WSM - TJX Companies: Favorable Environment Remains

2023-06-29 02:11:27 ET

Summary

- TJX, an off-price retailer, has seen strong performance in its Marmaxx segment (T.J. Maxx and Marshalls brands).

- The company has benefited from lower freight costs and a trade-down effect where higher-income consumers switch to off-price retailers during economic uncertainty.

- I maintain a $100 price target for the stock.

Back in March , I wrote that while the stock was not cheap, TJX Companies (TJX) was riding a perfect wave and that it should benefit from industry-wide destocking issues. The stock has returned over 13% since then. Let’s catch up on the name.

Company Profile

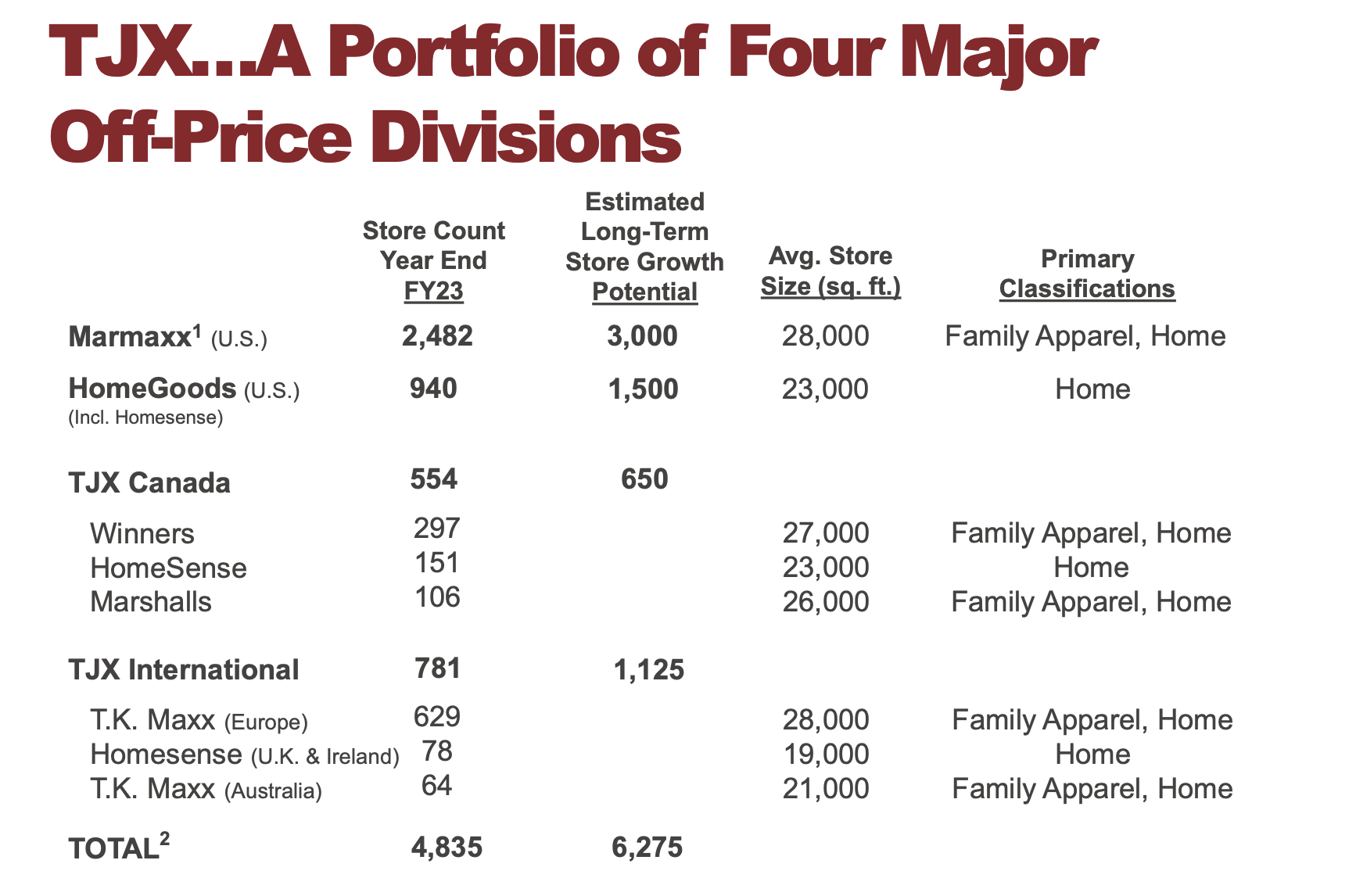

As a reminder, TJX is an off-price retailer that typically sells its items at -20 to -60% off full-retail price. It operates the T.J. Maxx, Marshalls, HomeGoods, HomeSense, and Sierra concepts in the U.S., as well as Marshalls, HomeSense, and Winners in Canada and T.K. Maxx, Homesense, and similar chains internationally.

