THO - THOR Industries: Too Much Risk Right Now

2023-04-04 15:09:12 ET

Summary

- THO posted disappointing Q2 FY23 results. Their revenues and net income declined significantly.

- The management has provided pessimistic revenue estimates for FY23, and I believe many challenges might hamper its growth in the coming quarters.

- The valuation seems fine, but it is too risky to invest in THO right now.

- I assign a hold rating on THO.

THOR Industries (THO) manufactures and sells RVs and accessories in North America and Europe. They provide travel trailers, luxury fifth wheels, caravans, urban vehicles, and aluminum extrusion to RV manufacturers. THO recently announced its Q2 FY23 results. I will analyze its financial performance and discuss its growth potential in this report. Their financial performance in Q2 FY23 was quite disappointing, and I believe there are several challenges that they might face in coming quarters which could hamper its growth. Hence I assign a hold rating on THO.

Financial Analysis

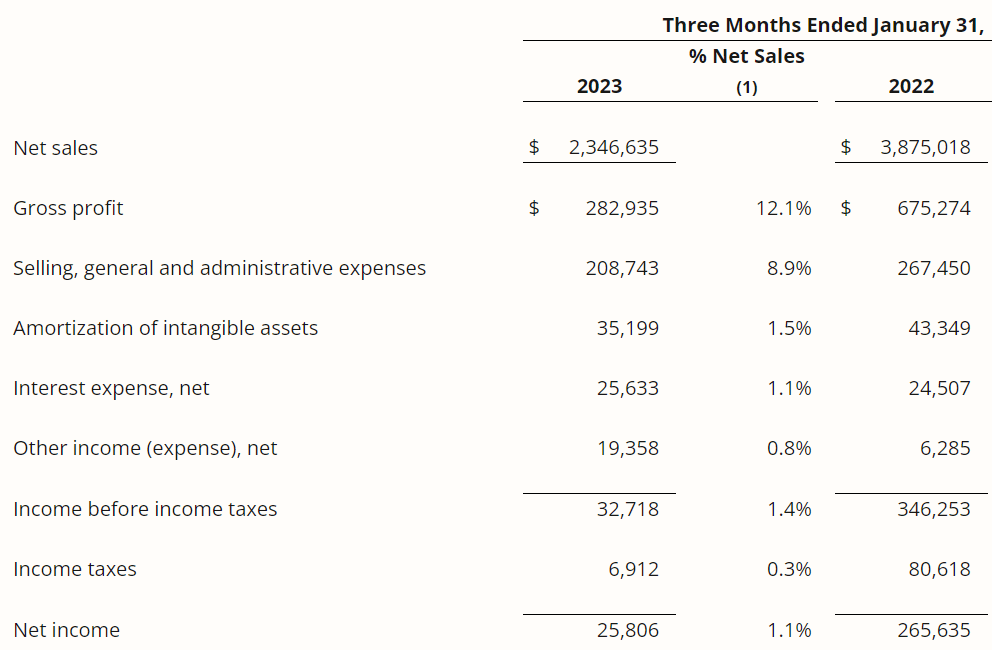

THO recently announced its Q2 FY23 results . The net sales for Q2 FY23 were $2.3 billion, a decline of 39.4% compared to Q2 FY22. I believe the main reason behind the drop was a decline in sales in the North American and European regions. In North America, the sales of towable and motorized RVs were down by 58.2% and 24.4%, respectively, in Q2 FY23 compared to Q2 FY22. I believe the sales of towable and motorized RVs were down due to a decrease in unit shipments. The unit shipments of towable and motorized RVs were down by 64.6% and 26.3%, respectively. I believe the main reason behind the decline in unit shipments was a lower consumer and current dealer demand. In Europe, RV sales were down by 10.6% in Q2 FY23 compared to Q2 FY22. Again, I think the sales were down due to a decline in unit shipments. I believe the decline in Europe was caused due to ongoing chassis supply issues.

{kind=link}

The net income for Q2 FY23 was $25 million, a decline of 90.2% compared to Q2 FY22. I believe the main reason behind the drop was a significant decline in net sales and a loss of $7.1 million in the towable EV segment. In my opinion, the financial performance of THO in Q2 FY23 was quite disappointing; a challenging market environment impacted its financial performance. Additionally, the management's revenue estimates indicate that they expect the poor run to continue in coming quarters, and I believe they might continue to struggle financially in coming quarters. Most of the independent dealers have full inventories, recessionary fears, and weak market conditions. Due to these factors, I believe the demand for RVs might remain low in 2023. Due to this, I think their financial performance in the coming quarters might be disappointing. After looking at all these factors, I don't trust the company much that they will do well financially, and their financial performance might adversely impact the share price.

