TGI - Triumph Group: An Uphill Battle Against A Pile Of Debt

2023-10-24 14:35:46 ET

Summary

- Triumph Group stock has lost over 40% of its value.

- The stock price decline is driven by the exercise of warrants, diluting shareholders by 17.2%.

- Triumph Group's free cash flow is inadequate to pay off its $500 million debt due in 2025 and $1.2 billion due in 2028, requiring costly refinancing or further shareholder dilution.

In June, I analyzed Triumph Group (TGI) stock and at the time I concluded there was no strong buy case for the simple reason that while the industry is facing a positive backdrop of higher production rates on commercial airplane programs, the cash position was unlikely to be adequate for Triumph Group to pay off its $500 million Notes due in 2025 pointing at the need for costly refinancing of debt. Since then, the stock has lost more than 40% of its value which could potentially offer a compelling entry point. In this report, I will be discussing whether that is the case.

Why Did Triumph Group Stock Tumble?

The stock price decline is not so much driven by the results, in my view, but rather by the exercise of warrants. In June 2023, the company issued a notice of redemption for its remaining outstanding warrants. Warrant holders could exercise their warrants with cash to receive one share per warrant. If all warrants would be exercised, it would mean that around 18.1 million shares needed to be issued. For the three months ended June 2023, 1 million warrants were exercised and 6.7 million warrants were exercised subsequently raising nearly $100 million including reduction in senior notes debt. Effectively, the warrant exercise meant that shareholders were diluted by 17.2%. Proceeds will be used to pay off the 2025 Notes, but it likely has made investors cautious as more funds are likely needed to pay off the debt and Triumph Group has already shown its willingness to diluted shareholders in the process.

What Are Analysts Expecting for Triumph Group Q2 FY24?

Triumph Group will be reporting its results on the 6th of November (estimated). Consensus revenue is $337 million pointing at 9.56% year-over-year growth but with expected earnings per share of -$0.02 compared to break-even in the comparable period last year.

