TRIN - Trinity Capital: When Taking Additional 2-3% Yield Compared To Peers Is Not Justified

2023-12-21 11:21:56 ET

Summary

- Trinity Capital Inc. is a BDC focused on providing debt and equipment financing to growth stage companies.

- The portfolio consists mainly of term loans and equipment financings, with a very minimal skew towards the equity component. Plus, most of investments are based on floating rates.

- While Trinity Capital offers a high yield of 13% and it has a great portfolio structure, it carries significant risk due to its heavy exposure to small companies in a cash burn cycle.

Trinity Capital Inc. ( TRIN ) is an internally managed BDC, which is more focused towards providing debt and equipment financing to growth stage, typically SMEs, companies.

The overarching investment objective of TRIN is to deliver attractive current income and, to a lesser extent, some capital appreciation through investments consisting primarily of term debt and equipment financings and, to a lesser extent, working capital loans, equity and equity-related investments.

As many of my readers have most probably noticed, I have been actively covering BDC names mostly due to structural tailwinds that make the entire segment interesting for long-term investors, who also tend to prefer a high yield component.

TRIN is not an outlier here. The question is whether TRIN is an optimal choice relative to its peers.

Portfolio overview

At a portfolio level, TRIN carries rather conventional positions across the key investment avenues.

{kind=link}

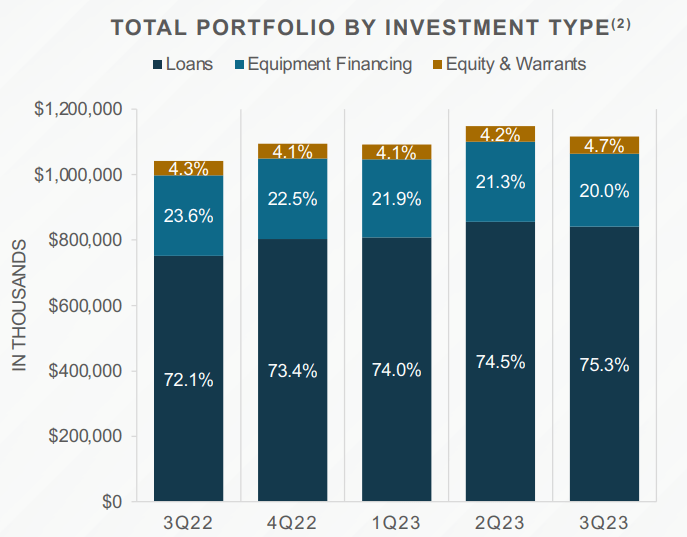

We can see how loans, which are mostly first lien, dominate the total AuM figure. What is a bit different compared to most of the BDC players is that we can see a notable exposure towards equipment finance, which could be deemed as a slightly de-risked position, especially in relation to first lien.

Moreover, the fact that TRIN has allocated only ~5% in equity type instruments could also be viewed positively, as this is clearly not material. Typically, one of the key areas of concern in the context of BDC profiles is the mismatch between assets and liabilities (plus, the expected dividend distributions to BDC shareholders). Since most BDCs apply additional leverage to magnify the return potential and tend to pay dividends frequently, having predictable incoming cash flow is critical. In case of a too heavy overweight allocation to equities, it is very clear that the overall risk profile increases (e.g., dividends are significantly less predictable than fixed income investments).

{kind=link}

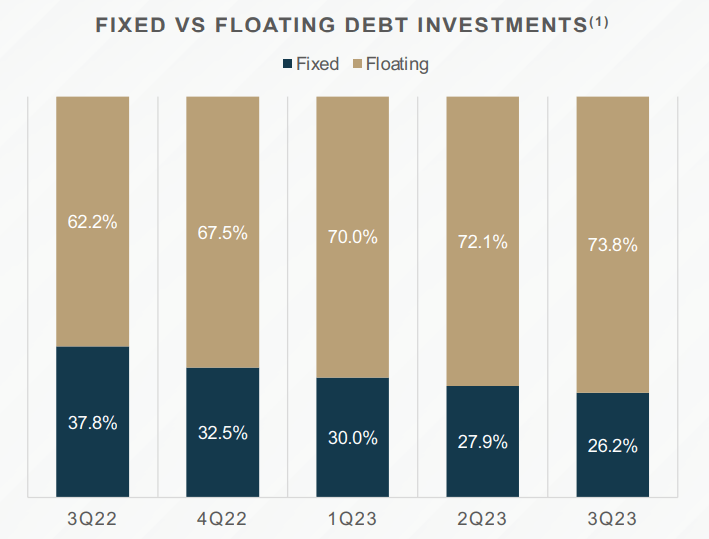

An additional positive factor is TRIN's floating vs fixed rate investment (or provided financing) structure, which has starting from mid-2022 become more attractive in the current interest rate environment.

