WMB - TYG: A Few Pluses But A Historical Underperformer

2023-07-17 07:11:34 ET

Summary

- Midstream MLPs have long been favorites of income investors due to their stable cash flows and very high yields.

- TYG invests in a portfolio of natural gas MLPs and renewable companies in an attempt to give investors exposure to the energy transition.

- The fund historically underperforms its benchmark indices by quite a lot, which is unfortunate.

- The fund yields 9.42% today and this appears to be sustainable.

- The fund trades at a very attractive discount to the net asset value.

For many years now, master limited partnerships have been some of the most popular investments available on the market for anyone that is seeking a high level of income from their portfolios. It is not difficult to see why as many of these companies, especially in the midstream segment, enjoy remarkably stable cash flows over time and pay out a substantial percentage of their cash flows to the shareholders. As the market does not assign particularly high multiples to these companies, the distributions represent a substantial percentage of the unit price (a high yield). We can see this quite clearly in the fact that the Alerian MLP Index ( AMLP ) yields 8.60% at the current price. That is obviously substantially higher than any other index in the market.

Unfortunately, there are a few problems with these companies. The most important for many people is that they cannot be easily included in tax-advantaged accounts, such as most retirement accounts. This is because of unrelated business taxable income, which can actually result in your retirement account being forced to pay taxes. In addition to this problem, it can be difficult to assemble a diversified portfolio of master limited partnerships unless you have access to a considerable amount of capital.

One easy way around both of these problems is to purchase shares of a closed-end fund that specializes in the sector. These funds are typically structured as corporations, which allows them to be included in a retirement account without any adverse tax consequences. These funds also provide easy access to a diversified portfolio that is managed by professionals, removing the large amounts of capital that an individual investor would need to assemble such a portfolio. Finally, these funds also have the ability to employ certain strategies that can boost their yields beyond that of the underlying assets. When we consider the high yields possessed by most master limited partnerships, this can result in these funds having remarkable yields.

In this article, we will discuss Tortoise Energy Infrastructure ( TYG ), which is one fund that can be used to invest in master limited partnerships and similar companies. This fund certainly proves the earlier statement about being able to provide a higher effective yield than the underlying assets since its 9.42% yield is quite a bit higher than the Alerian MLP Index. I have discussed this fund before, but a little while has passed since that time so naturally a few things have changed. This article will focus specifically on those changes as well as provide an updated analysis of the fund's financial condition. Therefore, let us investigate and see if this fund could be a worthy addition to a portfolio today.

About The Fund

According to the fund's webpage , Tortoise Energy Infrastructure has the objective of providing its investors with a high level of total return. This is not particularly surprising considering that this is an equity closed-end fund. As we can see quite clearly, the overwhelming majority of the fund is invested in common equity, although it does have a small amount of fixed-income exposure:

Morningstar

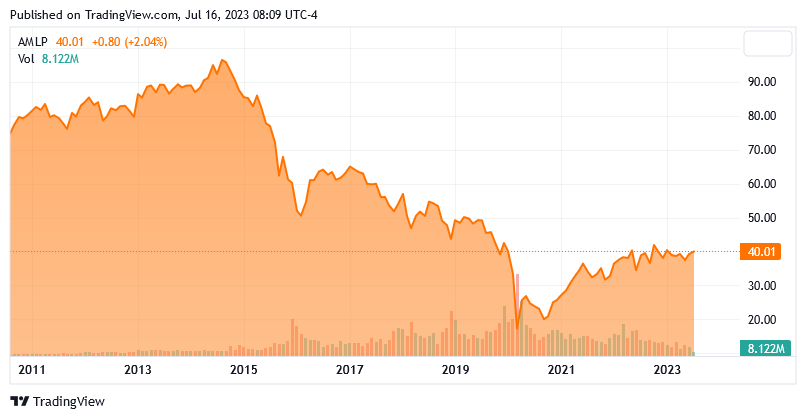

The reason why the fund's investment objective makes sense in this respect is that common equity is by its nature a total return vehicle. After all, investors typically purchase common equity in order to generate income through dividends and distributions paid by the issuing company. They also want to benefit from capital appreciation as the issuing company grows and prospers with the passage of time. As the fund is almost completely invested in these securities, it makes sense that this is the objective that it would be targeting. With that said, master limited partnerships and other energy infrastructure companies tend to deliver most of their investment returns in the form of distributions paid directly to the investors. This is quite obvious if we look at the Alerian MLP Index over the long term:

