TWST - Twist Bioscience: Biopharma And Data Storage Are Underappreciated

2023-03-08 11:36:51 ET

Summary

- Ongoing losses are likely to continue weighing on the stock, particularly as the Portland site starts up and begins to drag on gross profit margins.

- 2024 is potentially setting up to be a more positive year for Twist, with the launch of their data storage business and growing momentum in the Biopharma business.

- Twist's business appears undervalued, particularly when the latent value in Biopharma projects with downstream value, internal Biopharma projects and data storage are taken into consideration.

Twist's (TWST) stock price continues to flounder under the weight of large losses and declining growth. Much of this has been driven by a weak macro environment and ongoing investments in future products. In addition to secular growth within their core business, Twist can also potentially capitalize on a large data storage opportunity and downstream value within their Biopharma business. These opportunities, which are not reflected in current financials, do not appear to be reflected in Twist's valuation.

Market

Twist has exposure to a number of large and growing end markets, and estimate that their SAM is approximately 6 billion USD. This estimate is only for their core Synbio and NGS businesses, and does not take into consideration their Biopharma and data storage initiatives. Twist has stated that they are gaining market share in both Synbio and NGS by expanding their customer base, delivering differentiated high-quality products and anticipating market needs.

Twist's DNA makers market estimate is based on their being 120,000 medical researchers and 150,000 academic researchers, although it remains to be seen how much of this market Twist can actually capture. The liquid biopsy/MRD SAM is expected to increase to 2.2 billion USD by 2027 as sequencing costs decline and adoption of liquid biopsies increases.

Biopharma and data storage could both provide significant upside to Twist's addressable market. For example, the archiving market is currently worth around 35 billion USD, although DNA data storage is only likely to capture a fraction of this.

Table 1: Twist Estimated SAM (source: Created by author using data from Twist Bioscience)

Factory of the Future

Twist's Factory of the Future recently began shipping product and will be an important determinant of gross margins over the next few years. Oligo Pools and Gene Fragments are now being shipped from the Wilsonville site, and clonal genes are expected to begin shipping soon.

The initial targeted turnaround time is approximately 10 to 12 days for genes. As production in Portland is increased, Twist expects to introduce fast genes with premium pricing. Other Synbio products that will be introduced at the facility include long panels, impossible genes and R&D-based products.

The Factory of the Future will enable faster turnaround times , which will open up new time sensitive markets. Twist refers to researchers who currently make their own DNA for time reasons as the makers market. This includes large companies that in-source, as well as academic labs and medical researchers. Speed is critical to this group, which has so far disqualified Twist as a vendor. Genes are available today from competitors at a fast turnaround time, but their capacity is limited and the cost can be prohibitive.

With the new facility, Twist plans on offering gene synthesis that is the same or faster than if they did it themselves. The current process in San Francisco involves multiple steps , some of which require utilizing the same machines. As a result, DNA spends half of its time in freezers waiting for machines to be available. The Portland facility has more machines so that this bottleneck is removed. Twist is hoping to convert a significant portion of the makers market to customers when the Factory of the Future is fully operational.

In the fourth quarter of 2022, Twist had a manufacturing team training and producing test products at the facility. During this period there were 177 employees in Portland , 40 of whom had relocated from San Francisco. Twist has so far invested around 87 million USD in the Factory of the Future, and plans on investing another 20 million USD. This facility is expected to provide sufficient capacity for Twist to achieve in excess of 350 million USD annual revenue.

Synbio

Twist's Synbio vertical continues to grow at a reasonably robust pace, with 558,000 genes shipped in fiscal year 2022 compared to 372,000 genes in fiscal year 2021, a 50% increase. Future growth is likely to come from existing customer growth, as well as the introduction of new products. Twist is planning on introducing fast DNA, long fragments, RNA and GMP products in the Synbio vertical.

Twist believes they are competitive in Synbio because of their:

- Cost

- Scale

- Quality

- Customer experience

- Innovative products

In early 2022 Twist announced a new 4-year supply agreement with Ginkgo Bioworks ( DNA ) that includes a minimum of 58 million USD in product purchases over the contract lifetime. This is important as Ginkgo has historically been one of Twist's most important customers.

NGS

Within the NGS vertical, Twist wants to own the workflow between the sample and the sequencer. This is a market that could grow substantially, driven primarily by oncology. Twist is tracking around 20 key liquid biopsy customers and have been adopted in a number of their tests. As a result, Twist expects their volumes to increase in line with customer test volumes.

Twist estimates that its market share within target enrichment and library prep is currently 16%. Twist continues to win pilots which they believe bodes well for future growth. Within NGS, Twist expects the year to be back half-loaded .

