SLCA - U.S. Silica: Lower Margins And Guidance Across The Board - Rating Downgrade (Hold)

2024-01-17 08:00:00 ET

Summary

- U.S. Silica Holdings, Inc.'s Q3 earnings and guidance disappointed, causing a selloff in the stock.

- The company's core business of selling frac sand declined in Q3, along with its industrial segment.

- Short-term catalysts for the stock may come from potential M&A activity in the sand supplier sector.

- We rate U.S. Silica Holdings, Inc. stock as a Hold at current prices.

Introduction

U.S. Silica Holdings, Inc. (SLCA) has not come under our gaze since May of last year, and I thought it was time to revisit the company. It was trading in the mid-$11's at that last article, and I gave it an upgrade to buy, agreeing with analysts that the company had upside potential to the low $20's. That call looked pretty good into September, when the company rallied to over $14.00. The selloff in crude and gas since has pulled the stock back down into the $10's. A roller coaster ride if ever there was one. Please have a look at older articles for deep background on SLCA, as this article will focus on their Q3 financials and outlook for Q4 2023 ( expected February 23rd).

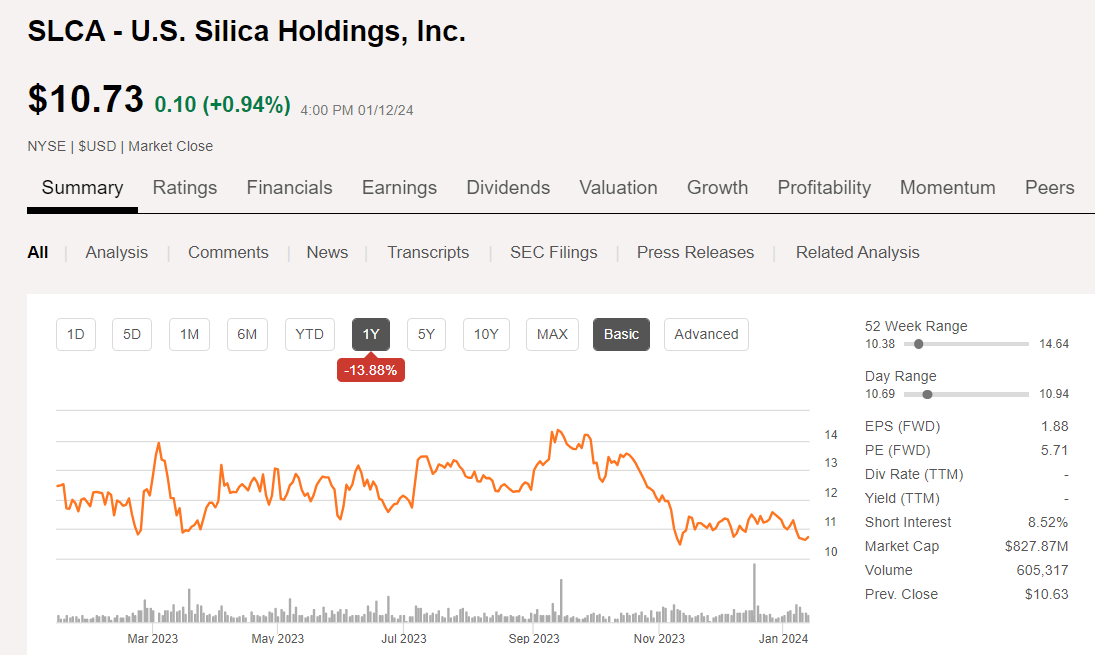

SLCA price chart (Seeking Alpha)

{kind=link}

The shares tanked on top and bottom line results when Q3 earnings were released, along with some fairly dour guidance for Q4. Analysts trimmed their expectations as a result and the shares came tumbling down. Their current ranking is Overweight , with 2 out of the three analysts covering the stock rating it a hold. Price targets range from $13.50-20.00, with a median at $14.00.

Recent trading has not been bullish, with a big move out of the stock on December 15th of last year. SLCA is currently sitting on its long-term support line at $10.73, and substantially below its 200 day SMA at $12.50. EPS projections have been trimmed from Q3's $0.39 to $0.25 for Q4, with a slight bump to $0.29 for Q1 2024.

With that, let's review the call for any relevant guidance.

The thesis for SLCA

The company is in the bulk materials-sand and logistics-Sandbox, for frac'ing, and diatomaceous earth, business, with a developing industrial segment that's tied largely to new build construction in the housing market. Selling frac sand remains its core business, driving 62% of its revenue and EBITDA. The industrial segment-ISP, comprises the rest of the revenue picture with fillers for paint and light colored sand for roofing tiles, but operates at a much higher contribution margin-$46.39 per ton vs. $26.55 per ton. Both of these businesses declined in Q3, 16% on the oilfield side, and 6% on the industrial side.

In the call the company mentioned a new venture on the oilfield side, the Guardian filtration system, intended to filter frac water entering pumping equipment. This looks like fairly dumb iron to me, and I don't see it as a big revenue driver. Equipment like this goes for a few hundred a day on a rental basis. Additionally, most frac water has already been filtered or treated a time or two before it hits the pumps, so this looks to me to be a final measure to insure nothing that won't go through the pump, ever hits the pump suction.

Guardian filter (SCLA)

Bryan Shinn, CEO, commented on the Guardian system in response to an analyst question during the Q3 conference call :

We have some commercial units out, and we have a lot of units out under trial. And I think there's a couple of big end users who are looking at potentially taking this technology across their entire system. So I think we'll have some success there. And as we look into 2024, I believe we'll definitely see some meaningful bumps there. The Guardian frac-fluid filtration system is performing well and gaining momentum in the market. Customers are experiencing positive outcomes through increased pump uptime and efficiency and decreased repair and maintenance cost.

