TSEM - Tower Semiconductor: Recent Years Of Incredible Growth Can Persist

2024-01-14 12:36:59 ET

Summary

- Tower Semiconductor presents a compelling investment opportunity with a low valuation and potential for growth.

- In recent news, TSEM has entered into a partnership with Intel which lends them to new market opportunities, to help drive more earnings growth.

- The valuation of the business remains appealing as it sits below historical levels, and leaving a very good upside as my price target lands at $38.

Investment Rundown

One of the hardest hit sectors when the interest rates began to increase last year was the tech sector. Looking at the stock chart for Tower Semiconductor Ltd (TSEM), I think we are looking at a very appealing opportunity right now for investing. The valuation has come down to what I think is a pretty low level, a FWD p/e of just 14. In the last 5 years, the company has averaged a far higher multiple, which might be because of the very rapid bottom line growth the company has managed to showcase going to around 2020, nearly doubling YoY. I don't think this type of momentum is sustainable over a very long period, but I do think a good chunk of it can be maintained.

With TSEM partnering up with Intel Corporation (INTC) I think they will be able to accelerate growth further and this environment of higher interest will be short-lived to suppress demand. Over the long-term the products and services that TSEM makes will be in high demand. The dental x-ray market for example which TSEM has exposure to is growing because of an increased demand for oral aesthetics leading to more x-rays needing to be done, beneficial for TSEM. As I am initiating my coverage of the company I will do so by rating it a buy.

