TSEM - Tower Semiconductor: Great Company But If The Deal Doesn't Happen Slightly Expensive

2023-04-27 14:34:44 ET

Summary

- The talks of the acquisition have hit another hurdle, which is worrying slightly.

- The most recent block of another major deal in the UK sheds some light that the company could face a similar fate.

- I wanted to take a look at the company itself, to see what the company is worth in case the deal doesn’t go through.

- With conservative assumptions and the lack of love for the sector, the company is slightly overvalued, and I would expect volatility going forward to bring a better entry point.

Investment Thesis

With the slowdown in merger talks over the last couple of months, and decent FY22 results, I wanted to take a look at Tower Semiconductor Ltd. ( TSEM ) itself to see if the deal doesn't go through, what I would be comfortable paying to own this Israeli company as it continues operating independently. Given the tensions between China and the US and the lack of love for the semiconductor sector amid the slowdown in demand, I rate the company a hold and slightly overvalued. The company may experience a tumble in price if the deal does not go through, which would provide a good entry point in the long run.

Briefly on FY22 Results

A lot of semiconductor companies have reported quite strong end-of-the-year results, and TSEM was positive also. The full-year revenues are up around 11%, with 22% organic growth y-o-y, with quite a nice bump in margins and net income. The company will not be holding a conference call for the guidance of Q1 '23 because of the agreement to sell to INTC.

Bumps in the Road to Acquisition

In February of '22, Intel ( INTC ) announced its plans to acquire TSEM for around $53 a share that was meant to close within 12 months. It is now the end of April '23, and it still hasn't closed. Furthermore, the Chinese regulators have slowed down the review of the acquisition because the regulators want the products to be available in China.

The big problem is the tensions between the US and China. The new CHIPS Act basically incentivizes American companies like Intel to invest in American soil rather than investing in China, and I don't think China is liking that one bit. It seems to me that China wants Intel to keep investing in Chinese assets and selling the products to China. That is a big deal for China because the country depends deeply on imports of semiconductor products, as they are not self-reliant yet and may not be for quite a while. According to this article , China imported 83% of semiconductors in 2020.

I thought for sure this deal would close rather quickly, however, these tensions are bringing me some worry. It may still close, but, as of writing this article, the U.K.'s Competition and Markets Authority blocked the massive Microsoft ( MSFT ) acquisition of Activision Blizzard ( ATVI ) sending ATVI shares down over 10%. Of course, MSFT will appeal this decision, but I thought that this deal would go through also and here we are.

So, I would like to look at TSEM as a company that is going to keep operating independently, touch briefly on the semiconductor sector's outlook in the short run, and see what the company, with reasonable growth assumptions, might be worth in the long run.

Semiconductor Outlook

We can see a lot of softness going into the first half of '23. Many news articles point to a big slowdown in sales of semiconductors for the last 4 months now, with double-digit declines. Companies that I've covered recently in their earnings calls do not deny that they see a lot of inventory build-up and the demand is quite soft, however, these companies see some positivity going into the second half of the year.

TSEM is no different on this issue. I would expect declines in revenues in the first half of the year and if everything goes well in the second half, we could see revenue bounce back. It is hard to speculate on that because the further we go into the year, the more likely we are going to experience some economic headwinds, as many economists predict we are going to go into a recession, which means that the softness in demand may persist longer than anyone is predicting.

The sector is not getting much love these days, that's for sure. It won't last too long as the sector is too important in a lot of different technologies, from communications, automotive, IoT, AI, and many other electronics, and will be a necessary sector for a long while. This means that the sector will come back to life once all the worries and other economic headwinds like supply chain issues and geopolitical tensions subside. The sector is quite cyclical, which means the sector may stay at this bottom for a little longer.

Financials

I've been covering a few semiconductor companies recently, and all of them have been showing rather healthy balance sheets. It is no different in TSEM's case either.

