TRUP - Trupanion: Pet Insurer Facing Headwinds

Summary

- Trupanion is an insurance business, not a subscription business.

- High churn and cost pressures could pressure business.

- TRUP stock could trade under $10 if valued similarly to other insurance companies.

While Trupanion ( TRUP ) touts itself as a subscription business, in reality it is an insurance company. In fact, the company tries to downplay that it's an insurance company, hardly providing any of the typical insurance company metrics you'd see in these companies' filings. The fact of the matter is that it operates a high-churn, low-margin pet insurance business. Meanwhile, the stock trades at a huge multiple to tangible book value ((TBV)), the valuation metric investors typically associate with P&C insurance companies.

Company Profile

TRUP provides medical insurance for cats and dogs throughout the United States, Canada, Puerto Rico, and Australia. Its primary "subscription" business uses a cost-plus model designed to spread the risk evenly within each category of pets.

The company considers its biggest differential to be the use of proprietary software to quickly pay vets directly for approved invoices. The company uses territory managers to help promote its offerings to vet offices and hospitals, who then in turn will market TRUP insurance to their clientele.

In its "Other Business" segment, the company underwrites pet insurance for third parties at a very low gross margin, typically around 7%.

Creative Metrics

TRUP likes to play up its own created metrics. One such metric is adjusted operating income, where it gives operating income excluding customer acquisition costs. Given the company's high 15%+ churn and low gross margins (13-14%), this isn't a particularly useful metric with which to look at the business. The pets that the company insures, meanwhile, become more expensive to service and then die out. This forces TRUP to continue to have to aggressively replace its pet customer base with new and younger pets.

TRUP also likes to talk about its over 30% IRR in its annual investment letter. However, the company straight-line churns, when in fact the company said during its IPO roadshows that the bulk of churn happens in year 1. This throws off the calculation and makes it look better than if it modeled churn how if typically occurs.

