LYFT - Uber: 12.5x 2024e FCF With Significant Growth Ahead

Summary

- I believe that Uber can generate $2/share in free cash flow per share in 2024 and ~$3.50 per share in 2026.

- While COVID was disruptive to ride-sharing, it killed off many of Uber's competitors and massively accelerated the growth of Uber Eats.

- Following 2022's tech wreck, VCs are no longer throwing capital at ride-share and food-delivery apps. Uber looks set to maintain/increase market dominance.

- Autonomous vehicles and ghost kitchens represent tremendous long-term opportunities for Uber.

- As investors gain confidence in free cash flow generation, I see the stock doubling in the near term.

Uber ( UBER ) shares fell 40% in 2022 (and are down around 40% from its 2019 IPO price). Beyond tech market malaise and general economic concerns, investor concerns include:

- history of unprofitability ($23 billion in accumulated losses)

- efforts by the Department of Labor to re-classify gig workers as employees which could increase operating expenses and raise costs to riders

- concerns that autonomous driving may introduce a set of new competitors in its ride share (mobility segment) business

Uber's current financial results have positively inflected as competitors have been forced to retrench (less VC funding available) and delivery operations have seen a step change increase in bookings, rendering the company's history of losses irrelevant. Further, as described below, I see autonomous vehicles as a source of opportunity rather than risk.

As we sit today, at $25/share, Uber trades at just 12-13x 2024 expected free cash flow per share (recently reiterated) and 7-8x my 2026 free cash flow estimate.

The Pandemic was a White Swan event for Uber

The pandemic brought a swift halt to Uber's core ride sharing business in early 2020. At the worst points of the pandemic, ride share bookings fell 75% from 2019 levels as stay-at-home orders lead to a near cessation of passenger movement. The pandemic initially seemed to be a negative Black Swan event for Uber. However, it has ultimately proven to be what is sometimes referred to as a White Swan - an unpredictable event with significant positive consequences.

While this fall off in demand caused a harsh decline in revenue and increased Uber's cash burn for a couple of quarters, it had several more important, long-term impacts on the structure of the global ride share market, including:

- Large losses and unwillingness of investors to continue to fund unprofitable operations lead smaller regional ride share companies like DriveNow, Via, and Juno to exit the market

- With a focus on cutting cash burn, Uber and Lyft ( LYFT ) reduced incentives to both drivers and riders. The companies finally began behaving as rational actors in a duopoly

Similarly, dire conditions forced Uber to re-evaluate its operations and lead the company to shutter unprofitable businesses and reduce its cost structure. Uber took the following actions to exit loss-making operations:

- Sold Jump (scooter/personal transport business)

- Merged Autonomous vehicle operations into Aurora

- Exited flying taxi business (Elevate)

This follows actions to exit markets where the company was losing money such as merging its China ride share business into DiDi ( DIDIY ).

Meanwhile, the 'stay at home' behavior of 2020 brought about a step-change surge in demand for Uber's Delivery segment - including its acquisition of Postmates, Uber Delivery saw bookings increase four-fold from pre-pandemic levels.

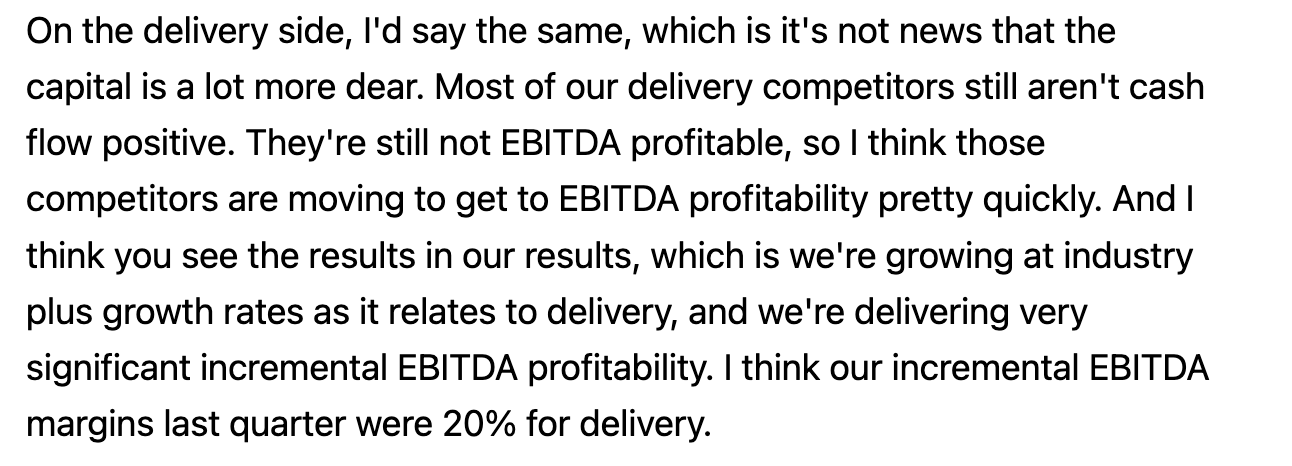

The massive increase in Uber Delivery (formerly known as Uber Eats) bookings lead the company to finally achieve the scale necessary to generate profitability in this business. Coupled with reduced competition (VC capital is not flowing to new food delivery businesses), segmental EBITDA has increased from -$316 million in 3Q19 to +$181 million in the most recent quarter - as incremental profitability is very strong (described below).