Technical Analysis

{kind=link}

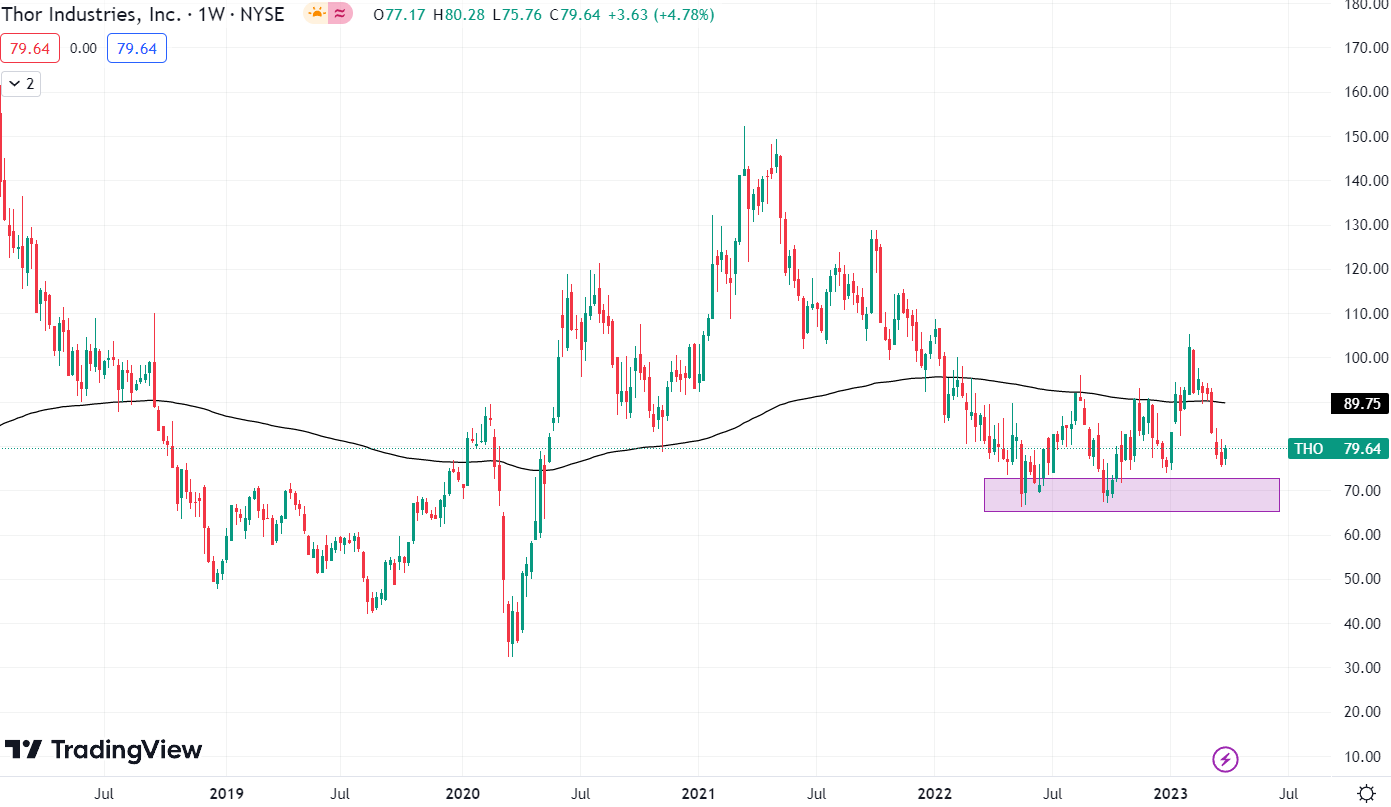

THO is trading at the level of $79.6. It is below its 200 ema, which indicates that it is in a downtrend. The stock has tried to give closing above 200 ema three times since August 2022 but failed; this indicates that the 200 ema is now acting as a resistance level. The stock is currently approaching the support level of $68. The $68 level is very important for the stock because if it breaks the level, it might fall to $45. So, I believe there is no buying opportunity in the stock as it is showing weakness. I think one should only enter the stock if it gives a closing above its 200 ema, which is at $90.

Should One Invest In THO?