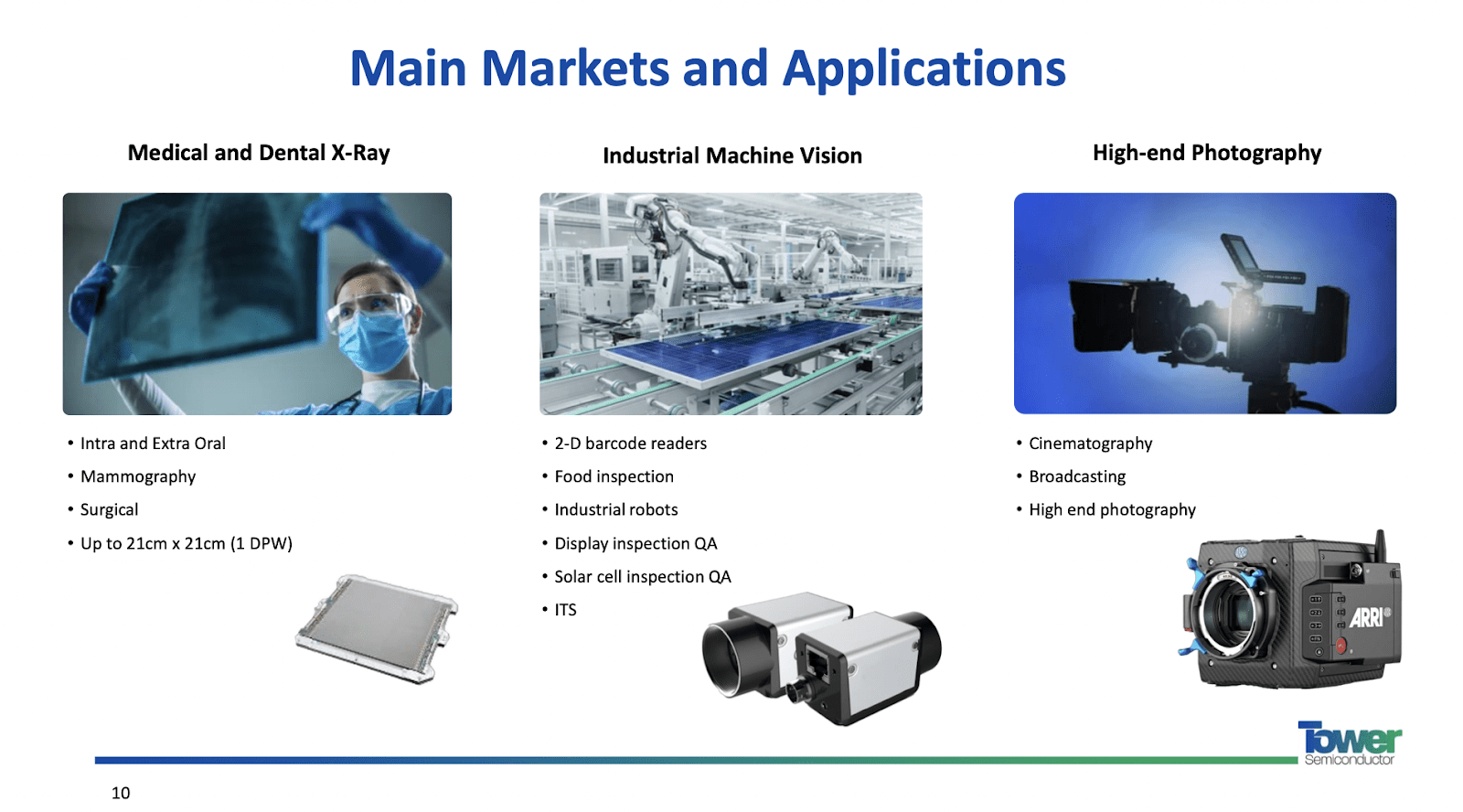

Company Segments

TSEM is a semiconductor foundry , that centers its operations on specialty process technologies for the production of analog-intensive mixed-signal semiconductor devices across global markets, including Israel, the United States, Japan, Europe, and beyond. Distinguished by its versatile offerings, the company provides customizable process technologies such as SiGe, BiCMOS, mixed-signal/CMOS, RF CMOS, CMOS image sensors, integrated power management, and MEMS. The semiconductor market is divided into many smaller markets and industries that all niche themselves towards one means. With TSEM you could divide it into medical and Dental x-rays, Industrial Machine Vision, and lastly High-end photography. The broader semiconductor market is expected to grow rapidly over the next several years, and I think the focus market that TSEM has will do the same as well.

Market Overview (Investor Presentation)

{kind=link}

Taking the industrial machine vision market, for example, it's expected to generate a CAGR of 11.3% in the US alone. With TSEM partnering with companies like INTC following the termination of their deal I think the business as a whole is still in a great position to benefit from increased demand. Even though they aren't fully based in the US, INTC lets them get a piece of the cake anyway.

The Intel Deal And What Next

Back in August, it was revealed the deal between INTC and TSEM was terminated. This decision appears to be a consequence of the ongoing geopolitical tensions between China and the US, ultimately leading to China blocking the deal entirely. This unexpected turn of events has had a significant impact on investor sentiment, with many initially anticipating substantial upside potential from the merger. The deal itself was quite significantly valued at $5.4 billion and in a way a route for an American company to gain semiconductor market share in Asia and more specifically in China. The rising tensions seem to have been a major reason behind the lack of support for the deal. Unfortunately, the opposite has occurred, with the stock price witnessing a substantial decline of over 30% from its 2023 peak. The termination of the deal triggers a contractual obligation, compelling Intel to pay Tower Semiconductor a termination fee of $353 million. This will add a nice bump to the yearly report by the company, but nothing that should result in a significantly higher earnings premium than its historical average I think.

{kind=link}

A trend that I have been covering a little bit before, mostly when writing about manufacturing in the US is deglobalization . It's not a trend that is solely applicable to the US, but rather to a lot of other countries around the globe too. I think deglobalization is affecting a deal between the likes of TSEM and INTC. Countries are aiming to secure domestic manufacturing, especially when it's in such a vital market like semiconductors

Earnings Highlights

Income Statement (Earnings Report (Nov 13))