Twist believes they are competitive in NGS because they offer:

- Quality

- Uniformity

- Lower sequencing costs

- Rapid customization

- Fast throughput

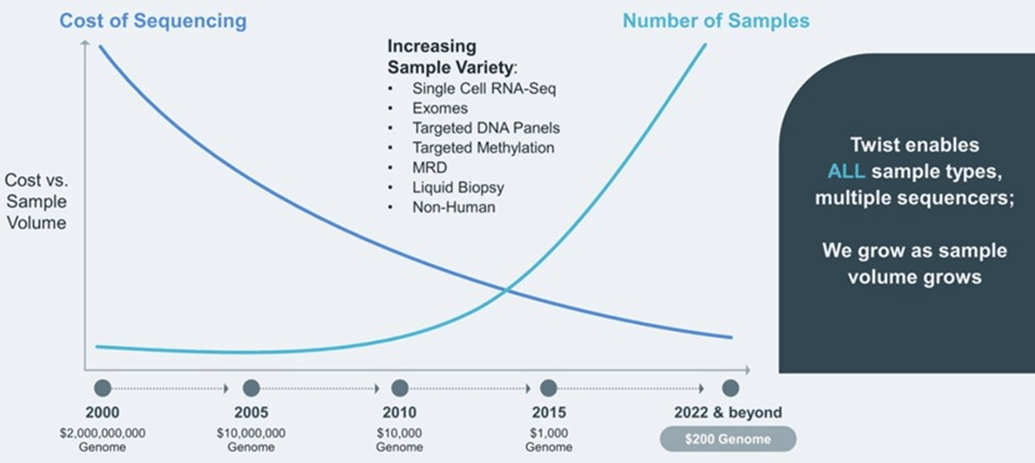

Advances in long read sequencing and less expensive whole genome sequencing options are causing shifts in the sequencing market. Twist believes this is an opportunity rather than a threat though, as they are sequencer agnostic.

Figure 1: Sequencing Costs and Sample Variety/Volume (source: Twist Bioscience)

{kind=link}

As sequencing costs continue to decline, some applications are likely to shift from exome sequencing to whole genome sequencing. When applications like germline sequencing, or population sequencing initiatives, move from exome to whole genome sequencing, Twist believes that they will have an opportunity to continue participating through their library prep offering.

Within oncology, the requirement for deep sequencing means that exome sequencing will remain the mainstay. Twist also believes that lower sequencing costs will lead to wider adoption of liquid biopsies and greater insurance coverage.

Figure 2: Genome Sequencing Viability (source: Twist Bioscience)

{kind=link}

Twist has been expecting the decline in sequencing costs for several years and has introduced new products to support expansion, most of which target cancer. Recent product launches include:

- A methylome panel

- cfDNA controls for liquid biopsy

- A patient-specific MRD panel targeting up to 500 mutations

Twist also plans on introducing an RNA sequencing workflow and SNP microarray conversion.

Biopharma

Twist's Biopharma business is based around their competitive advantage in DNA synthesis, which allows them to build unmatched libraries for screening. Twist is also targeting the launch of a combined service offering with Abveris in the second quarter of 2023 . This combination is expected to yield synergies that Twist believes will expand their reach and market share in the biopharma segment. Twist will be able to offer in vitro synthetic libraries, in vivo discovery and screening, and in silico lead optimization, candidate selection and optimization with machine learning.

Monetization options for the Biopharma business include:

- Upfront payments

- Spinouts

- Out licensing

- Milestones and royalties

Twist spun out their COVID-19 antibody program, committing 10 million USD in seed funding to Revelar. The program did not yield the outcome that Twist was hoping for though and Twist was quick to abandon the program.

Twist signed a discovery collaboration with MediSix in early 2022 . MediSix Therapeutics is a cell therapy company targeting T-cell leukemia and lymphoma. Under the agreement Twist will discover five novel antibodies directed against MediSix's targets. In return, Twist will receive an upfront payment and will be eligible for success-based milestone payments and royalties on product sales.

Twist also signed an agreement with Kriya Therapeutics to discover antibodies for applications in oncology and gene therapy.

Twist entered into a multitarget antibody discovery collaboration with Astellas Pharma. In addition to an upfront payment and research fees, Twist will be eligible to receive up to 11 million USD per product in milestone payments and royalties on product sales.

Some of Twist's new partners are focused on optimization projects, which typically do not include milestones and royalties. They are often a useful way for Twist to demonstrate their capabilities to customers though, and can lead to larger agreements later on. These types of fee-for-service projects typically take 3-6 months to complete.

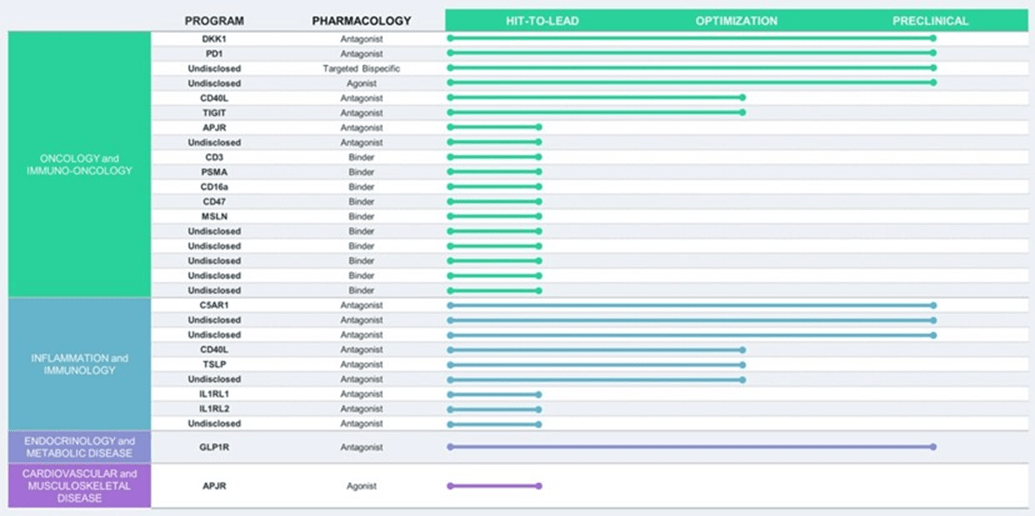

Twist also continues to advance a number of internal candidates through the early discovery stage and have several antibodies that have reached the preclinical stage. This could lead to out licensing by partners in time.