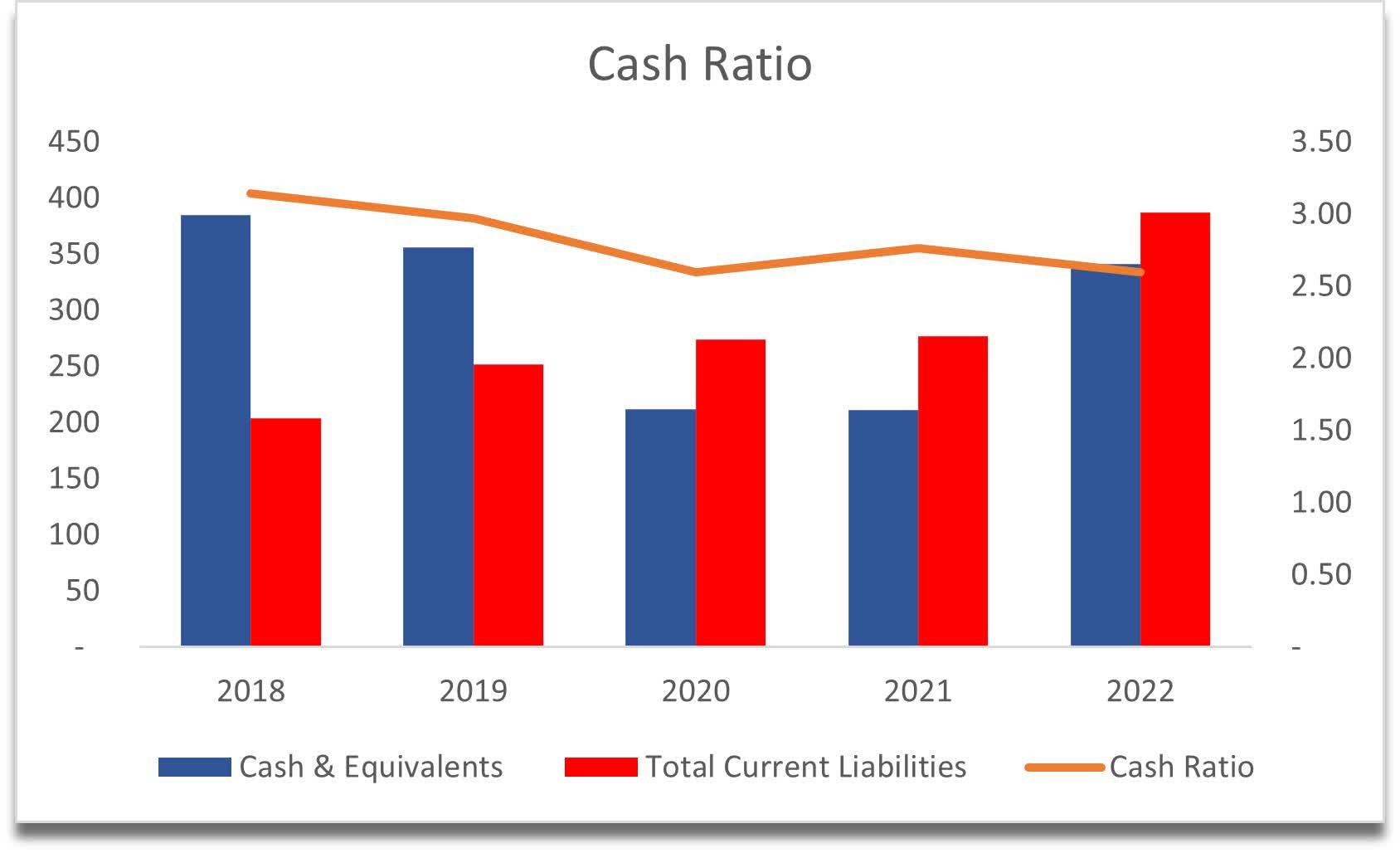

The company has around $1B in cash and short-term investments and $210m in long-term debt. Furthermore, if we take a more stringent look at the company's liquidity, TSEM has no problem paying off its short-term obligations with readily available cash and equivalents. The cash ratio, which is a more restricting look at the company's liquidity, is well above 2. This means that the company can cover its ST obligations solely with cash and short-term investment twice over.

The debt figure is also not an issue, as EBIT is much higher than the interest expenses on that debt.

