WMB - TTP: A Lot To Like With This 8.12%-Yielding MLP CEF

Summary

- Pipeline companies and MLPs are very good investments for income investors.

- These companies are very recession-resistant, pay out high yields, and have forward growth potential.

- The closed-end fund Tortoise Pipeline & Energy Fund includes some of the best companies in the industry, which should benefit its investors.

- The fund can easily maintain its distribution as its capital gains in the first half of 2022 were sufficient to cover three years of payouts.

- The fund is trading at a double-digit discount to the net asset value.

For decades now, master limited partnerships ("MLPs") have been among the favorite investments for income-focused investors. This makes a great deal of sense, as most of these companies are pipeline operators or other midstream energy firms, which tend to enjoy a remarkable amount of cash flow stability regardless of the broader conditions in the economy. Although there have been several companies that have converted to a corporate structure, their partnership fundamentals remain and they continue to pay out reasonably high yields.

Unfortunately, there are two problems with master limited partnerships. The first is that they can be very difficult to include in a tax-advantaged account such as most retirement accounts. This is due to the somewhat complicated nature of their taxation. The second problem is that it can be difficult to put together a diversified portfolio of these companies unless one has access to a substantial amount of capital.

Fortunately, there is an easy solution to both of these problems. That solution is to invest in the shares of a closed-end fund ("CEF") that specializes in investing in midstream companies and partnerships. This is because these funds provide easy access to a professionally-managed portfolio of companies with one very easy stock trade. In addition, many of these funds can boast a higher yield than any of the underlying companies actually possess.

In this article, we will discuss the Tortoise Pipeline & Energy Fund ( TTP ), which is one fund that investors can use for this purpose. As of the time of writing, the fund boasts a respectable 8.12% yield, so it can certainly prove attractive to an income seeker, and considering that many of these companies have fairly strong fundamentals, the fund may be able to deliver some solid benefits going forward. Therefore, let us investigate and see if this TTP fund could be a good purchase today.

About The Fund

According to the fund’s webpage , the Tortoise Pipeline & Energy Fund has the stated objective of providing its investors with a high level of total return. This makes sense considering that this is an equity fund. In fact, fully 99.59% of the fund is invested in common equity, with the rest consisting of cash:

CEF Connect

This is somewhat unusual for a fund, as we do not see very many that go all-in like this. It does make sense for this fund, though, since the traditional energy sector is substantially undervalued and has been for a while. I pointed this out in various previous articles as well as in a recent blog post . The same undervaluation applies to pipeline operators just as it does to upstream oil and gas producers. This is the big reason why the Alerian MLP Index ( AMLP ) currently has a 7.24% yield.

It makes a lot of sense for a common equity fund to be focused on total return as opposed to some other goal. This is because common equity is by its nature a total return vehicle. After all, most investors that purchase common equity are seeking both income through dividends and capital appreciation as the issuing company grows and prospers. In the case of midstream companies, this is particularly true as many of these firms have far higher yields than just about anything else in the market as well as boasting growth potential. For example, Canadian midstream giant Enbridge Inc. ( ENB ) currently pays a 6.53% dividend yield and is on track to produce CAD$16 billion in EBITDA in 2023, compared to only CAD$2.5 billion in 2008:

Enbridge

Enbridge is currently the second-largest holding in the fund:

CEF Connect

As my regular readers are no doubt well aware, I have devoted a great deal of time and effort to discussing midstream companies here at Energy Profits in Dividends as well as at Seeking Alpha. As such, every company on this list should be reasonably familiar. In fact, I have discussed every company on this list numerous times in the past except for Plains GP Holdings ( PAGP ), but that is simply the general partner of the familiar Plains All American Pipeline ( PAA ) and has very similar fundamentals. Overall, these are all among the best companies in the midstream sector, and many of them have fairly significant forward growth potential. For example, The Williams Companies ( WMB ) is currently expanding its enormous Transco pipeline system to keep up with the growing demand for natural gas in New York and New England. Energy Transfer ( ET ) is partnered with a major ethane exporter to supply natural gas liquids to the Gulf Coast, which I discussed in my last article on the company. In short, we should be able to expect most of these companies to be able to grow their cash flows over the next few years.