Figure 3: Twist's Internal Pipeline (source: Twist Bioscience)

{kind=link}

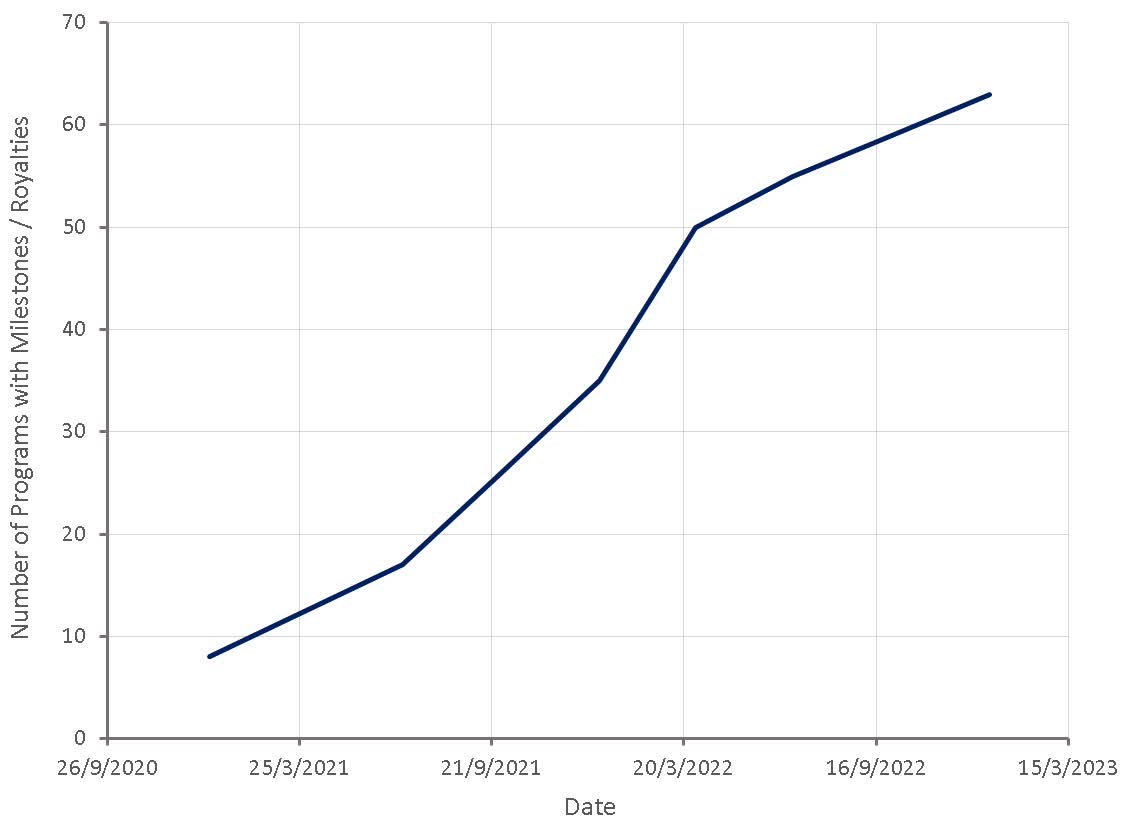

Twist continues to build up projects with either milestone payments or royalties. This is expected to provide significant economic return at some point in the future. They are not currently providing guidance on this though as payment timing and amounts are difficult to anticipate.

Figure 4: Twist Potential Downstream Value (source: Created by author using data from Twist Bioscience)

{kind=link}

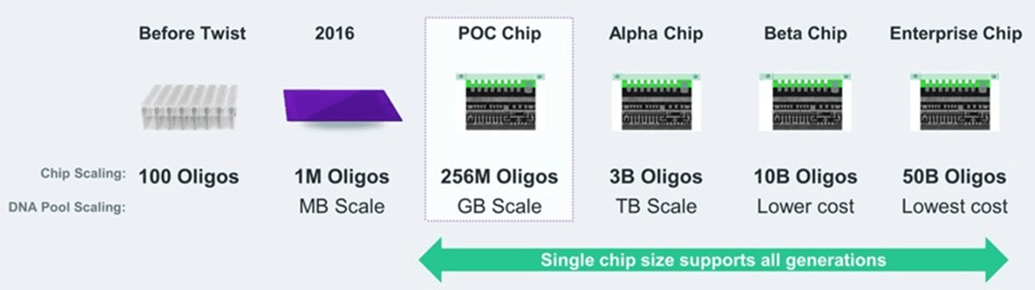

Data Storage

Twist currently has 37 employees working on their data storage team, although a commercial product is not expected in the short-term. Twist is currently working on a chip that they expect to enable limited early customer engagement. This is a fully integrated CMOS chip with electronic control that Twist is developing to achieve synthesis of up to 1 gigabyte of data in a single run. Twist is also working to integrate the chip into their prototype electrochemistry DNA writer system. They recently assembled a proof-of-concept writer, and are now writing software to coordinate all the steps required to code, write, to sequence and decode digital data.

