CA - Toronto-Dominion And Scotiabank: Debt Cycle Nears Its End

2023-06-28 08:30:00 ET

Summary

- As excessive debts collide with higher interest rates, the Canadian economy may be headed for deleveraging.

- In extreme cases, amortization periods for Canadian mortgages have reached 70-90 years.

- I'll assess the collapse of TD's First Horizon deal, potential loan losses, and balance sheet liquidity.

- In the decade ahead, I project returns in the range of 8% per annum for TD and BNS (Spoiler alert: Rating upgrade).

The End Of Canada's Long-term Debt Cycle

In Canada, debt has been growing faster than income for many years now. I believe Canada is now nearing the end of its long-term debt cycle, an event which only comes around every 75-100 years.

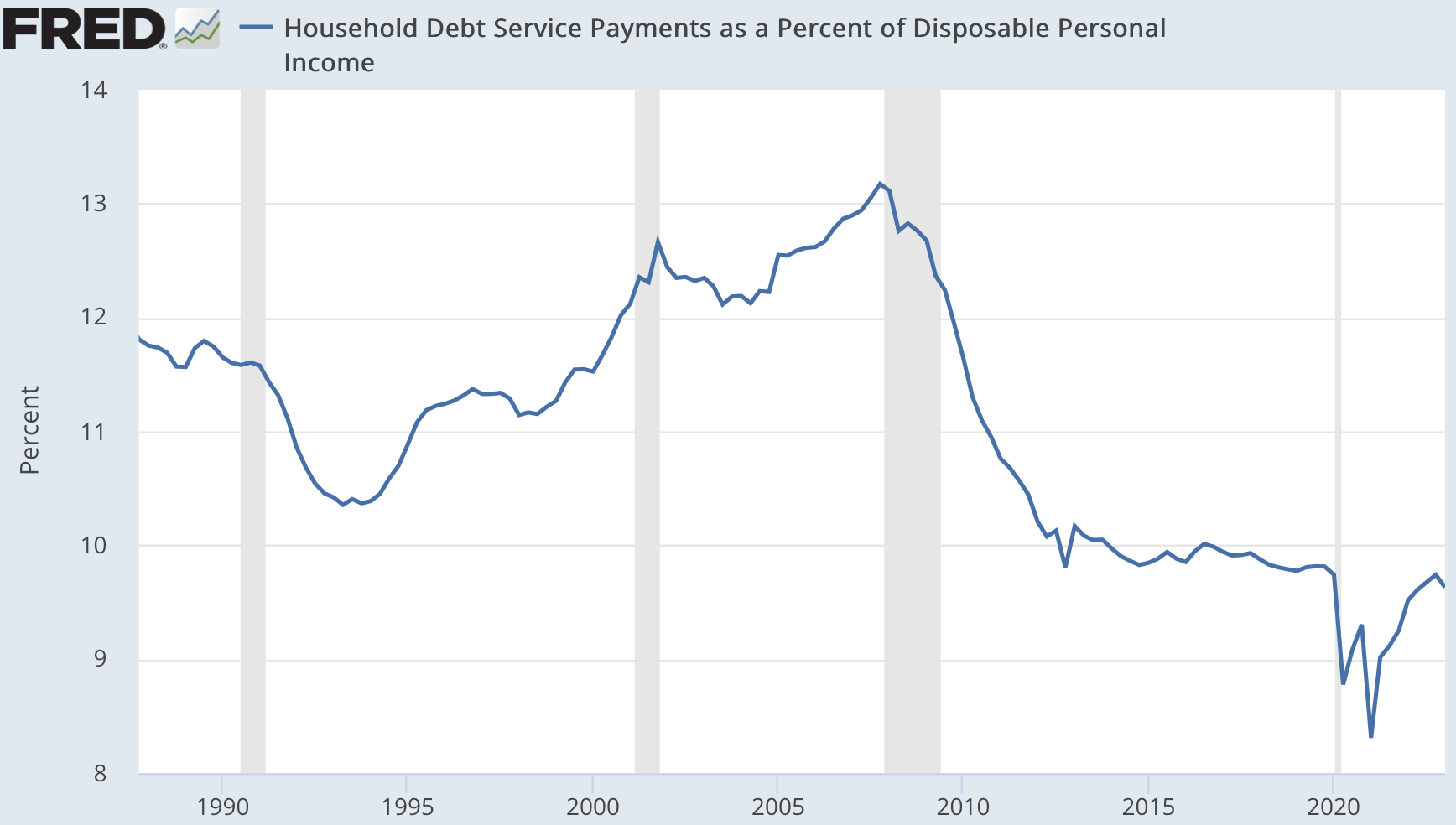

Canadian households recently reached a debt service to disposable income ratio of 14.9% , meaning 15% of household income is being used for debt repayment. This is higher than levels reached in the United States right before the great financial crisis and the meltdown of several U.S. banks in 2009. In Q4 2007, the United States had a household debt service ratio of 13.2% :

