SLCA - U.S. Silica Holdings: Higher-Margin Products Imply Undervaluation

2023-09-07 02:16:49 ET

Summary

- U.S. Silica Holdings is a manufacturer of silica-based performance material products primarily serving the oil and gas industry.

- Management expects to increase its presence in the markets with the development of new products, and effectively reposition the facilities owned by SLCA.

- Analysts expect positive free cash flow in 2024 and 2025, and further deleveraging could lead to better stock valuations.

U.S. Silica Holdings ( SLCA ) recently reported an impressive reduction in the net leverage, which, I believe, will most likely have a beneficial impact on the EV/EBITDA and EV/FCF multiple. In my view, further greater sales of higher-margin products mainly in the ISP business segment, greater productive capacity, and greater diversification of its reserve sources could lead to FCF margin improvements. There are obvious risks from concentration of clients and problems in the largest facilities owned by SLCA, however my forecasts implied a fair price significantly higher than the current stock price.

U.S. Silica Holdings

U.S. Silica Holdings is a manufacturer of silica-based performance material products primarily serving the oil and gas industry. In addition, the company operates in the market for the production of mineral materials through EP Minerals, a subsidiary of the company.

By the year 2022, Silica Holdings had 27 active mining projects and two other projects in exploration status, all of them within the United States. This company has more than 120 years of activity, which has led it to knowledge about reducing general costs and optimizing productivity, in addition to historical recognition and sustained relationships with some clients.

Operations of the company are divided into two segments, oil and gas and industrial applications. This business model allows the complementarity of production and final markets.

Among its clients, the majority operates in the oil and gas market, representing 63%, 56%, and 47% of total sales in the last three years respectively. The trend, as we see, is a growth in relationships with this category of customers, which changes the historical trend in relation to the company's clients, which were concentrated in certain areas of the construction industry and the manufacture of chemical products.

Analysts Are Expecting Positive Free Cash Flow In 2024 And 2025

I believe that it is worth mentioning the expectations of other financial analysts. They expect beneficial financial figures in 2023, but a decline in sales in 2024 and 2025. The operating margin is expected to remain relatively stable in 2023, 2024, and 2025, however net sales may decline in 2024 and 2025. More specifically, forecasters expect 2025 net sales to be close to $1.535 billion, EBIT of $255 million, net income close to $125 million, and free cash flow about $226 million.

Source: Marketscreener

With that about the net sales, it appears favorable that professional forecasters expect FCF growth in 2026 and double digit FCF/Sales in 2021, 2022, and 2023. I did take into account these figures in my DCF model.

Source: Marketscreener

Balance Sheet

As of June 30, 2023, Silica reported cash and cash equivalents worth $186 million, with accounts receivable of $194 million and inventories close to $161 million. Total current assets are equal to $557 million. The current ratio stands at more than 2x, so I believe that there are no liquidity problems right now.

The largest asset in the balance sheet is property, plant, and mine development, which is worth $1.148 billion, and did not increase as compared to the balance sheet reported in 2022. Additionally, the company also reported goodwill worth $185 million, intangible assets of about $136 million, and total assets worth $2.081 billion. The asset/liability ratio is larger than 1x, so I believe that the balance sheet stands in a solid position.

Source: 10-Q

I am not concerned about the total amount of debt, and it is worth noting that long-term debt, pension liabilities, and other contractual obligations declined recently. The largest liabilities include accounts payable and accrued expenses worth $156 million, long-term debt worth $871 million, liability for pension and other post-retirement benefits worth $28 million, and total liabilities of about $1.287 billion.

Source: 10-Q

First FCF Catalyst: Lower Cost Structure Driven By Capacity Increases

Much of the successful development of this company corresponds to the low cost structure that it has managed to establish throughout its operational history, together with the great productive capacity and great diversification of its reserve sources. Added to these factors are the transportation capacity and the historical relationship with its customers that positions it as a benchmark within this industry. With this level of know-how, I believe that we can expect further FCF growth driven by lower operating costs like we saw in the last five years.

Source: Ycharts

Silica Appears To Be In A Period Of Transformation, Which May Lead To Optimization Of Supply Chain Connections

Net sales growth during 2023 fell by considerable values ?compared to the same period of the previous year. To adapt to the new conditions, the company appears to be making some changes.

Management expects to increase the presence in the markets with the development of new products, and effectively reposition the facilities owned by the company to approach the needs of its customers. Additionally, I would be expecting greater sales of higher-margin products mainly in the ISP business segment. Finally, I would also expect further optimization of supply chain networks and improvement of logistics margins, specifically in Greenfield and Brownfield. I believe that these measures will most likely lead to FCF growth in the coming years.

