CCHWF - Troubled Trulieve Is A Timely Buy

Summary

- I have followed Trulieve since it went public in 2018.

- The company has evolved from solely a Florida operator to one that is a big player in a few markets.

- The price, near an all-time low, is very attractive.

Trulieve Cannabis ( TCNNF ) went public in September 2018, listing on the Canadian Securities Exchange after completing a reverse-merger. The stock trades slightly lower today and seems very cheap to me relative to its peers. I include it in both of my model portfolios, Beat the Global Cannabis Stock Index and Beat the American Cannabis Operator Index, though I had none to begin 2023. The company has evolved from a Florida-only operation to one that is active in multiple markets. In this piece, I detail the operations, discuss the financials, evaluate its valuation and take a look at the chart. I view Trulieve as the cheapest large MSO.

Operations

The company doesn't break out its revenue by state, but its largest market is Florida, where it is based and where it is a market leader. Trulieve was the first company to begin cannabis sales in 2016, but other producers are selling more now. The market is reported each week by the Office of Medical Marijuana Use, and there are two segments that are important, the medical cannabis products and flower. The state releases unit volumes and not revenue.

In last week's update , Trulieve's market share erosion was very evident:

Alan Brochstein, Florida Office of Medical Marijuana Use

While its share has been eroding, it remains very high. Its 124 stores are by far the leader, representing 23% of the total stores open. Trulieve generated 32.9% of the unit sales of medical cannabis products and 40.2% of the flower sales in the week ending 2/23. On medical cannabis products, the #2 company that week was Ayr Wellness ( AYRWF ) at 17.1% of the market. On flower, Ayr Wellness along with two others, Verano Holdings ( VRNOF ) and Curaleaf ( CURLF ), totaled 33.6% (all about equal).

I am a bit concerned about Florida, though it could legalize for adult-use, which I think would ultimately help Trulieve as the entire state would see growth. The state is highly vertically integrated, with no active wholesale market. This means that the producers must grow what they sell. If the state were to allow less vertical integration, this could hurt the company as smaller operators could quit trying to grow cannabis and buy from those who can grow it more effectively. Margins would come down in this scenario in my view.

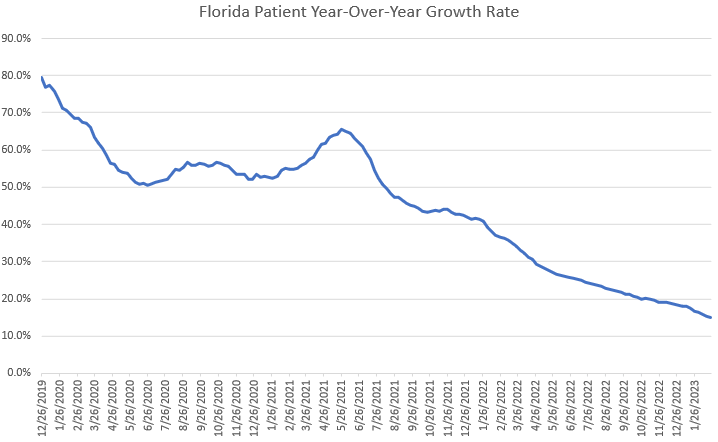

Patient growth, still strong, is slowing dramatically. In the week ended 2/23, year-over-year growth was a record low at 15%:

{kind=link}

The 792K patients are a very high 3.6% of the state's population. The strong growth has been driven by the addition of flower and then edibles to the original set of products sold. Additionally, the state's population growth was very strong following the pandemic. The slowing growth is a headwind.

Outside of Florida, where Trulieve has about 2/3 of its dispensaries, the company's acquisition of Harvest Health added Arizona and boosted its operations in Pennsylvania. Arizona has experienced very slow growth after legalizing for adult-use in 2021. In December, total sales of $108.6 million, according to BDSA, were down 6.4% from a year ago. It was up 18.6% from 12/20, which was before the state moved from medical-only. Pennsylvania, according to BDSA, fell 5.1% from a year ago in December to $102.4 million in medical cannabis sales.

These are the key parts of the company's focus now, though it is active in 9 states currently with two more under development. One can review Trulieve's investor deck from January for more information about the company's operations:

Trulieve_Investor_Presentation_January_2023.pdf

Financials

The company has some debt, but it is not substantial, in my view. Total debt was $553 million, and cash at the end of Q3 was $114.4 million. The net debt is about 1X adjusted EBITDA. The bulk of the debt is private placement notes totaling net $540.3 million. $130 million matures in 2024, and $425 million matures in 2026. The company also reported $220.2 million in deferred tax liabilities.