Twist also continues to work on the Alpha chip which they believe will lead to an inflection in the market. The Alpha chip will have greater density per unit area, which is expected to drive down costs significantly. As the technology matures and increasing automation can be realized, Twist expect to introduce an accessible archive solution targeted towards data centers.

Figure 5: Evolution of Twist's Data Storage Technology (source: Twist Bioscience)

{kind=link}

In parallel, Twist continues to advance their enzymatic synthesis approach. This is a low-cost scarless azelaic process to synthesize DNA that Twist expects to use for their enterprise data storage offering. Twist is still trying to optimize:

- Error rate

- Length of the DNA

- Speed of the reaction steps

- Overall cost

Once the technology has been developed, Twist will add applications that are suited to the enzymatic approach. This could include a decentralized OEM option or cell-free creation of blended DNA or other markets that Twist is not currently serving.

Twist is competing for tape, hard drive and flash memory. Their solution becomes more economical over time as DNA data storage avoids the expenses of migration, maintenance and energy. An early access product is expected to launch in late 2023, initially targeting customers within Media/Entertainment, Big Science/Healthcare, Preservationists and Governments.

Short Report

The Scorpion Capital short report is largely based around the accusation that Twist competes in a commodity market with undifferentiated technology and is only growing by engaging in predatory pricing, resulting in large losses.

The report claims that despite having costs that are actually higher than competitors, Twist prices their products 50-90% below the competition. Twist has been able to reduce the amount of reagents used by 99.8% compared to a plastic-plate platform. Reagents are a substantial driver of COGS, and this is an important component of Twist's lower cost base relative to competitors. Twist has also designed their technology so orders for multiple customers and multiple projects can be grouped on the one chip. Orders are synthesized in parallel on the chip, allowing Twist to leverage differentiated scale.

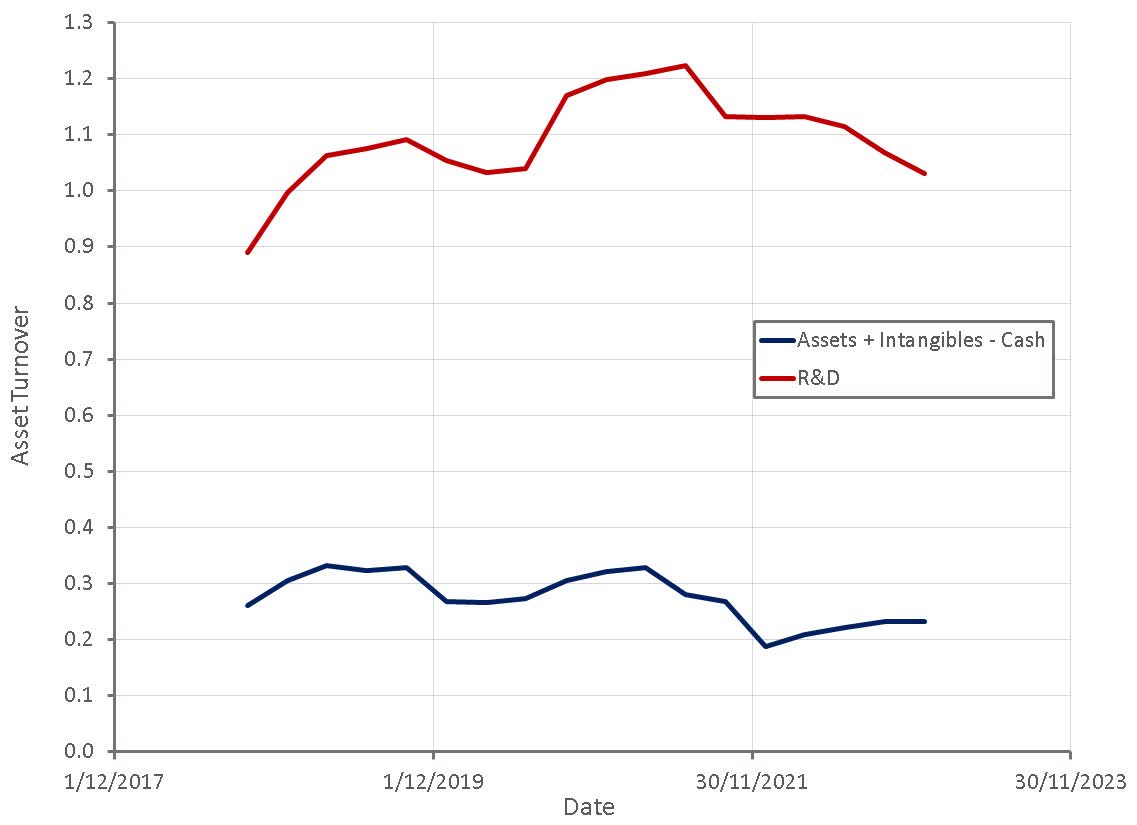

It was also suggested that Twist hides COGS as an R&D expense, with the report suggesting that Twist's gross profit margin is off by at least 50%. As a commodity DNA manufacturer the report suggests that Twist's R&D expenses should be low, ignoring the fact that the company is investing in drug development research, developing DNA data storage technology and continuing to develop new products within the Synbio and NGS verticals.