Source: Presentation To Investors

Further Deleveraging May Lead To Better Stock Valuations

I believe that the company has made significant improvements with regards to its net debt/adjusted EBITDA ratio. In the last presentation, Silica reported a ratio of close to 1.5x, which is significantly lower than what was reported in 2021. In my view, further reduction in debt levels will most likely lead to better EV/FCF valuations and more interest from investors.

Source: Presentation To Investors

DCF Model

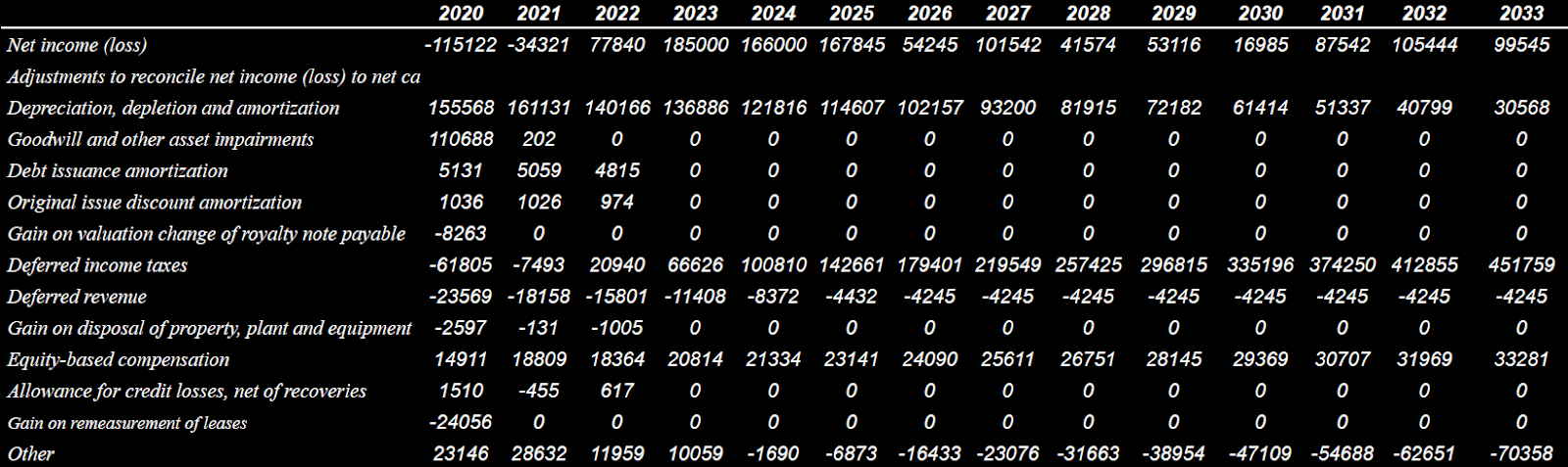

My forecasts include 2033 net income worth $99 million with the following adjustments to reconcile net income to net cash provided by operating activities. 2033 depreciation, depletion, and amortization could be worth $30 million, with 2033 deferred income taxes of $451 million, deferred revenue of -$5 million, and an equity-based compensation of close to $33 million.

