TSEM - Tower Semiconductor: Tough Current Market Climate But Long Term Remains Appealing

2023-07-13 03:08:58 ET

Summary

- The share price of Tower Semiconductor Ltd has been trending downward for the last 12 months, making it an appealing investment opportunity despite the downturn in revenues.

- The company's balance sheet is solid with a negative net debt of $702 million, and it offers a 12% upside if the acquisition with Intel goes through.

- Risks include a lack of operation in the North American market and a history of diluting shares, which could suppress the company's value in comparison to the rest of the sector.

Investment Summary

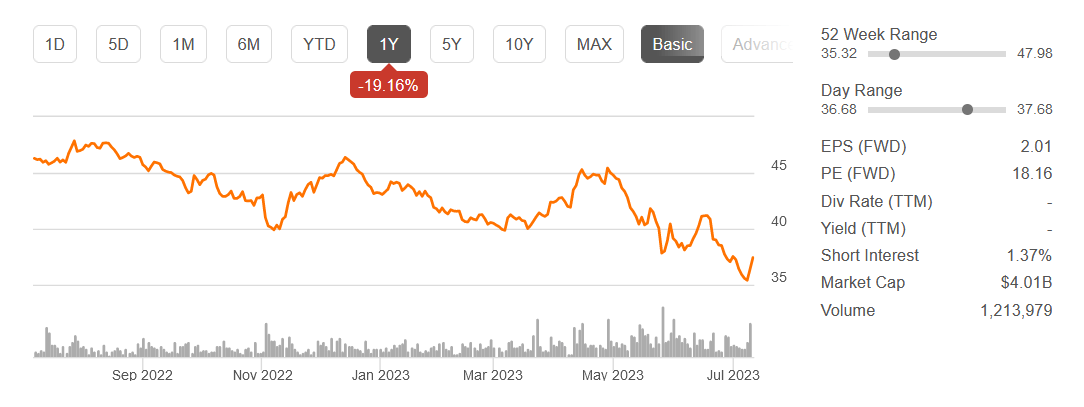

The semiconductor industry and any company related to it has seen a surge in coverage and many companies saw their share prices skyrocket. The AI hype was another catalyst for the industry, but for Tower Semiconductor Ltd. ( TSEM ) the share price has been trending downward for the last 12 months. Down around 25% from its highs of $47 per share it is starting to look very appealing to start a position in TSEM.

The semiconductor industry does seem to go in cycles as companies are building up inventory levels and then depleting them. In 2021 and 2022 we had supply chain issues which caused strong price hikes for many products in the industry. But as supply chains are seemingly easing it's becoming easier for companies to maintain more efficient inventory levels, which should bring a more steady growth path for TSEM and other companies in the sector. As I view the outlook as very positive I am rating TSEM a buy now.

Semiconductor Industry Remains Robust

The outlook for semiconductors still looks very solid in my opinion as demand remains even though inventory levels of many customers have been built up over the last 12 months. The estimates suggest a CAGR of 8.19% over the coming 5 years.

Market Outlook ( Mordor Intelligence )

I find it likely that TSEM will outgrow this in terms of revenue growth and perhaps the same will be true for the bottom line as well if they are more conservative with their share dilution from now on.

What has been discussed quite a lot concerning the semiconductor industry is the cyclical nature of it. It seems that it has times of extremely high growth and then times of consolidation. Right now I think we aren't in the high growth phase, as visible in the last report from TSEM where revenues dropped every year. But as inventory levels deplete, I think we will see another strong surge in revenues for TSEM. The rise of AI which caused companies like NVIDIA Corporation ( NVDA ) to surge is a statement about the cyclical nature of semiconductors and something that need to watch out for when investing in the industry. It can skew valuations but I think the last 12 months downturn for TSEM’s share price has put us at a favorable risk/reward ratio right now to begin an investment.