If this were the case, it would be clear that Twist's R&D expenses are not yielding any benefit to the company over time. Capitalizing R&D expenses and comparing them to revenue demonstrates that this is not the case. Despite investing heavily in products that are yet to realize meaningful revenue (drug development and data storage), revenue is growing in line with Twist's intangible R&D assets.

DNA data storage R&D spend was approximately 20% of total R&D spend in the first quarter of FY2023. Similarly, Biopharma R&D spend was approximately 25% of total R&D spend.

Figure 6: Twist Asset Turnover (source: Created by author using data from Twist Bioscience)

{kind=link}

The report also suggests that Twist's increase in gross profit margin is implausible, but this ignores the fact that Twist is realizing economies of scale and launching products in markets with better margin profiles.

The report points to the fact that Twist lacks GMP capabilities, which will severely restrict its growth, as 80% of order volumes are for GMP-standard product. Good Manufacturing Practice is a system for ensuring that products are consistently produced and controlled according to quality standards. It is designed to minimize the risks involved in any pharmaceutical production that cannot be eliminated through testing the final product. Twist plans on introducing GMP products in the near future.

Financial Analysis

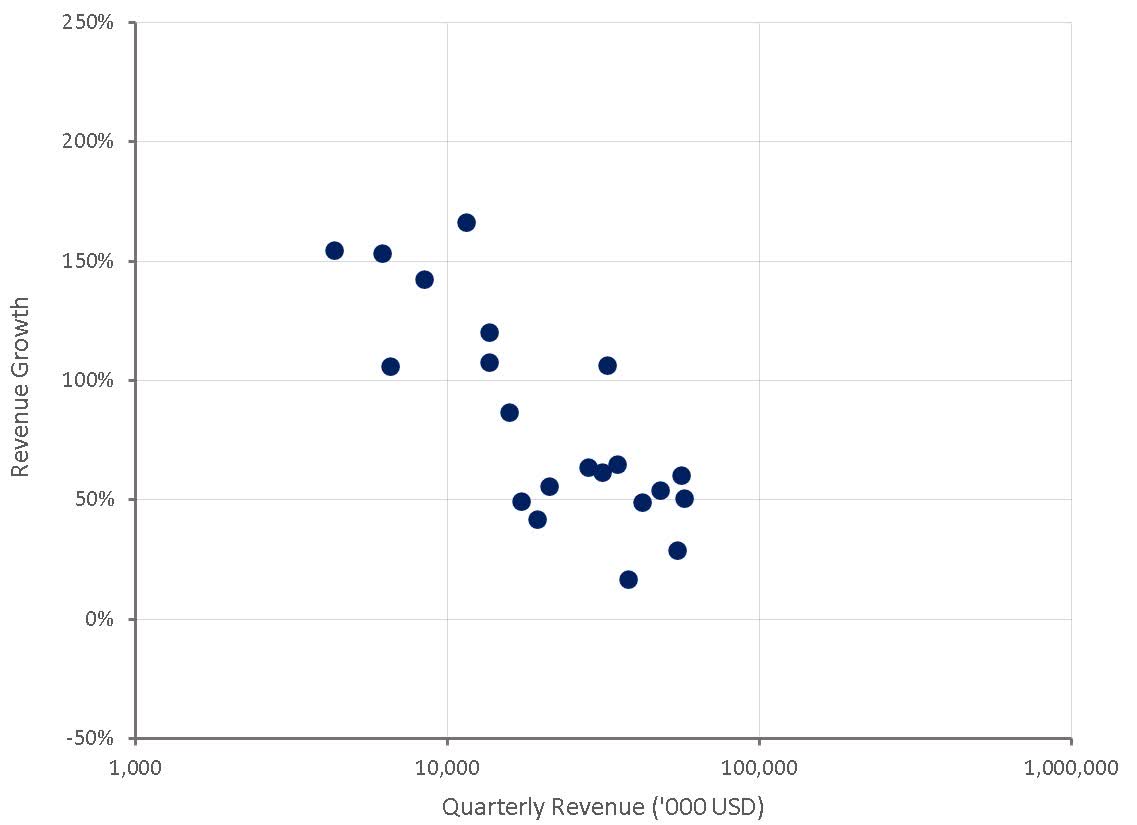

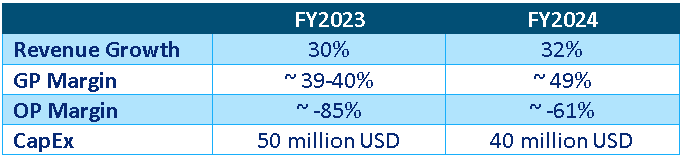

Twist is projecting FY2023 revenue in the 261-269 million USD range, indicating approximately 30% growth at the mid-point. This slowdown in growth, along with an expectation of a backloaded year have likely spooked investors somewhat. This is occurring against a backdrop of fairly weak growth in tech and biotech in general, and is not necessarily reflective of any Twist specific issues though. Given the company's ongoing losses, rapid growth is needed to reassure investors of Twist's future.