{kind=link}

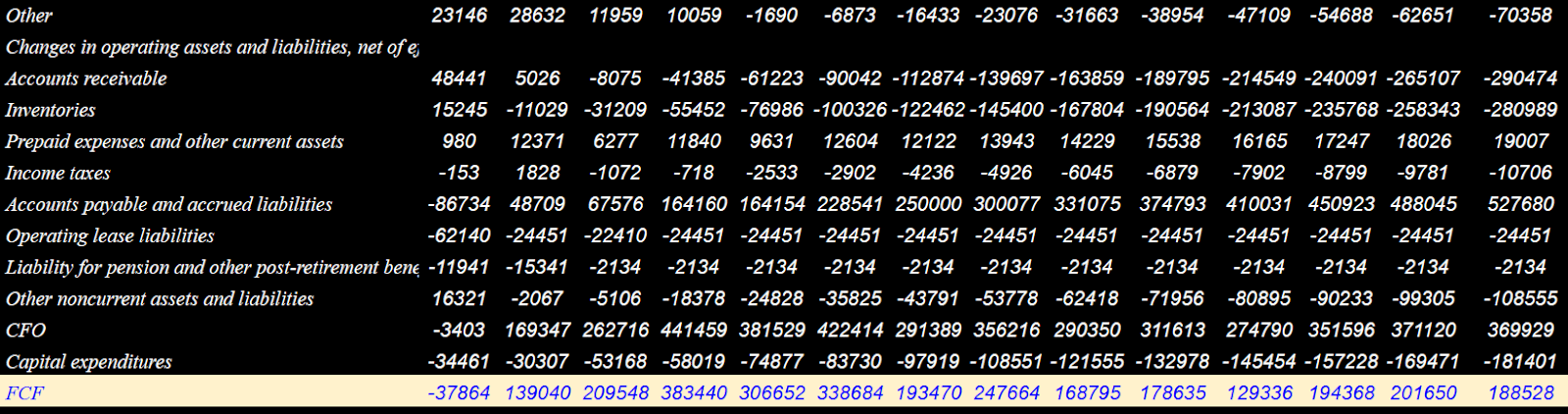

Changes in operating assets and liabilities would include changes in accounts receivable close to -$291 million, changes in inventories of close to -$281 million, and prepaid expenses and other current assets worth $19 million.

Additionally, taking into account changes in accounts payable and accrued liabilities worth $527 million and operating lease liabilities of -$25 million, CFO would stand at about $369 million. Finally, if we also include 2033 capital expenditures of close to -$182 million, 2033 FCF would be close to $189 million. In the past, the company reported FCF close to $222 million, so I believe that my figures are conservative.

Source: Ycharts

{kind=link}

It is also worth noting that I did not include, in my cash flow projections, extraordinary events, or items like changes in goodwill and other asset impairments, debt issuance amortization, original issue discount amortization, or gain on valuation change of royalty note payable.

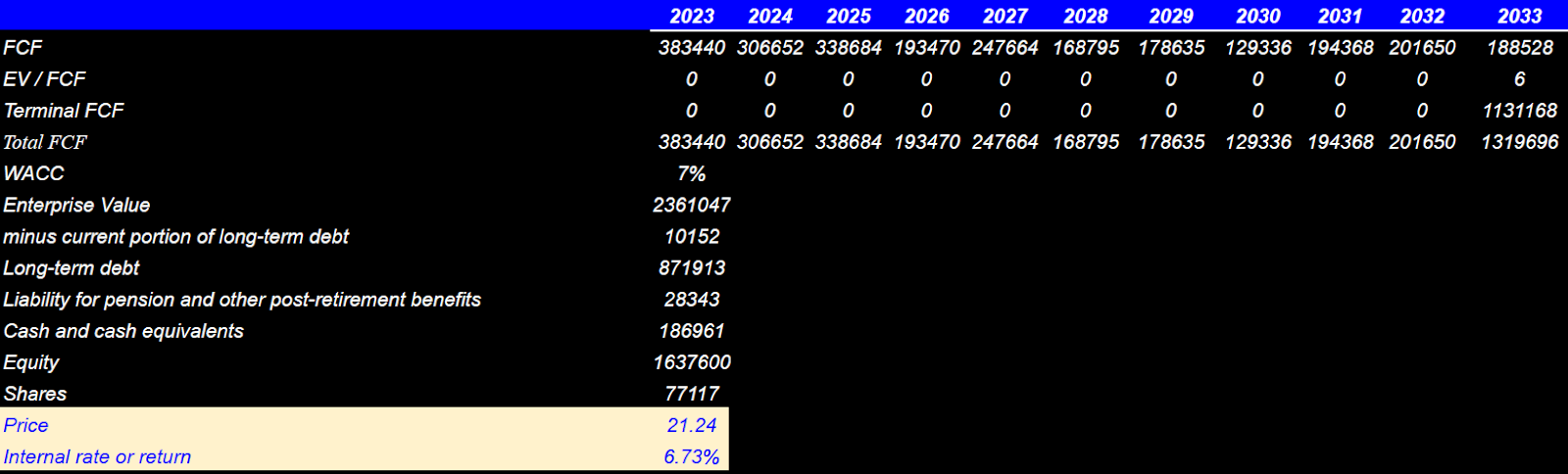

Hence, my forecasts would include 2033 FCF of $189 million, a terminal EV/ FCF of 6x, and a WACC close to 7%, which implied an enterprise value of $2.361 billion. Considering the current EV/FCF multiple and previous multiples, I believe that my terminal EV/FCF is conservative.

Source: Ycharts

Subtracting current portion of long-term debt of about $10 million, long-term debt worth $871 million, and liability for pension and other post-retirement benefits of $28 million, and adding cash and cash equivalents worth $186 million, the implied equity would be $1.637 billion, and the forecasted fair price would be $21 per share, with a forecasted internal rate or return of about 6.73%.