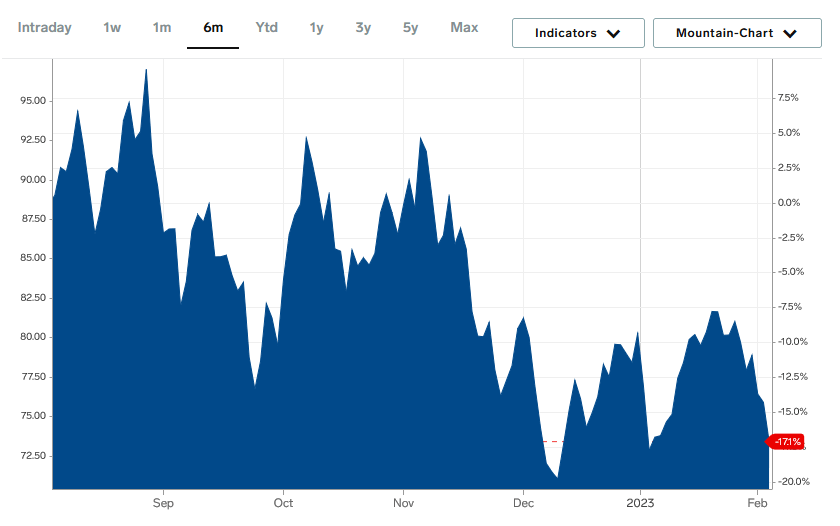

As everyone reading this is likely well aware, crude oil prices were incredibly strong during the first half of 2022, but they have since come down quite a bit:

{kind=link}

As we can see, the price of West Texas Intermediate crude oil is down 17.1% over the past six months. Fortunately, midstream companies are not particularly affected by this due to the business model that these companies use. In short, a midstream company enters into a long-term (typically five to fifteen years in length) contract with a customer under which the customer utilizes the midstream infrastructure to transport hydrocarbon resources. The customer then compensates the pipeline owner based on the volume of resources transported, not on their value. This provides a great deal of protection against fluctuations in energy prices. Indeed, although their market performance might make you think otherwise, companies like MPLX ( MPLX ) had virtually no change to their cash flows due to the pandemic or the decline in oil and natural gas prices that accompanied it. This cash flow stability is quite nice for our purposes as income investors because it provides a great deal of support for the distributions that these companies pay out. After all, it is much easier to pay out a sizable proportion of cash flow when the company can be confident that a similar amount of money will be available next year.

Indeed, many of these companies do pay out a sizable proportion of their cash flow compared to other industries. Analysts usually consider a midstream company’s distribution to be sustainable if its cash flow is only 120% of its distribution, but most of them pay out between half and two-thirds of their cash flows to the investors. These distributions would, of course, become income for the Tortoise Pipeline & Energy Fund, which it then passes through to its own investors.

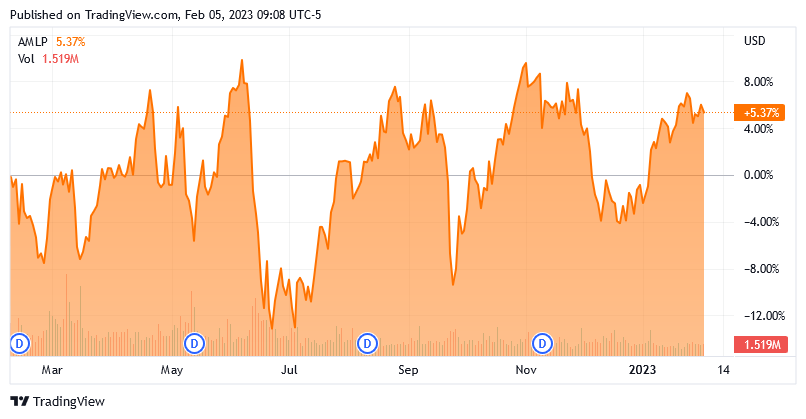

We have also seen significant capital gains among many midstream companies over the past year or two. This is in stark contrast to the rather disappointing performance of the rest of the market. The Alerian MLP Index is up 5.37% over the trailing twelve-month period:

