ZION - U.S. Bancorp Remains A Good Income Play

2024-01-09 11:58:02 ET

Summary

- U.S. Bancorp offers a sustainable dividend yield supported by strong fundamentals and a conservative payout ratio.

- The bank's recent acquisition of Union Bank is expected to boost earnings and increase its customer base.

- Despite challenges in the banking sector, U.S. Bancorp has maintained a stable deposit base and demonstrated resilience in its operating performance.

U.S. Bancorp ( USB ) offers an interesting dividend yield that seems to be sustainable over the long term, being supported by the bank’s strong fundamentals and conservative dividend payout ratio.

As I stated back in 2021 , U.S. Bancorp is a quality company within the banking sector and offers good income perspectives for long-term investors, due to a sustainable dividend over the long term.

However, its share price performance has been mixed since then, as the benefit of higher interest rates was to a large extent offset by the banking turmoil regarding regional banks in the first half of 2023, leading a lower share price now than about three years ago.

In this article, I review U.S. Bancorp’s most recent financial performance and update its investment case, to see if it remains an interesting income option in the banking sector or not.

Financial Overview

While U.S. Bancorp is not among the largest U.S. banks measured by total assets, like JPMorgan ( JPM ) or Bank of America ( BAC ) that have total assets in excess of $3 trillion, U.S. Bancorp is still the fifth-largest commercial bank in the U.S., measured by total assets of $674 billion in 2022.

The bank has grown historically both by organic efforts and through acquisitions, a strategy that has not changed recently. Its business profile is more geared to retail and commercial banking, even though it has a good business diversification across retail, commercial, payment services, corporate and wealth management operations.

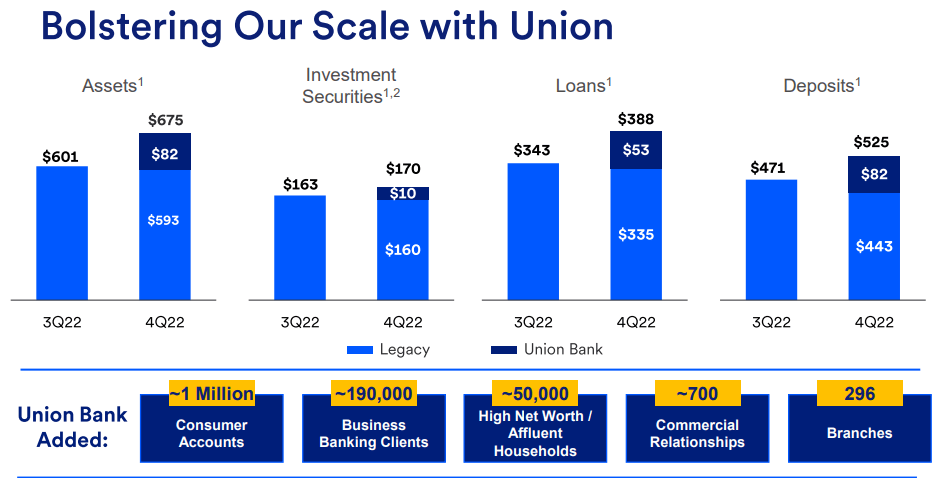

Since my previous coverage on U.S. Bancorp, the bank has completed a sizable acquisition, purchasing Union Bank for some $7.5 billion in December of 2022. This bank was part of the Japanese banking group Mitsubishi UFJ Financial Group ( MUFG ), increasing U.S. Bancorp’s customer base by about one million retail customers and 190,000 small business customers. It also enhanced the bank’s position in the West Coast, increasing its deposit and loan market share in California in a significant way. Union Bank had some $58 billion in loans and about $90 billion in deposits, being a good fit for U.S. Bancorp’s group operating profile in the retail and commercial banking segments.

While this acquisition was not cheap, U.S. Bancorp expects to reach cost synergies of about $900 million, and increase its earnings per share by double-digits when all cost synergies are extracted. The internal rate of return from this acquisition is expected to be around 20%, excluding potential revenue synergies, thus the bank seems to be have some room to achieve an even higher return from this acquisition if it can cross-sell more products to Union Bank’s customer base.

{kind=link}

Union acquisition ( U.S. Bancorp )

Beyond this acquisition that boosted its balance sheet and is expected to be positive for its earnings in the first year, U.S. Bancorp’s financial performance has also been supported by higher interest rates and good levels of credit quality.

