BMO:CC - Toronto-Dominion Bank: Best Pick Among Canada's Major Banks

Summary

- The Toronto-Dominion Bank reported solid fiscal 2022 results although not all business segments contributed to growth.

- Financial stability is always an issue when talking about banks, but the Toronto-Dominion Bank seems to be a great pick although the Canadian housing market might be hot.

- Due to two acquisitions, the Toronto-Dominion Bank increased its U.S. presence.

- The stock appears to be overvalued already and among the major five Canadian banks, Toronto-Dominion Bank could be the best pick right now.

(Note: All amounts in Canadian dollars unless otherwise indicated)

Canadian banks should be on the watchlist of every dividend investor and on the watchlist of every long-term investor in high-quality businesses. And without much doubt, the Toronto-Dominion Bank ( TD ) is a high-quality business – similar to the other major Canadian banks. But while I covered the Bank of Nova Scotia ( BNS ) in November 2022 and the Royal Bank of Canada ( RY ) in January 2023, my last article about the Toronto-Dominion bank was published in August 2022 and an update seems more than overdue.

At the time of publication, I was rather neutral, but the bank clearly outperformed the S&P 500 in the meantime (58% total return including dividends vs. 21% price increase for the S&P 500 ( SPY )). I still have problems to articulate a clear opinion about banks: On the one hand these stocks are really cheap and, in my opinion, we should take advantage of opportunities when they present themselves. On the other hand, I am really worried about the economic hurricane that might come. And even if we are not talking about a hurricane but only a “normal” recession, I still don’t want to buy banking stocks at the eve of a global recession. Nevertheless, let’s start by looking at the full year results.

Solid Full Year Results

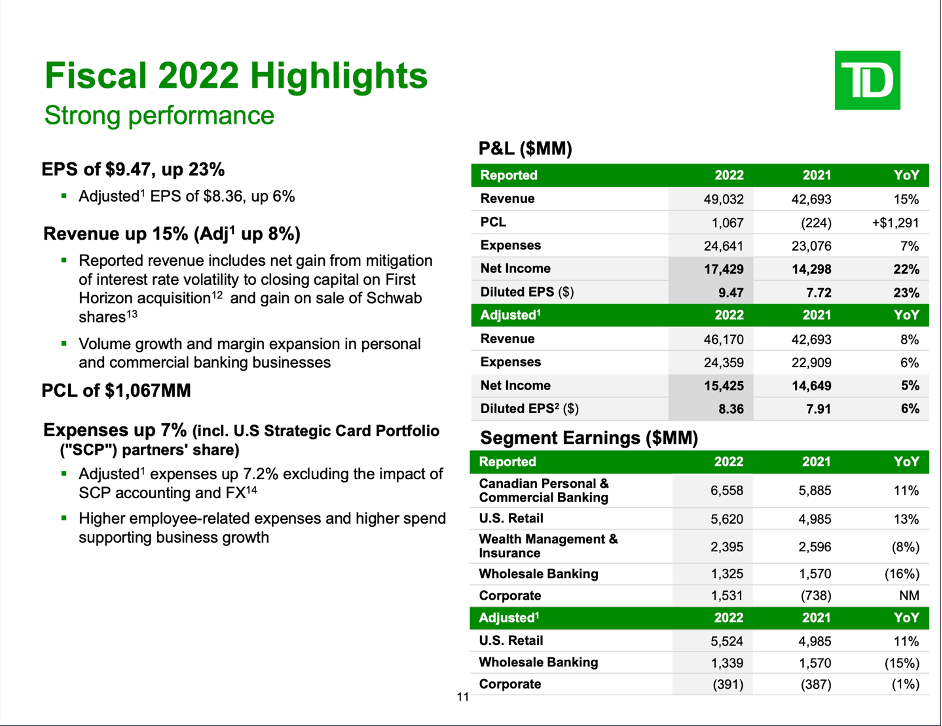

The Toronto-Dominion Bank could report strong results for fiscal 2022. Total revenue increased from $42,693 million in FY21 to $49,032 million in FY22 – resulting in 14.8% year-over-year growth. And net interest income increased 13.4% year-over-year from $24,131 million in FY21 to $27,353 million in FY22 while non-interest income increased 16.8% YoY from $18,562 million in FY21 to $21,679 million in FY22. And like most other banks, the Toronto-Dominion Bank already increased provision for credit losses and instead of a recovery of credit losses of $224 million in the previous year, provision for credit losses was $1,067 million in FY22. But despite the higher provision for credit losses, diluted earnings per share increased from $7.72 in FY21 to $9.47 in FY22 – resulting in 22.7% year-over-year growth.