{kind=link}

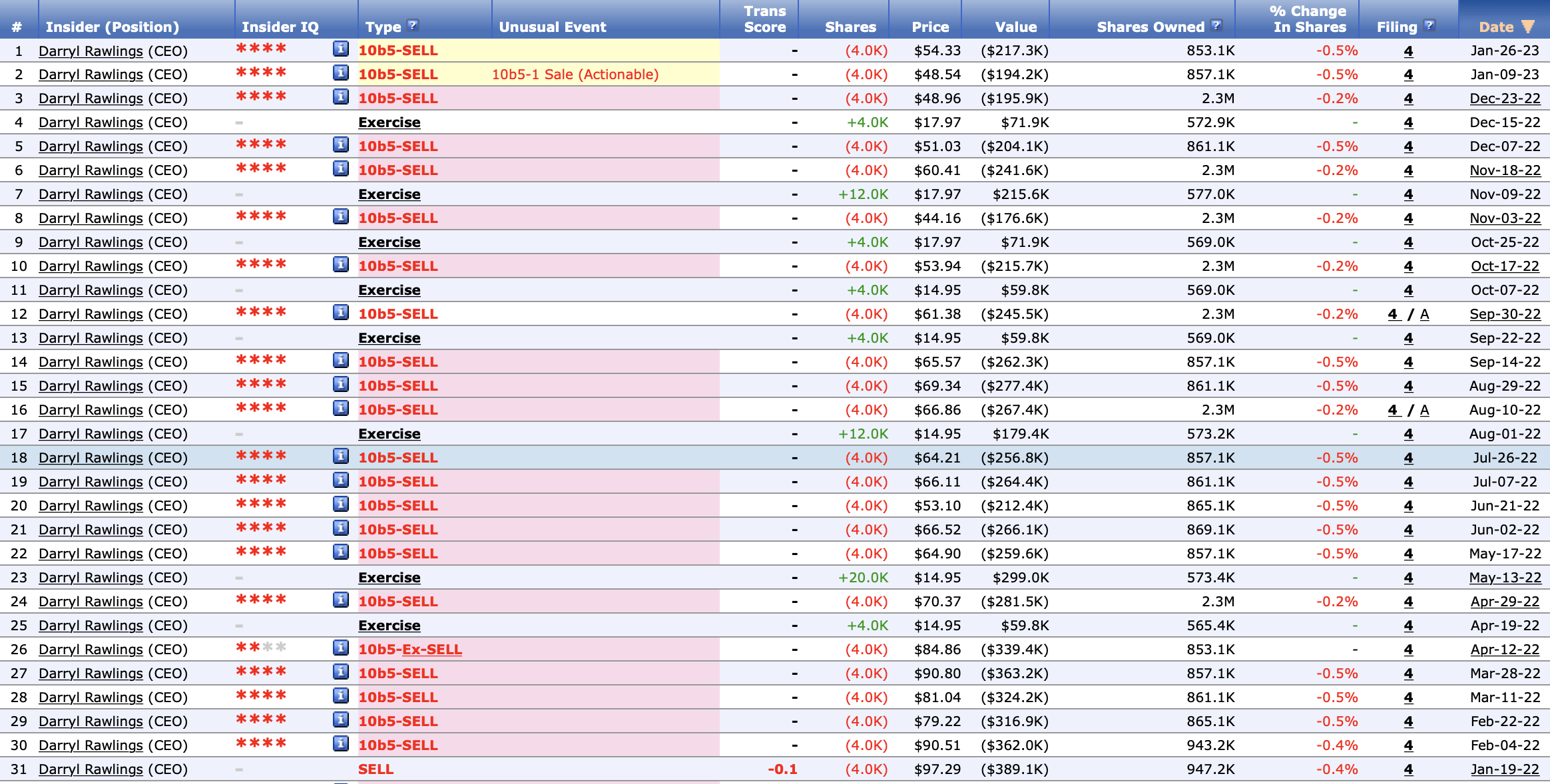

CEO Selling Stock

At the same time, CEO Darryl Rawling continues to aggressively exercise long-dated options then sell the stock.

{kind=link}

Down Side Risks

TRUP is currently facing several headwinds. One of the biggest is margin pressure.

The company noted on its Q2 earnings call that vet inflation of 8-12% is nearly double the 5-6% historical trend. Not surprisingly, in Q3, the company began to see margin pressure from these higher vet costs. Subscription gross margins fell -250bps to 15.9%. ARPU and its projected lifetime value of a pet both fell sequentially. ARPU dropped -0.7% to $63.80, while lifetime value fell -5.6% quarter over quarter to $673. Pet acquisition costs also fell, down -13% sequentially to $268. The company said ARPU has been impacted by mix of business.

In addition, the pet insurance sold by TRUP is not cheap, and could be an expense that households drop (or don't purchase) as the economy weakens. TRUP already aggressively raises its customers' premiums year in and year out, and in Q3 after seeing margin pressure the company indicated it was about to get even more aggressive with price increases in 2023.

On the Q3 call , President Margaret Tooth said:

"Absent the impact of mix changes, cost of invoices was up approximately 10% over the prior year period, outpacing our average rate increase of 7% for the same period. As Darryl alluded, we are taking actions to get ahead of the changes we are seeing in veterinary medicine. Absent the impact of changes in mix, we now have pricing increases of 11% flowing through into early 2023 with another 7% planned going into next year. We will continue to closely monitor the rate of inflation and are poised to roll forward additional pricing adjustments as needed in the coming months. As a reminder, rate changes are immediate for new enrollments but are applied for existing pets once every 12 months. So the impact of these changes will flow through in 2023 with the full benefit showing up in late 2023, and we anticipate being back on track to hit our margin target."

TRUP already has a high churn business, with about 15.5% of pet owners canceling their insurance with TRUP each year. If a weakening economy and higher renewal rate price hikes further increase churn, this would be very bad for the company. The company also needs new, younger pets to replace the pets it churn, so any slowdown in adding pets would also be harmful.

In addition, the company also seems to get distracted from its core U.S. pet insurance business. The company is currently testing a pet food offering, which is obviously greatly strays from its core insurance offering. It has also recently made some questionable overseas acquisitions, buying pet insurance companies in the Czech Republic and Slovakia.

Conclusion

TRUP has been a strong-performing stock over the years, often praised for its steady growth and the fact that its CEO writes good shareholder letters and compares himself to Warren Buffett.

The company loves to grow its top line, yet generally does so with little economic benefit. In fact, its TBV has fallen from $6.91 per share at the end of 2020 to $6.13 at the end of last quarter. The reason behind this is that TRUP is not a sticky SaaS company with high margins, it's a high-churn, low-margin insurance company that is now facing margin pressure. Despite this, at over $60, the stock trades at nearly 10x TBV while P&C insurance stocks often trade below 1x TBV.

TRUP's answer for its deteriorating margins, meanwhile, is to aggressively increase prices (by 18%) for its already high-churn business going into a weakening macro environment for a product most of its customers will not use. Meanwhile, it looks to be making silly acquisitions while its CEO aggressively sells shares.

In addition to not creating much economic benefit for shareholders, TRUP also doesn't have the benefit of a typical insurance company float (the cash insurers hold and invest that has yet to be paid out to claims). Buffett claims much of his success to being able to invest using Berkshire's ( BRK.A ) cost-free float.

Unfortunately for investors, the CEO writing good letters and comparing himself to Warren Buffett is not a strong investment thesis.

If the stock were to be valued similar to other insurance companies, the stock could fall to below $10 a share.

For further details see:

Trupanion: Pet Insurer Facing Headwinds