META - Top 5 Stocks To Consider Avoiding As We Begin 2024

2024-01-01 08:30:00 ET

Summary

- I discuss the top five stocks investors should avoid buying at the current levels unless we get a steep pullback.

- It's important to consider that market outperformance could be challenging as the market rotates to other stocks.

- While the quality of these five stocks is high, they shouldn't be regarded as a buy at any price.

- I show you how I assess these stocks and help you make sense of my approach.

I presented my 2024 outlook in mid-December 2023, discussing the areas of focus investors should consider when structuring or rebalancing their portfolio in 2024. While I don't usually provide real-time stock picks outside of my service, I would like to provide an analysis to help investors think about some of the stocks I would be wary about as we prepare for the year ahead.

The S&P 500 ( SPX ) ( SPY ) has outperformed Wall Street strategists' bearish prognostications, finishing the year up 25%. The Nasdaq ( NDX ) ( QQQ ) has also powered higher, up 44%. The Dow Jones Industrial ( DJI ) (DJX) burst into a new all-time high three weeks ago and finished the year up 14% YTD.

As a result, with the broad market doing a surging run to finish the year, bearish prognosticators likely found nowhere to hide as they reassessed why they had gotten the market sentiments so wrong! With the market starting 2024 on the right footing, following a stunning 2023 that dumbfounded most Wall Street strategists, I believe investors will need to be more cautious on stock selection, as I argued in my 2024 outlook.

These are some of the top stocks I would avoid adding at the start of 2024. Avoiding doesn't necessarily mean selling or shorting. It means I will be careful to initiate or add exposure at the current levels. My assessment is based on several metrics I usually look at when assessing any opportunity. Seeking Alpha Quant's factor ratings often feature as one of my primary tools. I then assess the economic moat ratings based on Morningstar's approach and consider their fair value estimates. I then use my internal valuation metrics (relative, discounted cash flow, sum-of-the-parts) and compare them against the suggested ratings from Seeking Alpha and Morningstar.

After considering these, I look into the stock's price action analysis to determine whether the risk/reward is attractive enough. I want to assess whether the current buy levels could indicate a value trap. I also want to evaluate whether the current buy levels could be over-optimistic, suggesting I should await a pullback.

I've recently presented in several articles why waiting for a healthy pullback and not joining the FOMO crowd are prudent strategies to outperform the market consistently. You can consider my recent articles on Micron ( MU ), Crocs ( CROX ), RTX Corporation ( RTX ), and Charles Schwab ( SCHW ) for a start to understanding my perspective.

Should We Avoid The Magnificent Seven?

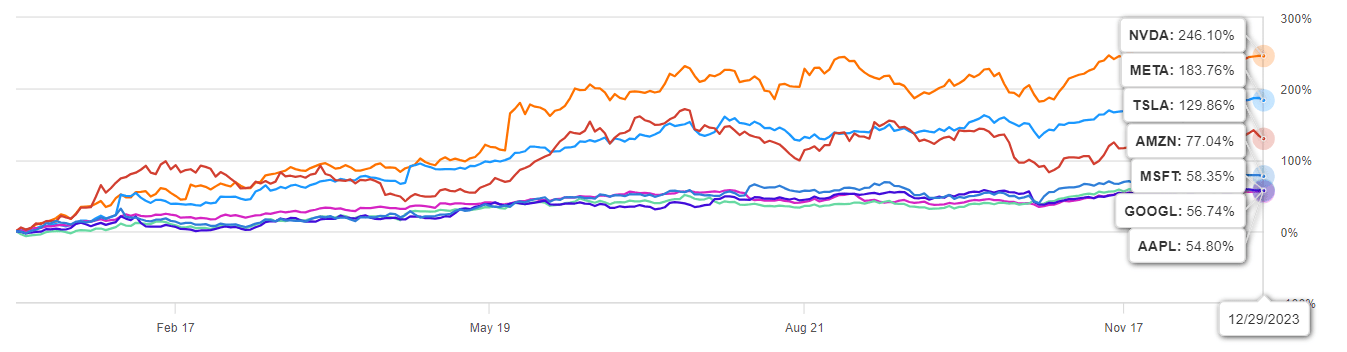

The Magnificent Seven comprises Apple ( AAPL ), Microsoft ( MSFT ), Google ( GOOGL ) ( GOOG ), Amazon ( AMZN ), Nvidia ( NVDA ), Tesla ( TSLA ), and Meta Platforms ( META ). These stocks have outperformed the S&P 500 significantly as a group, notching a return of 115% YTD. Therefore, it's timely to reassess whether investors should avoid adding all or just some of them as the market considers their thesis in the year ahead.