{kind=link}

Toronto-Dominion Q4/22 Presentation

When looking at the different segments, we get a rather mixed picture. While the two biggest contributors to earnings – Canadian Personal & Commercial Banking as well as U.S. Retail – both reported double-digit growth rates, Wealth Management & Insurance as well as Wholesale Banking each reported declining earnings.

Financial Stability

Solid growth rates for the top and bottom line are great and certainly important for investors, but it is even more important to look at the financial stability as high growth rates can become meaningless when a bank will tumble in times of economic distress. This is especially important, as I see dark clouds on the horizon. It might come as no surprise to you that I also talked about the financial stability in my recent articles about the Royal Bank of Canada as well as the Commonwealth Bank of Australia ( OTCPK:CBAUF ). And although the Canadian banks can’t match the impressive financial health metrics Australian banks can report (the CET1 ratio for example), Canadian banks can still be seen among the safest banks in the world.

{kind=link}

Toronto-Dominion Q4/22 Presentation

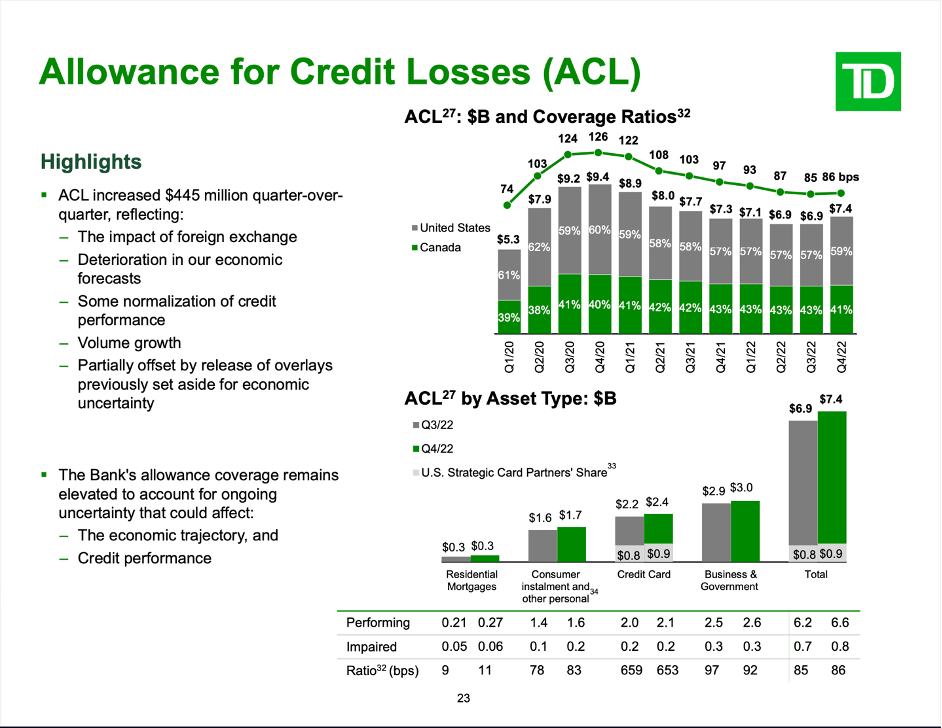

As mentioned above, the provision for credit losses were higher again than in previous quarters. And the allowance for credit losses is also higher, but certainly no reason to worry. Allowance for credit losses increased $445 million quarter-over-quarter and is now at $7.4 billion.

