TGI - Triumph Is Cheap: The Stock Decline Cannot Really Be Explained

2023-08-03 09:26:06 ET

Summary

- Triumph Group's recent quarterly results did not justify the significant decline in its stock price in my view.

- The company's new product lines, including fueldraulic actuators and thermal systems, are expected to drive future net sales growth.

- Despite concerns about debt, management expects positive free cash flow growth and announced a small divestiture, indicating potential for higher valuation.

Triumph Group ( TGI ) did not really deliver detrimental figures in the last quarter, but I think that the market did not like the new notes and the increase in debt. In my view, the new fueldraulic actuators, the AH-64 thermal systems, and the CH-53k would most likely accelerate net sales growth in the coming quarters. Besides, management continues to expect future FCF growth, and recently announced a small divestiture, so I would not worry much. In my view, even considering risks from the total amount of debt, the company could trade at a higher valuation.

Triumph Group Q1 2024 Earnings Results

Headquartered in Radnor, Pennsylvania, Triumph Group designs, manufactures, and repairs a long list of aerospace and defense systems and components. The company works with players in the global aviation industry, OEMs, and military and commercial aircraft operators. The following are figures from the last quarter about the distribution of sales by end market.

Source: Investor Presentation

I wrote about the company p reviously. I believe that readers may want to have a look at that article before going through this new update. In my previous assessment, I noted that a decrease in the US Defense budget would most likely be a risk, but I believed that the stock had an upside potential.

Even taking into account a declining commercial aerospace market and a decrease in the US Defense budget, I believe that the company is a buy at the current price mark. Source: Previous Article

Recently, shareholders saw a decrease in the stock price to less than $10-$11 per share, which appears to be a significant reaction to a recent quarterly report. I really do not think that the quarterly report would justify such a dramatic decrease in the stock price. Hence, I took some time to reassess the valuation of Triumph Group.

Source: SA

Triumph Group missed by only $0.05 Non-GAAP, which would not, in my view, explain why the stock price declined more than 21% in a few sessions.

Source: SA

It is also worth noting that both Military OEM sales and Commercial Aftermarket sales increased at a double digit rate driven by organic growth and improvement in overall air travel metrics among other factors. I really do not believe that the quarterly results were that detrimental.

Military OEM sales increased $8.8 million, or 15.5%, all of which were organic, primarily due to increased sales related to the CH-53K, V-22, and UH-60 programs. Source: Press Release

Commercial Aftermarket sales increased $24.5 million, or 38.7%. Excluding impacts from divestitures, organic Commercial Aftermarket sales increased $25.9 million, or 42.5%, driven by the continued improvement in overall air travel metrics, favorably impacting both repair and overhaul services and spare part sales on an equal basis. Source: Press Release

In terms of EBITDAP margin, Triumph Group reported quarterly EBITDAP margin of close to 10.9%, which is close to the figure reported in the same quarter in 2022. Net income margin was also only 0.9% lower than the figure reported in the same time period in 2022. I really do not see that these declines would explain the decline in the stock price.

Source: Quarterly Report

Finally, it is worth noting that Triumph Group noted in the quarterly presentation that it expects positive FCF beyond 2024. I believe that the new information about the future FCF expected is significantly more valuable than the recent small decline in profitability.

Source: Investor Presentation

The Recent Debt Increase May Help Explain Why Some Shareholders Are Selling TGI Shares

I believe that the new list of notes and net debt may explain why some shareholders are selling shares. In my previous article, the company had reported debt including interest close to 6.25%, 7.75%, and 8.875%. In total, the net debt stood at close to $1.469 billion.

Source: Previous Article

In the most recent quarterly report, Triumph noted a note payable in 2028, including interest rate of 9%. The net debt now stands at close to $1.556 billion. I think that the increase in net debt and new interest payable may lower the implied valuation from a DCF model perspective.

Source: Investor Presentation

Balance Sheet: Less Cash Than In March 2023, But Inventory Increased Q/Q

The new balance sheet reported for the quarter ended June 30, 2023 included a decrease in cash as compared to the quarter ended March 31, 2023. As a result, total current assets also decreased to about $871 million, and the total amount of assets decreased to $1.654 billion.

With that, it is also worth noting that the total amount of inventory increased from about $389 million to close to $429 million. I see this change with optimism. Management would not report increases in inventory if it thinks that the business model is not going to perform in the coming quarters.

Source: Quarterly Report

With current liabilities worth $344 million and long-term debt of $1.67 billion, the asset/liability ratio stands at less than 1x, which is not ideal. With that, the state of the balance sheet is not new. In my last article, the asset/liability ratio was also under one.

