TGI - Triumph Group: 13% Yielding Notes Too Risky After Refinancing

2023-03-21 08:43:47 ET

Summary

- Triumph Group recently refinanced its debt due in 2024.

- After refinancing, the next maturity, due in 2025, is yielding 13%.

- An analysis of the operations and refinancing leaves too much risk on the table.

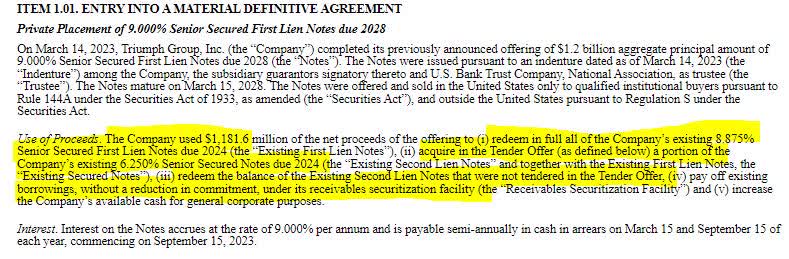

Triumph Group ( TGI ) a component supplier of the defense and aerospace industry, recently completed a tender offer of its 6.25% senior secured notes maturing in 2024. The company also paid off a second series of 8.875% notes maturing in 2024. Both payouts were funded by the issuance of 9% Senior Secured First Lien notes due in 2028.

{kind=link}

{kind=link}

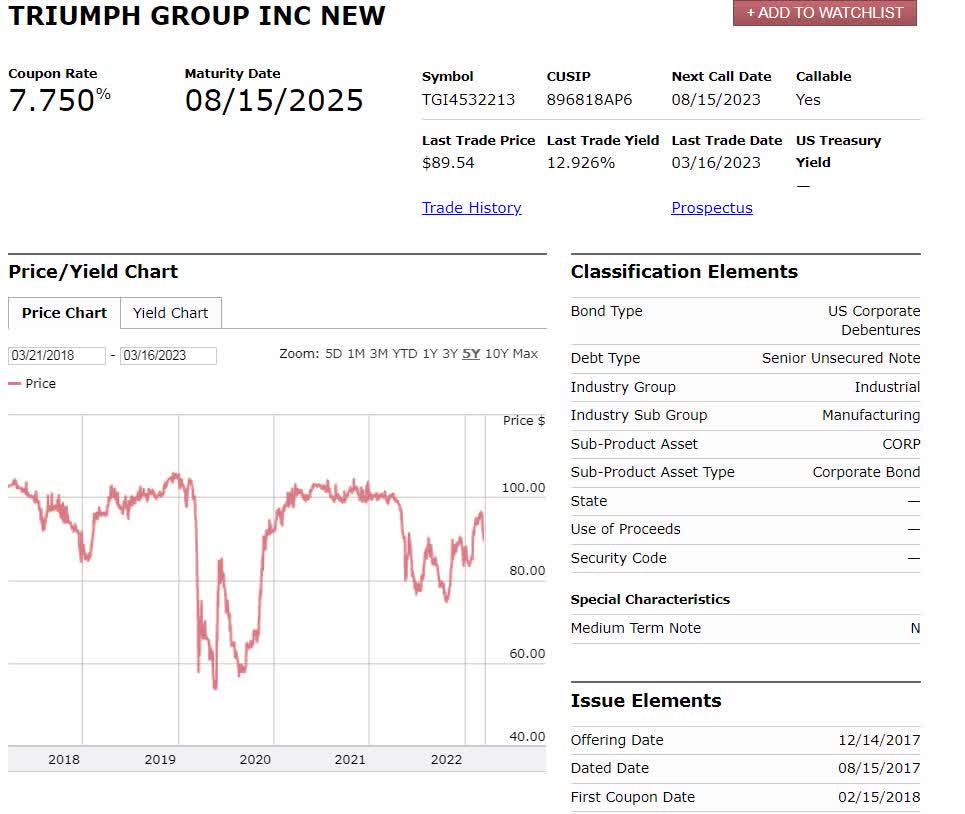

After the dust settled, the company’s 2025 maturing bonds were left as the next maturity and are yielding nearly 13%. While the success of the tender offer may make the nearer term bonds more attractive, I believe the underlying fundamentals of the business, combined with the new debt structure, make investing in Triumph’s bonds too risky.