{kind=link}

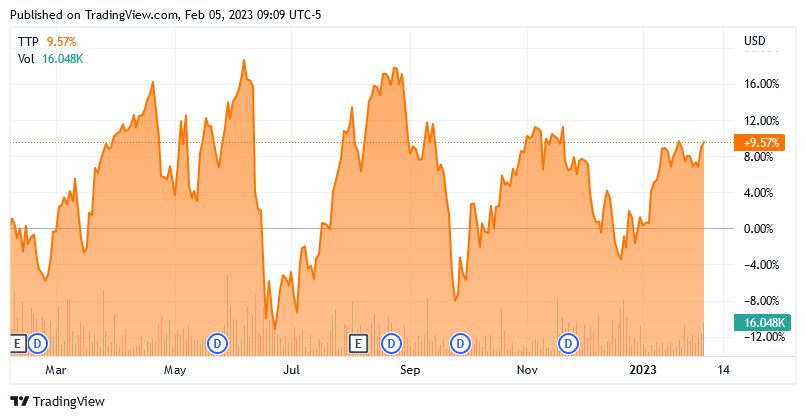

The Tortoise Pipeline & Energy Fund has certainly not disappointed, either. In fact, the fund has beaten the index and appreciated 9.57% over the same period:

{kind=link}

When we consider that the Tortoise Fund has a higher yield than the index, we can clearly see that an investor in the closed-end fund would have done much better than an index investor. That is particularly true for an investor that reinvests the distribution into shares of the fund, which is the recommended strategy unless one really needs the distributions to cover their personal expenses. This, interestingly, makes this one of the few closed-end funds to have beaten its corresponding index over the past year. One potential reason for this is that this fund employs leverage to boost its returns, which we will discuss in just a few minutes.

As my regular readers on the topic of closed-end funds are likely well aware, I do not generally like to see any individual asset in a fund account for more than 5% of the fund’s portfolio. This is because that is approximately the point at which an asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, then the risk will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market in aggregate does not. If that particular asset accounts for too much of the portfolio, it may end up dragging the entire fund down with it.

As we can see above, this fund has seven companies whose weightings surpass that 5% limit. This is certainly a bit concerning but hardly unusual. In fact, nearly all midstream closed-end funds have a fairly high weighting to only a few companies. This is due to the fact that there are only a limited number of midstream companies in the United States and Canada that are actually publicly traded. This is partly due to the industry consolidation that has occurred over the past decade or two. Despite being commonplace among any sector fund, investors should still ensure that they are willing to be exposed to the risks of these companies before making an investment in the fund. In this case, though, the largest positions in this fund are among the largest and most financially-secure companies in the industry so pretty much anyone that is willing to invest in the midstream sector, in general, will be more than happy to have exposure to the companies that comprise the top ten holdings of this fund.