Magnificent Seven YTD total return % (Seeking Alpha)

{kind=link}

Nvidia, Meta, and Tesla led with triple-digit YTD gains. It easily dwarfed the 50+% upside MSFT, AAPL, and GOOGL delivered. As a result, the contrarian in us might be curious about whether the laggards in the Magnificent Seven could outperform. At the same time, the top performers might take a break, allowing the rest of the market to catch up.

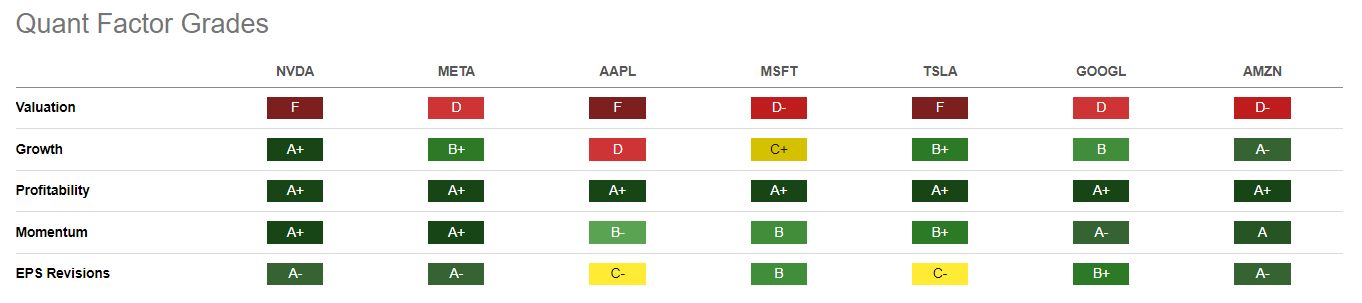

Magnificent Seven Quant Grades (Seeking Alpha)

{kind=link}

If we consider the Quant grades for the Magnificent Seven, it's clear that they are generally not cheap. Their relative valuation grades suggest they trade at a premium against their peers, with the most attractive valuation grade assigned "D."

However, Aside from AAPL and MSFT, they also post more robust growth grades than their peers. All are quality companies with best-in-class "A+" profitability grades. As a result, investors should continue to hold these stocks as core positions, but that doesn't mean they should be added at any price. While quality doesn't come cheap, we must be circumspect about assessing attractive risk/reward profiles.

| Ticker | Name | Price/Fair Value |

|---|---|---|

| AAPL | ||

| Apple Inc | ||

| 1.20 | ||

| TSLA | ||

| Tesla Inc | ||

| 1.18 | ||

| META | ||

| Meta Platforms Inc | ||

| 1.10 | ||

| NVDA | ||

| NVIDIA Corp. | ||

| 1.03 | ||

| MSFT | ||

| Microsoft Corp. | ||

| 1.02 | ||

| AMZN | ||

| Amazon.com Inc | ||

| 0.98 | ||

| GOOGL | ||

| Alphabet Inc Class A | ||

| 0.87 |

Morningstar Price/Fair value ratio.

Morningstar's wide moat ratings for all (except for Tesla) corroborate the Magnificent Seven's high-quality competitive advantages. However, with the exception of GOOGL, all of them are assessed to be generally overvalued or fair valued at the current levels. With that in mind, investors who have not managed to join their rallies in 2023 (due to over-pessimism) are urged to consider waiting for more attractive buy levels.

I would consider avoiding AAPL, NVDA, and MSFT at the current levels, as their price action aren't constructive. Unless a steep pullback occurs, I wouldn't be keen to add more exposure. However, I'm generally in favor of my GOOGL, AMZN, and META positions, and I would consider adding more in 2024.

AAPL's "D" growth grade suggests investors must be careful about expecting its iPhone-driven upside to continue further. While the impending retail launch of its Vision Pro could drive investor sentiments in 2024, I don't expect the product to be earnings accretive in the near term. As a result, the recovery of AAPL in 2023 could find more impediments in 2024 as the market reconsiders whether AAPL is already overvalued.

Nvidia must prove that it can continue outperforming the upgraded analysts' expectations after notching consecutive beats. However, with Intel ( INTC ) and AMD ( AMD ) lifting their game to capture a slice of Nvidia's market share, CEO Jensen Huang and his team are under immense pressure to justify Wall Street's outlook, even as they fend off the more intense competitive threats. I believe the market wouldn't be "compassionate" to anything less than stellar from Nvidia in 2024.