Additionally, the common equity tier 1 capital ratio increased from 15.2% in the same quarter last year to 16.2% this year and although it can’t match the ratio of the Commonwealth Bank of Australia (last reported number: 18.6) it is still one of the highest in the world. We can also look at the loan-to-deposit ratio and with total loans being $831 billion and total deposits being $1,230 billion, we get a ratio of 68% and usually every ratio below 80% is seen as acceptable. And when looking at the loan-to-asset ratio (total assets being $1,918 billion) we get a ratio of 0.43. In this case, every ratio below 0.6 can be seen as acceptable.

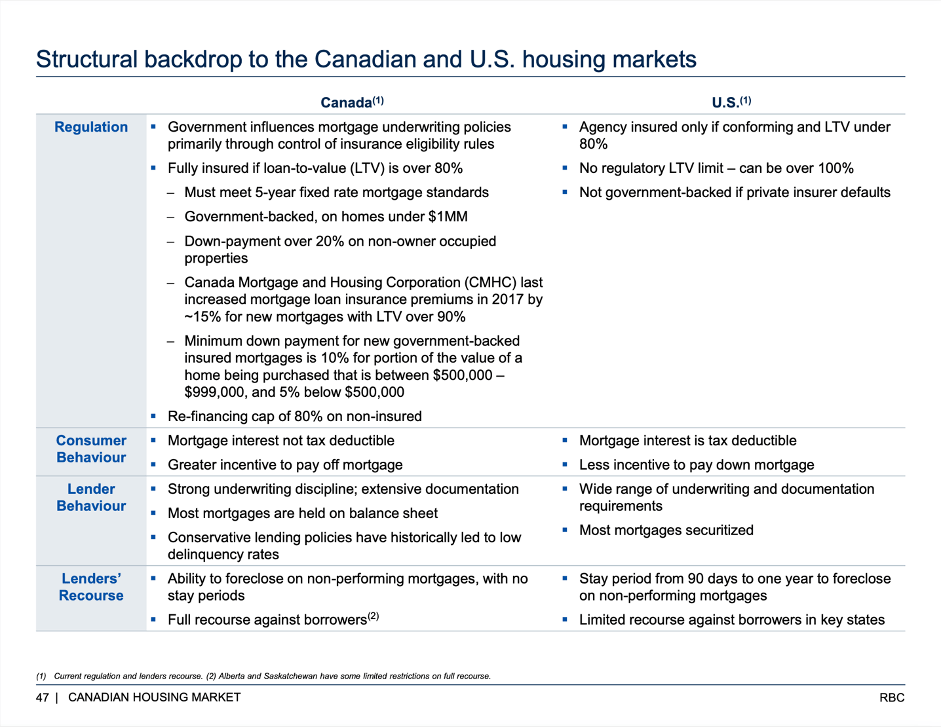

In my last article about the Royal Bank of Canada, I talked about the Canadian housing market in more detail as the extremely expensive Canadian housing market is often seen as problematic. And while we can see the high prices as well as the fact that interest rates are usually only fixed for 5 years (but that is also the case in my other countries around the world) as problematic, we should not spin these facts as being too negative. The Canadian housing market should be closely watched, but it seems unlikely we will see a repetition of what happened in the United States in 2007. The Canadian housing market has the (negative) potential for Canadian banks to lead to some bad quarters, but I don’t think we see the Canadian banks tumbling. The reason can be found in the structural backdrop to the Canadian housing market (for example, mortgages with less than 20% down payment must be insured).

{kind=link}

Royal Bank of Canada Q4/22 Presentation

And the higher quality of the Canadian housing market is also visible in the much lower default rates during the last few decades (for example compared to the United States).