Figure 7: Twist Revenue Growth (source: Created by author using data from Twist Bioscience) Table 2: Twist Guidance (source: Created by author using data from Twist Bioscience)

{kind=link}

{kind=link}

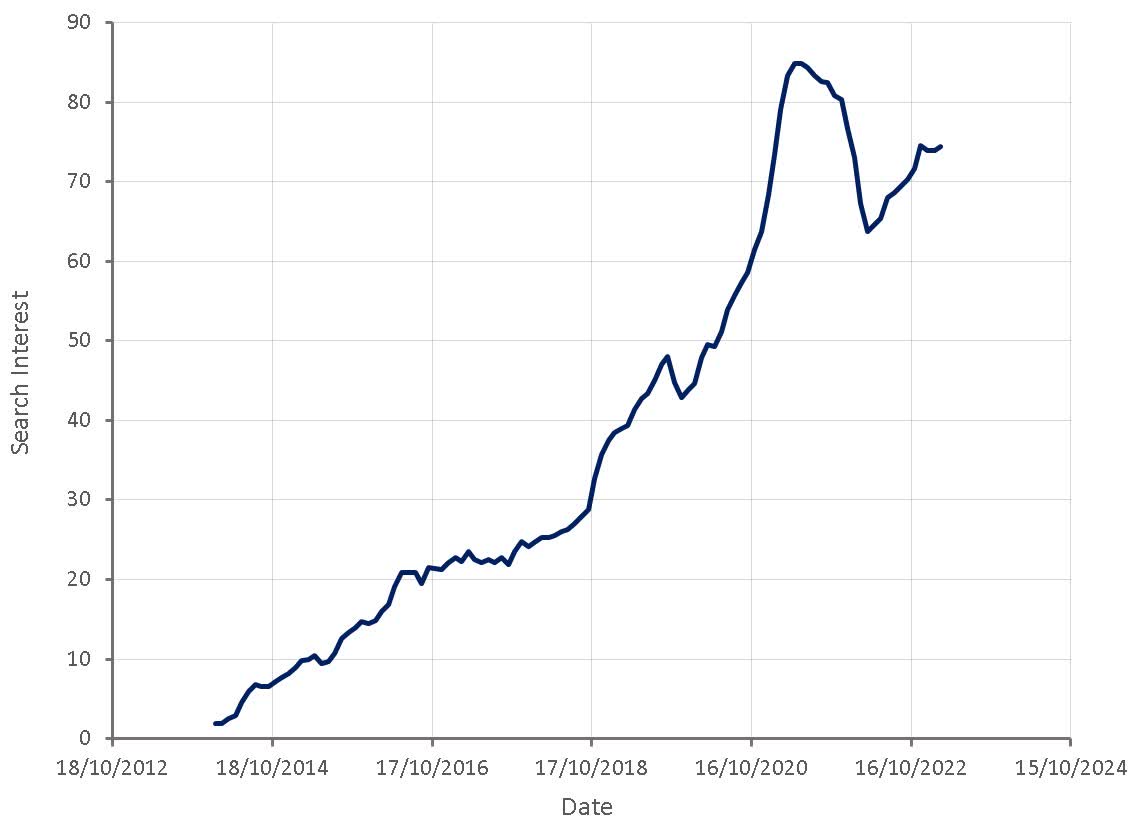

Search interest indicates growing interest in the company, which could be expected to translate into demand over time.

Figure 8: "Twist Bioscience" Search Interest (source: Created by author using data from Google Trends)

