TSEM - Tower Semiconductor: The Deal Is Dead A Very Attractive Entry Point (Rating Upgrade)

2023-08-16 09:38:43 ET

Summary

- Tower Semiconductor will continue operations independently after China denied regulatory approval for its acquisition by Intel.

- Intel will pay Tower Semiconductor $353 million in termination fees, resulting in a one-time cash event.

- Tower Semiconductor's recent financial results were not the best, but the company's strong financial position and future growth potential make it a good investment opportunity.

Investment Thesis

Both companies agreed to part ways since China did not provide regulatory approval on the acquisition, which means that Tower Semiconductor ( TSEM ) will continue its operations independently. This temporary setback is providing what I believe is a really good opportunity to invest in a solid semiconductor company that already has good financials in place, therefore, I am updating my rating from “Hold” to “Buy” as I believe the company will be just fine in the long run on its own.

Approval Denied

So, I woke up to the news which wasn't too surprising to me but big news for TSEM, not much so for Intel ( INTC ) as INTC stock is not budging pre-market. The news that Intel and Tower agreed to terminate the previously announced merger due to what I think is the continuous geopolitical tensions between China and the US, which culminated in China blocking the deal altogether. That is not the outcome current shareholders of TSEM have hoped for that is for sure, however, it seemed that the writing was on the wall for a couple of months now and that was reflected in the company's share price dwindling YTD and is down around 33% if we include the pre-market numbers.

With the termination of the deal, as per the agreement, Intel will be paying TSEM $353m in termination fees. There is no date as to when this is going to be paid, however, this one-time cash event will result in around $3.2 in EPS. It is not better than a buyout at over $50 a share, however, it is still better than nothing. What this essentially means is the company will continue to operate as it has in the past but just got a little bump in earnings one year.

Outlook and Latest Quarter Results

The last time I covered the company was in April when I looked at the company's financials in detail, so feel free to have a read here . In the same article, I looked at the semiconductor sector in a little more detail than I will here. In that article, I also mentioned that the company is slightly too expensive if the deal falls through and expect a 10%-15% drop on the news that the deal is dead, fast forward to August 16 th , in the pre-market, the company is currently down around 12% and around 38% since the first time I covered the company. I think it is time to re-evaluate.

The company recently reported Q2 ’23 earnings , which beat consensus estimates but weren’t the best in my opinion, however, I wasn’t surprised about the results either because as I covered in April, I expected revenues to continue to fall a little while longer because of the softness in demand and overall negative sentiment in the semis sector. Revenues were down around 16% y-o-y, gross profit was down around 22% from the same quarter a year ago while operating profit was down around 28% compared to the same quarter a year ago. Net profit came in at $51m or $0.46 a share compared to $58m Q2 ’22 and $0.53 a share (a drop of 12% y-o-y).

So, not the greatest results, however, I was expecting this to happen, so I’m not surprised. Unfortunately, the company has not been providing any guidance for a while now because of the acquisition by Intel, however, now that the deal is dead, I will be listening intently to the company's guidance for next quarter's release, which is scheduled sometime in early November.

As for the broad semiconductor sector outlook, it seems that a lot of reports point to a trough in the first half of ’23 with some signs of growth in the second half of the year apparent. This report suggests the continuation of headwinds for the rest of the year; however, we will see robust growth in most if not all segments of the semiconductor sector in '24 and beyond, which bodes well for the future of TSEM.

Financials

I’ve covered the financials in the previous article in more depth by looking back at historic figures, so I won’t be repeating myself here, however, I will have a look at the company’s current state to see how well it is still doing.

As of Q2 ’23 , the company has around $912m in liquidity against $178m in long-term debt. Safe to say the company is still as strong as before and is at no risk of insolvency. The company’s current ratio is still very high, and while it is not a bad thing, it is above my acceptable effective ratio of around 1.5- 2.0 because this tells me that the company isn’t utilizing its cash pile very efficiently. It could be using that cash to start expanding its operations and be more aggressive in it or reward shareholders with some share repurchases or some other way. I believe now that the deal is off, the company will start to develop its operations further.

TSEM in my opinion is still a very strong company financially, with plenty of liquidity on hand and with very little long-term debt, which means the company will continue surviving the headwinds that we are yet to see in the next half of the year.

Valuation

I made some changes to my 10-year DCF analysis, and I will present two separate valuations here. One will be without the $353m one-time cash payment to TSEM and one with.

I also assumed a -18% growth in revenues for both valuations in ’23, then a subsequent 15% growth in ’24, which will linearly grow down to 5% by ’32, giving me around 7% CAGR for the next decade.

For the optimistic case, I went with 9% CAGR, while for the conservative case, I went with 5% CAGR for the next decade on both valuations.

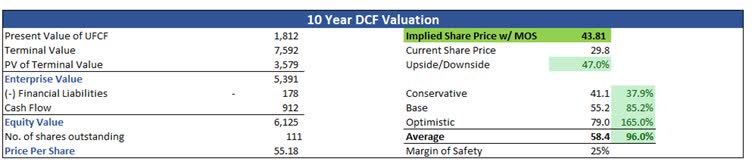

Also, for both valuations, I left margins as I had them in April. Same with the 25% margin of safety. With that said, if we include the $353m in extra income at the end of '23, the company would be trading for 6.7x earnings of FY23 and overall intrinsic value would be $43.81 a share, meaning there is around 47% upside from the current (pre-market) valuation.

{kind=link}

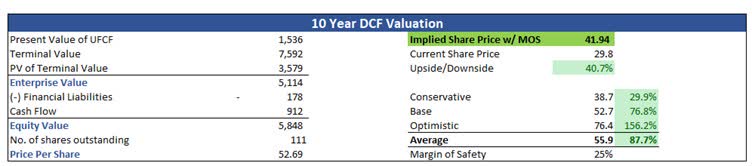

Now, if we don't include the $353m, the intrinsic value would still be $41.94 a share, implying a 40% discount to fair value according to my calculations.

{kind=link}

Closing Comments

I don’t think this is the end of the road for TSEM now that the deal is dead. The company will continue to operate as normal going forward as an independent company. I would rate the company a strong buy right now, however, I feel like because of this short-term noise, the stock price may continue its further decline because of the news. I am going to upgrade it from Hold to Buy as I believe the risk/reward here is very enticing and further declines in share price only help the long-term investor to accumulate shares in a fantastic company like TSEM.

I will be looking at opening a small position, to begin with very shortly, and will welcome further price depreciation in the aftermath of the dead deal.

For further details see:

Tower Semiconductor: The Deal Is Dead, A Very Attractive Entry Point (Rating Upgrade)