TGI - Triumph Group: Bright Aerospace Prospects Little Value Upside For The Stock

2023-06-08 19:54:47 ET

Summary

- Triumph Group, Inc. is seeing promising margin expansion and industry forecasts for airplane production.

- This might be a stock you regret buying years from now.

- Current projections for Triumph Group stock, however, don't justify a buy due to its debt load.

Triumph Group, Inc. ( TGI ) recently announced that General Electric ( GE ) awarded a long-term contract to the company for all variants of the CFM LEAP turbofans that power the Boeing 737 MAX, Airbus A320neo, and COMAC C919. This has sparked my interest in investigating any prospective value for TGI stock.

What Will Drive Growth Going Forward For Triumph Group?

{kind=link}

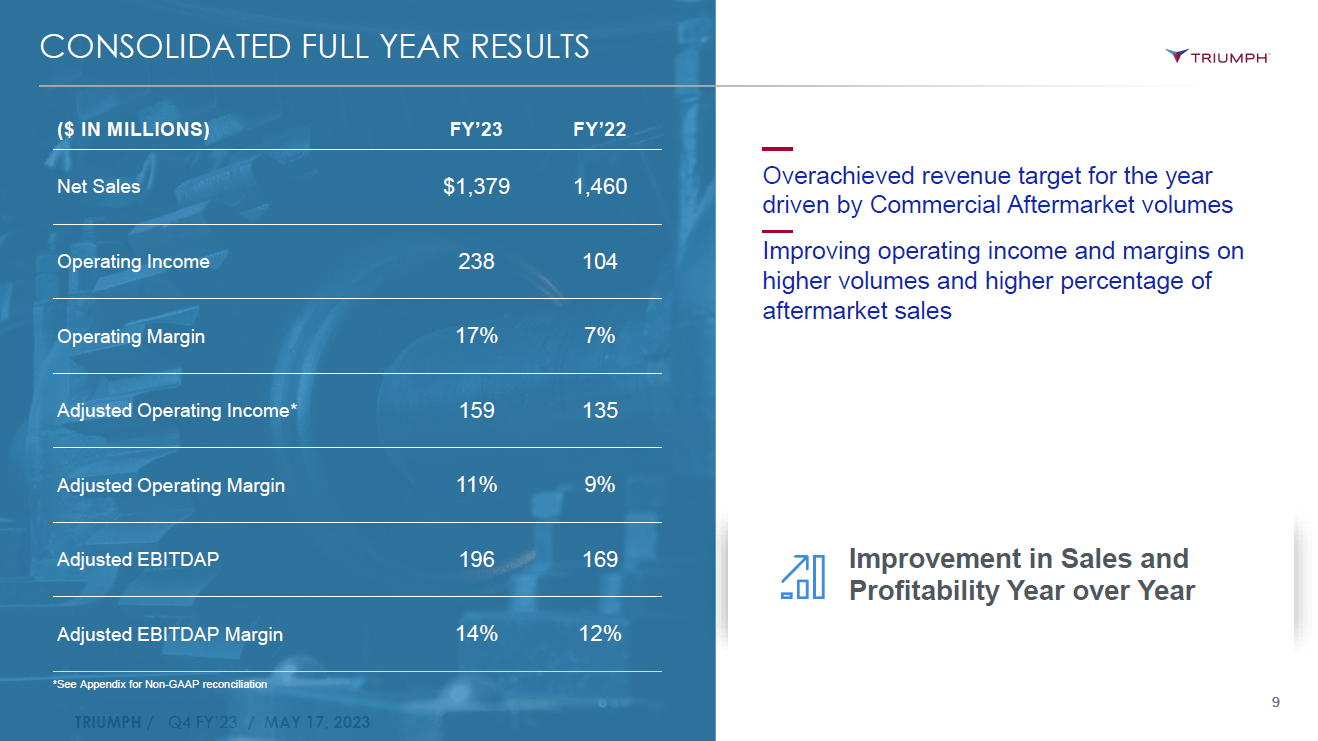

I don’t want to spend most of this report discussing the fiscal Q4 earnings results , but there are a few notable items that are worth highlighting. The first is that revenue declined by roughly 5.5%, or $80 million dollars. This was driven by a $206.9 million decline from divested programs or exited/sunsetting programs. These include the commercial OEM segment and $31.3 million lower defense sales caused by divestitures and lower sales on the E2-D Advanced Hawkeye and AH-64 Apache, and $11.5 million or 5.1% in Military Aftermarket sales due to lower spares and repair volumes.

A significant portion of the decline was offset by higher production for the Boeing 737 and increased sales activity for the CH-53K and CH-47 helicopter programs. Continued strength in reviving the global airline fleet and increasing utilization drove revenues in the commercial aftermarket segment up by $87 million.

We also see that margins improved, and I would attribute that to an overall attractive mix and the divestitures seem to be favorable. It took out almost $210 million in costs, while taking out $238.2 million in sales. This indicated that low-margin and even loss-making business was terminated, pushing the margins higher.