{kind=link}

This admittedly does not look good for the index at all, as two devastating losses in 2015 and 2020 actually caused its price action to be sharply negative. However, the total return of the portfolio has actually been positive over this time period. The Alerian MLP ETF has returned an average total return of 2.61% since inception, which is obviously not as good as several other things in the market but it is still far better than the chart above would illustrated. This is because the money that most master limited partnerships pay out is sufficient to offset any price declines over the long term.

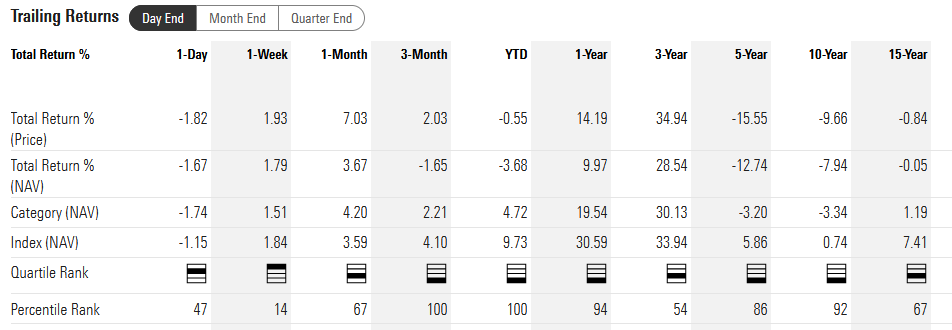

Tortoise Energy Infrastructure actually has unfortunately done somewhat worse. As we can clearly see here, the fund actually had a negative total return over the past fifteen years, which was far worse than the index:

{kind=link}

It did manage to beat the index a few times though, but most people looking at a fund like this are going to be interested in the long term. As we can clearly see, the fund disappoints as it lost to the index year-to-date and over the past year. Its performance relative to the index over the past ten years and fifteen years is even worse. An investor would have been much better off buying the index, although the Tortoise fund does have a higher yield right now so that might appeal to a few people.

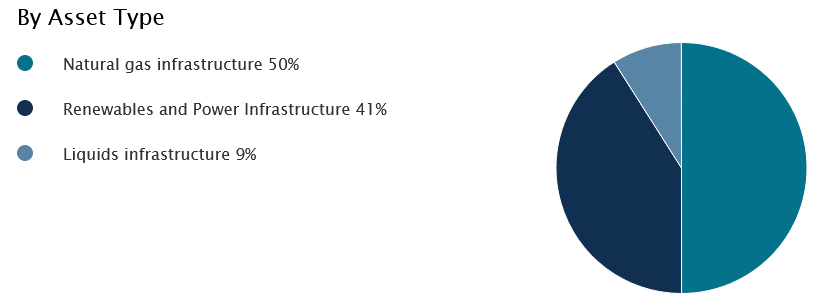

One important thing to note here is that the Alerian MLP Index is not a perfect comparison for Tortoise Energy Infrastructure. One big reason for this is that the closed-end fund includes renewable energy and other things that are going to have very different performance characteristics than fossil fuel-based energy companies. As we can see here, about half of the fund is invested in natural gas infrastructure and 41% is invested in renewables infrastructure:

{kind=link}

As some readers may recall, renewables performed very badly last year as the 2021 bubble in highly speculative companies that had limited economic prospects came to an end. That came on the heels of a devastating 2020 performance for fossil fuel-based master limited partnerships. The index actually delivered a 25.12% gain in 2022 as fossil fuel companies outperformed everything during that year. This fund would not have benefited as much from that as the losses from the bubble bursting offset some of the gains from the traditional energy side of the portfolio.