{kind=link}

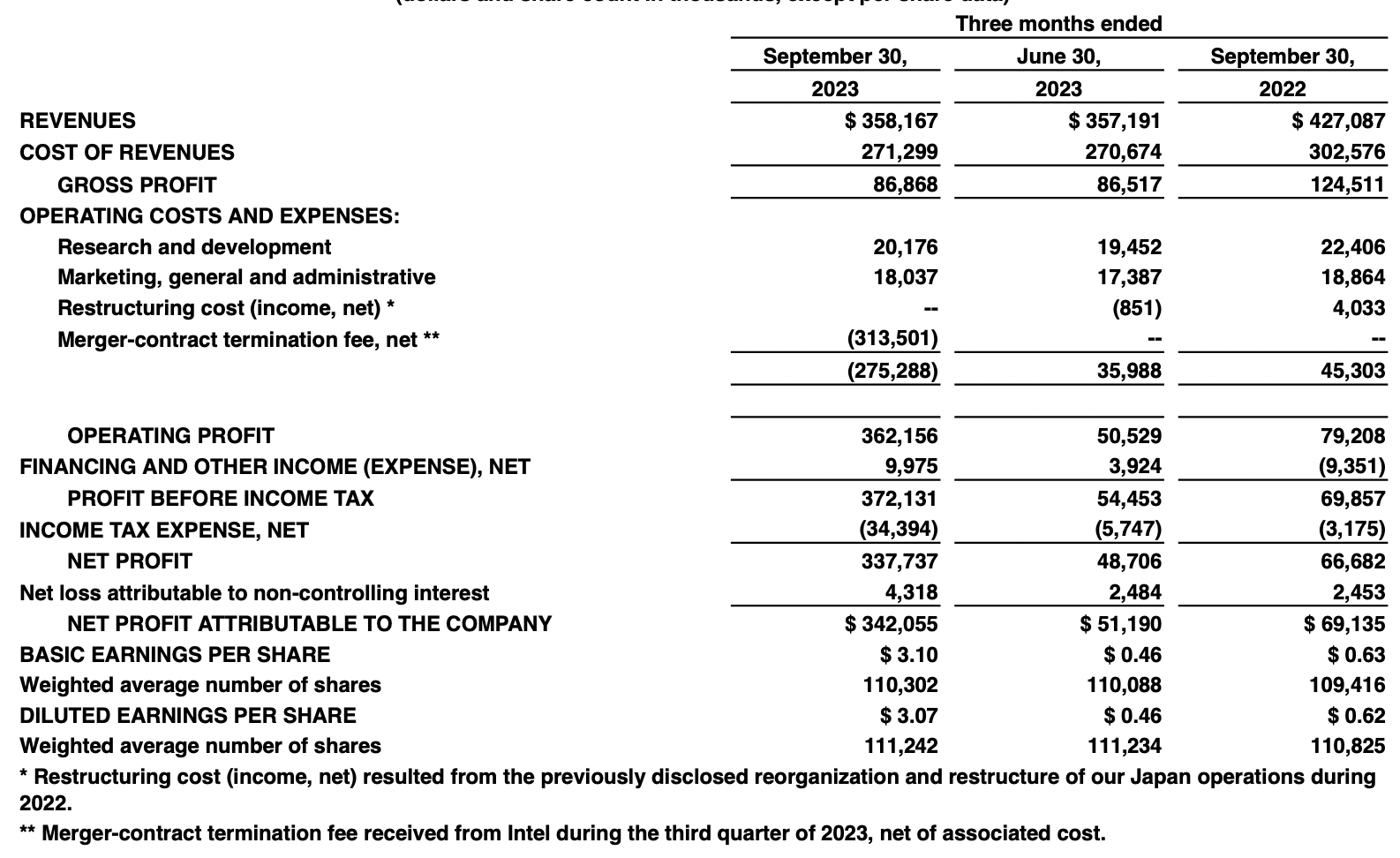

The last earnings report by TSEM was released on November 13 and I think the heightened interest rates have been noticeable in terms of revenues and earnings. YoY the top line fell by 19% which came as demand fell in a market coming off some very hot years with incredible demand. My focus for the quarter was far more on the bottom line and how it managed to maintain it. With the over $300 million termination fee that TSEM received they have managed to post a much higher EPS YoY landing at $3.1. Removing the termination fee we land at a net income of $29 million instead and with 111.2 million shares outstanding that is an EPS of roughly $0.26, a hard drop YoY. What dragged down the result was the higher income tax expenses which might not be a persistent issue, so the focus will be on how TSEM can raise the margins and EPS further in the Q4 FY2023 report. I think demand will pick up and we will see decent growth in 2024 for TSEM. The one-time cash infusion that TSEM received I don't think is enough to support a much higher valuation on its own, but it does mean the company has more M&A opportunities. My valuation for TSEM relies more on the continued demand in the markets it operates in and the growth of those. I think over the next decade a CAGR for the EPS of roughly 9 - 10% is likely. Since around 2020, the semiconductor industry has been on fire, and TSEM has done well to capture that demand, raising the net income by 96% annually since then. But as I also mentioned, the dental x-ray market will lead to more demand for TSEM as well, as oral aesthetics becomes more and more popular.

I want to quickly mention a little more about the deal that TSEM and INTC have. It was released in September last year the INTC will help provide 300 mm manufacturing capacity for TSEM and in return, TSEM will invest up to $300 million in assets like equipment in the New Mexico factory that INTC has. This partnership is beneficial to both businesses, but as far as TSEM goes I think this ramp-up in production capabilities will lead to strong top and bottom-line growth. As of the last quarterly ending, TSEM had a little over $300 million in cash and $1.7 billion in current assets leaving them in a strong position to make these investments rather quickly if so necessary in my opinion. The factory is set to manufacture the TSEM's 65-nanometer power management BCD flows and other flows in the product lineup of the company. These products are used in a lot of markets, but some of the more specific applications would be for LED drivers, or battery management but also analog and digital controllers.