In short, SLCA is a play on frac'ing activity, which is at lower levels YoY thanks to the prolific results from technology improvements. It also has an industrial lever to pull in the home building and paint additives businesses. This segment is also under stress thanks to record high home prices and interest rates shutting out all but a small segment of the population, as the Atlanta Fed notes .

Short-term catalysts

The primary catalyst for SLCA might be in the area of M&A. The M&A fever has largely escaped the OFS sector, and sand suppliers in particular are ripe for consolidation. Bryan Shinn addresses an analyst question in this regard during the call:

We think we all know as consolidation happens and there's more contiguous acres out there, lateral lengths will increase over time. And all that is, I think, beneficial for larger sand providers and logistics providers like us, because at the end of the day, a lot of the smaller guys just can't support the huge simul fracs that are out there today. So it may well necessitate consolidation, John, so we'll see. Hasn't really happened yet, but I think that could be on the horizon at some point here.

So we'll put a sticky note on that idea and not be surprised if announcements are forth coming.

Q3 and guidance

Total revenue decreased 10% to $367 million. Adjusted EBITDA decreased 17% to $102.1 million. OCF- cash flow from operations of was $76.7 million. And total company contribution margin decreased 14% to $129.2 million. Selling, general and administrative expenses for the quarter increased 2% sequentially to $29.3 million driven by slightly higher spending across the category in the quarter.

In Q3, they used excess cash on the balance sheet to extinguish an incremental $25 million of outstanding debt at par. Since the second quarter of 2022, SLCA has reduced their outstanding term loan balance by 26% or $320.1 million through repurchases and normal principal payments. At the end of the third quarter, their net leverage ratio improved to 1.4 times.

The oil and gas segment reported revenue of $231.4 million for the third quarter, a decrease of 12% when compared to the sequential second quarter.

Volumes for the oil and gas segment performed slightly better than their previous guidance, decreasing by 9% to total 3.1 million tons, while Sandbox-their field support logistics equipment, delivered loads decreased 8% compared to the sequential second quarter.

Segment contribution margin decreased 16% compared with the second quarter to $82.9 million, which on a per ton basis was $26.55. These results were driven by the sequential decline in U.S. completions activity, profit mixed, lower pricing, and reduced fixed cost absorption.

The industrial and specialty product segment reported revenues of $135.5 million, which was a 6% decrease compared to the prior quarter. Volumes for the ISP segment decreased 4% sequentially and totaled 999,000 tons. Segment contribution margin decreased 10% on a sequential basis and totaled $46.3 million, which on a per ton basis was $46.39.

The sequential decrease in the results for the ISP segment was due to reduced volumes for building products, DE fillers and filtration, and glass. On a year-over-year basis, contribution margin dollars were flat and contribution margin percentage expanded 11% due to pricing increases and cost improvement initiatives.

As of September 30th, 2023, the company's cash and cash equivalents totaled $222.4 million, a sequential increase of 19%, which includes the impact of the $25 million loan extinguishment. At quarter end, their $150 million revolver had $0 drawn, with $129.2 million available under the credit facility after allocating for letters of credit.

Looking ahead to Q4 2023

Kevin Hough, CFO noted:

Looking out to the fourth quarter, the high level of profit in customer contracts in our oil and gas segment, coupled with our sticky and diverse customer base in the industrial and specialty product segment, gives us reasonable confidence in our visibility for the remainder of this year. We continue to expect strong operating cash flow generation for the balance of 2023. We plan to direct our free cash flow to fund our growth capital needs, while we continue to reduce our net debt level.

Our current net leverage ratio expectation is that it will be below 1.5 times for the remainder of the year. Regarding capital spending, we will continue to be disciplined in our investments and focus on maintaining operating levels at our facilities while pursuing profitable growth. For full year 2023, we are revising our capital spending forecast to $60 million to $65 million as we have accelerated our capital investment for industrial growth projects.

Finally, we are lowering our forecast for the full year 2023 SG&A expense which is now expected to be down approximately 10% to 15% year-over-year reflecting a supplier contract termination and M&A related expenses that took place during the prior year along with ongoing cost control measures.

The forecast for the full year 2023 depreciation, depletion, and amortization expense continues to be flat to down 5% given higher CapEx spending levels in prior years for assets that have become fully depreciated. Our estimated effective tax rate for full year 2023 is approximately 26%.

We continue to anticipate that we'll generate robust operating cash flow of about $265 million this year with our net leverage ratio remaining below 1.5 times at year-end

Q3 earnings call.

Your takeaway

With the deceleration we are seeing in the OFS sector presently, it's hard to come up with a bullish thesis over the short term for U.S. Silica Holdings, Inc. With volumes and margins under stress and about 5 mm tons of new frac sand capacity coming on line, as noted in the call, the company lacks a catalyst to go higher. The company is trading at a reasonable 3.3X EV/EBITDA, so is not over priced at current levels.

The company pays no dividend, as it allocates free cash to debt reduction and growth capex for the ISP segment.

At this point, I have to agree with analysts that SLCA rates a hold at current prices, but if the share price dipped back into the single digits, U.S. Silica Holdings, Inc. stock might become a buy.

For further details see:

U.S. Silica: Lower Margins And Guidance Across The Board - Rating Downgrade (Hold)