U.S. Household Debt Service As Payments A Percentage Of Disposable Income (FRED)

{kind=link}

A Look At Canada's Ballooning Debt

In my estimation, the risks in Canada are elevated. This may be why you see the likes of Bank of Nova Scotia ( BNS )(BNS:CA) and The Toronto-Dominion Bank ( TD )(TD:CA) yielding 6.4% and 4.7%, respectively. I foresee a hard landing for the Canadian economy as excessive debts collide with higher interest rates. This was discussed in my prior articles on TD Bank. Below is a look at the accumulation of debt in Canada over the past 50 years.

Canada's private debt to GDP:

Private Debt As A Percentage Of Nominal GDP - Canada (CEIC)

{kind=link}

Canada's household debt to disposable income:

Household Credit Market Debt To Disposable Income - Canada (Trading Economics)

{kind=link}

Debt cannot grow faster than income forever. This trend will eventually reverse, and the reversal is often sparked by a risk-off deleveraging, like we saw in the United States and Europe in 2009.

Now, let's rewind to how this all started. Interest rates have declined somewhat steadily since the 1980s, making debt more affordable and incentivizing businesses and consumers to leverage up. Canadian banks have grown alongside this debt accumulation because more debt equals more assets and more customers paying interest:

The problem is, interest rates are now rising due to inflationary pressures, some of which are structural. Interest rates in Canada may have bottomed out in 2020, reaching levels not seen in 5000 years:

5000 Years Of Interest Rates (Business Insider)

I would not rule out structurally higher interest rates over the next 50 years. Following the end of the world's long-term debt cycle, in the 1930's, interest rates marched higher for 50 years (Ending in the 1980s).

Higher Interest Rates - A Blessing And A Curse

On one hand, higher interest rates are a blessing for banks because they can lend out money at higher rates, causing net interest margins to rise. Typically, the more zero-interest-bearing deposits customers have sitting in chequing accounts, the more net interest margins rise. This hasn't helped out much at Bank of Nova Scotia because only 5% of its deposits are non-interest bearing, and the bank's online subsidiary, Tangerine, has been offering new customers relatively high interest rates . However, at TD Bank, net interest margins increased from 1.56% in 2021 to 1.76% in Q2 2023 .

Now, the curse; higher interest rates make it more difficult for customers to service their loans. This is especially true for customers with variable and fluctuating interest rates. In Canada, households can typically choose between 5-year fixed mortgages and variable mortgages. Those who took on variable-rate mortgages are now getting crushed by higher interest rates. Many of these customers would already be in default, but instead, Canadian banks are allowing customers to pay only interest (And no principal) on their mortgage loans. Paying only interest means you are effectively renting your house from the bank. In extreme cases, amortization periods for Canadian mortgages have been stretched out to 70-90 years, Victor Tran (From Ratesdotca) told BNN Bloomberg . As for 5-year fixed mortgages, The Globe And Mail reported:

"The Bank of Canada estimates that mortgage borrowers who renew their loans over the next few years will see a spike of 20 per cent to 40 per cent in their monthly payments."

This increases the risk of default, but thus far, banks have chosen to restructure loans that CMHC doesn't insure. As Ray Dalio once said , "Lenders would rather have a little of something than all of nothing." In this case, banks are getting their money back later than expected. As for defaults, Canada's Tolga Yalkin of OSFI (Canada's banking regulator) said :

“We wouldn’t be doing our job as the prudential regulator if we assume past credit performance will be future. And low delinquency rates can quickly turn, as we saw in the 2008 global financial crisis in the U.S.”

In my opinion, with debt service costs stretched so far, the risk of default stretches beyond uninsured mortgages to credit card loans, business loans, and lines of credit.

The Collapse Of TD's First Horizon Deal

TD planned to acquire First Horizon Corporation ( FHN ) for $13.4 billion dollars. Thankfully for TD shareholders, that acquisition fell through. It was intercepted by U.S. regulators. This would have been a terribly timed acquisition, in my opinion. First Horizon's stock has since fallen off a cliff alongside fellow U.S. regionals:

First Horizon is not well capitalized, in my view. Dodd-Frank regulation was rolled back in 2018 for America's smaller banks, those with less than $250 billion in assets. These banks are now at risk of deposit runs due to their tiny slivers of liquidity. Apparently, TD was willing to take on this risk at a $13.4 billion valuation; the equity of First Horizon now has a valuation of less than $6 billion in market cap. This is a snippet of the capital allocation chops at TD Bank.