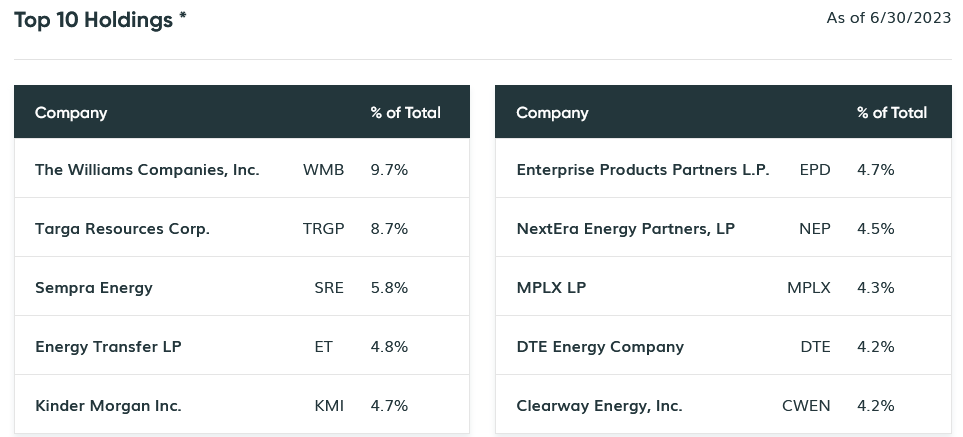

As my long-time readers are no doubt well aware, I have devoted a considerable amount of time and effort over the past few years to discussing various master limited partnerships and similar energy companies here at Energy Profits in Dividends and over at the main Seeking Alpha site. As such, the majority of the fund's largest holdings will probably be familiar to most readers. Here they are:

{kind=link}

I have published about nearly all of these companies over the years. In fact, Clearway Energy ( CWEN ) is the only company on this list that I have never discussed. Clearway Energy is an American developer of solar and wind projects that operates throughout the United States. NextEra Energy Partners ( NEP ) is a renewable energy yieldco that sells renewably-generated electricity under long-term power purchase agreements and pays out most of its cash flow to its shareholders. DTE Energy ( DTE ) is a regulated electric and natural gas utility that has garnered considerable praise among environmental activists by virtue of its green energy ambitions. Sempra ( SRE ) is another regulated utility that has considerable operations in California, and like all California utilities is devoting a considerable amount of effort to guiding its customers through the energy transition. The remainder of these companies are traditional fossil fuel midstream partnerships and corporations. For the most part, these are among the best midstream companies available in the market right now, so it is hard to complain about the firms that the fund's management has chosen to represent the sector. The Williams Companies ( WMB ) in particular is very well positioned to deliver strong forward growth due to the strong fundamentals for natural gas.

As I have mentioned in various previous articles on closed-end funds, I do not generally like to see any single position account for more than 5% of the fund's portfolio. This is because that is approximately the level at which the asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification but if the asset accounts for too much of the portfolio then it will not be completely eliminated. Thus, the concern is that some event may occur that causes the value of a given asset to decline when the rest of the market does not and if that asset accounts for too much of the portfolio then it may end up dragging the fund down with it. As we can clearly see above, there are three assets that individually account for more than 5% of the portfolio. As such, anyone that is considering purchasing the fund's shares should be willing to be exposed to the risks of these assets individually. This is still less concentration at the top than most energy infrastructure funds though, as many of the fund's peers have six or seven highly weighted assets. Thus, this one is a bit more diverse than many competing funds, which has a certain appeal.