{kind=link}

Royal Bank of Canada Q4/22 Presentation

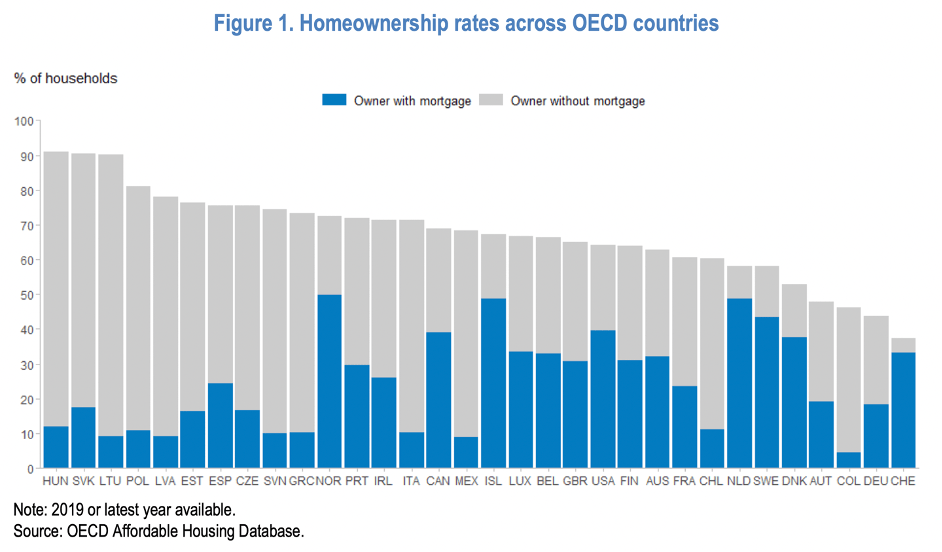

But we still must consider that Canada – together with the United States – has one of the highest percentages of households with a mortgage (about 40% to 45% of total households).

{kind=link}

OECD Working Paper "Mortgage finance across OECD countries"

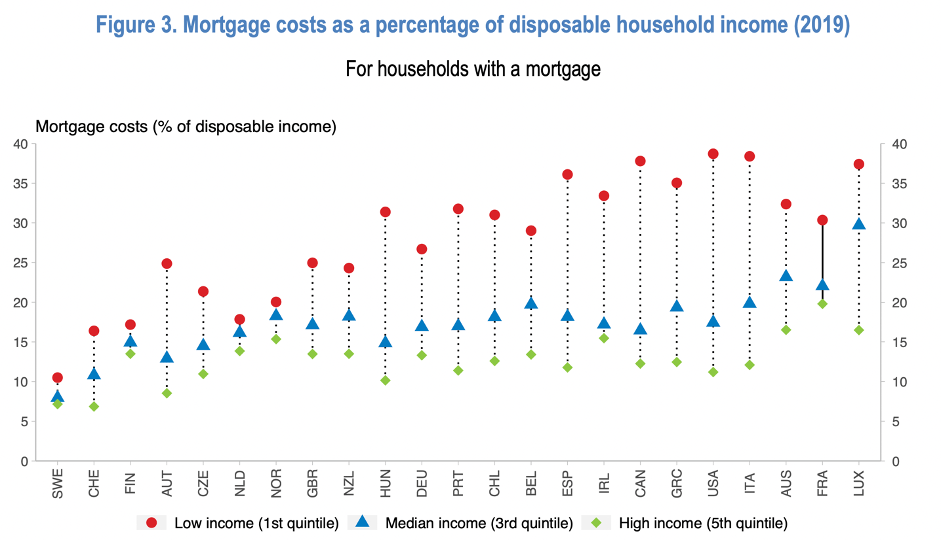

And we can also see that especially in Canada and the United States, mortgage costs make up a huge part of disposable household income – especially for low-income households. And that could be a recipe for disaster (and delinquencies).

{kind=link}

OECD Working Paper "Mortgage finance across OECD countries"

In case of the Toronto-Dominion bank we also must mention the U.S. exposure. The Toronto-Dominion bank was generating $18,442 million in revenue in the United States (38% of total revenue) and $760.7 billion of its assets are also “U.S. assets” (40 % of total assets). When looking at the allowance for credit losses above, we can also see that 59% are for the United States (however, only $0.3 billion are for residential mortgages). And the Toronto-Dominion bank will increase its presence in the United States with two acquisitions it made in 2022.