Fundamentals Of Midstream

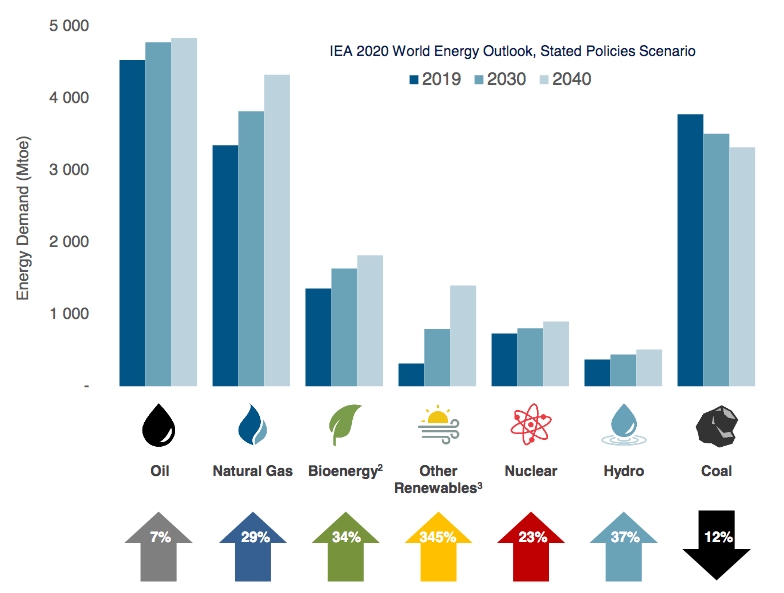

Earlier in this article, I stated that midstream companies have fairly strong fundamentals and growth prospects. This may seem surprising since midstream companies make their money by transporting crude oil and natural gas and we have all heard from politicians and the media that these fuels will soon become obsolete. However, nothing could be further from the truth. In fact, the International Energy Agency projects that the global demand for natural gas will increase by 29% and the global demand for crude oil will increase by 7% over the next twenty years:

{kind=link}

Perhaps surprisingly, it is climate change concerns that will drive the demand growth for natural gas. As everyone reading this is no doubt well aware, these concerns have induced governments all around the world to impose a variety of incentives and mandates that are intended to reduce the carbon emissions of their respective nations. One of the most common of these incentives is to encourage electric utilities to retire old coal-fired power plants in favor of renewable energy. Unfortunately, wind and solar energy are not reliable enough to support the needs of modern society. After all, wind power does not work when the air is not moving. Solar energy does not work at night and is less effective on cloudy or rainy days, which are quite common in many parts of the world. The usual solution to these problems is to supplement renewables with natural gas turbines since natural gas is reliable enough to provide the “always-on” power that most people expect from the electric grid. It also burns cleaner than any fossil fuel so it still serves the goal of reducing carbon emissions.

The case for crude oil may be more difficult to understand, particularly as many governments are pushing things such as electric cars that will reduce the demand for gasoline and other refined products. However, it is a very different story if we look at the various emerging markets around the world. These nations are expected to benefit from significant economic growth over the projection period that will have the effect of lifting the citizens of these nations out of poverty and putting them securely into the middle class. These newly middle-class people will naturally begin to desire a lifestyle that is much closer to that of their counterparts in the developed nations than what they have today. This will require increased energy consumption, including energy derived from crude oil. As the populations of these nations substantially outnumber the populations of the various developed nations around the world, the growing crude oil consumption in these nations will more than offset the impact of stagnant-to-declining crude oil consumption in the developed nations.

Naturally, the growing demand for hydrocarbons will require increased production of these resources to satisfy that demand. However, as we have already discussed, the midstream companies like the ones owned by the Tortoise Pipeline & Energy Fund do not actually produce any resources. Nevertheless, they will still benefit from this demand growth. This comes from the fact that the United States and to a lesser extent Canada are among the few countries in the world that have the ability to increase their production of crude oil and natural gas in order to satisfy this demand. This is due to the wealth of regions like the Permian Basin and the Marcellus Shale. In order for this production growth to proceed, the producers would need to get the resources to the market where they can be sold. This is exactly the function performed by midstream firms. As we have already discussed, these companies see their cash flows increase when transported volumes increase and obviously this scenario would result in increased volumes of resources flowing through their pipeline infrastructure. Thus, the midstream companies in which the fund is invested should be able to deliver growth as this situation plays out. This is exactly the reason why many of them are constructing new infrastructure. Ultimately, this should all result in distribution and unit price growth, which will obviously benefit investors in this fund.

Leverage

As mentioned in the introduction to this article, closed-end funds like the Tortoise Pipeline & Energy Fund have the ability to generate higher yields than those possessed by any of the underlying assets. In addition, we also saw that this fund was able to beat the index in terms of capital gains over the past year. One of the methods that it uses to accomplish both of these things is the use of leverage. Basically, the fund borrows money and uses those borrowed funds to purchase shares or partnership units of midstream companies. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield and gains of the portfolio. This fund is able to borrow money at institutional rates, which are substantially lower than retail rates. As such, this will usually be the case.