{kind=link}

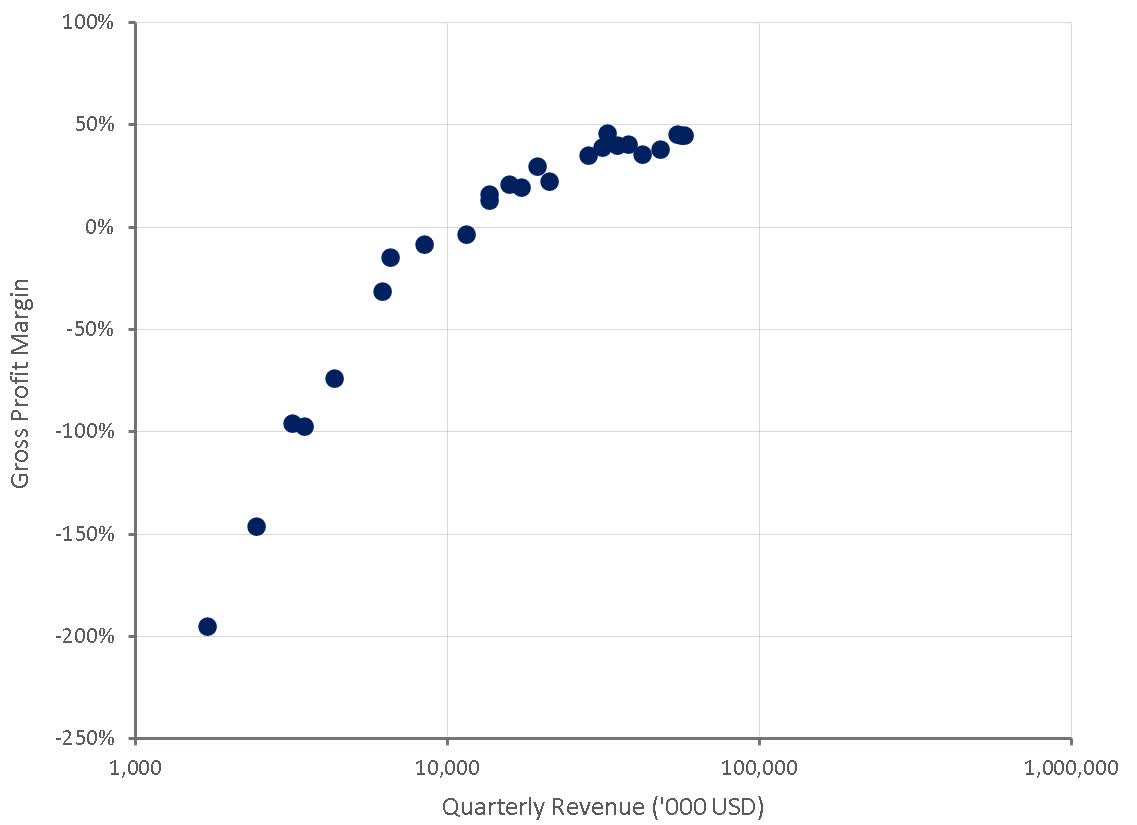

Twist still anticipates achieving gross profit margins in the 55-60% range in the long-term for the core business. Management has stated that the contribution margin for NGS is 80% and for Synbio 65-70%. As the business continues to scale, this should naturally lead to improving margins over time.

There is also the potential for an evolving product portfolio to lead to improved margins. The ASP for fast genes is expected to be higher, which should lead to better margins. The IgG product line is also another opportunity for Twist to improve their gross profit margins. This is a general feature of Twist's strategy, and the company expects to drive margins by moving up the value chain into areas like long genes, impossible genes, RNA, etc., over time.

Gross margins for the Biopharma business are around 60%. While the economics of the data storage business remain uncertain, Twist believes they could be compelling, with initial models indicating gross margins as high as 60-65%.

In the near-term, gross profit margins will be under pressure though, due to the opening and scale-up of the Portland facility. This is simply a function of the site temporarily operating sub-scale, causing a high burden from fixed costs, rather than any meaningful shift in Twist's production costs. Gross margins for the second quarter are expected to be approximately 30% , before rebounding as operations scale.

Figure 9: Twist Gross Profit Margins (source: Created by author using data from Twist Bioscience)

{kind=link}

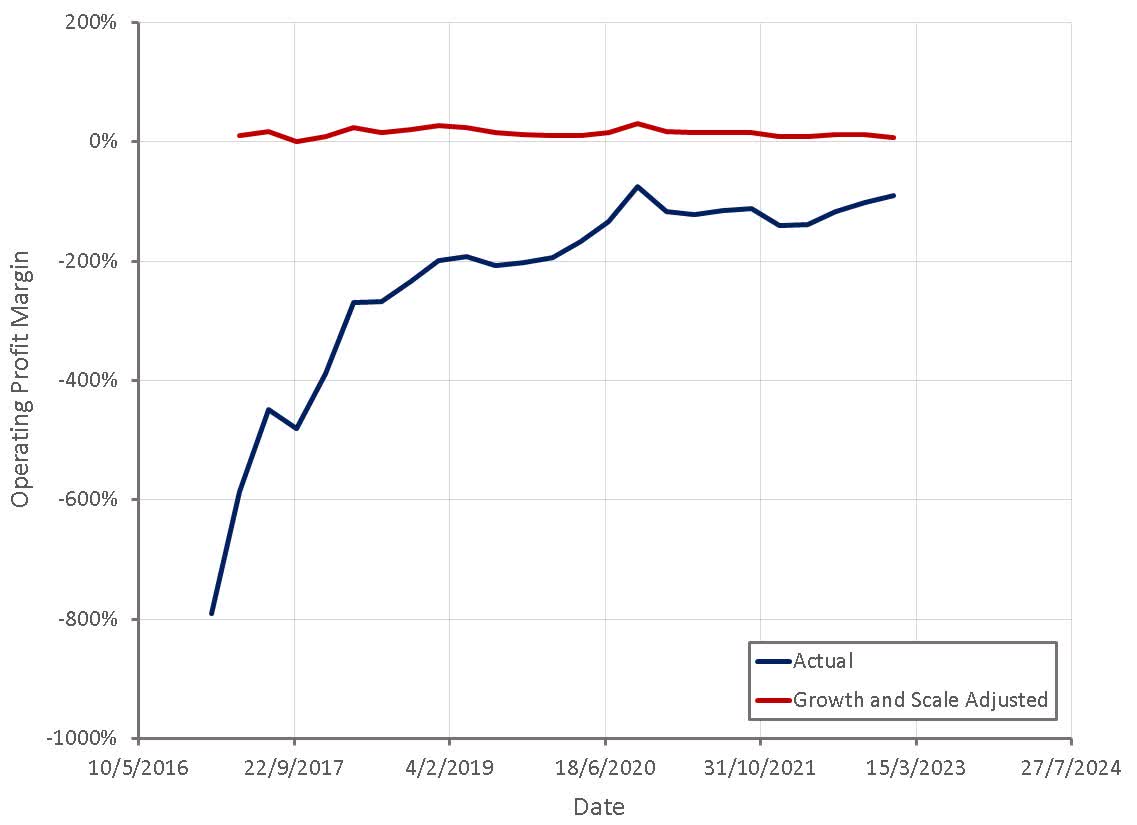

Twist expects their core business to achieve adjusted EBITDA breakeven at 300 million USD revenue. At that point Twist also expects to have options for data storage that could further mitigate spend. They are also targeting adjusted EBITDA breakeven at 80 million USD revenue for the Biopharma segment. Twist will likely never have a high margin business, but based on their current performance it seems reasonable to eventually expect operating profit margins around 15%.