Its largest segment is called Marmaxx, which consists of its T.J. Maxx and Marshalls brands. Both retailers sell an assortment of apparel, footwear, accessories, and home fashion through its stores as well as online. The segment also include Sierra stores, which sells active apparel, footwear, and outdoor gear.

Its HomeSense segment includes its HomesGoods and HomeSense brands, which sell items such as furniture, decorative accessories, rugs, lighting, and cookware. The company also has a Canadian segment and an International segment as well.

{kind=link}

Company Presentation

Apparel Leads the Way

In my original write-up, I noted that TJX was in a solid position, as prior-year supply chain issues caused many retailers to over order, which led to retailers having to de-stock and brands needing to find places to offload excess inventory. This in turn I said could lead to both lower acquisition costs and better quality inventory. These dynamics showed up in Q1.

One area this was seen was with gross margins, which improved 100 basis points to 28.9%. The company credited better buying as well as lower freight costs.

It also showed up in sales on the Marmaxx side, with same-store sales up 5%. However, apparel sales were even stronger, with comps up high single digits. Traffic was also strong, up mid-single digits.

Discussing current state of the market on its Q1 earnings call , CEO Ernie Herrman said:

“And on Marmaxx is, as you could see by the strong performance, on [same-store] sales, we show it as a 5[%]. It was a very strong 5. And we really like the positioning on open-to-buy. They're the big ships. We like the open-to-buy that we have there and the liquidity because the markets as we talked about, they're just really flooded with a lot of inventory across many brands. And so that, combined with the fact of the good, better, best advantage that we have and we have so much long-tenured merchants in that role, then planning and allocation teams that were really able to leverage the market, I think, better than a lot of other retailers to achieve some of these merchandise margins that are driving their profit performance. Again, a lot of the other retailers can't bob and weave as much because they're not as broad as we are. So it gives us more retailing play, I think, in surgically addressing the retails as we do.”

Not surprisingly, TJX’s HomeSense segment did not perform as well as its Marmaxx segment, with same-store sales off -7%. If you’ve read any of my recent articles on home furnishing and décor names, you know the industry as a whole has been struggling. There was a lot of pull-forward of demand due to Covid, and the industry is down by as much as 20%, according to Wayfair ( W ).

Now this does help TJX on the buying front, but the demand front still remains challenging. However, on its Q1 call, the company did say it was seeing a pick-up in sales and that traffic was improving. The company has been looking to take advantage of the bankruptcy of Bed Bath & Beyond by adjusting inventory at stores near where there were closures. It’s doing this on a store by basis, and it thinks it can take market share in the process. I’d also note that comps get a lot easier in Q2 and Q3 for the segment.

In my initial article, I pointed out that freight costs had been headwind that could turn into a tailwind this year. That is starting to play out. The company said that it benefited much more than expected from lower freight costs in Q1. As a result, it now expects a more than 100 basis point boost to gross margins this year from lower freight expenses. The company said it is seeing this especially in ocean rates. As an aside, it is commentary like this makes me question why Williams-Sonoma (WSM) is experiencing margin pressure due to ocean freight costs .

Another area I previously discussed was that TJX should benefit from a trade down effect. This also appears to be playing out, with the company saying its higher-income demographics were driving its comps. It’s not uncommon during periods of economic uncertainty for higher-income consumers to switch to off-price from places like department stores. With TJX getting some great inventory from popular brands due to retailers previously over ordering, this trade-down trend should continue.

Valuation

TJX stock currently trades at 16x the FY 2024 (ending January) consensus EBITDA of $6.42 billion. Based on FY25 analyst estimates of $7.01 billion, its trades at ~14.7x.

It trades at a forward PE of 23.2x the FY24 consensus of $3.57.

The company is projected to grow revenue 6.4% in FY24 to $53.1 billion.