{kind=link}

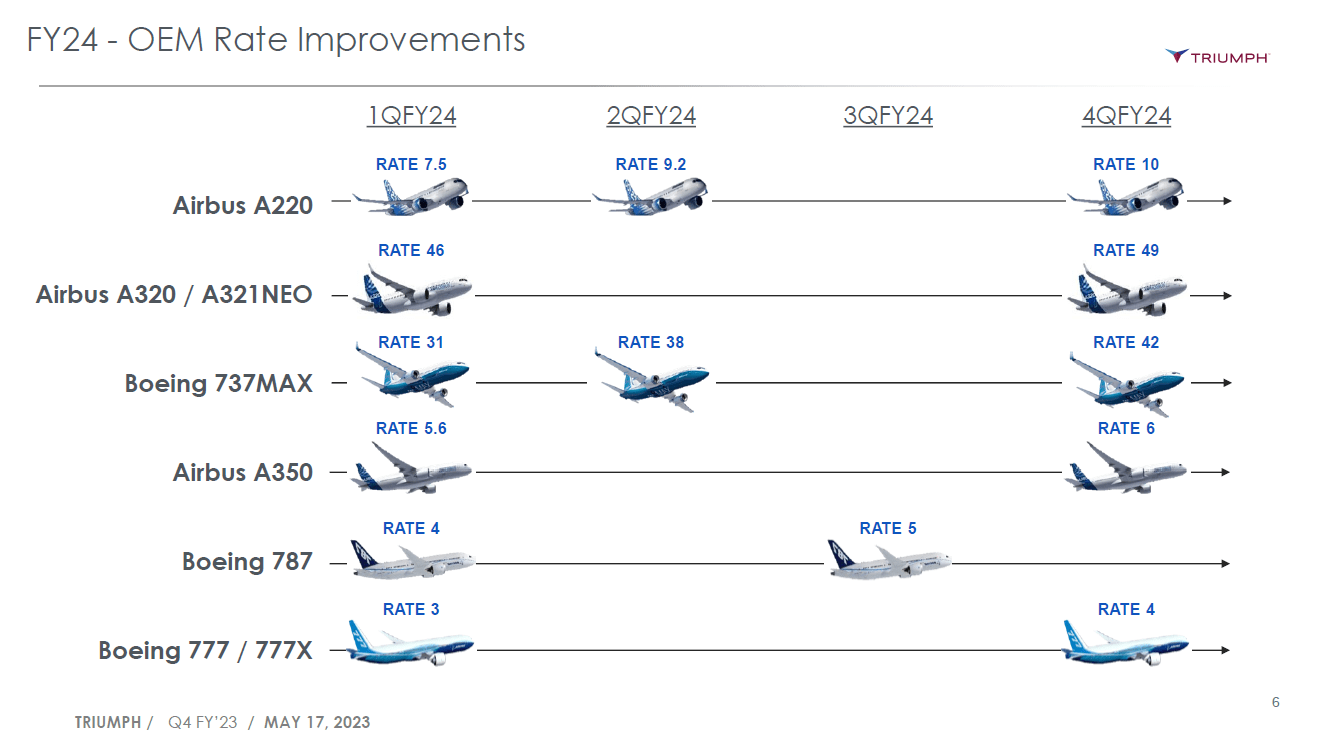

What I liked about the presentation was the slide above. We see that in the current financial year, there are significant increases on the single aisle programs. In addition, the wide body programs are going up in rate. That bodes well for Triumph’s business, with the bigger increases seen at the Boeing (BA) programs. This is driving expectations for 7 to 10 percent organic growth and Adjusted EBITDAP margin to grow to 16% from 14%, with positive free cash flow in the range of $35 million to $50 million from a negative cash flow of $73 million in FY2023.

Is It Enough To Mark Triumph Group Stock A Buy?