Nevertheless, its business is not among the most geared to interest rates in the banking sector, due to its diversified business mix, while other banks have higher sensitivity to rates, such as Comerica ( CMA ) or Zions ( ZION ). Indeed, U.S. Bancorp’s net interest income ((NII)) represented less than 60% of its total revenues in 2021, compared to about 70% for Comerica and some 85% for Zions.

This means that during a period of rising interest rates, like the one experienced from the beginning of 2022 to the summer of 2023, U.S. Bancorp’s revenues were boosted by rising rates, but not to the same extent of some of its peers.

Despite that, U.S. Bancorp also benefited from higher interest rates, given that its NII increased to $14.7 billion in 2022, up by 18% YoY. On the other hand, noninterest revenue declined to less than $9.5 billion (-7.5% YoY), leading to overall revenues of $24.3 billion, up by just 6.5% YoY. While the bank was able to report positive revenue growth last year, this clearly shows that its business is not much geared to interest rates, having a more stable revenue profile over the economic cycle than some of its peers.

Regarding credit quality, U.S. Bancorp maintained relatively low levels of provisions for loan losses in the year, but booked some provisions in the last quarter of the year due to the acquisition of Union Bank. This can be seen as a conservative approach by its management, to better align the combined bank credit quality, having a one-off negative effect of $791 million, before tax, in Q4 2022.

Its net income was $5.8 billion, down by 27% YoY, due to acquisition costs and much higher provisions for credit losses, while in 2021 the bank had reverted provisions made in 2020 due to the pandemic. Despite reporting lower earnings in 2022, U.S. Bancorp’s return on equity ((ROE)) ratio, a key measure of profitability in the banking sector, was 12.6%, which is still a very good level of profitability.

During the first nine months of 2023 , the banking sector suffered from the turmoil in the regional segment, following the collapse of SVB Financial Group ( SIVBQ ), which also led to trouble at Signature Bank and First Republic Bank.

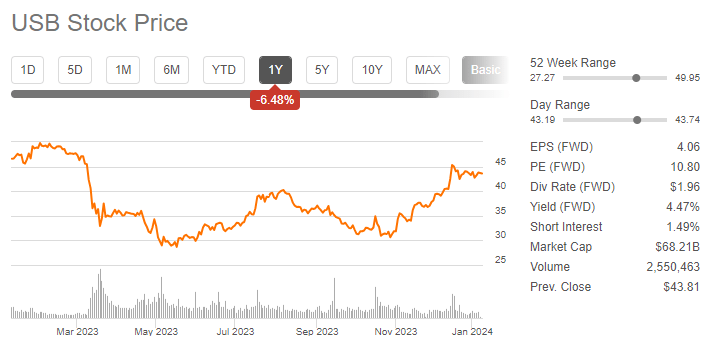

Not surprisingly, U.S. Bancorp was also affected by negative investor sentiment towards smaller and medium-sized banks, pushing its share price down over the past year.

{kind=link}

Share price (Seeking Alpha)

Despite this backdrop, the bank’s operating performance has remained resilient, showing that it has strong fundamentals and customers continue to trust its brand.

This can be seen by its total deposits, which declined a little bit in Q1 2023, to $505 billion (-3.7% compared to the end of 2022), but recovered to $518 billion by the end of September. This was a positive outcome during a tough period for U.S. regional banks, but U.S. Bancorp was able to retain its deposit base, which is key for a stable and sustainable business model in the banking industry.

Moreover, considering that its loan book amounted to $375 billion at the end of Q3 2023, U.S. Bancorp’s balance sheet leverage is low, measured by a loans-to-deposits ratio of only 72%. Usually, a ratio between 90-95% is good, while a ratio below that shows a conservative position, thus U.S. Bancorp low leverage was also likely a reason why it did not have much deposits outflows during 2023.

Regarding its operating momentum, U.S. Bancorp’s revenues amounted to more than $7 billion in Q3, up by more than 11% YoY, supported by higher interest rates and its acquisition of Union Bank. Despite higher revenues, U.S. Bancorp’s earnings were impacted by integration costs of $1.1 billion during the first nine months of 2023 (total integration costs expected to be about $1.4 billion), and higher provisions for loan losses.

