UTZ - Tootsie Roll Industries: A Great Company With Limited Upside

Summary

- Tootsie Roll Industries has fared well recently from a fundamental perspective in most respects.

- Long-term, the company will likely continue to do well, and its share price recently has reflected that sentiment.

- Even so, the stock does look to offer limited upside, given how pricey shares are today.

Very few companies in the world are as iconic as Tootsie Roll Industries ( TR ). This candy company, which has been around since 1896, is a sizable player in the confectionery market with a market capitalization of $2.5 billion as of this writing. Recently, financial performance achieved by the company has been promising considering how developed the enterprise is, and that management has not really prioritized growth as of late. Long term, the company's prospects are certainly positive. But this does not mean that investors should consider this an attractive opportunity to buy into. Although the company's shares have outperformed the market over the past few months, those shares are trading at levels that should be considered quite lofty. As such, I've decided to retain my ‘hold’ rating on the business for now.

Attractive fundamental performance

Back in early May of this year, I wrote an article digging into the question of whether Tootsie Roll Industries made sense for investors to invest in. At that time, I reiterated that the company made for a good defensive play for long-term investors. This was because of its sturdy fundamentals and attractive cash flows. The company had also gotten cheaper at that point from a fundamental perspective. But in my opinion, shares were not yet cheap enough to warrant meaningful upside potential for shareholders. And because of that, I ended up keeping my rating on the business a ‘hold’, reflecting my belief that shares would likely perform more or less along the lines of what the broader market would for the foreseeable future. Since then, strong performance, particularly on the top line, has helped shares rise by 7.4%. That compares to the 3% decline experienced by the S&P 500.

{kind=link}

Author - SEC EDGAR Data

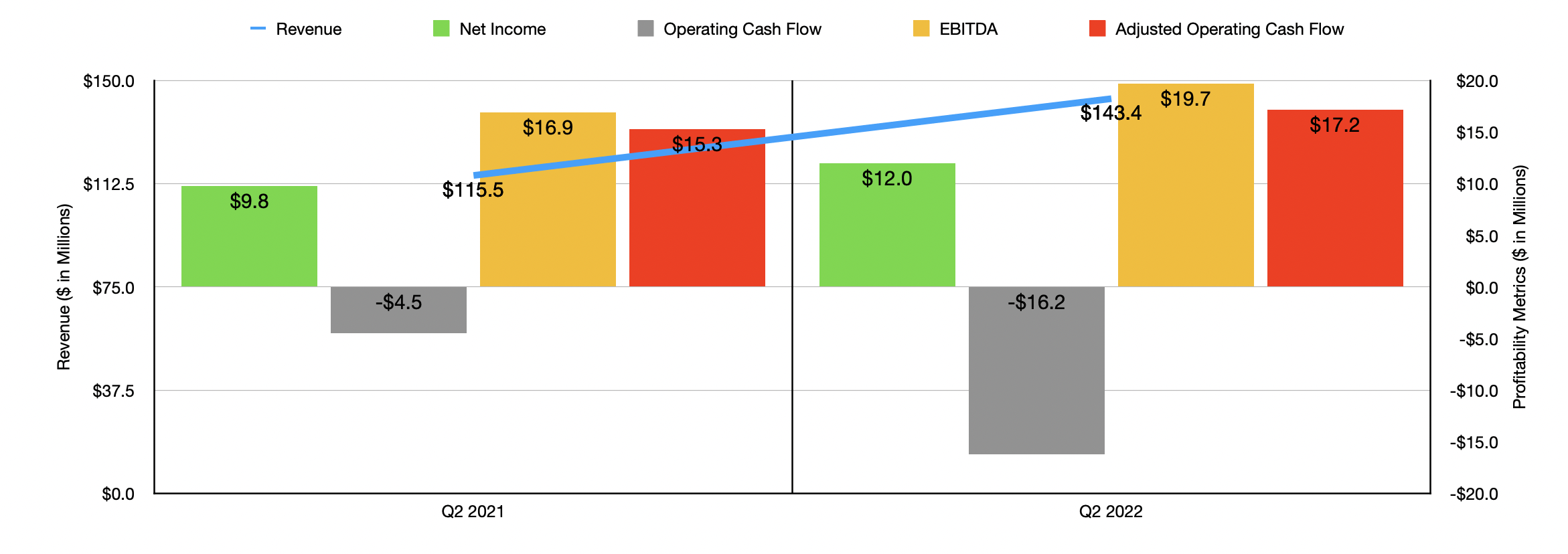

Given this return disparity, I would say that my ‘hold’ call has so far proven to be overly pessimistic. However, it's also important to note that fundamentals can and do change, sometimes for the better and other times for the worse. In this case, strong sales growth seems to have pushed shares higher. To see what I mean, we need only look at financial performance covering the second quarter of the company's 2022 fiscal year. This is the only quarter for which data was not available when I last wrote about the firm but is available now. Sales for that quarter came in strong at $143.4 million. That represents an increase of 24.2% over the $115.5 million generated in the second quarter of 2021.