However, the use of leverage is a double-edged sword because debt boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I generally do not like to see a fund’s leverage less than a third as a percentage of its assets for this reason. Fortunately, this fund is fulfilling that requirement. As of the time of writing, its leveraged assets comprise 21.77% of the fund’s portfolio. Thus, the Tortoise Pipeline & Energy Fund appears to be running a reasonable balance between risk and reward. This is a good situation overall.

Distribution Analysis

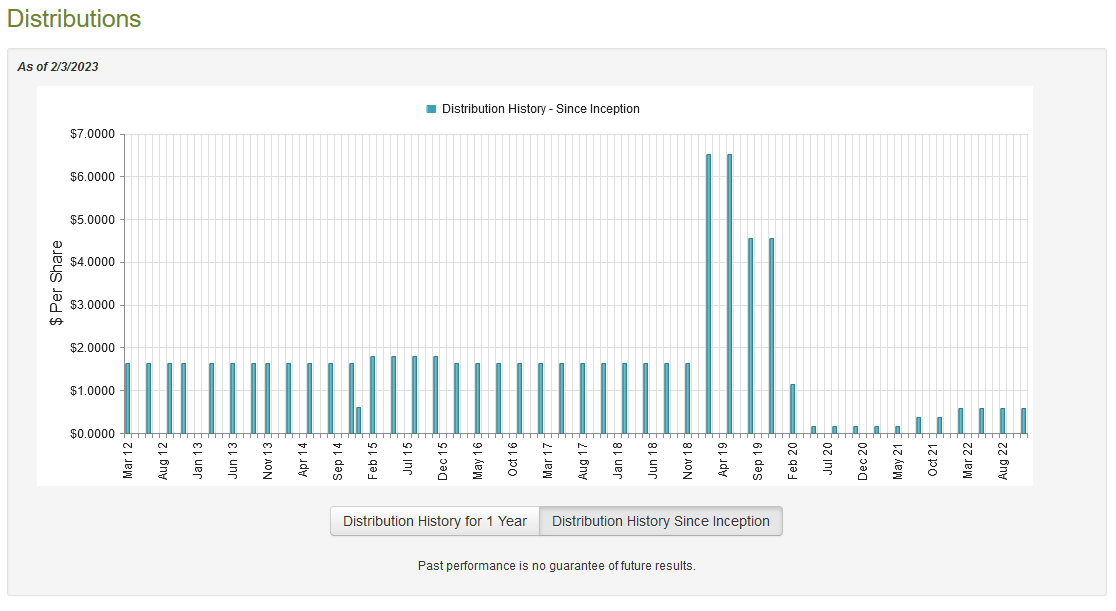

One of the biggest reasons why investors purchase midstream companies is the high yields that they tend to possess. Indeed, the Alerian MLP Index currently yields 7.24%, which is higher than just about any other index in the market today. The Tortoise Pipeline & Energy Fund takes this to a new level by employing leverage to boost the overall yield and return. As such, we might assume that the closed-end fund boasts a suitably high yield itself. This is certainly the case as it pays out a quarterly distribution of $0.59 per share ($2.36 per share annually), which gives it an 8.12% yield at the current price. Unfortunately, the fund has not been particularly consistent about its payout over the years as it has varied a great deal since 2019:

{kind=link}

The fact that the fund’s distribution has been somewhat inconsistent may be a bit of a problem for some investors. However, it is not surprising given the events of the past few years. Back in 2020, crude oil prices collapsed following the imposition of the pandemic-related lockdowns due to the severe reduction in demand. Although this had a very limited impact on the cash flows of midstream companies, some of them still cut their distributions in order to reduce debt and become almost completely independent of the hostile capital markets. That would naturally reduce the money flowing into the fund so it would have to cut its payout as a result. That is hardly unique as pretty much every midstream fund cut its payout during that time. We have slowly seen a restoration of the distribution as various midstream partnerships have increased their own distributions, although it still remains well below pre-pandemic levels. However, anyone purchasing the fund today would receive the current distribution at the current yield and so the fund’s past is not really the most important thing. The important thing for us today is to determine how well the fund can maintain its current distribution.