In Q3, Trulieve reported revenue of $300.8 million, up 34%. Of course, much of the growth was due to M&A. Gross profit in Q3 increased just 9% as the ratio fell from a very high 68.7% to 55.9%. Operating expenses soared by 123%, weighed down by an impairment charge of $52 million. The company moved from an operating profit of $66.3 million to a loss of $25.8 million. TCNNF reported retail revenue of $283.6 million, up 39%, and wholesale revenue of $17.2 million, down 14%. Adjusted EBITDA in Q3 was up 1% to $98.8 million.

For the first three quarters of 2022, revenue increased 48%. Importantly, this isn’t all organic, as the company has purchased Harvest early in Q4 of 2021 and several other deals. Gross margin was 56.8%, down from 68.5%. Operating profit plunged by 79% to $44.7 million. Adjusted EBITDA rose 11% to $315.5 million. Operating cash flow of -$31.9 million was a lot worse than the first three quarters of 2021 at $75.1 million. Capital spending was steady near $191 million.

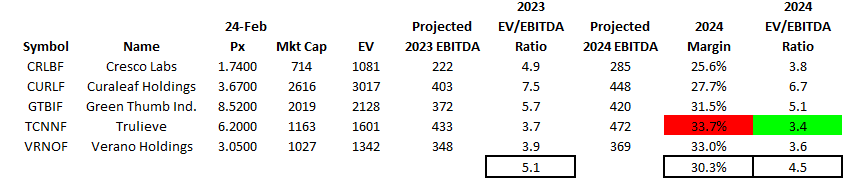

Trulieve had planned to release its Q4 financials this week, but it has changed the date to March 8th. For 2023, analysts project revenue will grow 5% to $1.31 billion. This number has come down over the past six months, as it was $1.44 billion at the end of August. Adjusted EBITDA is projected to gain 5% too, reaching $433 million. In 2024, analysts expect revenue to expand 7% to $1.4 billion with adjusted EBITDA growing 9% to $472 million, the highest among the largest 5 MSOs, which include it and Cresco Labs ( CRLBF ), Curaleaf ( CURLF ), Green Thumb Industries ( GTBIF ) and Verano Holdings ( VRNOF ).

Valuation

Trulieve has a good capital structure in my view. The market cap at $6.20 is $1.16 billion, and there are not many shares that could be created. The price to tangible book value at 6.0X is low compared to its peers, but one can find some leading Canadian LPs that are cash-rich and operating legally federally that trade below tangible book value.

Looking at the 2023 projections, Trulieve is expected to have the second-highest revenue among its peers and the largest adjusted EBITDA. The same can be said for 2024. The table below shows the valuations for 2023 and for 2024 on an enterprise value to projected adjusted EBITDA basis:

{kind=link}

3.4X projected adjusted EBITDA in 2024 is the lowest among the five companies, though its projected margin is the highest. I think that its margin could come down as it expands outside of Florida and as Florida potentially declines for everyone. If one reduces the margin by 20% to 27.0%, the EV/adjusted EBITDA for 2024 would still be 4.3X, which is below Curaleaf, the highest at 6.7X, and GTI, at 5.1X. I recently described here at Seeking Alpha Curaleaf as relatively expensive. Verano is a good comparison, as it is also big in Trulieve's key states of Florida, Arizona and Pennsylvania. I like Verano, but I like Trulieve more.

I can remember when the companies traded at 20X adjusted EBITDA. I am not expecting that to happen this year, but the current ratios are very low. Looking at year-end and using 2024 estimates, I think the stock can get to 7X, though the adjusted EBITDA estimate may come down. At the current expected $472 million, it would be $3.3 billion, which suggests a stock price of $15.30, up 147%. If the margin drops from an expected 33.7% to 28%, the enterprise value would be $2.74 billion at 7X, though the ratio might lift in that scenario. This suggests a price of $12.30, up still by 98%. Perhaps the MSOs will do even better, especially if 280E were to be eliminated or the higher exchanges permitted them to uplist.