{kind=link}

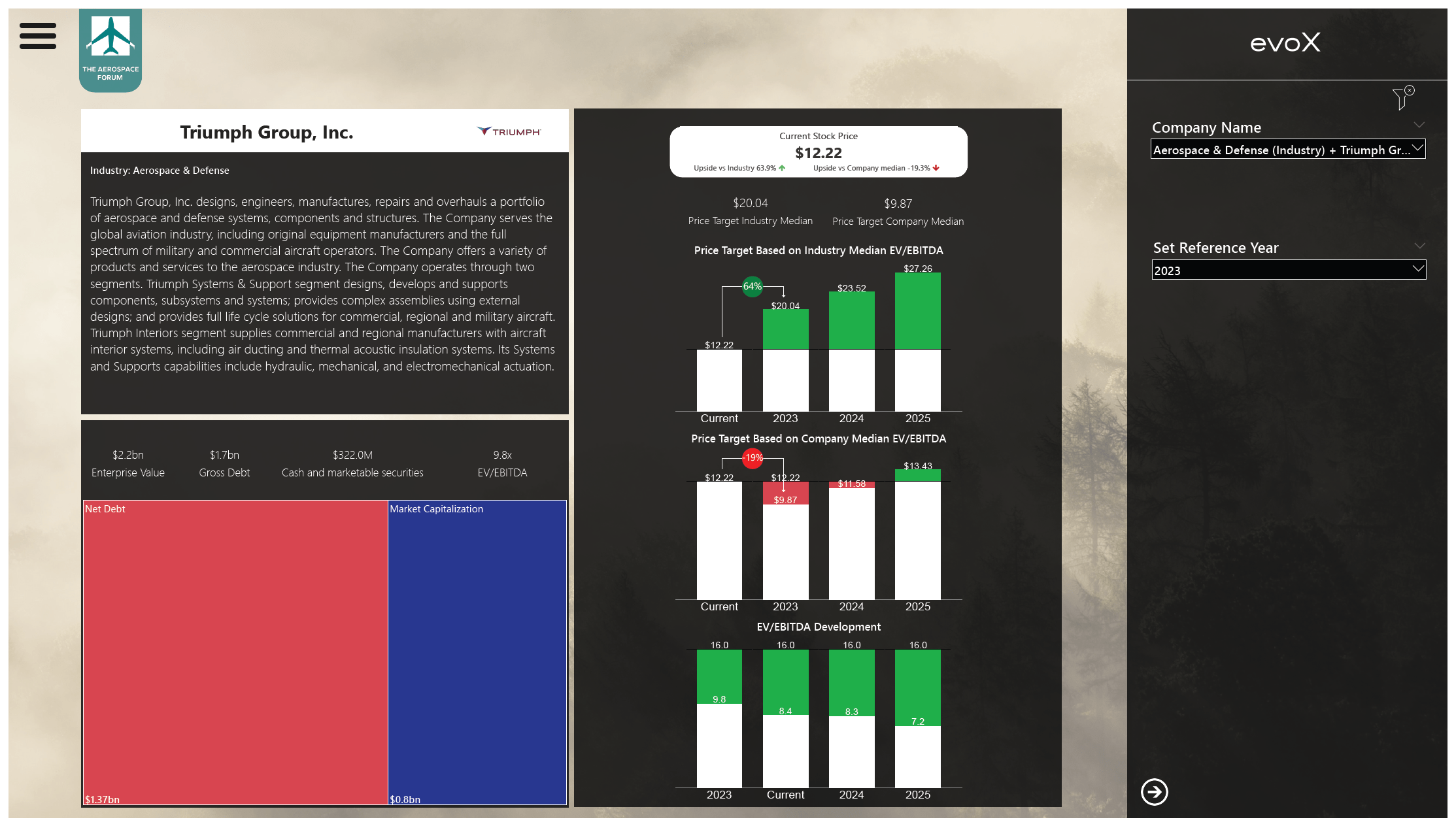

I’ve entered the numbers for Triumph Group into the evoX Financial Analysts tool developed for subscribers of The Aerospace Forum. This is hosting price targets for a growing number of companies in the aerospace and airline industry. I am actually glad I did. When looking at the increases in production rates, I was almost convinced that there would be a strong incentive to buy. Maybe there is, and in five years from now you, will wonder why you did not buy and I might ask myself that same question.

However, with the earnings projections for the coming years, there is little reason to buy. Compared to its own median enterprise multiple, Triumph Group is overvalued for two years ahead, which hardly makes for a strong investment case. Moreover, its net debt of $1.37 billion is going to be a challenge. The company has $500 million in debt repayment due in 2025 and $1.2 billion in 2028, while its cash position in 2025 will not even be $500 million. Simply speaking, this means that the company will highly likely refinance its debt, creating a more manageable maturity profile, but a true deleverage is not something that will happen any time soon.

Realistically, it also would not make sense for Triumph Group to pay a dividend. They might do it since a dividend would be rather small to their cash outflows and also when measured against their debt repayments. However, most of the debt repayment we will be seeing from Triumph Group will be driven by debt refinancing, which will likely continue to be a pressure into the second half of the decade. The company can only hope that by that time the production of commercial airplanes has strengthened substantially, allowing Triumph Group to retire the debt.

Conclusion: Triumph Group Has High Hopes, But Debt Pressures Stock

I think the clear conclusion that can be drawn is that Triumph Group will be benefiting from increased production rates of commercial airplanes. However, given its low cash position relative to its debt, there does not appear to be a lot of upside to TGI stock in the years to come. A sell rating might be a bit harsh, but Triumph Group stock is definitely not a buy in my book. It would be a hold for the extremely patient investor. I would think there are better names to invest in, and that is actually an outcome that surprises me somewhat because things really looked promising for Triumph Group, Inc.

For further details see:

Triumph Group: Bright Aerospace Prospects, Little Value Upside For The Stock