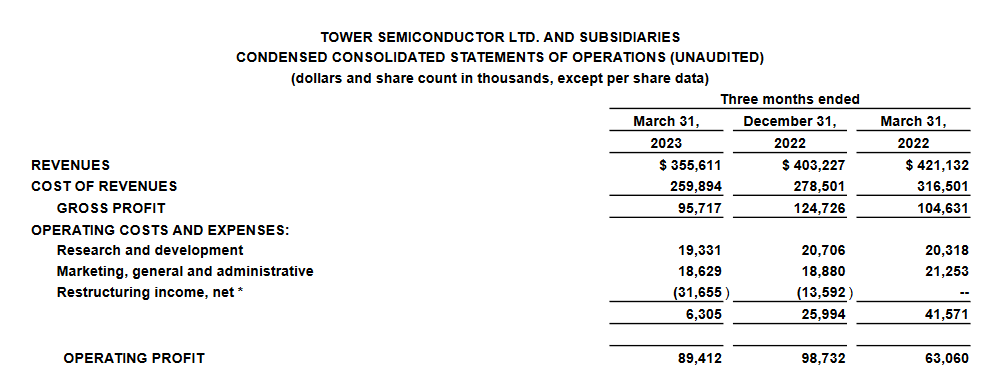

Quarterly Result

For Q1 2023 TSEM experienced both a YoY and a QoQ decline in revenues. The quarter ended with them generating $356 million, down from $421 million 12 months ago. Moving over to the bottom line for TSEM the EPS landed at $0.65, down QoQ but up significantly from Q1 2022 when EPS was $0.5. The increase seems to have been due to restructuring income and the improvement and restructuring of their Japan operations.

{kind=link}

Looking ahead to Q2 the company is not providing any guidance as they have signed an agreement with Intel (INTC) regarding this. I think we aren't likely to see even lower revenues. Demand seems persistent and I expect to see a QoQ growth and revenues landing above $380 million for the quarter.

Much of the appeal with TSEM a year ago was that Intel was aiming to acquire them in a $4.5 billion deal, but there seem to have been struggles in this matter. But Intel is facing challenges as they communicate with Chinese regulators to make the acquisition come true. Right now TSEM is just over $4 billion in valuation and trading at a 12% discount to what the deal was planned at. This is baking in that there is a decent risk of the Chinese regulators saying no to the deal. But as far as Intel is concerned, they are remaining on track to acquire this and say they are making progress .

Risks

One of the risks that we see facing TSEM is a lack of being able to operate in the North American market. The Chips Act that was passed in the US was meant to further the growth of American manufacturers and with that including semiconductor companies, and companies like Intel. I fear that perhaps TSEM will have to take a backseat in terms of priority here as more investments will go to funding American companies and establishing them in the semiconductor industry.

Besides this the company has also a disappointing history of diluting shares, increasing around 10% over the last 5 years. In my view, I think this is very unnecessary as the levered FCF is quite strong at TTM $238 million. That's enough cash flows to cover all the long-term debts, which put TSEM in a fantastic financial spot, but they still view dilution as necessary it seems. I think if this is a habit that continues over the long term then TSEM will be valued at a suppressed multiple in comparison to the rest of the sector, somewhere around 16 - 17 I think.

Valuation & Wrap Up

The share price for TSEM has been hammered over the last 12 months, down around 25% from their 52-week highs of $47 per share. The lacking progress in the Intel deal seems to have been the cause for this. But In my opinion, even without the deal, TSEM looks like a very good investment opportunity right now despite the downturn in revenues. I think the cyclical nature of semiconductors is on full display here and investors should be aware that earnings results like TSEM’s are going to be commonplace.

{kind=link}

The balance sheet of TSEM is solid and they even have a negative net debt of $702 million. This highlights the low likelihood of debt becoming an issue for the company in the near term. But a lower multiple seems to apply to the company as they have explored Chinese manufacturing and operations there, but also that shares have been continuously diluted the last 5 years. Despite all that, I think investing right now offers the opportunity to get into a solid semiconductor company, which also offers a 12% upside if the acquisition with Intel goes through. A win-win in my opinion and a good enough reason to invest.

For further details see:

Tower Semiconductor: Tough Current Market Climate, But Long Term Remains Appealing