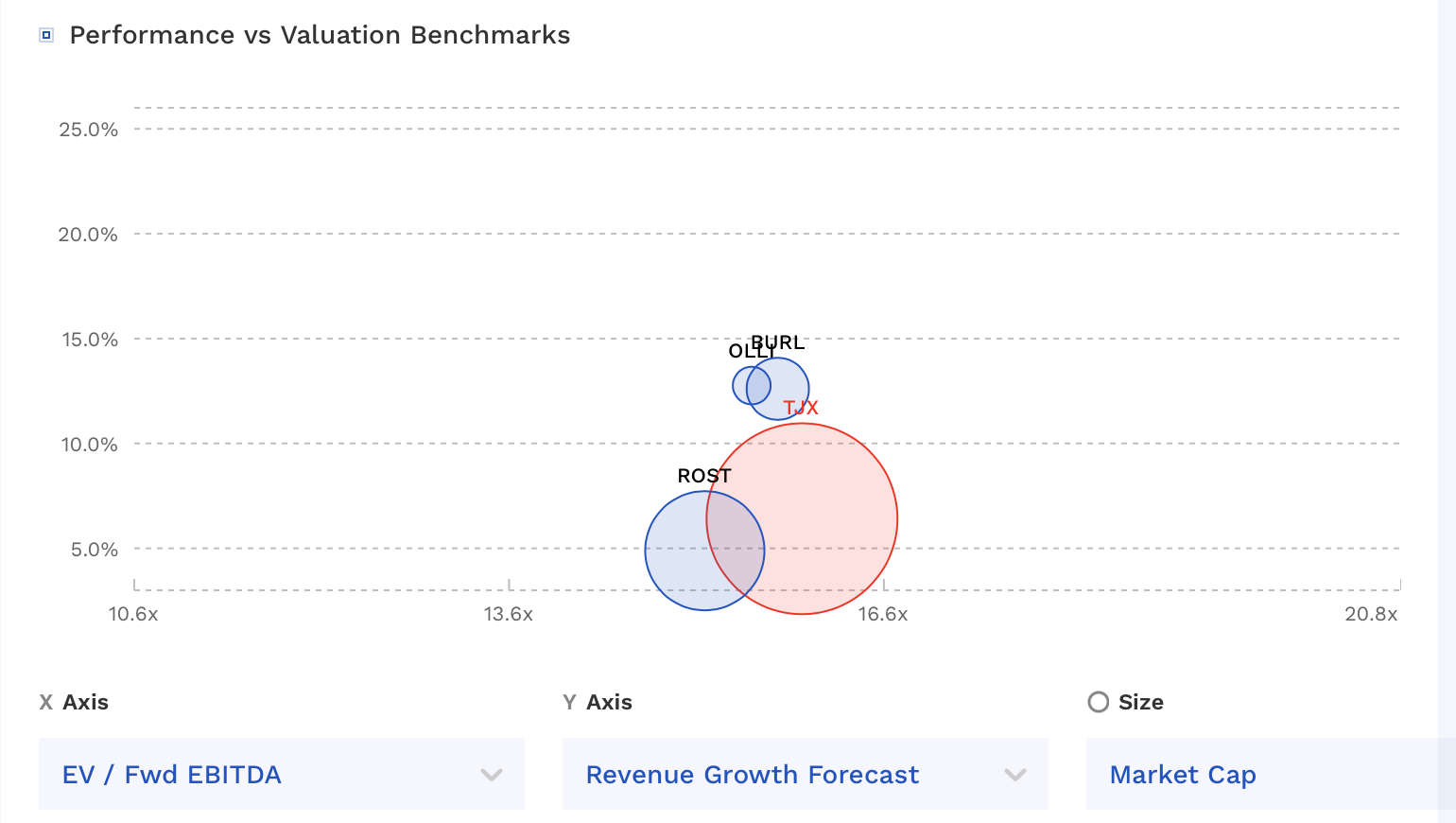

TJX trades at a similar multiple to its off-price peers.

{kind=link}

TJX Valuation Vs Peers (FinBox)

Conclusion

While I still believe that TJX is fairly valued, I think the stock should continue to work in this favorable setting. Off-price retail remains in an ideal operating environment, with attractive inventory acquisition dynamics and consumers looking for bargains. While its ties to home décor and furnishings is a bit of a negative, the company does look well situated to benefit from Bed Bath & Beyond’s bankruptcy and store closures. Lower freight costs are also turning into a nice tailwind for margins.

My $100 price target remains in place. I think with the combination of some out-performance and margin expansion, the stock should be able to get there. That would be about a 17.5x multiple based on the FY25 consensus.

For further details see:

TJX Companies: Favorable Environment Remains