TRUP - Trupanion: High Growth Pet Insurance Is Scaling Rapidly

2023-08-22 16:12:58 ET

Summary

- Trupanion's pet insurance business may be recession and inflation resistant.

- Price increases can be passed down to the consumer. Rising vet costs make buying insurance more necessary.

- Trupanion's low price-to-sales ratio and unique position compared to other insurance businesses suggests potential upside.

Trupanion’s ( TRUP ) stock has been beaten down over the past few months. In my humble opinion, this makes the current stock price attractive from a valuation perspective if you view the company as a "growth" story. The company isn't profitable yet but is in the process of scaling its business. In this article, I discuss Trupanion's top-line revenue, the stickiness of its business, and future prospects and risks.

Trupanion Can Resist Macroeconomic Headwinds

Looking at Trupanion’s 10-Q , we can see the company is growing and expanding at a healthy rate. The company’s total number of enrolled pets increased by 25% year over year to 1,679,659. This growth was more or less evenly distributed between the company’s subscription business and its other business. Subscription business represented products under the Trupanion brand name and had 943,958 enrolled pets.

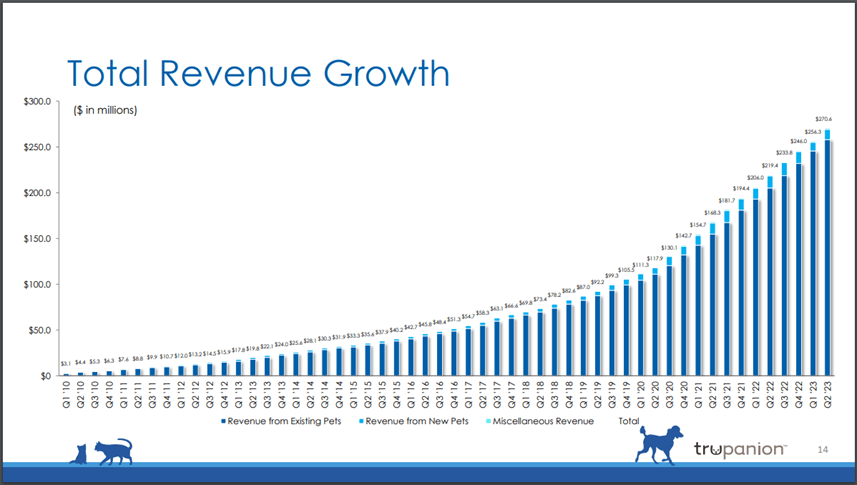

Looking at data from Seeking Alpha , we can see that Trupanion has been growing its revenue at a very healthy pace. The company’s 3-year and 5-year CAGR is at 32% and 30% respectively. In fact, looking at the Quarter over Quarter growth chart, the company has been growing its top-line at a fairly consistent pace even during the height of the COVID-19 pandemic.

Revenue graph (Company Press Release)

{kind=link}

This highlights to me one important fact about this business. For Pet owners, a Pet’s medical well-being is not a discretionary expense. One of the bearish cases I’ve seen about the company is that in the midst of a recession, consumers would start cutting back on spending on Pet insurance. However, this narrative fails to take into account the strong love Pet owners have, which is especially true for Millennials.

Studies have shown that Millennials treat their Pets like family. In a survey , 81% of Millennials have admitted to loving their pets more than certain family members. The survey also showed the extent that Millennials were willing to go to “afford a life-saving treatment” for their Pet. The survey revealed some interesting statistics;

- 49% of Millennials would take on a part-time second job for their Pet

- 43% would sell their TVs

- 41% would sell their laptops

- 29% would sell their jewelry

In fact, Trupanion was able to grow top-line revenue in one of the most uncertain periods in world history, the COVID-19 pandemic. Revenues grew from $304 million in 2018 to $383.9 million in 2019 to $502 million in 2020. Furthermore, the US remains a very large underpenetrated market. North American Pet Insurance penetration is at 3% much lower than for example the UK at 25% or even Australia at 9%. The entire industry is now worth $3.5 billion and continues to grow exponentially. Because of these factors, I am not too worried about Trupanion’s top-line growth prospects.

Rising Veterinary Costs Can be Passed On

The other issue that bears have against Trupanion is the rising veterinary costs. With overall Consumer prices up, it's no surprise that rising costs would start affecting other businesses as well. According to data from the Associated Press, the price for vet services has jumped 10% over the past year, much faster than the general rate of inflation.

This average is double the approximately 5% to 6% historical cost of care for Trupanion. The company actually expects the price for vet services to continue to increase in the next 3 to 4 years to the tune of around 10% to 15%. The rising costs have resulted in a really high loss ratio of 77% for the company’s subscription business (with veterinary invoices at $133.4 million). This number is unsustainable for an insurance company in my view.

In response to these increasing costs, and with the goal to get loss ratios at more economical levels, Trupanion has been increasing prices . The company has requested from New York an 18% increase in rates. This is still pending state approval. In California, the company requested a 28% rate increase but was only approved for 12%. Last June, the company also asked Florida regulators for a 48.9% price hike on top of the 14% hike approved in February. Like what happened in California, I expect Florida state regulators to negotiate this rate down if ever it is approved.

I fully believe these price increases can be passed down to the consumer. If you think about the psychology of insurance, higher medical bills actually necessitate the purchasing of medical insurance. I think of it in my own life, if the average surprise hospital bill was $3000, I could probably fund this with my own savings. But if the average surprise hospital bill is $100,000 for out-of-pocket, you bet I would make it a priority to get covered. The whole point of buying insurance is to avoid catastrophic large outsized costs. So higher medical costs actually pressures people to buy insurance. The same dynamics apply to Pets if we make the assumption that these animals are considered to be “family members”.

Trupanion Insurance (Investor Presentation)

{kind=link}

Valuation and Conclusion

In my view, you can't really evaluate TRUP stock like other legacy insurance businesses. It wouldn't be an apples-to-apples comparison. Trupanion is currently in a "Blue Ocean" of opportunity and unknowns vs more traditional companies that have established business models.

Pulling out various companies' Forward Price to Sales Ratio, we can see that Trupanion is at the lower end of a P/S of 1.1x. This ratio is much lower than what other subscription companies from the tech industry are trading for (3x to 5x P/S).

I've seen arguments that Trupanion isn't a tech firm. That may be true but it is still a subscription business that is growing at a 20%+ CAGR. Lemonade ( LMND ) another fast-growing new type of insurance company has a P/S ratio of 2.3x. We can even use another fast-growing traditional specialty insurance company, Markel ( MKL ) as a benchmark of 1.3x.

I am currently valuing TRUP stock at 1.5x forward sales which at the current price levels would imply a price target of $39.5. This is a 40% increase from the current stock price. The main risks I see are on the regulatory side, if price increases are blocked by the government. However, I believe the risk to reward is favorable for this stock.

For further details see:

Trupanion: High Growth Pet Insurance Is Scaling Rapidly