Increasing Its United States Presence

Similar to the Royal Bank of Canada, which acquired the Canadian banking operations of HSBC, the Toronto-Dominion Bank also made two major acquisitions in 2022. In February 2022 the acquisition of First Horizon Corporation ( FHN ) was announced and in August 2022, the acquisition of Cowen Inc. ( COWN ) was announced.

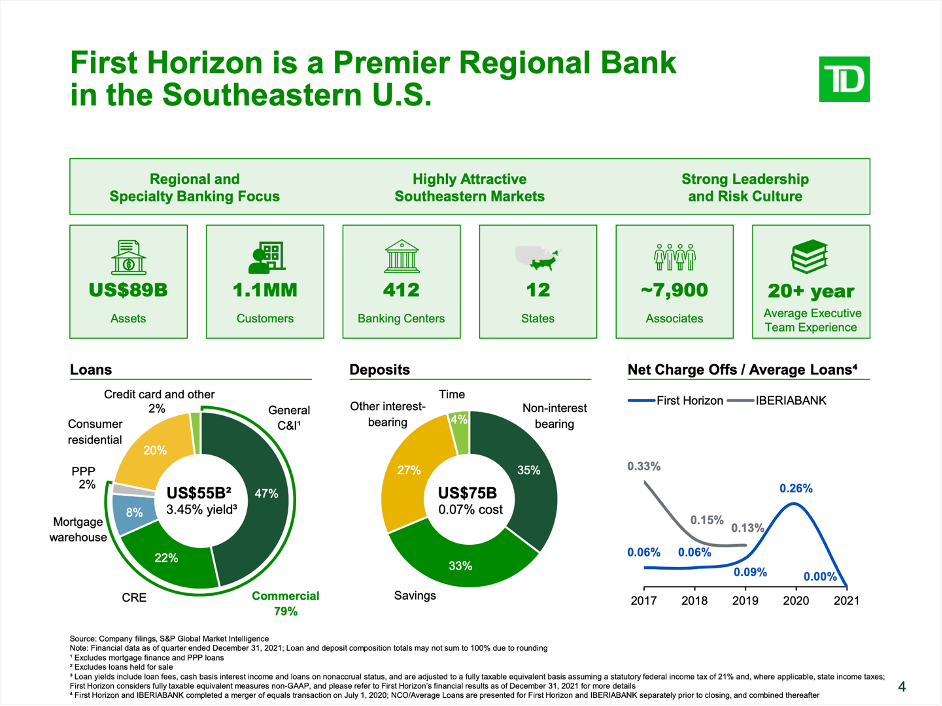

First Horizon Corporation was founded in 1864 and is now the fourth largest regional banking company in the Southeast. The acquisition is accelerating the long-term strategy of the Toronto-Dominion bank to grow in the United States. The bank is active in 12 states and has 412 banking centers as well as 1.1 million customers. Additionally, the bank has $55 billion in loans as well as $75 billion in deposits.

{kind=link}

TD First Horizon Acquisition Presentation

The deal, which is expected to close in early 2023 is valued at US$13.4 billion. This is valuing one share for US$25.00 in an all-cash transaction.

