FISV - Toast: The All-In-One Restaurant Solution

Summary

- Toast is a recent public restaurant technology company rapidly growing its footprint.

- The company's operating metrics are impressive, and the company appears to be taking market share.

- There's plenty to like here; I'm on the sidelines for a few more quarters of visibility into where the company is headed.

When I sat down to start researching Toast ( TOST ), I thought I had a good idea of what I was going to find. However, this company is not very highly covered yet in its first year post-IPO, and in many ways it doesn't quite fit in to some of the frameworks I'm used to categorizing companies by. For instance, is Toast a cloud company? Kind of, but not really. It's more of a fintech, but one that is set up exclusively for the restaurant industry, with contracts and requirements for client payment processing solutions.

There's plenty to like here, and a couple of things I really don't. Toast is definitely a good one to keep an eye on from here, and I'll likely open a small position sometime in the next year once the company gets its feet under them in the public markets if they keep hitting the right marks.

{kind=link}

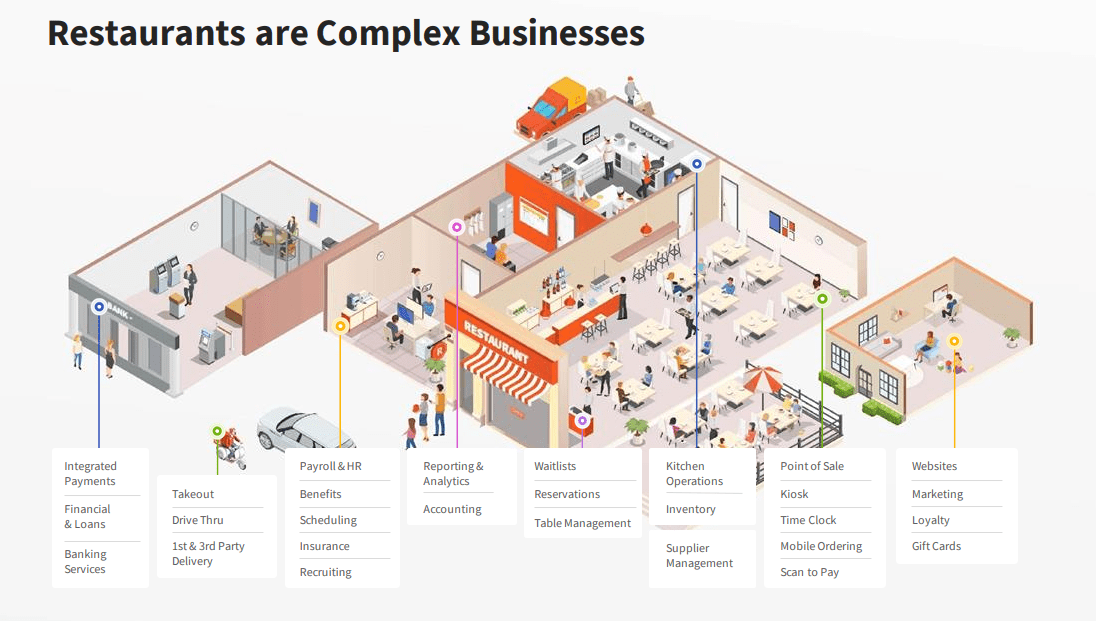

The restaurant industry is notoriously behind in modernizing its technology infrastructure, especially outside of the enterprise cohort. The major national chains have tailor-made solutions and high visibility into their businesses, but the smaller restaurants are in some cases still using paper for some processes, and it requires a lot more work by managers and owners to understand and control the flow of money.

Toast is the market leader in a tailor-made solution for these restaurants. Through a couple of tuck-in acquisitions, the company continues to build out its offering to its customers to provide a full front-to-back solution for increased visibility and process optimization. The company offers its POS devices, locks in customers to use its payment processing, and offers invoicing solutions, inventory management, HR solutions, and more. This ultimately leads to significant switching costs for its customers as a restaurant is able to dramatically improve its operations using Toast, and the company's offerings become deeply ingrained into the restaurant's daily functions.