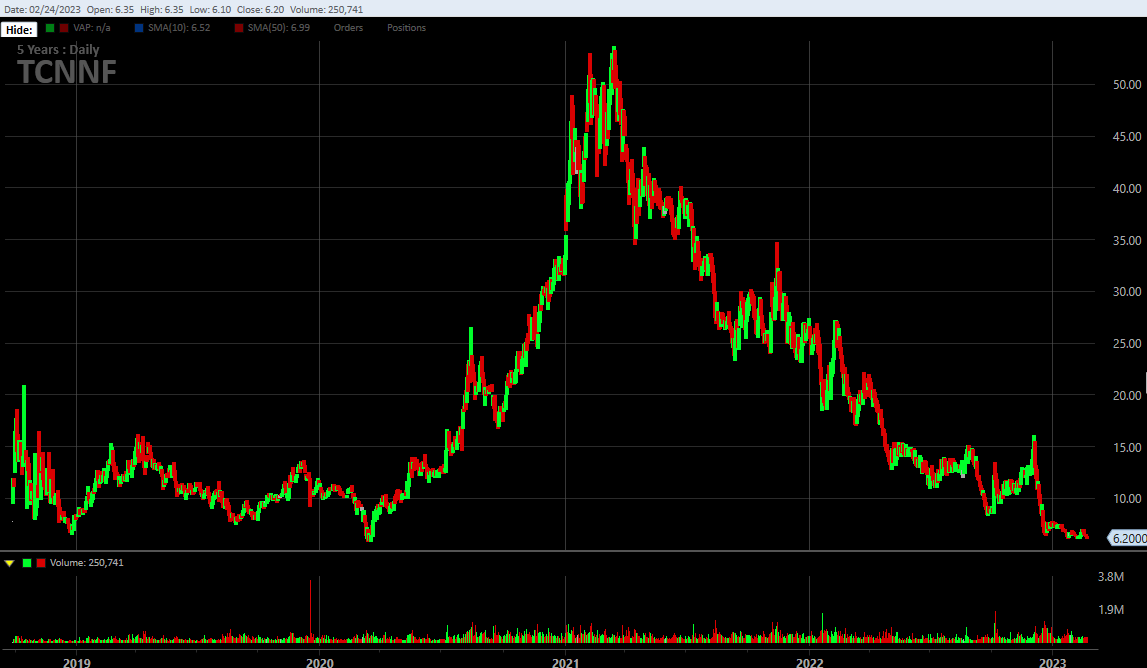

The Chart

Trulieve has been bottoming out this year just above $6, very close to its all-time low set in March 2020 when the stocks tanked following the pandemic becoming an American issue. The stock traded briefly below $6, but $6.00 was the all-time closing low.

{kind=link}

The stock, forming a potential double-bottom, trades just slightly higher than it did in March 2020, while Curaleaf and GTI trade a bit higher compared to then. This chart of relative performance from March 18, 2020, when Trulieve closed at $6.00, illustrates the underperformance since then:

Ycharts

Trulieve was performing better at first, but it has performed worse since the peak. Over the past year, it has fallen a lot more than Curaleaf and GTI:

Ycharts

I think that perhaps investors were too optimistic a few years ago, but they appear to be too pessimistic today.

Another factor in my view is the support that Curaleaf and GTI have gotten from their large shareholder, AdvisorShares Pure US Cannabis ETF ( MSOS ). I have been critical of MSOS for being way too concentrated in the top 5 MSOs, now at 77.5%, but the top 2, GTI and Curaleaf, represent over 45% of the ETF combined. This is currently over $182 million. Trulieve is just 14.4% as of 2/24, which is $58 million. Since November 11th, MSOS has seen its total number of shares fall by 1.8%. It has boosted its ownership of Curaleaf shares by 6.0%, and it has cut its GTI shares by 1.4%. The number of Trulieve shares MSOS owns has dropped 2.0%.

Conclusion

I have been cautious about the largest MSOs for a few reasons, one of which is that large holder MSOS has been suffering shares being redeemed, and the ETF has recently trimmed them. This could get worse, though I am not sure that it will. Beyond that dynamic, the Tier 2 MSOs appear to be very cheap relative to the largest ones. As I described in a recent article about Columbia Care ( CCHWF ), I find it to be an incredible buy opportunity , especially compared to its pending parent, Cresco Labs.

I have always liked Trulieve, but I haven't always liked the stock. I do now, though not as much as some of the Tier 2 names or members of the other sub-sectors. For those who want to invest in American cannabis companies, I think that Trulieve, which could more than double this year, makes a lot of sense.

For further details see:

Troubled Trulieve Is A Timely Buy