Source: Quarterly Report

New DCF Model: Higher Cost Of Capital, Lower EV/ Terminal FCF Because Of The Increase In Debt, And The Interest Rate

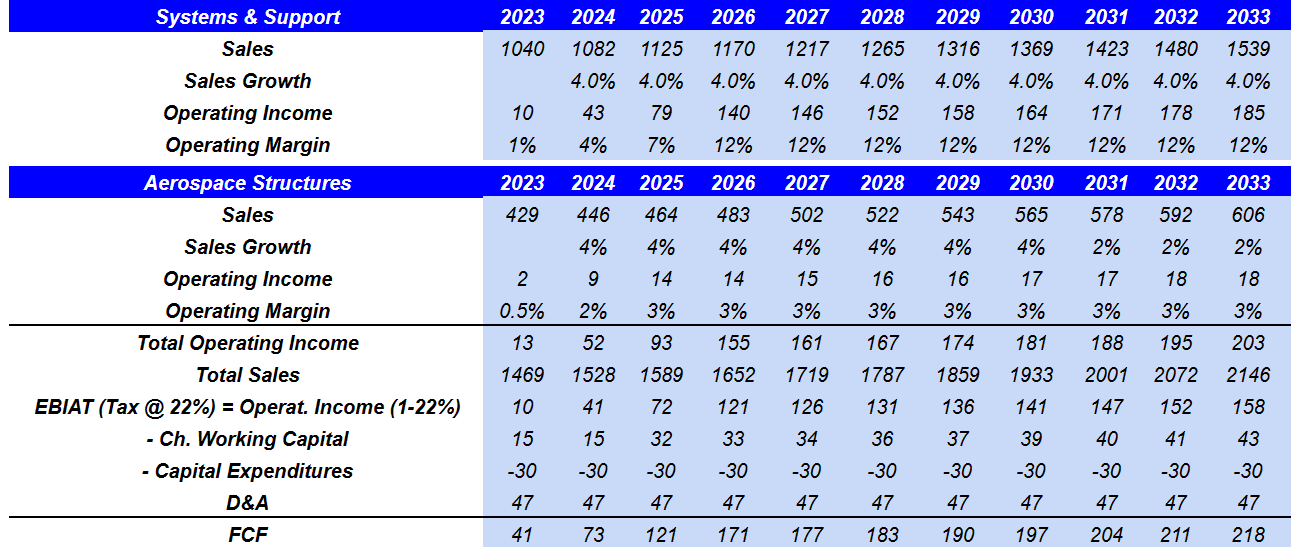

In my new DCF model, I included the new product lines, which were announced recently. I believe that the fueldraulic actuators, the AH-64 thermal systems, and the CH-53k helicopters could accelerate future net sales. The company offered some information in a recent presentation.

Source: Investor Presentation

I also think that new capital expenditures for the Systems & Support operating segment, which offers substantial operating margin, will most likely accelerate the FCF growth. In my opinion, manufacturing efficiency and capacity expansion could also enlarge future net income.

We currently expect full year capital expenditures in fiscal 2023 to be in the range of $25.0 million, of which approximately $22.0 million pertains to our core Systems & Support operating segment. The majority of our fiscal 2023 capital expenditures are capital investments designed to improve our manufacturing efficiency and expand our capabilities. Source: Quarterly Report

Besides, with a lot of property and equipment, inventory, and positive operating margins, I would not discard divestitures in the coming years. As a result, with new cash from sales of divisions, Triumph Group may lower its net debt, and the EV/FCF would most likely trend higher. In this regard, it is worth mentioning that the company noted a divestiture in the last quarter.

Organic cost of sales adjusted for intersegment sales increased by $75.8 million, or 15.2%, partially offset by declines from the Staverton, United Kingdom, divestiture of $10.7 million. Source: Quarterly Report

I lowered my expectations a bit, and also lowered the terminal EV/FCF mainly because of the financial risk coming from increases in the interest rate being paid now. As of today, I assumed a conservative sales growth of 4% and 2033 operating margin of 12% in the Systems & Support division. I also included sales growth of 4% and an operating margin of 3% in the Aerospace Structures division. The results would also include FCF growth.

More in particular, I obtained total operating income of $203 million, with 2033 total sales of $2.145 billion, EBIAT of $158 million, with 2033 changes in working capital close to $42 million, capital expenditures of about -$30 million, and D&A worth $47 million. 2033 FCF would be close to $218 million.

