SLCA - U.S. Silica Holdings: Hard To Pass Up On This Solid Company

2023-09-29 04:46:57 ET

Summary

- U.S. Silica Holdings Inc. is a company operating in the energy sector, focusing on commercial silica production in the U.S.

- The company has shown improvement in its business model and stronger margins, with expected growth in the silica market.

- Risks include a potential threat to its primary business segment and concerns about its debt, but the company has made progress in paying down debt and improving its financial position.

U.S. Silica Holdings Inc (SLCA) is operating in the energy sector where it mostly focuses on making and selling commercial silica in the U.S. The company has a very rich history that dates back to 1894. The last couple of years have seen a pretty steady climb upwards for the share price, after reaching a bottom back in March of 2020.

The last report for the company showcased its ability to keep improving its business model and deliver stronger margins as demand increased. The industry isn't perhaps prone to any massive disruptions, but some growth is expected for the silica market, averaging a CAGR of 6.4% between now and 2031. These growth prospects are adequate in my opinion to justify a buy right now for the company, which is also trading at a significant discount to the rest of the sector, offering a nearly 40% lower valuation based on forward valuations. I think that paired with the ongoing efforts to put the company in a better financial position is enough to make for a buy case currently.

Operational Overview

Looking at the most recent report from the company, I think it goes to show the strength of the business model and its ability to perform very well despite challenging market conditions.

Quarter Results (Investor Presentation)

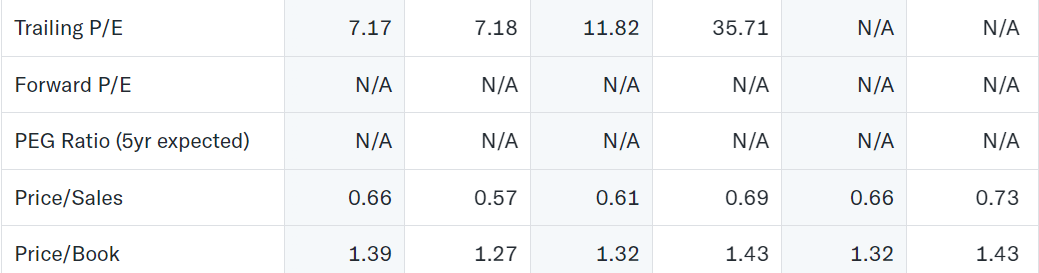

With improvements in the operating cash flows, SLCA now has a better chance to stop diluting shares and instead focus on providing as many benefits to shareholders as possible in my opinion. What a key focus continues to be for SLCA though is further deleveraging, which should let them trade at a higher p/b in my opinion as the risks are lower. The p/b right now is around 1.27, and I think something more in line with the sector could be suitable, which would be 1.72. This indicates a decent upside potential and something that could be realized if more and more debt repayments continue to happen.

Risks

A substantial deceleration in the homebuilding sector has the potential to pose a threat to SLCA's primary business segment: roofing tile coating, also known as its Industrial and specialty Products business. However, it's important to note that this concern is relatively remote at present due to several mitigating factors.

SLCA is reaping the rewards of two significant trends in the industry: the increased completion intensity, measured by the amount of sand used per foot, and the growing inclination towards drilling longer wells. Discussions surrounding the development of 15,000-foot wells have become increasingly frequent in industry conversations. When combined with the current practice of injecting 3,000 pounds of sand per foot, this translates to an additional 15 million pounds of sand per well.

Debt Levels (Seeking Alpha)

Besides this hoover, the debt does remain a concern in my opinion as it is still far above the current cash position at $870 million in total. It should be said though that SLCA has made strong progress in paying this down to reach a better and more sound financial position to work from. The benefit of the added debt seems to have been the possibility of investing in stronger growth projects and delivering a consistent positive net income for investors. The last two years have shown strong progress on that front and just the last quarter showcased a 102% YoY increase to the bottom line. If the market conditions worsen and demand softens for SLCA though I can see them facing difficulties in spying down the debt, which may result in a lower multiple and a drop in the share price.

Company Financials

Managing the financials of the company in the best way possible is an obvious priority for a lot of companies and what SLCA has going for it is the improvement and rescheduling of their debts. The company managed to postpone the repayment of $950 million of debts to 2030 rather than 2025. This significantly lowered the risk that share dilution will occur in the next few years. Instead, the company now is in a better financial position which is less stressful.

Balance Sheet (Earnings Report)

What SLCA has done very well though is to still pay down the debts and maintain a better and better position year-over-year. In just the last 12 months the company has paid down nearly $200 million, and the long-term debts now sit at $871 million in total. The cash position does in my opinion also remain in a good spot at $186 million. Going into the coming quarters I think the debts will be further reduced, but it seems to come somewhat from share dilution as it has been rising steadily in the last few years. I would like to see a stop to that and for SLCA to instead pay down debts using FCF and leverage their asset base into expanding those FCF. Since the debts have been rescheduled further out, I think the company is in a position where this shift can occur without risking anything significant.

Last Pointers

Right now I think investors are getting a very good deal with SLCA. The earnings multiple is nearly 40% below the sector, a discount that I think comes from the fact that previously the company has had trouble generating constant net incomes, but it seems that is changing right now. The last report showcased a triple-digit growth to the bottom on a YoY comparison.

{kind=link}

In terms of valuation, I think a P/E around 9 - 10 is applicable and that leaves a double-digit immediate upside potential right now and is much of the reason for my buy rating. Looking at a similar company or peer we have Select Water Solutions Inc (WTTR) which is trading slightly higher than SLCA currently at a P/E of nearly 9, but with worse margins than SLCA. Just based on this I think the market is discrediting some of the potentials and if WTTR can get a higher price whilst having worse margins I think investors are certainly not overpaying for SLCA right now. This all leads me of course to be rating the business a buy today.

For further details see:

U.S. Silica Holdings: Hard To Pass Up On This Solid Company