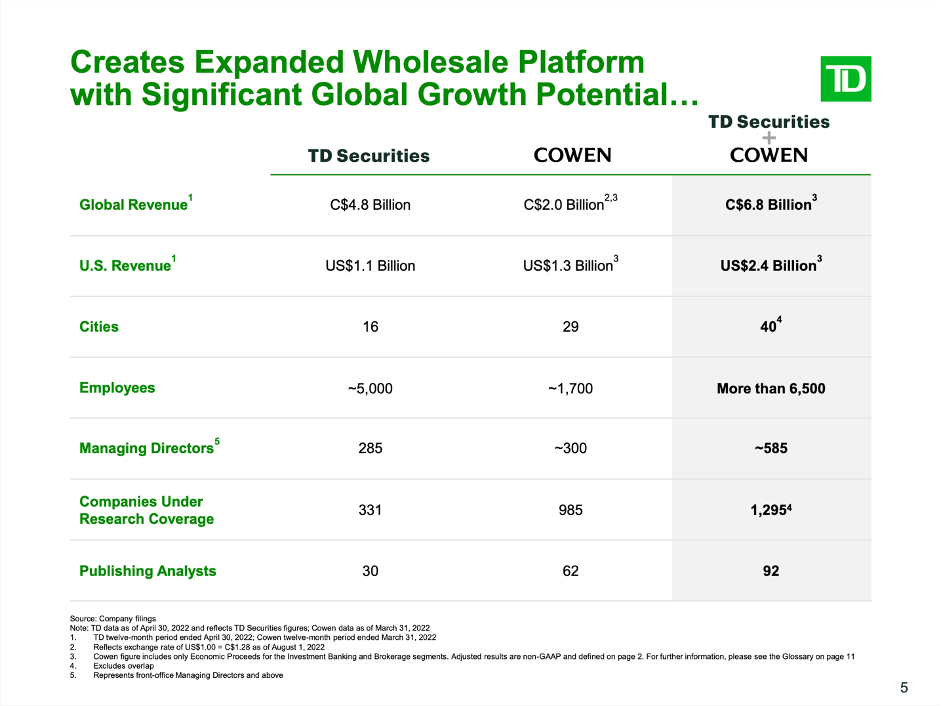

And in August 2022, the Toronto-Dominion Bank also announced it will acquire Cowen Inc. This deal is valued at US1.3 billion or US$39.00 per share and is also fitting the long-term strategy to grow the presence of the Toronto-Dominion bank in the United States. Cowen is an investment bank offering investment banking services, equity and credit research as well as prime brokerage and trading services.

{kind=link}

TD Cowen Acquisition Presentation

The Toronto-Dominion Bank also expected to achieve between US$300 million to million in revenue synergies in three years from now.

Intrinsic Value Calculation

At the time of writing, the Toronto-Dominion Bank is still trading for a single digit P/E ratio (9.66) which is extremely cheap for a high-quality business. And when looking at the last ten years we see that TD was never trading for a really high P/E (the highest valuation multiple was 15.36 in 2014) and is also trading below the average P/E ratio of the last ten years (which was 12.40).

And when trying to determine an intrinsic value by using a discount cash flow calculation, we can take the net income of fiscal 2022 as basis (which was $17,429 million). To be fairly valued (and assuming a 10% discount rate as well as 1,821 million outstanding shares), the Toronto-Dominion bank does not have to grow ever again. Generating the same net income as right now would be sufficient to be fairly valued (leads to an intrinsic value of $95.71).

On the one hand, we should not forget that the Toronto-Dominion bank could grow its bottom line with a high pace in the recent past and we must question if the bank can sustain the current net income level (especially in case of a global recession). On the other hand, the Toronto-Dominion bank could report high growth rates not just in the last few years but with high consistency. In the last ten years, EPS grow with a CAGR of 10.85% and since 2001 (I can’t take the last 20 years as TD reported a loss in 2002), earnings per share increased with a CAGR of 11.15%. And while the fiscal 2022 net income as basis might be a little high, zero percent growth for Toronto-Dominion bank seems very unrealistic for the years to come and hence we can rather see the stock as undervalued.

Recession Resilient

The biggest risk right now – and the reason why I don’t buy any banks at this moment – is the global recession as a scenario with a high probability of happening in 2023. Keeping that in mind, we should also look at the performance of the Toronto-Dominion bank during a recession. In my last article about the Royal Bank of Canada I called it pretty recession resilient (at least for a bank) as the steepest decline for earnings per share was 40% during the Great Financial Crisis and revenue declined only 4%.

When looking at the data for the Toronto-Dominion bank the performance during recessions is slightly worse, but still not problematic. First of all, the Toronto-Dominion bank was profitable in every year since the early 1980s aside from 2002 when the company had to report a loss. Second, the company had to report declining earnings per share on several occasions, but revenue did not decline steeper than 12.6% and earnings per share also declined “only” about 40% during the Great Financial Crisis. However, in the early 2000s, earnings per share declined steep. But all in all, the Toronto-Dominion bank can be seen as recession resilient (at least for a bank) and will probably perform much better than many other banks during a potential upcoming recession.