{kind=link}

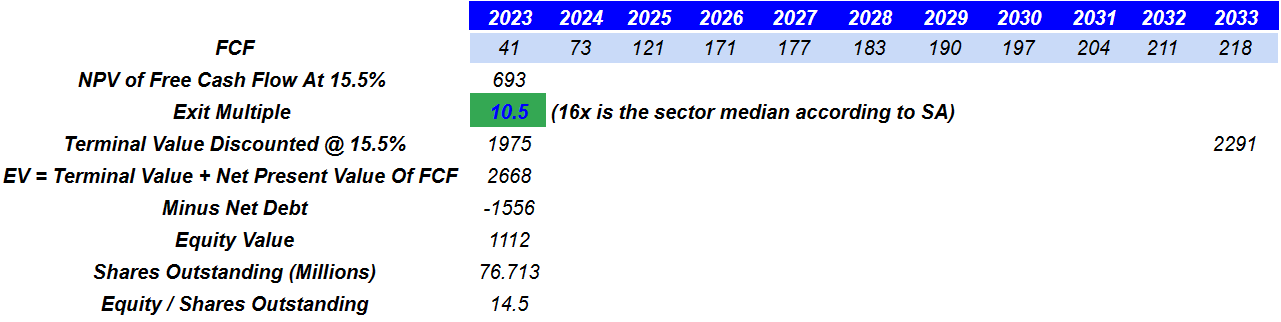

Additionally, with a WACC of 15.5%, the terminal value discounted would be close to $1974 million. If we subtract the net debt, the equity value would stand at -$1.556 billion. Finally, the implied equity valuation would be close to $14.5 per share.

{kind=link}

Other analysts obtained similar results. 9 Analysts obtained an average valuation of close to $13.78 per share, and the higher price target stood at $19 per share.

Source: Market Screener

On a side note, I want to mention that my figures are considerably more conservative than those given by management. In my view, other analysts using the expectation of management would most likely obtain a more fair price than my price target.

In 2024, the company expected net sales close to $1.39 billion, with CFO close to $60-$80 million and FCF of $35-$50 million. It is worth noting that the company expects to deliver organic sales growth close to 7%-10%, which is larger than my net sales growth expectations of around 4%. My numbers are very conservative because I wanted to show that the current stock price of close to $9-$10 is far from reality. I believe that the company is worth much more than that price mark.

Source: Investor Presentation

There Are Some Risks

Apart from the total amount of debt outstanding, I believe that the most serious risk for Triumph Group comes from its exposure to defense-related programs with the U.S. Department of Defense. If the DoD decides to reduce the total amount of money dedicated to defense, or lowers the budget because of some problem related to the U.S. debt , I believe that Triumph may lower its net sales expectations. As a result, I think that future FCF expectations would lower, which may lead to lower stock valuation.

We derive a significant portion of our revenue from the U.S. Government, primarily from defense-related programs with the U.S. Department of Defense. Levels of U.S. defense spending are very difficult to predict and may be impacted by numerous factors such as the political environment, U.S. foreign policy, macroeconomic conditions, ongoing or emerging geopolitical conflicts such as conflict between Russia and Ukraine, and the ability of the U.S. Government to enact relevant legislation such as authorization and appropriations bills. Source: 10-k

Further increases in interest rates or lack of liquidity may impact the ability to renegotiate the debt of Triumph Group. As a result, I believe that the company may not be able to obtain good conditions for its debt. In the worst case scenario, the cost of capital would increase significantly, and the fair valuation would most likely decline.

The company also depends on several contracts with large conglomerates like Boeing ( BA ). If these large clients decide to discontinue some of the relationships with Triumph Group, I believe that we may see sharp declines in sales, which may lead to lower stock prices.

A significant portion of our net sales is to Boeing. As a result, a significant reduction in purchases by Boeing could have a material adverse impact on our financial condition, results of operations, and cash flows. In addition, some of our individual companies rely significantly on particular customers, the loss of which could have an adverse effect on those businesses. Source: 10-k

Considering the total amount of debt and the recent issuance of warrants , in my view, we could expect issuance of shares. As a result, I think that the share count could increase, which may lead to decreases in the fair valuation of Triumph Group. The stock price could decrease.

The company also competes with many large corporations and divisions or subsidiaries of OEM, which may also have larger resources, and may offer better solutions than Triumph Group. Also, clients may decide not to outsource production systems, which may lower the revenue potential for the company.

Our OEM customers may choose not to outsource production of systems, subsystems, components, or aerostructures due to, among other things, a desire to vertically integrate direct labor and overhead considerations, capacity utilization at their own facilities, or a desire to retain critical or core skills. Source: 10-k

Conclusion

I cannot understand how Triumph Group saw a significant decline in its stock price after the figures delivered in the last quarter. Additionally, I believe that investors may soon see revenue growth from the new fueldraulic actuators, the AH-64 thermal systems, and the CH-53k, which were announced in the last quarter. Besides, management continues to expect future FCF growth beyond 2024, so I do not think that shareholders may worry that much. If the company reshapes its balance sheet, and analysts continue to focus on the FCF expectations given by management, Triumph Group will most likely trend higher.

For further details see:

Triumph Is Cheap: The Stock Decline Cannot Really Be Explained