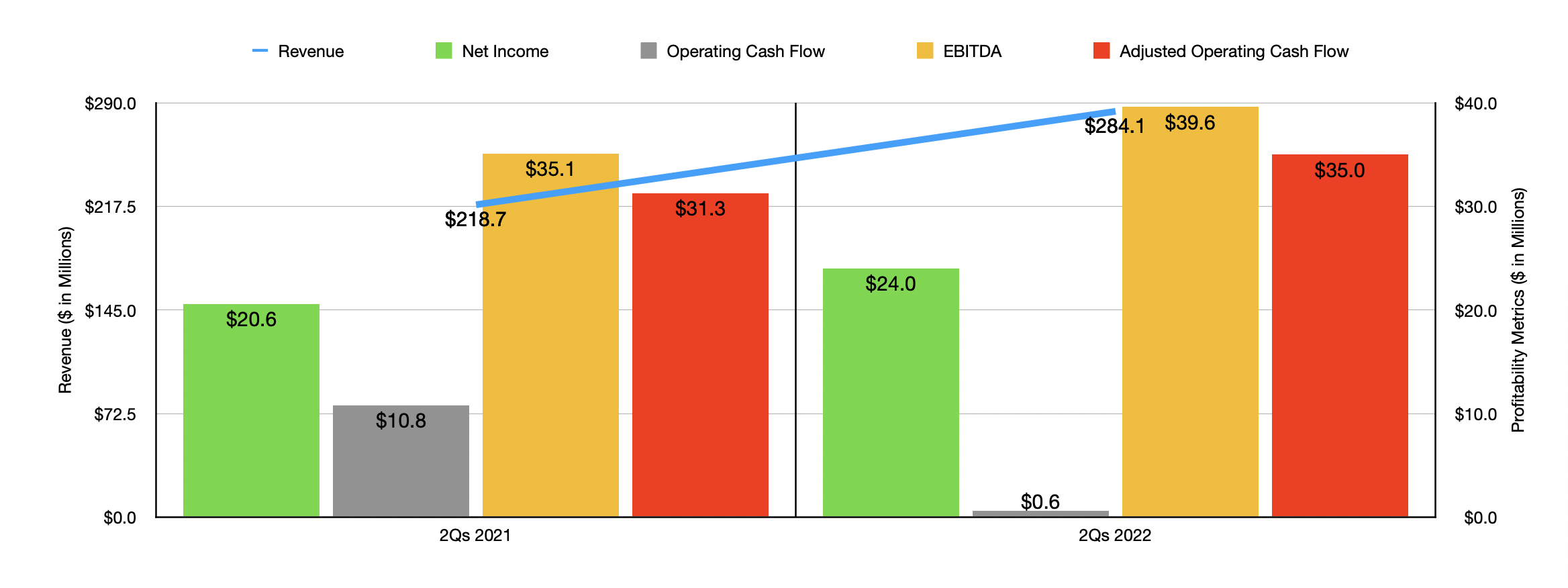

During that quarter, net product sales growth totaled 24%, With strong demand generated by effective sales and marketing programs pushing the company's revenue higher. Management attributed this growth, in part, to consumers returning to more activities and lifestyles that they experienced prior to the COVID-19 pandemic, leading them to be in situations where they were more exposed to the company's products. However, another contributor involved a change in the timing of sales that was rescheduled from the preceding periods due to some supply chain and manufacturing delays the company had experienced. This increase in revenue helped to maintain the company’s year-to-date results, with revenue of $284.1 million for the first half of the year, beating out the $218.7 million generated the same time last year by 29.9%.

{kind=link}

Author - SEC EDGAR Data

With revenue rising, profitability followed suit. Net income in the second quarter of the year came in at $12 million. That's 22.4% higher than the $9.8 million generated one year earlier. Although this is a nice increase in profitability, it is also true that profits rose at a slower pace than revenue did. Management attributed this to significantly higher input costs, with product costs of goods sold climbing from 66.3% of product sales to 67.1%. This was more than offset, thankfully, by a reduction in selling, marketing, and administrative costs from 28% of total revenue to 14.4%. For the first half of the year as a whole, profitability totaled $24 million. That represents an increase of 16.5% over the $20.6 million generated the same time one year earlier.

There are, of course, other profitability metrics that we should pay attention to. Operating cash flow, for instance, fell from negative $4.5 million in the second quarter of 2021 to negative $16.2 million the same time this year. Though if we adjust for changes in working capital, this metric would have risen slightly from $15.3 million to $17.2 million. And over that same window of time, EBITDA for the business also improved, rising from $16.9 million to $19.7 million. These same trends can be seen by looking at the year-to-date results as well, with operating cash flow falling from $10.8 million to $0.7 million, while the adjusted figure for this rose from $31.3 million to $35 million. Meanwhile, EBITDA increased slightly from $35.1 million to $39.6 million.