There have been surprisingly few changes since the last time that we discussed this fund. In fact, the only notable change is that ONEOK ( OKE ) was removed and replaced by NextEra Energy Partners. This could be related to some of the troubles surrounding the merger between ONEOK and Magellan Midstream Partners. It is still uncertain whether or not that merger goes through, as the final vote is scheduled for sometime in the next few months. ONEOK has been one of the poorest-performing midstream companies year-to-date, but it is not atypical for a merger to cause the acquiring company's stock to weaken. The stock's disappointing performance could have been one of the factors that caused the company's removal from the fund's largest positions, especially as this underperformance undoubtedly caused its weighting to fall even in the absence of any trading activity on behalf of the fund's management.

The fact that so few positions have changed recently could lead one to believe that the fund has a fairly low annual turnover. This is, however, not the case as Tortoise Energy Infrastructure had an annual turnover of 73.84% in 2022. That is not out of the ordinary for an equity closed-end fund, but it is still higher than may be expected given the paucity of changes over the past month. The reason that this is important is that trading equities or other assets costs money, which is billed directly to the fund's shareholders. This creates a drag on the fund's performance and makes management's job more difficult. This is because the fund's management needs to generate a sufficiently high return to cover the excess costs and still deliver a competitive return to the shareholders. This is a difficult task that very few management teams are capable of achieving on a consistent basis. This typically results in an actively-managed fund underperforming its index benchmarks. As we have already seen, this one is no exception as it has consistently underperformed its own benchmark index in terms of total returns.

Leverage

As mentioned in the introduction, closed-end funds like Tortoise Energy Infrastructure have the ability to employ certain strategies that have the effect of boosting their yields beyond that of any of the underlying assets. One of the strategies that is used by this fund is leverage. In short, the fund is borrowing money and using that borrowed money to purchase common equities of midstream and renewable companies. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that this strategy is not as effective today with interest rates at 5% as it was eighteen months ago when rates were at 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. Thus, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of assets for that reason. Fortunately, this fund satisfies that requirement as its levered assets comprise 26.39% of the portfolio as of the time of writing. Thus, this fund appears to be striking a reasonable balance between risk and reward. We should not have to worry too much about the fund's leverage.

Distribution Analysis

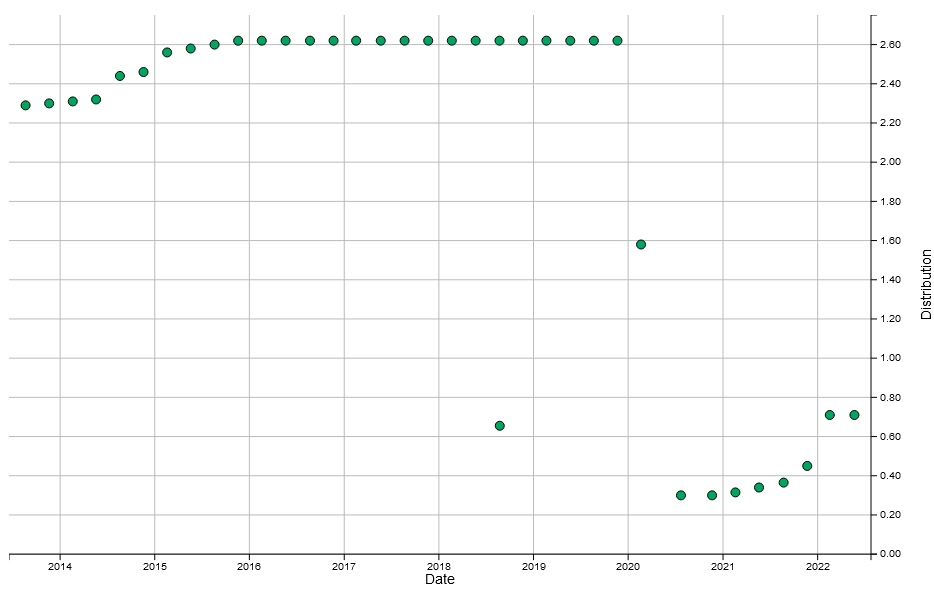

As mentioned earlier in this article, the primary objective of Tortoise Energy Infrastructure is to provide its shareholders with a high level of total return. However, the fund aims to deliver the majority of its total return in the form of direct payments to its investors. This makes sense as most midstream companies and master limited partnerships also deliver the majority of their total returns in the form of direct payments to the investors. The fund simply collects this income, applies a layer of leverage to boost it, and then pays out all of it plus any capital gains to the shareholders. As such, we can assume that the fund has a very high yield itself. This is certainly the case as it pays a quarterly distribution of $0.71 per share ($2.84 per share annually), which gives the fund a 9.42% yield at the current price. Unfortunately, the fund has not been particularly consistent in its distribution over time:

{kind=link}

As we can clearly see here, the fund cut its distribution substantially back in 2020 and has yet to return it to its previous level. However, the fund has been making worthy attempts to increase its distribution since the steep cut. It is not surprising that it had to cut in 2020 though as that was a very uncertain time for the industry. As I pointed out in numerous previous articles, there were numerous midstream companies that cut their distributions during that year in order to strengthen their balance sheets. This was mostly due to the uncertainty about the future of the industry and the market's general unwillingness to provide financing. For the most part, though, their cash flows remained relatively stable. The fund still had to cut its distributions in order to preserve its own capital, however.

However, the fund's past is not necessarily the most important thing for anyone buying today. This is because a new investor will receive the current distribution at the current yield and is not affected by the fund's actions in the past. As such, the most important thing today is the fund's ability to sustain its current distribution going forward. Let us investigate that.

Unfortunately, we do not have an especially recent document that we can consult for this purpose. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on November 30, 2022. As such, this report will not include any information about the fund's performance over the past eight months. This is unfortunate as a lot has happened over that period, including a decline in the price of natural gas. In addition, midstream master limited partnerships are generally up year-to-date so the fund may have had the potential to earn some gains that will not be reflected in this report. During the full-year period, Tortoise Energy Infrastructure received $26,970,895 in dividends and distributions along with $970,150 in interest from the investments in its portfolio. However, some of this money came from master limited partnerships and so is not considered to be income for tax purposes. The fund thus reported a total investment income of $13,122,158 during the period. It paid its expenses out of this amount, which left it with $6,557,431 available for shareholders. As might be expected, this was nowhere close to enough to cover the $33,451,804 that the fund actually paid out in distributions during the period. At first glance, this could be concerning as the fund's net investment income was not nearly enough to cover its distributions.

However, the fund does have other methods through which it can acquire the money that it needs to cover its distributions. For example, it might have sufficient capital gains that can be sent out to accomplish this task. That was, fortunately, the case here. During the full-year period, the fund reported net realized gains of $112,955,888, which was partially offset by $11,085,418 net unrealized losses. However, the fund's assets still increased by $46,574,244 after accounting for all inflows and outflows during the year, despite the fact that it bought back $23,235,549 worth of its own stock and paid its distributions. The fund thus clearly appears like it can cover its distribution for quite some time, especially if its performance so far this year was at all comparable to what it had last year. Overall, there is probably nothing for us to worry about for the time being here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like Tortoise Energy Infrastructure, the usual way to value it is by looking at its net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. That is fortunately the case with this fund today. As of July 13, 2023, Tortoise Energy Infrastructure had a net asset value of $37.02 per share but the shares only trade for $30.15 each. This gives the shares a whopping 18.56% discount to the net asset value at the current price. This is a very large discount that is in line with the 18.81% discount that the shares have averaged over the past month.

Conclusion

In conclusion, midstream master limited partnerships have long been a favorite investment of anyone seeking income. Tortoise Energy Infrastructure offers a way to add these companies to a retirement account and earn a market-beating return at the same time. Unfortunately, this fund has a history of underperformance as it consistently underperforms its benchmark indices. It does offer some exposure to the renewable sector though, which is a very real plus. The 9.42% current yield appears sustainable and the valuation is going to be difficult to beat. My biggest problem here is that the fund's history of underperformance greatly weakens its appeal for long-term investors.

For further details see:

TYG: A Few Pluses, But A Historical Underperformer