Competitors in the space, Square ( SQ ), Clover ( FISV ), and Lightspeed will likely maintain a footprint in the market, but Toast is moving towards an offering that will be difficult to match for any competitor not willing to go all-in on this specific industry. Strong evidence of this came as Lightspeed most recently trimmed its revenue guidance and projected almost no growth in next year's new units, while Toast continues to show strong unit and revenue growth.

The company signs with clients to an initial contract of 1-3 years, which sells the hardware to the restaurant and locks them in to using the company's payment processing offering. This sets Toast up for a 1.5-2 year payback window as it takes a cut on every transaction on top of the subscription revenue derived from each piece of hardware given to the restaurant. Using this transaction data, Toast partners with banks to offer loans to the typically underserved SMB cohort and pays the loan back by taking an additional cut off of the restaurant's sales. Using this data, the company is confident it is able to intelligently underwrite these loans and preclude much of the usual default risk.

{kind=link}

The market Toast operates in is a tough one. Restaurants are well-known for a high failure rate in the first few years of operations. However, Toast has managed to maintain a net revenue retention rate around 119% from 2015-2021, through one of the most significant demand shocks the restaurant industry has likely ever seen with the global pandemic. As the company scales and reaches some level of market saturation, the churn figures may not be as rosy, but that is a long way off, and the company has a considerable runway for further market penetration and further expansion of its offerings to increase take rates among existing customers.

ARPU is heading in the right direction, and new customers brought in to the ecosystem are increasingly taking on more of the Toast offerings, which is great to see and points towards further expansion in take rates for earlier customers.

{kind=link}

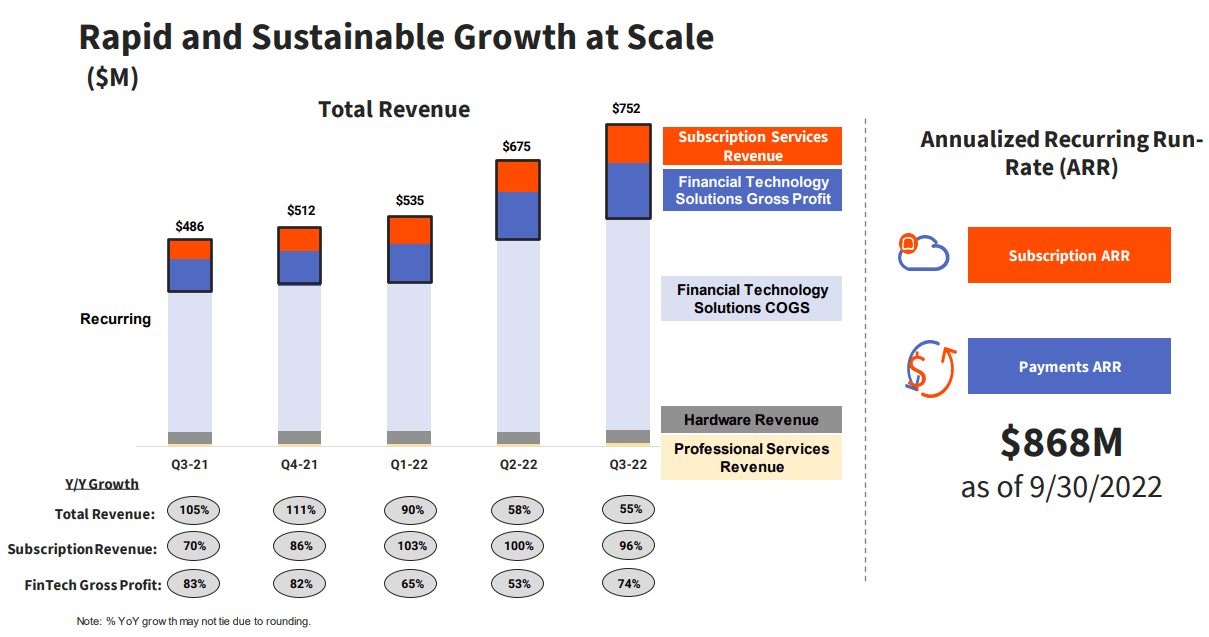

Looking above, there's something important to note before getting into the company's recent performance. This ARR figure. On the earnings call, management specifically talked about the growth rate of subscription revenues, but didn't cite the figure. Additionally, annualized recurring run-rate, when shortened to ARR, sounds a whole lot like annualized recurring revenue for cloud companies. So, when the headline shows $868M in ARR, its eye-popping for a company this size. However, that's not what it is. It's including subscription revenues ($90M in Q3 2022) with seasonally adjusted financial solutions revenue ($628M in Q3 2022) subtracting Toast Capital loan revenues. Here's the actual verbiage from the press release (the italicized stuff most people ignore):