{kind=link}

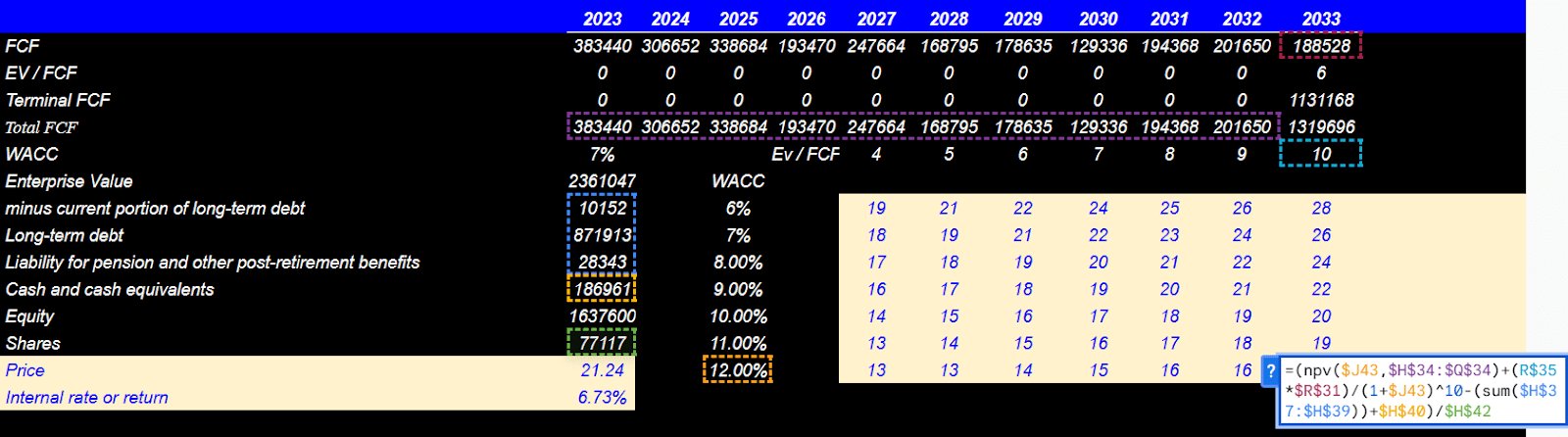

Other financial analysts may come with very different financial models, including different EV/FCF multiples and different cost of capital. With this in mind, I ran a small sensitivity analysis to understand whether the fair price would change a lot depending on changes in the WACC or the EV/FCF. With a WACC ranging from 6% to 12% and EV/FCF changing from 4x to 10x, the implied forecasted price would be close to $13 and $28 per share.

{kind=link}

Competitors And Risks

Competitive markets for Silica Holdings are characterized by a concentration in a low number of national players and a large number of minor regional products. In January 2023, there were 122 commercial silica products, with 201 active operations centers in 32 US states. This market is highly conditioned by transportation costs, which deserves specific security conditions. This leads to a few companies being able to establish a nationwide customer and service structure like Silica Holdings.

The uncertainty condition in this market is high as a result of the global economic conditions. In addition, Silica Holdings' operations depend to a large extent on the activity of its clients in the oil and gas market as well as their production cycles. Currently, there are major transformations in these areas.

On the other hand, the company's operations are highly concentrated on just four of its production plants, which combined accounted for 29% of the company's sales. This is undoubtedly a risk factor in the event of complications in any of these facilities as well as the reduction in the demand for frac sand due to the appearance or development of new proppants that are used in hydraulic fracturing techniques.

The concentration also extends to its clients, which among the top ten confirmed 40% of Silica's revenues in 2021 and 2022. The loss of any of these clients could have serious effects on operating conditions and access to available capital, which also depend on the payment capacity of its clients and the fulfillment of deadlines in the contracts.

Conclusion

I am overall very impressed with the reduction in the net leverage reported by U.S. Silica Holdings. As a result, I believe that we may see further improvements in the EV/FCF and EV/EBITDA in the coming years. I also think that greater sales of higher-margin products mainly in the ISP business segment and lower operating costs will most likely lead to FCF margin improvements. I do see risks from any problems in the largest facilities operated by Silica, client concentration, and changes in the price of certain raw materials. With that, I believe that Silica could trade at more than $21 per share.

For further details see:

U.S. Silica Holdings: Higher-Margin Products Imply Undervaluation