Microsoft has benefited from its AI partnership with OpenAI. The recent internal troubles at OpenAI demonstrated Microsoft's leverage as it looks to cement its market leadership in the generative AI space. Investors must remain on the lookout for the ambitions of Amazon and Google as they look to unseat Microsoft's enterprise leadership in the cloud computing space. Amazon Web Services, or AWS, is determined to make sure it doesn't give up its IaaS lead as Microsoft looks to offer a more competitive overall package in its partnership with OpenAI. In addition, Google will be keen to demonstrate that it can gain market share while generating profitable growth. However, with GOOGL's valuation at a relatively attractive level, the market likely hasn't re-rated GOOGL fully, ascribing execution risks in its quest to close the gap on MSFT and AMZN.

For TSLA, it's a mixed bag. While I believe the low $200s level should hold, buyers must demonstrate conviction to break decisively above the $280 level. Tesla is expected to beat its full-year deliveries forecast of 1.8M cars for 2023. However, the market likely expects the Elon Musk-led company to demonstrate whether its plans for a mass-market car could accelerate as it looks to fend off BYD's ( BYDDF ) challenges in the global EV market. With BYD stepping further in its ambitions to penetrate the European market, Tesla needs to bolster its ability to scale quickly against BYD's incredible industrial prowess and vertically integrated supply chain.

Should We Avoid Stocks Linked To Weight Loss Drugs?

The success of the biopharma stocks linked to the success of the weight loss drugs has lifted their valuations to significant highs. As a result, it's arguable that the market could have priced in over-optimism on their prospects, which could cause investors to be disappointed if they don't execute accordingly.

I've covered Eli Lilly ( LLY ) and Novo Nordisk ( NVO ) recently, explaining why I'm cautious about investors who missed their surge in 2023 to be wary (see here and here ). You can refer to these articles for more in-depth information.

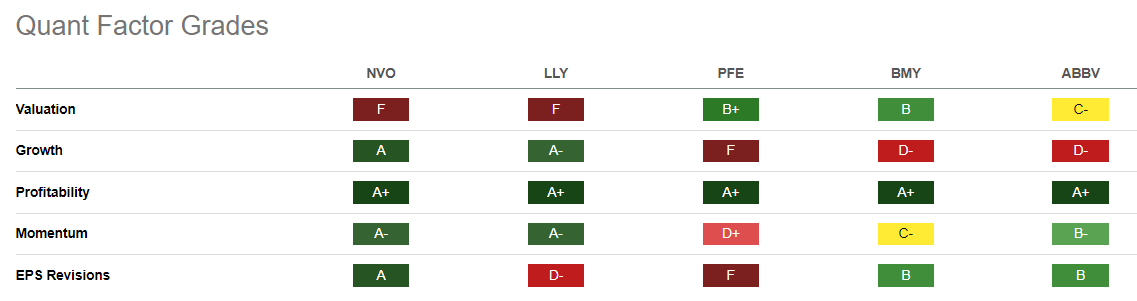

LLY & NVO Quant Grades Vs. Peers (Seeking Alpha)

{kind=link}

The bifurcation in the Quant metrics between LLY, NVO, and their peers is significant. As seen above, with NVO and LLY positioned for growth, it has led to a substantial surge in 2023, with both stocks up more than 50% YTD. In LLY's case, it finished the year up more than 60% YTD.

However, the "F" valuation grades for LLY and NVO suggest caution is necessary. Morningstar's price/fair value ratings corroborate my thesis, with both stocks assessed to be overvalued by about 30%.

Some investors could point to their robust "A-" momentum grade to vindicate the market's enthusiasm. Sure, but do note that the stocks potentially top out when their momentum is generally stronger and not within the "D" or "F" range. In other words, we must assess possible market tops carefully based on price action (since the market is forward-looking) and not just look at momentum grades.