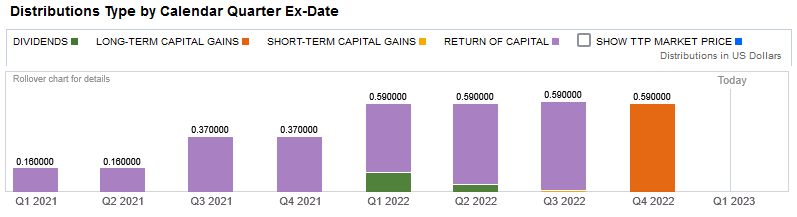

The fact that the fund’s distributions consist almost entirely of return of capital is not particularly encouraging:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. Obviously, this is not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital. One of these is the distribution of money received from a master limited partnership. Another is the distribution of unrealized capital gains. As these are both things that this fund might be doing, we should investigate exactly how it is financing its distributions in order to determine exactly how sustainable they are likely to be.

Unfortunately, we do not have a particularly recent document to consult for that purpose. The fund’s most recent financial report corresponds to the six-month period that ended May 31, 2022. As such, it will not include any information about the fund’s performance over the past eight months, which was a weaker period of performance for most of these companies than the first half of 2022. Nonetheless, it should still at least give us some insight into the cause of the return of capital distributions that the fund made over the period. During the six-month period, the Tortoise Pipeline & Energy Fund received a total of $1,249,990 in dividends and $45 of interest from the investments in its portfolio. It is important to note that these figures do not include the $1,460,895 that the fund received from the various master limited partnerships in its portfolio as those are considered to be a return of capital distribution. We will discuss that later. Overall, the fund reported a total income of $1,250,035 during the period. It paid its expenses out of this amount, which left it with $202,386 available for the shareholders. That was obviously nowhere close to enough to cover the $2,628,772 that it actually paid out in distributions during the period. This may be concerning at first glance.

However, the fund has other methods of obtaining the money that it requires to cover the distribution. One of these is through earning capital gains. The period in question was a very strong one for the energy industry in general and as might be expected, the fund had a great deal of success at earning capital gains during the period. The Tortoise Pipeline & Energy Fund reported net realized gains of $375,428 and another $19,205,074 net unrealized gains over the course of those six months. This was easily more than enough to cover the distributions. In fact, the fund saw its assets increase by $17,154,116 during the six-month period after accounting for all inflows and outflows. That increase would include all of the capital gains as well as the money that the fund received from the various master limited partnerships in the portfolio. Overall, we can clearly see that it is in pretty good shape financially as that increase alone was sufficient to maintain the distribution for more than three years. We should not have to worry at all about the fund reducing the distribution.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that portfolio. In the case of a closed-end fund like the Tortoise Pipeline & Energy Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. As we have seen in several previous articles here at Energy Profits in Dividends, this is the case with many midstream closed-end funds. It is the case with the Tortoise Pipeline & Energy Fund as well, which is nice because this implies that we are purchasing the fund’s assets for less than they are actually worth. As of February 3, 2023 (the most recent date for which data is available as of the time of writing), the Tortoise Pipeline & Energy Fund had a net asset value of $33.75 but the shares only trade for $29.07 apiece. This gives the shares a 13.87% discount to the net asset value at the current price. This is not as attractive as the 16.26% discount that the shares have averaged over the past month, but frankly, any double-digit discount like this is a very reasonable price to pay for any closed-end fund today. Overall, the price here is very reasonable.

Conclusion

In conclusion, pipeline operators and master limited partnerships are very good companies to include in any income portfolio. This is because of their general stability and growth potential over the coming years. The Tortoise Pipeline & Energy Fund certainly looks to be a good way to add these companies to your portfolio as it has outperformed the index over the past twelve months and still manages to boast a higher yield. The fund also includes some of the best companies in the industry and can easily sustain its 8.12% current yield. When we combine this with an attractive valuation, there is much to like here with Tortoise Pipeline & Energy Fund.

For further details see:

TTP: A Lot To Like With This 8.12%-Yielding MLP CEF