{kind=link}

{kind=link}

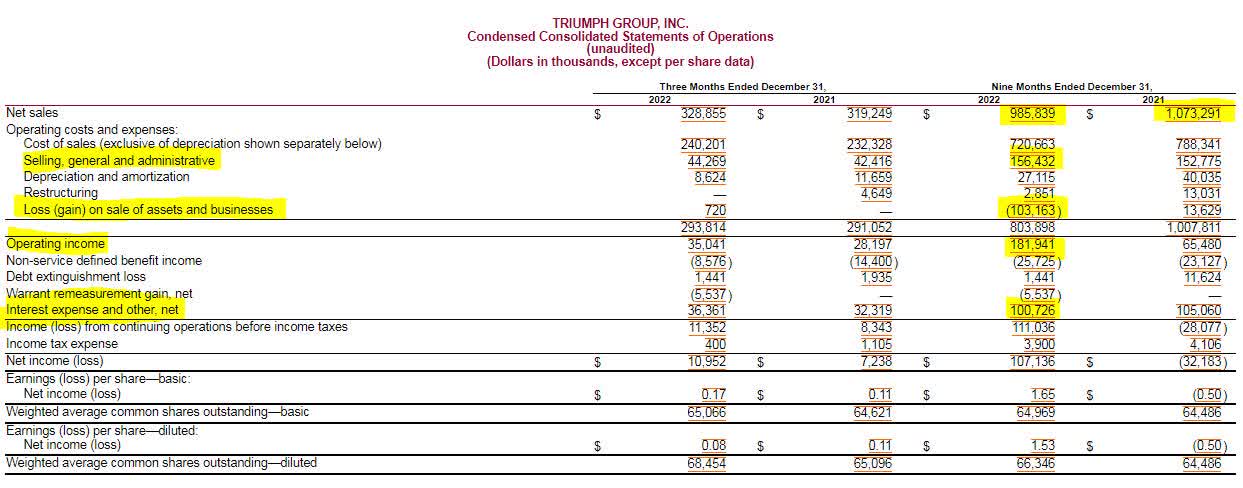

Triumph’s operating results showed headwinds hitting the company. Revenue declined by $87 million or approximately 8% in the nine months ending December 31, 2022 versus the same period a year ago. On the expense side, cost of sales declined by $68 million (not commensurate with sales), and SG&A costs rose. Ultimately, operating income was much higher than 2021 due to gains related to the sale of assets. Without the asset sale, the company would not have had the operating income to cover interest expenses.