{kind=link}

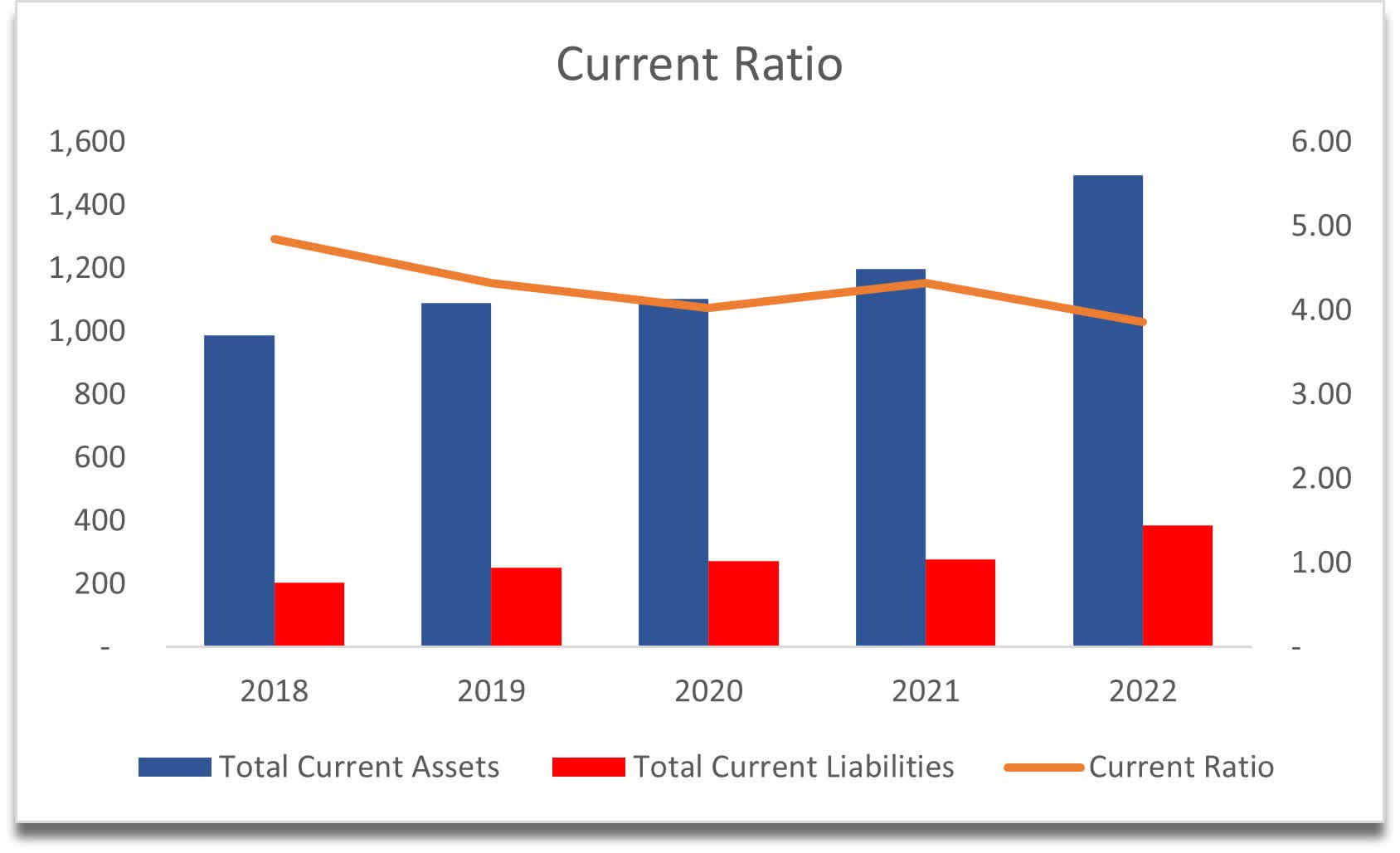

Naturally, this means that the company's current ratio is even better, which stands at around 4 at the end of FY22.

Current Ratio (Own Calculations)