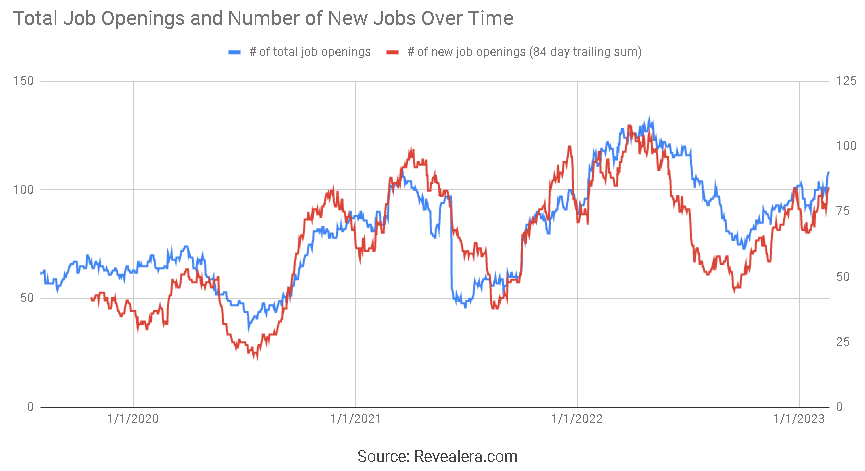

Figure 10: Twist Operating Profit Margins (source: Created by author using data from Twist Bioscience) Figure 11: Twist Job Openings (source: Revealera.com)

{kind=link}

{kind=link}

Valuation

Twist's current valuation is quite modest given the company's potential, and this appears to be the result of growing doubt about the business model. Twist is in a period of heavy investment, which is dragging on margins, and the business still needs to scale before profitability is achieved. This is being exacerbated by a weak macro environment.

Investors should keep in mind that Twist's data storage business is not yet generating revenue, and Twist stands to collect significant downstream value from Biopharma projects, which is also not reflected in the company's current financials.

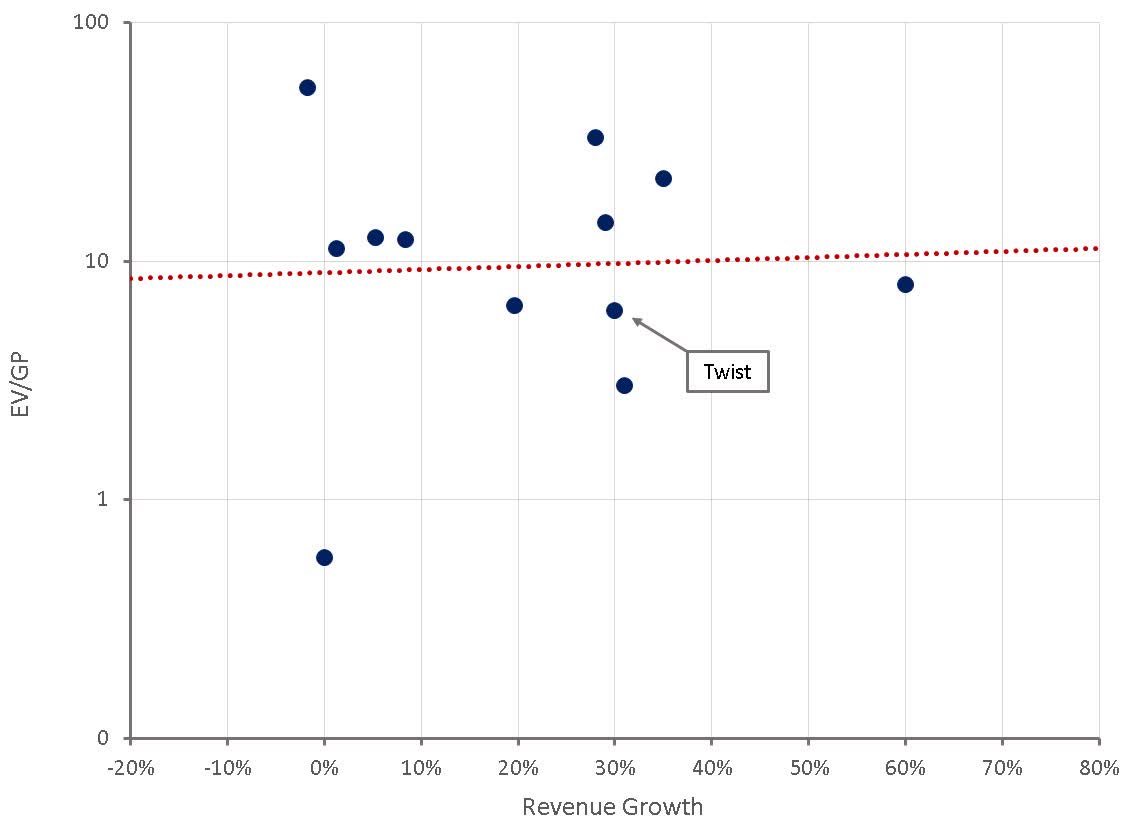

Figure 12: Twist Relative Valuation (source: Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Twist Bioscience: Biopharma And Data Storage Are Underappreciated