{kind=link}

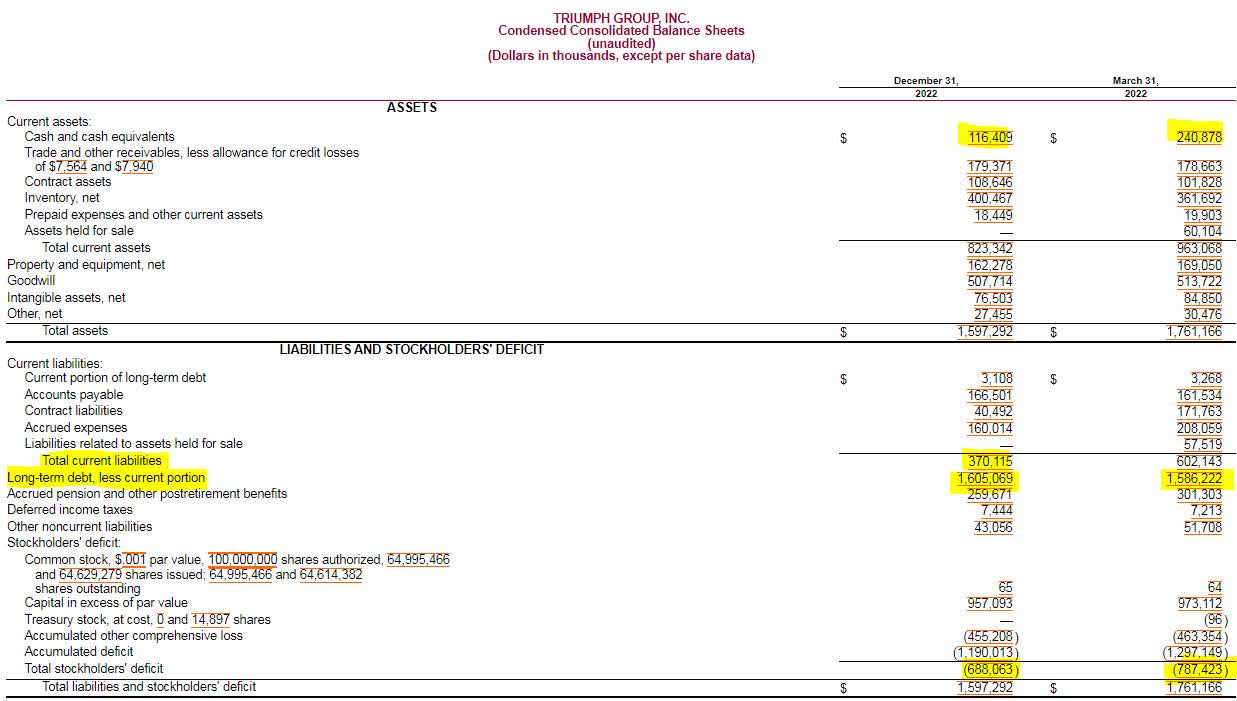

In the nine months since the fiscal year end, Triumph’s balance sheet showed improvements to its current ratio. The company saw its current liabilities decline markedly due to the drop in contract liabilities. The company’s cash balance was cut in half and long-term debt ticked up by $20 million. Interestingly, the company held $60 million in assets and $57 million in liabilities for sale that it appears to have sold for $163 million (due to gain of $103 million). This sale leads me to be optimistic that Triumph could get additional premiums for asset sales.