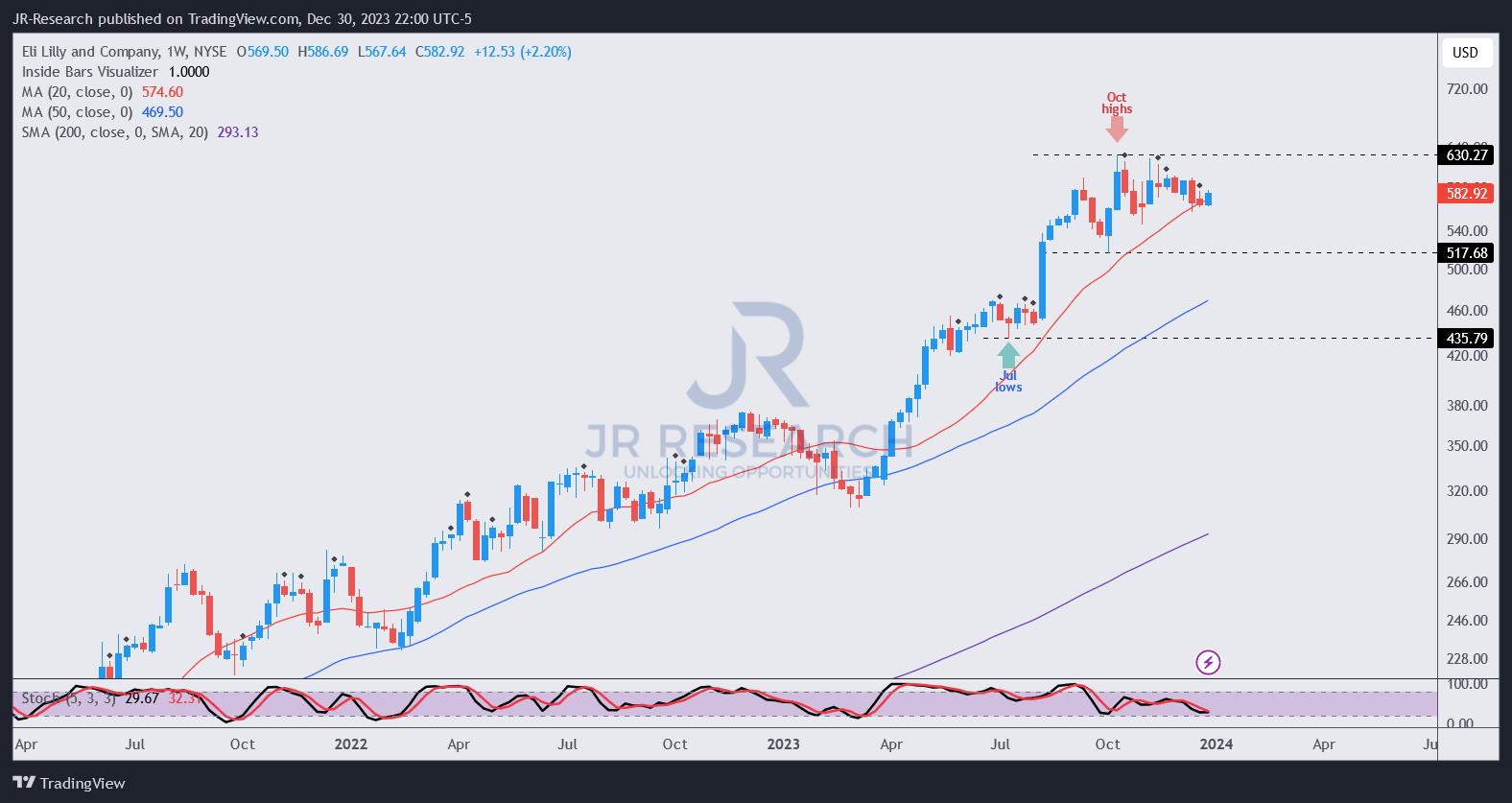

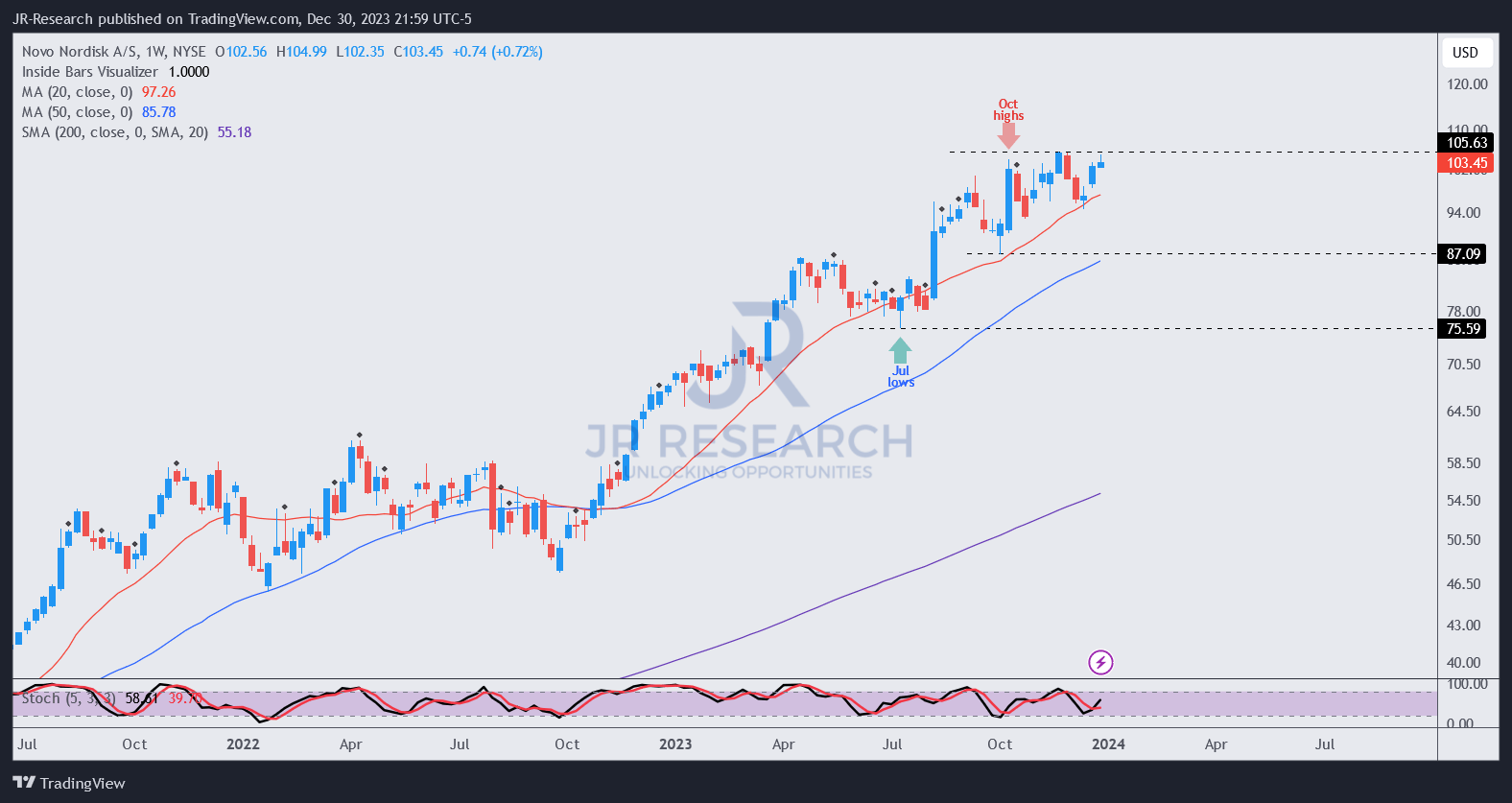

LLY price chart (weekly) (Seeking Alpha) NVO price chart (weekly) (TradingView)

{kind=link}

{kind=link}

The price action of both stocks suggests underlying rotation had already occurred since October 2023 as they topped out. Buyers are still trying to maintain their upward bias, although the failure to break decisively above their respective highs suggests caution is justified.

Both companies have given their investors much to savor over the past five and ten years. Note that NVO delivered a 5Y and 10Y total return of 38.2% and 24.1%, respectively. Compared to its YTD total return of more than 50%, investors need to ask whether a return to the long-term average is well overdue.

For LLY, it has delivered a 5Y and 10Y total return of more than 40% and 30%, respectively. Compared to its YTD return exceeding 60%, continued optimism in expecting outperformance seems unlikely.

As my recent LLY article highlighted, competitors are also " developing weight loss drugs," including oral therapies. As a result, big biopharma peers recognize the appeal of these drugs and are likely determined to partake in the market's growth. Therefore, I don't believe it's reasonable to assume that Lilly and Novo Nordisk could continue dominating the market without facing intense challenges that could affect their pricing levers moving ahead.

While the current supply-constrained market could offer near-term advantages to both companies, investors need to ask whether their implied overvaluation could have reflected these tailwinds. I believe the market has astutely priced in excellent execution from these two companies over the next few years, suggesting any less-than-stellar performance could cause investors to take profits and reallocate their portfolio in a hurry. As a result, investors looking to go on board at the current levels are likely late.

Therefore, I would consider avoiding them unless I assessed a well-deserved pullback in NVO and LLY in 2024 to dissipate the froth.

Takeaway

The 2023 winners listed above have outperformed the market and their peers significantly. While I hold a core position in most Magnificent Seven stocks, I would be careful about adding MSFT, AAPL, and NVDA at the current levels.

For the healthcare plays, I assessed that investors must be cautious about the valuation bifurcation between NVO, LLY, and their peers. Their relative over-optimism/pessimism shouldn't be expected to be sustained in 2024 as the market reallocates.

These are the top five stocks I urged investors to consider avoiding as 2024 begins in earnest.

For further details see:

Top 5 Stocks To Consider Avoiding As We Begin 2024