{kind=link}

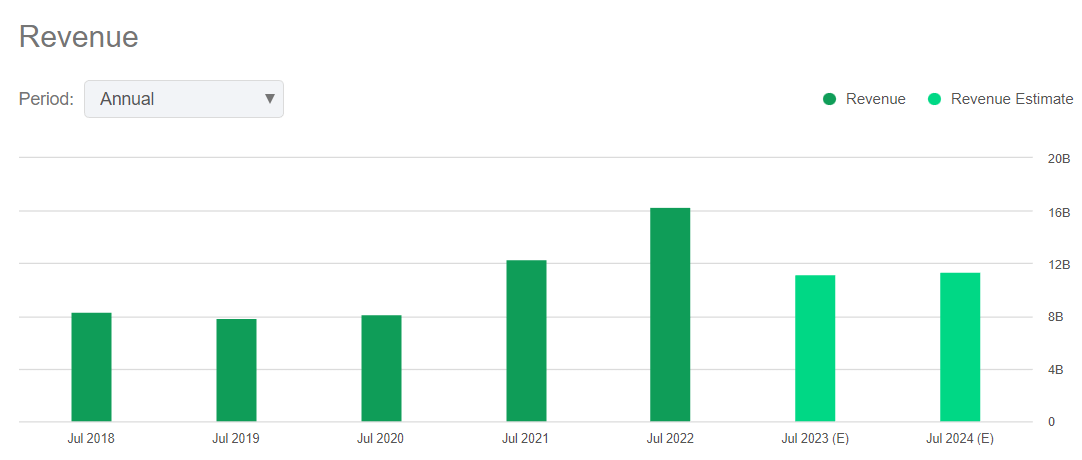

The revenue estimate for FY23 is around $11.2 billion, which is 31.2% lower than FY22 revenue. The estimates suggest that they might struggle in FY23, and we might see the effect of poor performance in the share price because, in my opinion, price follows profits. I believe they might face difficulties achieving the revenue targets; I am saying this because I believe there might be less demand for RVs in North America. There may be less demand for RVs from independent dealers in 2023 due to many independent dealers restocking their inventories in 2022. In addition, macroeconomic headwinds like recessionary fears and weaker market conditions might hamper its revenue growth. If we look at the company backlog in North America, they had backlog orders worth $3.1 billion by the end of 31 January 2023, which was $14.6 billion by the end of 31 January 2022. The significant decline in the backlog is a matter of concern. In my opinion, they might face various uncertainties and challenges in the coming quarters, which could impact their financial performance, and we might see its effect on the share price. Given the financial, technical, and demand trends for RVs, I think it is best to avoid THO because there are presently more drawbacks than advantages.

Now talking about its valuation. I will use EV / Sales and P/E ratios to judge its valuation. The EV / Sales ratio of a firm is calculated by dividing a company's enterprise value by its annual revenue. THO has an EV / Sales ((FWD)) ratio of 0.52x compared to the sector ratio of 1.12x. The Price/ Earnings ratio is calculated by dividing a firm's stock price by EPS. THO has a P/E ((FWD)) ratio of 13.61x compared to the sector ratio of 14.34x. After looking at both ratios, I believe it is undervalued. I believe the valuation is justified because they have performed quite well in the last two financial years; their revenues and net income grew significantly in FY22. But their performance in FY23 till now has been disappointing due to macroeconomic headwinds, so despite being undervalued, I think one should avoid it for now.

Risk

About 13.0% of its consolidated net sales for FY22 were to FreedomRoads, LLC. FreedomRoads, LLC recently bought several formerly independent RV dealerships. The loss of independent dealers or the ability to demand better conditions from the company due to FreedomRoads, LLC's acquisitions could seriously harm its operations. Additionally, a decline in FreedomRoads, LLC's liquidity or creditworthiness could adversely impact its sales and accounts due and result in repurchase obligations under its repurchase agreements. Recent acquisitions and ongoing acquisitions by other independent dealers with U.S. bases have increased the concentration of independent dealers and given these multi-location dealers more bargaining power.

Bottom Line

Despite having an attractive valuation, I believe there is no buying opportunity in THO right now. They might face several uncertainties and challenges in the coming quarters, which can hamper their revenue growth. In addition, their financial performance in Q2 FY23 has been disappointing, in my opinion, so I believe investing in THO right now can be risky. Hence after analyzing all the parameters, I assign a hold rating on THO.

For further details see:

THOR Industries: Too Much Risk Right Now