In the last quarter, its provisions amounted to $515 million, up by 42% YoY, reflecting some deterioration in credit quality across its loan book, plus some issues in the commercial real estate ((CRE)) sector. U.S. Bancorp has some exposure to this sector, amounting to $54 billion at the end of last quarter, or 14% of its total loan book. This can be an area where the bank is likely to suffer higher losses in the short term, even though its exposure to office (the category that is riskier right now) is only 13% of U.S. Bancorp’s total exposure to CRE, thus it doesn’t seem to be big enough to make it a major issue in the coming quarters.

CRE exposure ( U.S. Bancorp )

Due to the combination of higher costs and provisions for loan losses, U.S. Bancorp’s net income was $1.5 billion in Q3, down by 5.9% YoY, and its ROE was 11.9%.

Going forward, U.S. Bancorp will benefit from the full integration of Union Bank and will not report much more integration costs in the coming quarters, which will support higher earnings in 2024, but on the other hand provisions are expected to increase and interest rates may start to come down in the coming months, which can represent important headwinds for earnings growth.

Despite that, according to analysts’ estimates , U.S. Bancorp’s net income is expected to increase to $6.3 billion in 2024, compared to $5.5 billion in 2023, showing that the full benefit of its Union Bank acquisition is yet to be recognized in the bank’s bottom line.

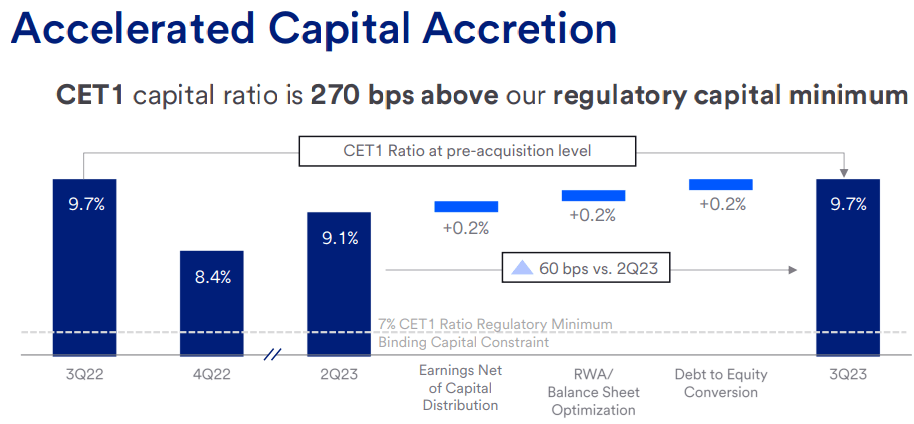

Regarding its capitalization, its CET1 capital ratio suffered a significant hit from the Union Bank acquisition, but over the past few quarters the bank has increased its capital ratio to 9.7% at the end of last September. This is not among the best capitalized banks in the U.S, but it’s an acceptable ratio and is 270 basis points above regulatory requirements, leaving some room for an attractive shareholder remuneration policy.

{kind=link}

Capital ( U.S. Bancorp )

Indeed, U.S. Bancorp has a good dividend history , delivering a growing dividend over the past few years. Its current quarterly dividend is $0.49 per share, or $1.96 per share annualized, which at its current share price leads to a dividend yield of about 4.5%. This is slightly above the average of its peers, showing that U.S. Bancorp offers an interesting yield.

Moreover, its dividend is well covered by earnings, given that its dividend payout ratio based on 2023 earnings is about 56% and is expected to drop to less than 50% in 2024. This is a conservative dividend payout ratio, thus U.S. Bancorp seems likely to maintain a growing dividend trajectory in the coming years, plus it’s also likely to perform share buybacks to return more capital to shareholders.

Conclusion

U.S. Bancorp has a sound business model and its recent acquisition of Union Bank seems to be a good move to improve the bank’s profitability level. Due to its quality profile, it usually trades at a premium valuation to its peers, and currently is trading at 1.5x book value compared to 1.22x book value for the US banking sector.

Additionally, it’s trading at a similar valuation compared to its own historical average over the past five years, thus U.S. Bancorp seems to be fairly valued right now and its investment case remains highly dependent on the dividend, being the main reason to currently buy its shares.

For further details see:

U.S. Bancorp Remains A Good Income Play