Most of the incremental investments are made on floating rate basis, which should gradually render the portfolio more sensitive to the interest rate dynamics. This should also help easier align the external leverage component with the captured yield levels.

Trinity Capital

Yet, the most important issue for TRIN, in my view, is the underlying businesses to which the financing has been channeled. And there are two unfavorable aspects here:

- Most of the provided financing has been made to early stage, small growth companies, which per definition embody much greater risk characteristics than the average business for which most BDCs lend.

- To make the matters worse, TRIN has also stated under its loan policy that in many of business where TRIN acts as a lender, there is still a cash burn problem.

Thesis

So, from the above we can conclude that while TRIN has indeed structured its portfolio and allocations in a rather attractive and optimal manner, looking at this more deeply, it is evident that there is a huge risk factor embedded in the Fund.

Consequently, the portfolio yield, as of Q3, 2023, stood at 16.7%, which is very attractive to say the least. Obviously, the key driver of this is not the equity or bias towards mezzanine or other inherently risky positions, but the unpredictable and risky early stage growth companies, which are still burning cash.

A significant portion of the portfolio yield is passed through to the investors, which leads to a lucrative yield of ~13%. This is indeed high as on average BDCs offer yields that are closer to 10% (i.e., between 10-11.5%).

{kind=link}

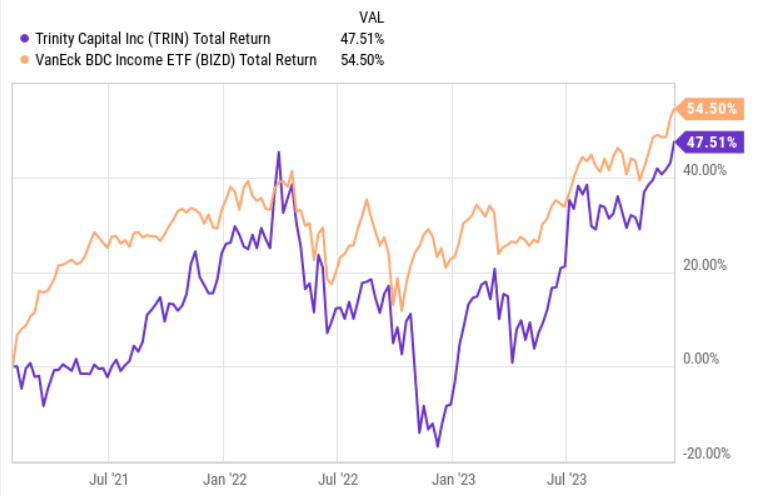

If we look at the historical 3-year total return chart, we can see how it indicates that TRIN has quite consistently underperformed the broader BDC segment.

Plus, it has been very volatile and at the beginning of interest rate increases, the Fund experienced a major shock due to concerns around companies' ability to service more expensive TRIN loans.

Considering all of this, I see no notable reason to go long TRIN, when other peers - which carry rather similar portfolio structures yet with an investment skew towards more sound enterprises with stronger cash generation - provide yields at only 200-300 basis points below TRIN.

To give you a couple of examples:

- Oaktree Specialty Lending Corporation ( OCSL ) - 10.8% yield

- Blackstone Secured Lending Fund ( BXSL ) - 10.9%

- BlackRock TCP Capital ( TCPC ) - 11.6%

The bottom line

The BDC space is well-positioned to benefit from secular tailwinds in the overall lending markets, which are increasingly turning to private credit solutions, where companies such as TRIN can step in and provide attractive financing.

TRIN's portfolio structure is optimal, allowing it to capitalize on the high interest rate environment, and is also nicely distributed across the key investment categories with very limited exposure towards equities.

The currently offered yield of 13% is not only attractive, but is one of the highest in the sector.

Having said that, TRIN is heavily exposed to small companies, which are still in a cash burn cycle. In fact, this has, to a large extent, been also the key reasons behind TRIN's volatile performance and negative alpha compared to the BDC index.

In my humble opinion, it is not worth chasing for additional 200-300 basis points in yield by simultaneously assuming much greater risk than what is embedded in other BDC peers.

For further details see:

Trinity Capital: When Taking Additional 2-3% Yield Compared To Peers Is Not Justified