Annualized Recurring Run-Rate ("ARR") is defined as a key operational measure of the scale of Toast's subscription and payment processing services for both new and existing customers. To calculate ARR, Toast first calculates recurring run-rate on a monthly basis. Monthly Recurring Run-Rate ("MRR") is measured on the final day of each month for all restaurant locations live on the Toast platform as the sum of (i) Toast's monthly subscription services fees, which is referred to as the subscription component of MRR, and (ii) Toast's in-month adjusted payments services fees, exclusive of estimated transaction-based costs, which is referred to as the payments component of MRR. MRR does not include fees derived from Toast Capital or related costs. ARR is determined by taking the sum of (i) twelve times the subscription component of MRR and (ii) four times the trailing-three-month cumulative payments component of MRR. Toast believes this approach provides an indication of its scale, while also controlling for short-term fluctuations in payments volume. ARR may decline or fluctuate as a result of a number of factors, including customers' satisfaction with the Toast platform, pricing, competitive offerings, economic conditions, or overall changes in its customers' and their guests' spending levels. ARR is an operational measure, does not reflect Toast's revenue or gross profit determined in accordance with GAAP, and should be viewed independently of, and not combined with or substituted for, Toast's revenue, gross profit, and other financial information determined in accordance with GAAP. Further, ARR is not a forecast of future revenue and investors should not place undue reliance on ARR as an indicator of Toast's future or expected results.

It may be needling, but this feels misleading to me. Recognize there is a huge difference between the figure they are reporting here, and the ARR of, say, Workday ( WDAY ), where it is entirely based on subscriptions from its clients and not transaction volumes of a swath of small and medium-sized restaurants.

{kind=link}

Looking at the most recent quarterly results, all of the numbers are pointed in the right direction and the company is showing pretty monstrous growth in its key metrics. Subscription revenue is not nearly as high as the company's ARR figure, at $90M on the quarter, so I would consider this company as more of a fintech with a solid lock-in with its clients than a cloud software company as far as where it derives the majority of its revenues from.

The one concern to make sure to keep an eye on is transaction volumes are both seasonal and can easily be affected by economic pressures. A significant recession can quickly shift customers' spending habits, and lower gross payment volumes would immediately be felt in the company's annual recurring run-rate .

Management is projecting adjusted profitability by the end of 2023, which is obviously not the same thing as real profitability as far as the balance sheet goes, but would show impressive expense management while the company scales. With $644M on the balance sheet and no long-term debt, I don't currently have any liquidity concerns for the company, and it's early days in their growth story so I'd rather the company focus on taking market share versus making the income statement as pretty as possible.

As you'd expect, the company is printing shares like it's going out of style, and most recently booked $57M in stock based compensation expenses in the most recent quarter. I wouldn't expect that to slow down anytime soon as the company increases its head count. With the minimal operating history for Toast, I didn't bother trying to make graphs to show the number over time, but just recognize dilution is the name of the game with these earlier-stage tech companies.

Putting it all together, Toast has a great runway ahead of it. The company's offering is great, the growth is incredible, and if management hits its targets, we could be looking at a company well on its way to carving out a strong moat in an industry in desperate need of a solid tech solution. There are a ton of moving parts here that could catch a wrench, though. Toast Capital sounds like a good idea until it doesn't. If a recession hits hard enough to significantly impact GPV, it could cause a massive impact to the company's reported numbers. Lastly, management needs to show its ability to keep expenses in check as it continues to chew up market share. I'm on the sideline for now, but I'm definitely interested in the Toast story and will continue to follow. I'm calling it a hold for now.

For further details see:

Toast: The All-In-One Restaurant Solution