{kind=link}

Looking at the valuation I think we derive the most value from this, rather than some shareholder-friendly action like a dividend or buybacks. The company is trading at its lowest multiple in recent years, just 14x FWD earnings. With a 5-year average of 19, I think we are left with a good amount of upside here in the medium term. The company has been impacted by higher interest rates, which has taken a toll on the demand in its target markets, but I think this year and in 2025 that will reverse. Given the positive performance so far by TSEM and how R&D expenses are flattening out whilst revenue grows, I think a p/e of 17 is fair to target here. With EPS estimates of $2.28 from my side in FY2024, I am left with a price target of $38 here. This leaves an upside of 34%, something I am very happy to buy into right now, resulting in a buy rating here. I arrive at the EPS estimate because I believe a recovery in demand will be visible this year, and for interest rates to decline, alleviating some pressure on the earnings for the business and ultimately leading to solid YoY EPS growth rate. In 2023 TSEM's EPS is expected to be $1.93. My FY2024 EPS estimate includes a recovery in the markets and for net margins to grow to 40%. I don't think the dilution of shares will accelerate and for FY2024 to see it around 111.8 million. This means I see NI at $254 million in 2024, or $2.28 EPS. YoY that would be an EPS percentage growth of 18%. The increased production capabilities in the US will aid with this EPS growth I think along with robust capital expenditures.

Risks

In the current landscape of deglobalization, there's a notable risk for a company like TSEM, which hasn't established a robust presence in the expansive US market-a significant arena for industry participation. However, the strategic partnership with INTC signals a proactive move to tap into this crucial market in my opinion. To maintain a competitive edge, TSEM must be judicious in its expenditures, especially in R&D . Although R&D has consistently accounted for a substantial portion of operating expenses, heightened competition could exert additional pressure on TSEM's earnings, potentially resulting in a dip in valuation.