{kind=link}

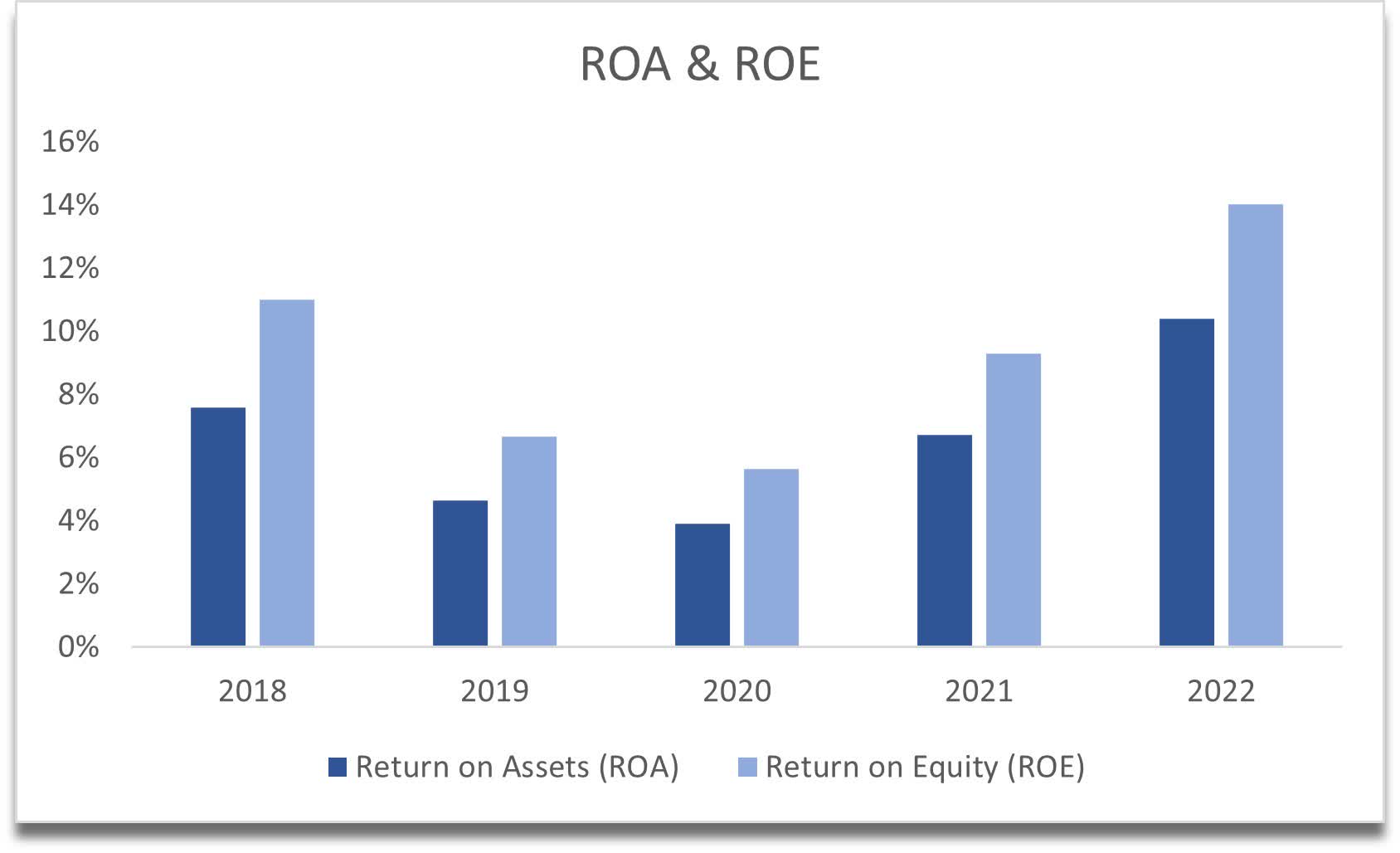

In terms of efficiency and profitability, ROA and ROE are quite good, sitting at around 10% and 14% respectively. The company is able to use assets and equity efficiently and bring in higher profitability.

ROA and ROE (Own Calculations)