Free Cash Flow Is The Problem

{kind=link}

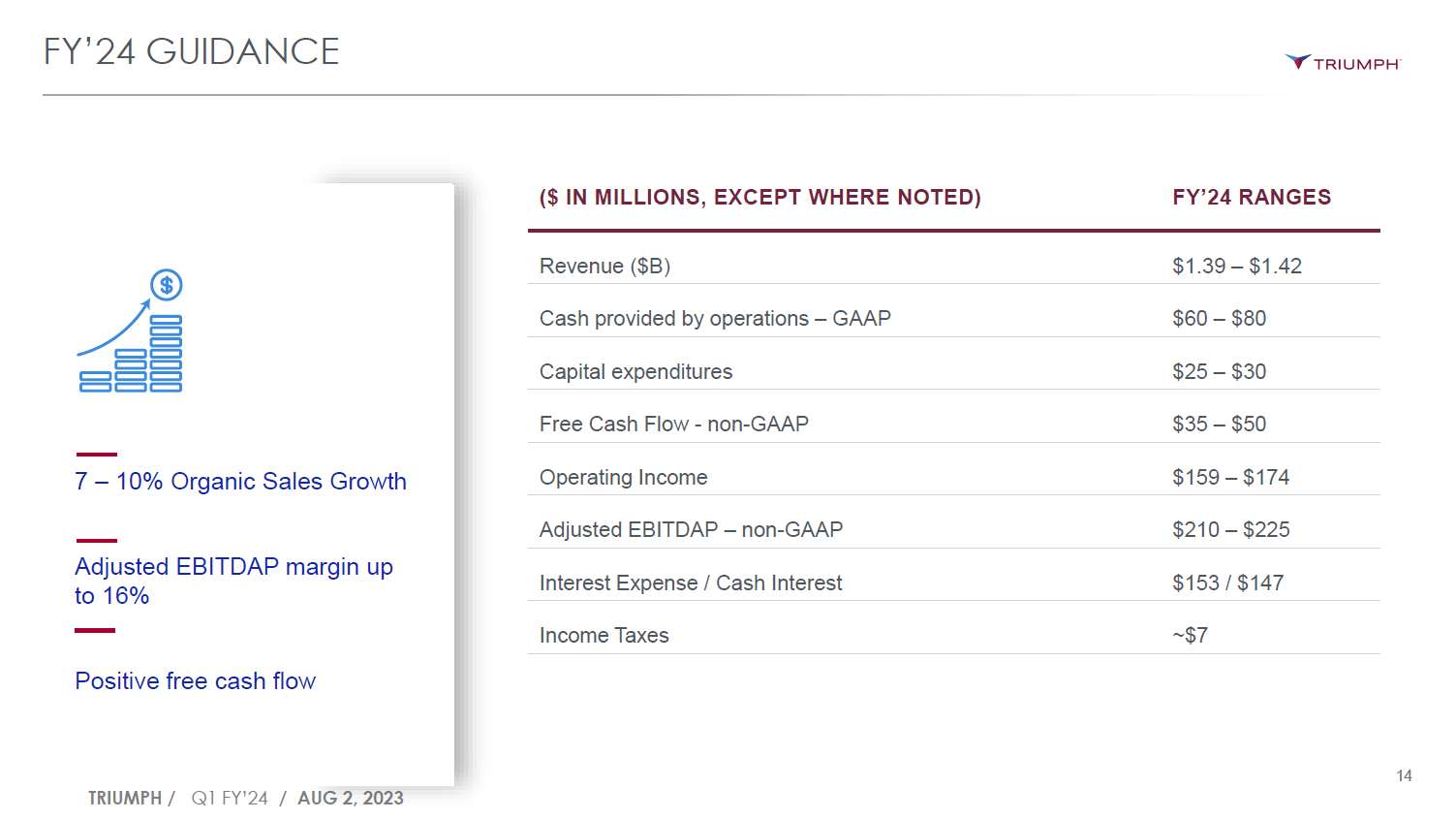

With $500 million due in 2025, one would expect free cash flow to be adequate in the years to come but the reality for Triumph Group is less rosy. For FY2024, the free cash flow will be $35 million to $50 million pointing at a free cash flow margin of only 3% well short of the 7.5 to 15 percent seen in the industry. From FY24 to FY26, around $190 million to $200 million in free cash flow will be generated, which means significant debt refinancing is required or shareholders are at risk to be diluted even further.

Debt Profile Is Keeping TGI Stock Grounded

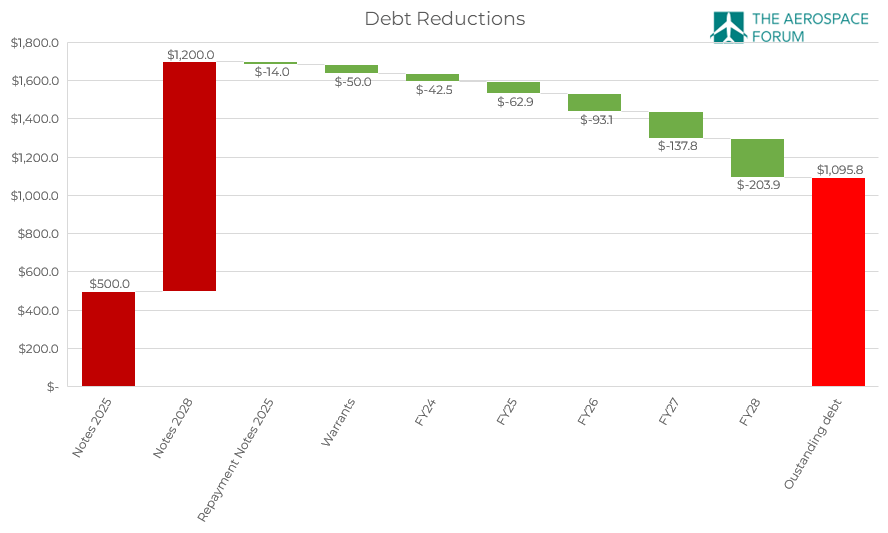

From the 2025 Notes, $14 million out of $500 million has been retired with another $50 million labeled to be used to reduce debt, which would put the outstanding balance for the 2025 Notes at $436 million. Even if we apply the FY24 and FY25 to be used for principal payments, it would reduce the outstanding balance to $336 million.

| Year |

| FCF |

| Sales |

| FCF Margin |

| FY24 |

| $ 43 |

| $ 1,405 |

| 3% |

| FY25 |

| $ 63 |

| $ 1,531 |

| 4% |

| FY26 |

| $ 93 |

| $ 1,669 |

| 6% |

| FY27 |

| $ 138 |

| $ 1,820 |

| 8% |

| FY28 |

| $ 204 |

| $ 1,983 |

| 10% |

In September 2023, TGI stock declined even further as the company outlined a 48% CAGR between FY2024 and FY2028 on 9% CAGR in net sales. My calculations show that indeed an appreciable FCF margin would be reached in this case, but the main issue is that there is $1.2 billion in notes due while the company already seems to be struggling to pay the 2025 Notes back.

{kind=link}

Putting the Notes due 2025 and 2028 together against the repayments, warrants proceeds to be applied to the debt and the free cash flow in the coming years, we see that even if Triumph Group is able to deliver the projected free cash flow it will be inadequate to pay off the Notes which means that the company will have to refinance or dilute shareholders once again.