{kind=link}

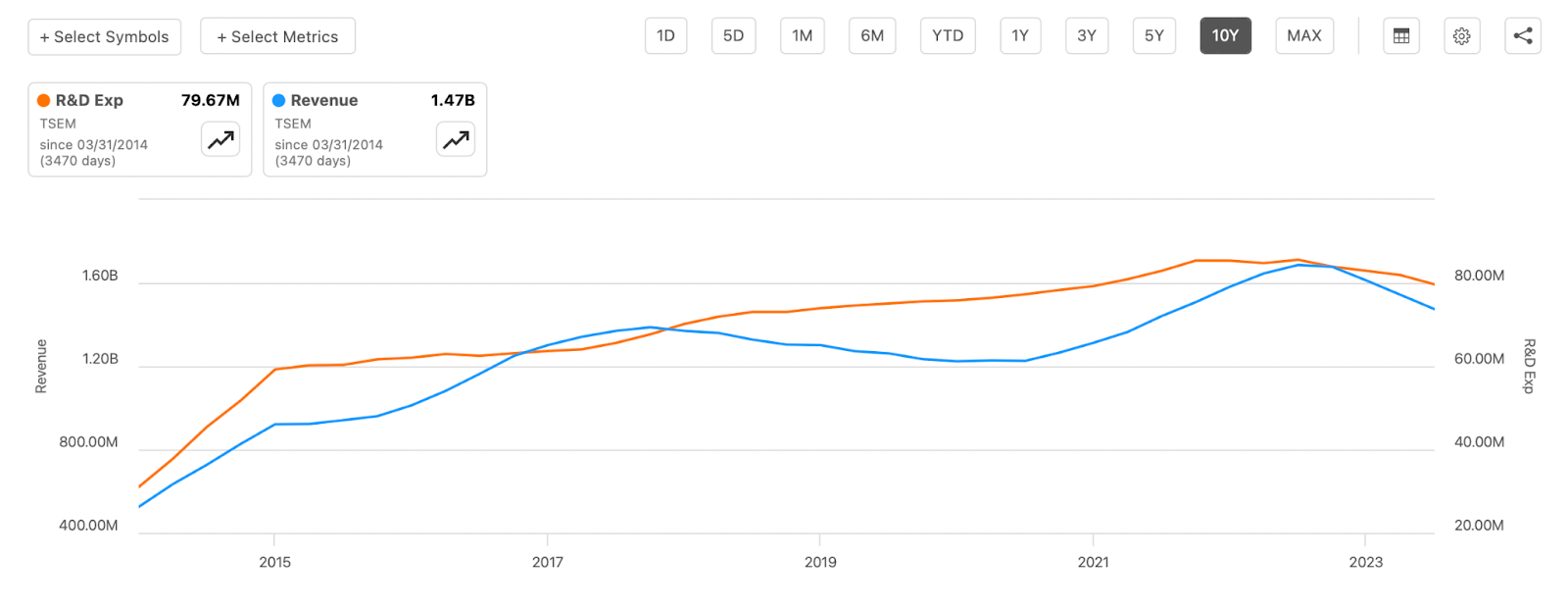

Looking at the chart above here we see the development of the R&D expenses and the relation to revenues. We can see that the revenues are finally starting to catch up and go in line with the expenses, I think this is a good sign and one that shows TSEM being in a market with higher demand and that they have achieved some sort of MOAT as they can raise costs without losing demand. Another final risk is the ongoing conflicts in the Red Sea. I think a lot of companies who deal on a global basis will be looking at the developments here for the next several quarters. Should there be increased threats it may drag the markets down, and the stock price of TSEM along with it.

Final Words

I haven't covered TSEM before but I am glad I did as I think the company holds a lot of potential right now in 2024. The company may have had its deal with INTC terminated as regulatory approval by China fell flat. The two companies are still partners and this opens up a big market opportunity for TSEM in the US, one that can deliver a lot of earnings potential. With the target price leaving an over 30% upside from today's prices I am initiating my coverage of the company by rating it a buy.

For further details see:

Tower Semiconductor: Recent Years Of Incredible Growth Can Persist