{kind=link}

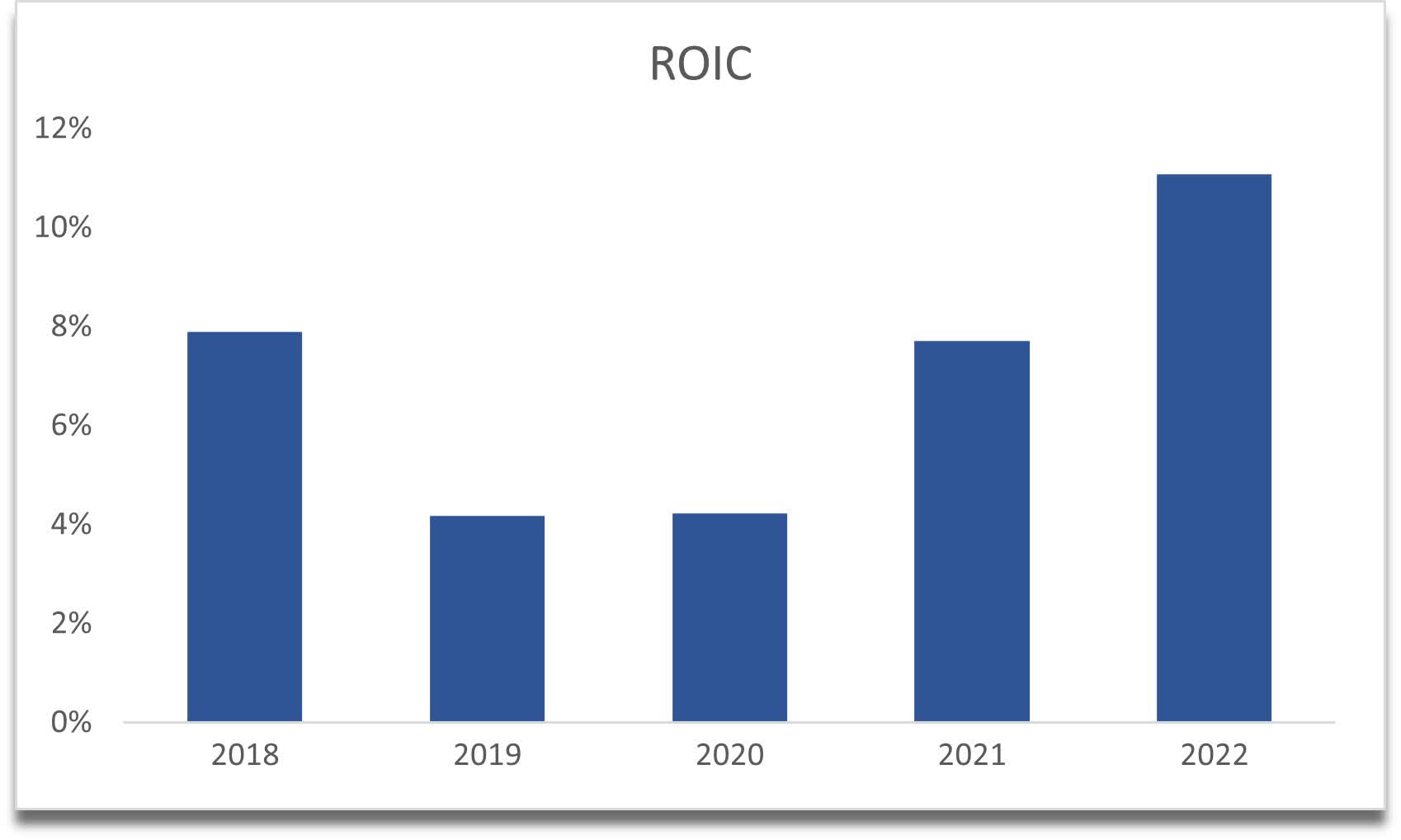

ROIC is also quite decent and has improved in the last couple of years. This means that the company is able to achieve some sort of competitive advantage and a decent moat in the sector, which is fantastic.

{kind=link}

Just like other semiconductor companies I've covered, TSEM has no glaring issues on the books, which is a great position to be in to withstand further economic headwinds that we will experience this and probably next year too.

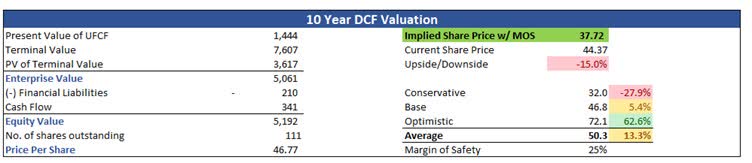

Valuation

I wanted to take a simple approach to valuing TSEM. For my DCF model in the base case, I assumed a -10% revenue decline in '23 with a 15% increase the next year and a linear decline in the growth to 5% growth by '32. This gives me around 8% average revenue growth for the next decade, which I think is quite conservative, given that the company is quite small still, and I expect it to grow at higher rates, however, I always like to be more conservative just to be on the safer side, and that way the returns are much better in the long run.

For the optimistic case, I went with a 10% average return, while on the conservative side, I went with a 6% average return.

The company has improved its margins quite a bit from '21, so to account for the softness in demand in 23, I will take away 100bps from margins and improve them back to FY22 margins by '32, which is also on the conservative side, seeing that in one year the company managed to improve net margins by 600bps.

On top of the conservative estimates, I would also like to put another 25% discount as a further margin of safety. 25% is the lowest MoS I go for and only increase it if I see some red flags on the company's balance sheet. TSEM has an outstanding balance sheet.

With that said, the company's intrinsic value with these conservative estimates is $37.72, which implies a 15% downside from current valuations.

DCF Valuation (Own Calculations)

{kind=link}

Closing Comments

This is the price I would be comfortable paying for a company that is very promising in the industry that is seeing very little love currently and if the company is not going to be acquired anytime soon.

Given the negative sentiment in the global economy, the lack of love for the sector, and uncertainty in the deal going through, I believe that the volatility will present a good entry point in the future if the company stays independent.

If it does go through and the Intel's CEO manages to sweet-talk the regulators in China, current investors have nothing to lose right now and got about a 20% upside. If the deal falls through, I wouldn't be surprised to see the company dropping 10%-15% on the news which can be a good entry point for long-term investors, as the company is quite healthy and has good prospects in the sector, that is still going to grow at a projected CAGR of 12.2% .

I'll keep an eye out on the development of the deal and I will be happy either way. Happy for current investors who will get a nice bump for their shares and for the new investors who can get in on a lower price in case the deal is dead.

For further details see:

Tower Semiconductor: Great Company, But If The Deal Doesn't Happen, Slightly Expensive