{kind=link}

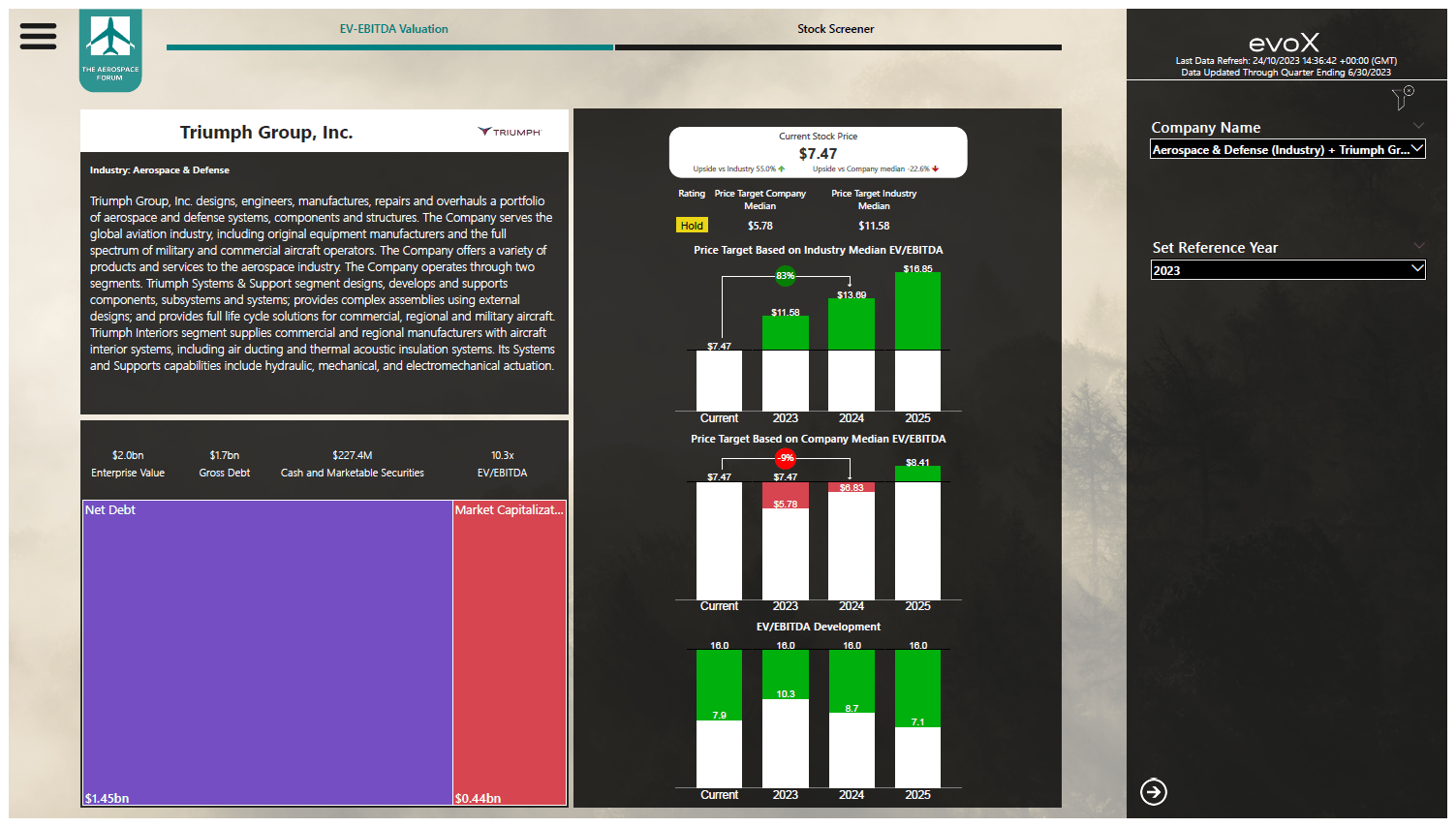

If we look at the projections for the coming years, the company is overvalued by around 9% based on the company median. Valuing the company in line with the industry would provide an appreciable 83% upside, but I don't see any reason why a company struggling to pay its debt with free cash flow should trade in line with its peers. Allowing the share price to reflect FY25 results, the upside would be 13%. Wall Street analysts have a $12 price target implying over 60% upside. However, I don't think that this accurately incorporates the risks faced with regard to favorable refinancing terms of its big pile of debt or possible dilute shareholders in the process of deleveraging.

Conclusion: TGI Stock Is Unattractive Even After a 40% Drop

The drop in share price of 40% exceeded the dilution significantly, but in my view that has not made the stock attractive. Triumph Group expects to grow free cash flow at an annualized rate of nearly 50%, but even that won't be enough to retire the debt associated to the notes due 2025 and 2028, which gives birth to the risk of further shareholder dilution or high cost of debt to refinance. As a result, I maintain my Hold rating for the stock.

For further details see:

Triumph Group: An Uphill Battle Against A Pile Of Debt