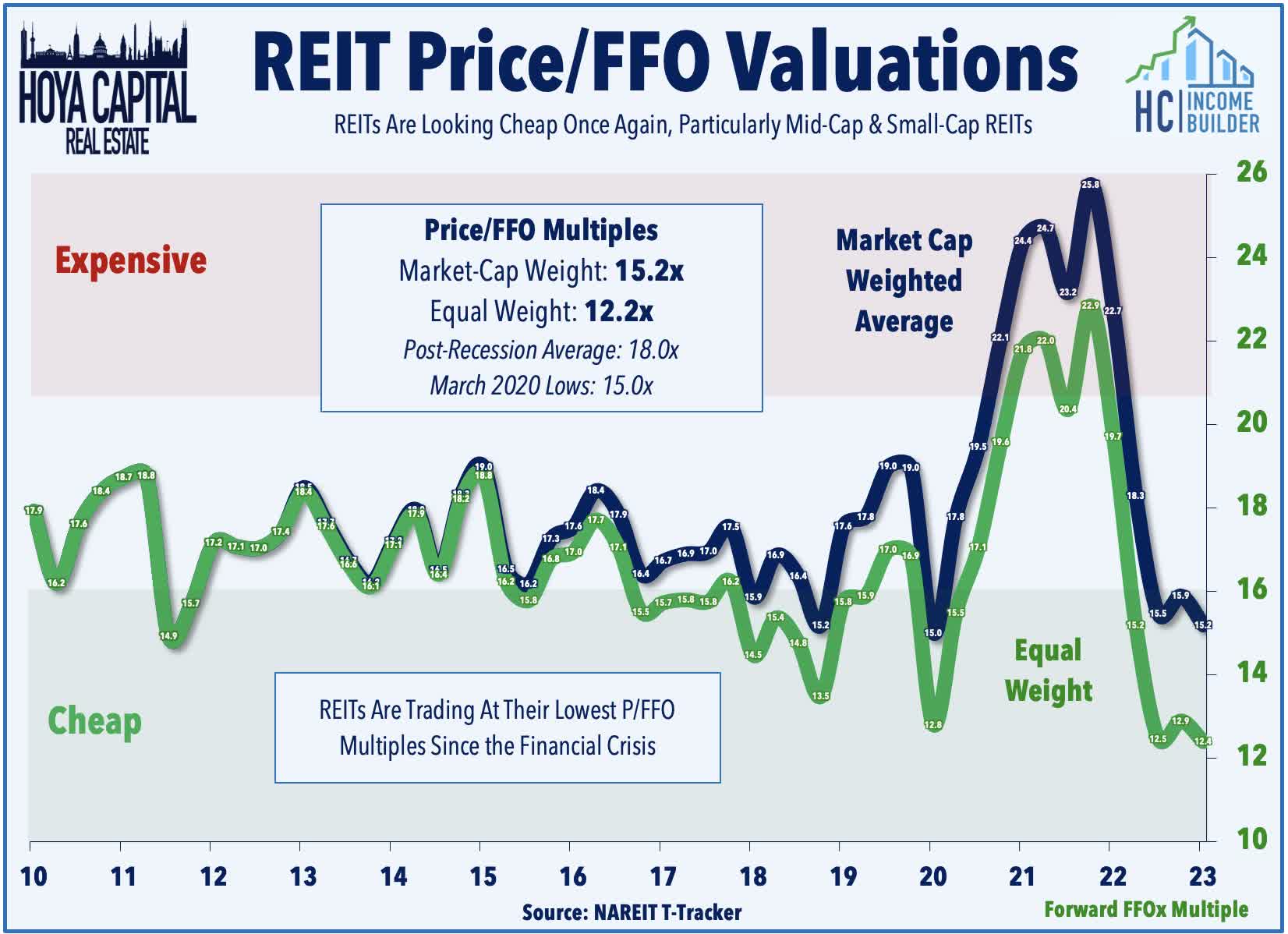

Owing to the harsh lessons from the Great Financial Crisis, most REITs have been exceedingly conservative with their balance sheet and strategic decisions, ceding ground to higher-levered private-market players. It took several quarters, but private real estate markets are finally "catching up" to the reality of sharply higher interest rates, and the recent market turmoil may accelerate the distress that loomed over the private-market firms and lenders that pushed leverage limits. Many well-capitalized REITs are equipped to "play offense" and take advantage of acquisition opportunities as private players seek an exit. The extended sell-off over the past three quarters has pulled REITs back into "cheap" territory as the "Rates Up, REITs Down" paradigm has weighed on valuations. Equity REITs currently trade at an average Price/FFO multiple of 15.2x using a market-cap weighted average and 12.2x on an equal-weight basis, which is the "cheapest" since the early 2000s.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

This Time Is Different