Comparing To Other Canadian Banks

In my opinion, the Toronto-Dominion bank is the most attractive pick among the major Canadian banks right now.

| Bank | Dividend Yield | P/E ratio | EPS CAGR 10-year | Return on Equity 5-year average |

|---|---|---|---|---|

| Toronto-Dominion Bank | ||||

| 4.23% | ||||

| 9.66 | ||||

| 10.85% | ||||

| 15.31% | ||||

| Royal Bank of Canada | ||||

| 3.89% | ||||

| 12.17 | ||||

| 8.42% | ||||

| 16.47% | ||||

| Bank of Nova Scotia | ||||

| 5.79% | ||||

| 8.85 | ||||

| 4.39% | ||||

| 13.50% | ||||

| Bank of Montreal ( BMO ) | ||||

| 4.27% | ||||

| 6.66 | ||||

| 12.51% | ||||

| 14.31% | ||||

| Canadian Imperial Bank of Commerce ( CM ) | ||||

| 5.78% | ||||

| 8.92 | ||||

| 5.46% | ||||

| 14.25% |

Although it does not have the highest dividend yield or the lowest P/E ratio, when looking at the overall picture the Toronto-Dominion Bank seems to be the best pick among the major Canadian banks right now. The combination of a double-digit EPS growth rate in the last ten years, a single digit P/E ratio and a 15.3% RoE in the last five years makes it a high-quality investment.

When Will I invest?

The tense relationship between deeply undervalued stocks on the one side and fear of a recession with negative consequences on the other side remains and therefore the question “When will I invest” is more than justified. In my last article about the Royal Bank of Canada I tried to provide an answer to the question:

“At this point, one might ask why I am so reluctant to invest in banks - despite the solid dividend yield, the low valuation, and the high quality of the business for some banks - including the Royal Bank of Canada. The answer is not so simple and not just based on fundamental aspects. My reservations are based on two different aspects.

First, fundamental problems which are not visible yet. We established above, that the Royal Bank of Canada has a solid balance sheet, great metrics and seems to be stable for several decades, which is certainly reassuring. However, I know what I don't know - and I simply don't know enough about banking to detect underlying issues a bank might have. And I know that not just the economy, but our society is an extremely complex system with feedback loops, unintended consequences, chain reactions and interdependences that could lead to outcomes nobody - and I mean nobody - could have foreseen. And banks are a prime candidate for such negative outcomes due to a high level of complexity.

Second, sentiment and typical bear market behavior. While the Royal Bank of Canada is already trading for a low valuation multiple, I have troubles to imagine that banks will withstand a global recession and bear market. It could happen - due to the rather low valuation multiples - but in my opinion we will see at least a 20% to 30% drawdown for most banking stocks (and this is including stable banks like the Royal Bank of Canada).

To answer the question when I will invest: When the crisis is already in an advanced stage - maybe with housing prices significantly down, maybe delinquencies increasing and unemployment already at a high level. When the Royal Bank of Canada is still performing solid at that stage (and revenue as well as earnings per share can decline), I will start investing.“

And the same is true for the Toronto-Dominion Bank.

Conclusion

In my opinion, the Toronto-Dominion Bank is one of the best banks in the world to own and among the five major Canadian Banks – which can all be seen as high-quality banks – it could be one of the best picks right now. But we seem to be at a “ make or break” moment for the S&P 500. It seems like people are getting greedy again (see CNN Fear & Greed for example) and after a 50% price increase for Bitcoin, my Twitter timeline is getting filled again with unrealistic price targets as well as unjustified bullishness. In my opinion, it is still the more likely scenario that we are in for a nasty surprise in the coming weeks and months (with the S&P 500 declining steeply) and in such a market environment I don’t want to buy banks.

For further details see:

Toronto-Dominion Bank: Best Pick Among Canada's Major Banks