Do Canadian Banks Have Enough Liquidity?

| ___________________ |

| Bank of Nova Scotia |

| Toronto-Dominion Bank |

| Liquidity Coverage Ratio |

| 131% |

| 144% |

| CET1 Ratio |

| 12.3% |

| 15.3% |

| Loans To Deposits |

| 81% |

| 71% |

| Assets To Equity |

| 17.4 |

| 16.6 |

Although TD and Scotiabank meet the Canadian regulatory requirements of a 100% liquidity coverage ratio and a 11% CET1 ratio, I wouldn't mind seeing Scotiabank increase its liquidity.

Also, these banks are far less liquid than banks South of the border (In the United States) in terms of their loans to deposits and assets to equity. Canadian banks have enjoyed higher returns on equity due to this leverage.

I'm not overly worried about fleeing deposits. Because there are so few Canadian banks, deposits tend to move back and forth among the big banks, reducing the risk of deposit flight.

In my view, the loan portfolios are the main risk. What happens if these loans blow up? For example, what would happen if 10% of these loans went bad, and resulted in losses averaging 30% of principal? Scotiabank would lose $17 billion (In excess of its allowance) plus forgone interest and TD would lose $19 billion (In excess of its allowance) plus forgone interest. This would wipe out net income and produce a large loss, representing risk to the dividends and to your ownership percentage (In the case these banks decide to issue equity to bolster their balance sheets). Given where Canada's debt bubble stands, I wouldn't rule out this outcome.

Long-term Returns

In terms of the tailwinds, I like that TD has a presence in the United States where household debt service ratios are much lower. I also like Bank of Nova Scotia's online bank, Tangerine, which seems to be resonating with Canadian youth due to its high interest savings accounts and zero fee checking accounts. This is made possible by Tangerine's capital light model. I also like Scotiabank's large international presence, including its presence in Latin America.

On the headwinds side, if Canadian banks are forced to improve their balance sheets and lend more conservatively, growth could suffer. Also, should CMHC fail in the next recession, there could be changes in the Canadian financial system. A deleveraging in the consumer and corporate sector could weigh on growth for years. Moreover, I would not be surprised to see trading fees come under pressure given the moves we've seen in the industry towards zero commission trades.

In the decade ahead, I project total returns of roughly 8% per annum for TD and BNS:

| U.S. Security |

| TD |

| BNS |

| Current EPS |

| $5.96 |

| $5.10 |

| Current Dividend |

| $2.90 |

| $3.20 |

| Compound Annual Growth Rate |

| 2% |

| 1% |

| Year 10 EPS |

| $7.25 |

| $5.63 |

| Terminal Multiple |

| 12x |

| 11x |

| Year 10 Price Target |

| $87 |

| $62 |

| Annualized Returns ( Dividends Reinvested ) |

| 8% |

| 8.5% |

Note: This is a base-case estimate. The compound annual growth rate is for dividends and earnings.

My projected growth rates look low, but remember that this is a base-case scenario. The United States and Europe faced the end of their long-term debt cycle in 2008.

The history of EPS growth coming out of such an event is not good:

Notice that JPMorgan Chase, which was headed by a brilliant manager in Jamie Dimon, avoided this outcome and grew tremendously. If Scotiabank or TD should run into a brilliant CEO, the upside could materialize.

The Bottom Line

The end of Canada's long-term debt cycle signals problems ahead for TD and BNS. Investors shouldn't assume these banks will continue to grow like they have in the past. The track records of European and U.S. banks, whose debt cycles peaked in 2008, tell the tale. Canadian mortgages are being stretched out to longer amortizations to avoid default, but the real losses could come in the form of consumer and corporate loans. Investors in TD and BNS should manage their exposure and have a long time horizon. Don't rule out the possibility of negative earnings, dividend cuts, and share dilution in the short term. But, looking out 20 to 30 years, I see Canada prospering and Canadian banks having substantially more earnings and equity. I'm upgrading TD to a "Hold" and have a "Hold" on BNS as well.

For my top pick among banks stocks, check out my latest "Strong Buy" bank here .

Until next time, happy investing!

For further details see:

Toronto-Dominion And Scotiabank: Debt Cycle Nears Its End