{kind=link}

Author - SEC EDGAR Data

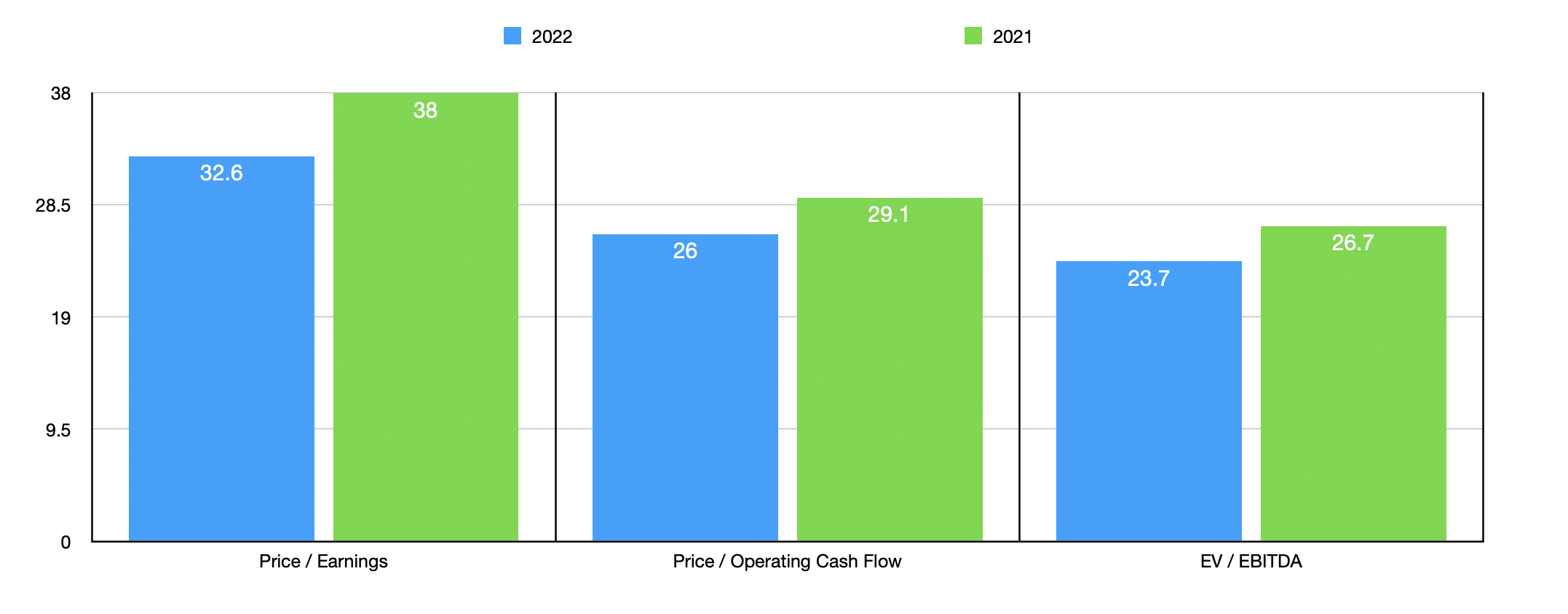

Unfortunately, management does not really offer any guidance when it comes to the 2022 fiscal year as a whole. But if we annualize results experienced so far this year, we should anticipate net income of $76.1 million, adjusted operating cash flow of $95.4 million, and EBITDA of $99.8 million. Using these figures, we can see that the company is trading at a price to earnings multiple of 32.6, at a price to operating cash flow multiple of 26, and at an EV to EBITDA multiple of 23.7, all of course on a forward basis. If, instead, we were to rely on 2021 figures, these multiples would be 38, 29.1, and 26.7, respectively. While these numbers are awfully high on an absolute basis, they aren't that unreasonable for the space that Tootsie Roll Industries operates in. Using the forward figures, I compared the company to five similar firms. On a price-to-earnings basis, four of these companies had positive results, with multiples of between 21.3 and 61.1. Using the price to operating cash flow approach, the range for the four firms was between 12.1 and 67.1. In both cases, two of the four companies were cheaper than Tootsie Roll Industries. Using the EV to EBITDA approach, the range was between 11.2 and 25.6, with our prospect more expensive than all but one of the firms.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Tootsie Roll Industries |

| 32.6 |

| 26.0 |

| 23.7 |

| Hostess Brands ( TWNK ) |

| 25.0 |

| 13.8 |

| 14.2 |

| Utz Brands ( UTZ ) |

| N/A |

| 31.9 |

| 18.9 |

| J&J Snack Foods ( JJSF ) |

| 61.1 |

| N/A |

| 25.6 |

| TreeHouse Foods ( THS ) |

| 52.8 |

| 67.1 |

| 11.2 |

| B&G Foods ( BGS ) |

| 21.3 |

| 12.1 |

| 13.0 |

Takeaway

As I have said before, Tootsie Roll Industries is a quality company and a great defensive play. If you are looking for something to protect you if the market goes down, this is a good candidate to consider given that it is a major player in the industry and has robust and attractive fundamental performance. Having said that, shares are incredibly pricey on an absolute basis, while being more or less fairly valued compared to similar firms. In all, this leads me to take something of a neutral stance on the company, keeping with the ‘hold’ rating I had on it previously.

For further details see:

Tootsie Roll Industries: A Great Company With Limited Upside