{kind=link}

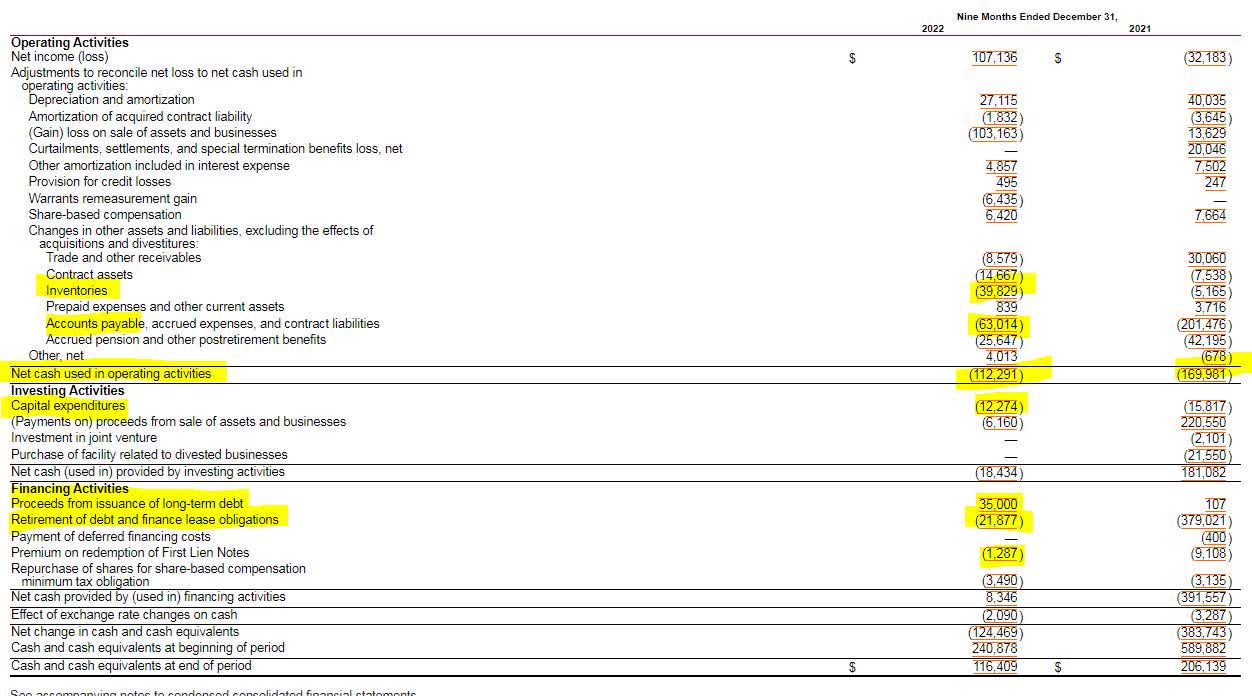

Triumph’s cash flow statement demonstrates how the organization used the cash it generated in the first nine months of the fiscal year. The company burned $112 million in operating cash for the first nine months of this fiscal year, mainly due to a $40 million build in inventories and $63 million in paydown of accounts payable. With capital expenditures, the company’s free cash flow deficit is nearly $125 million. For the most part, the company used cash on hand to fund its cash flow deficit, but did borrow a net of $12 million during the year.

{kind=link}

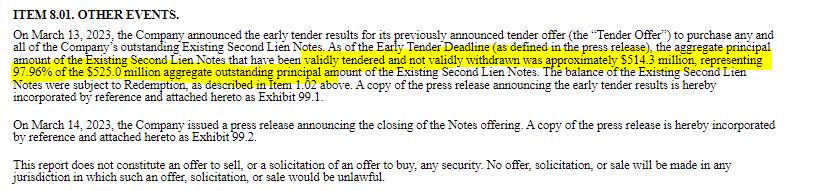

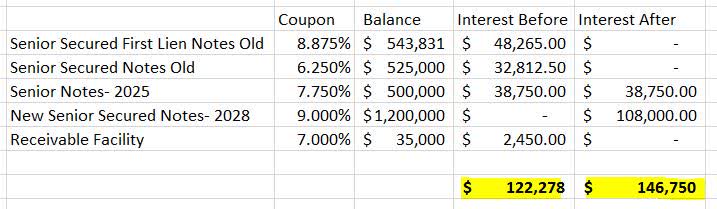

Triumph’s cash burn is concerning considering it had over $1 billion of debt coming due in 2024. The company also has $500 million coming due in 2025. After the most recent earnings report, Triumph successfully tendered 98% of its second lien notes due in 2024, redeemed first lien notes due in 2024, and then redeemed the remaining second lien notes. Triumph accomplished this by issuing new 9% senior secured first lien notes due in 2028. The notes were offered and sold to institutional investors only.

{kind=link}

By comparing the debt structure at the end of December with the new debt structure following the issuance of the new notes, investors can see that Triumph is facing higher interest expenses to the tune of $25 million per year, further straining cash flow. The paydown of the securitization facility does increase liquidity by $35 million, bringing it to around $150 million, but nowhere near the level of debt maturing in 2025.

Debt issuance and tender offer data uploaded into spreadsheet

{kind=link}

{kind=link}

Triumph Group will need new financing to pay off its 2025 bonds, and the company may need additional financing to boost liquidity between now and then. The presence of $1.2 billion in institutional investor debt senior to these bonds is concerning as well. These investors could pressure Triumph into a distressed exchange or prepackaged restructuring should refinancing efforts fail to materialize. These factors make the 2025 notes too risky for the time being.

For further details see:

Triumph Group: 13% Yielding Notes Too Risky After Refinancing