Uber CEO commentary on Delivery Economics (September Goldman Sachs Conference transcript from Seeking Alpha)

{kind=link}

Sustainable Competitive Advantage

Uber has a 65%+ market share in most markets served (representing 80% of gross bookings). This is a significant competitive advantage for a two-sided marketplace - by having the largest number of drivers Uber is able to provide the quickest service (shortest pickup times) to riders. Similarly, having the most riders attracts more drivers as a large base of riders reduces downtime (time without riders in the car).

This advantage is further enhanced by the presence of Uber Eats which gives drivers more opportunities to earn (drivers can do both Uber Eats and Mobility). Further, the cost of attracting new users and drivers to the Uber platform is significantly reduced as Uber can use Mobility to attract new drivers and consumers to Uber Delivery (and vice versa - use Delivery to attract new Mobility customers). Uber's cost of attracting new customers/drivers via cross promotion is 75% below using third-party advertising (such as social media). This is an important competitive advantage that is not available to competitors like Lyft, DoorDash ( DASH ), and Just Takeaway ( JTKWY ). Today, only 17% of Uber users use both Delivery and Mobility, implying a meaningful opportunity to gain share in both platforms via cross promotion.

Further, as the largest platform for mobility and food delivery, I see Uber's competitive moat strengthening over the next several years (as discussed below).

Future Growth Opportunities are Abundant

Beyond the continuing benefits of a less competitive environment, a massive step change in delivery volumes, and the benefits of operating Delivery and Mobility platforms, I see the potential for massively positive benefits to Uber from a couple of emerging trends, namely ghost kitchens and autonomous driving. In addition, Uber has a large advertising opportunity.

Ghost kitchens are kitchens solely focused on cooking and packing food for takeout/delivery without providing sit down dining for customers. These kitchens can be optimized for takeout and have lower real estate costs. Further operational complexity is reduced as there is no in restaurant dining (no need to worry about scheduling waitstaff for instance).

Ghost kitchens can be co-located (10-20 'restaurants' under one roof) with an optimized pickup experience for drivers. Drivers can pick up food from 10-20 different restaurants at one location. Not having to drive from restaurant to restaurant minimizes the amount of time a driver spends picking up food, improves food quality (stays hot/fresh), and ensures faster delivery times to customers at a lower cost. While ghost kitchens are still in their infancy, the step change in food delivery volumes suggests that increasing adoption is a matter of 'when' rather than 'if'.

Ultimately, I see Uber as the prime beneficiary of increased ghost kitchen adoption as the total market size for food delivery increases the total addressable market by decreasing the cost of food delivery and improving quality. The change to restaurant economics will create an opportunity for value capture which will be best exploited by the largest delivery platforms which match customers and riders.

Autonomous vehicle adoption represents another large area for a significant increase in profitability for Uber. Driver earnings represent the largest share of value that lies between gross bookings (total cost to the rider) and operating profit to Uber in the mobility space. The gradual adoption of autonomous driving will allow Uber to significantly increase its take rate over time. Further, insurance costs (a large operating expense borne by Uber) should decline significantly as autonomous vehicles are less accident-prone than human drivers.

There are many potential forms that can be taken in the relationship between autonomous driving and ride sharing. It is possible that this can be done in a capital-light way whereby consumers and/or fleets choose to have their vehicle 'opt-in' to ride share and share the economics with Uber. Alternatively, Uber may choose to deploy its cash flow (discussed below) to purchase autonomous vehicles and capture the entire booking. While it is impossible to predict which form this ultimately takes, I believe that Uber's dominant position in ride sharing will only be enhanced given that 100 million consumers are currently using the platform. I also expect that autonomous vehicles will benefit the Delivery segment as well.

I don't see autonomous vehicle adoption as a threat to Uber's position. First of all, the auto market is highly fragmented . No automaker has enough market share to capably serve the ride sharing market (riders would be waiting much longer if they requested only a Tesla (TSLA), for example). Further, autonomous driving adoption will be gradual - the market will be in a hybrid state many years. Consider that even if 100% of vehicles sold each year were autonomous (unlikely for a multitude of reasons), this would only represent 9% of the total fleet (average vehicle age in the US is 12+ years). Further, autonomous driving, thus far, has mainly been limited to geographies with limited weather disruptions (rain/snow can disrupt sensors). Gradual adoption benefits ride sharing incumbents who have a large base of customers (Uber has ~100 million riders) and drivers and can provide a vehicle to the rider in the shortest amount of time (be it a human-driven or autonomous vehicle).

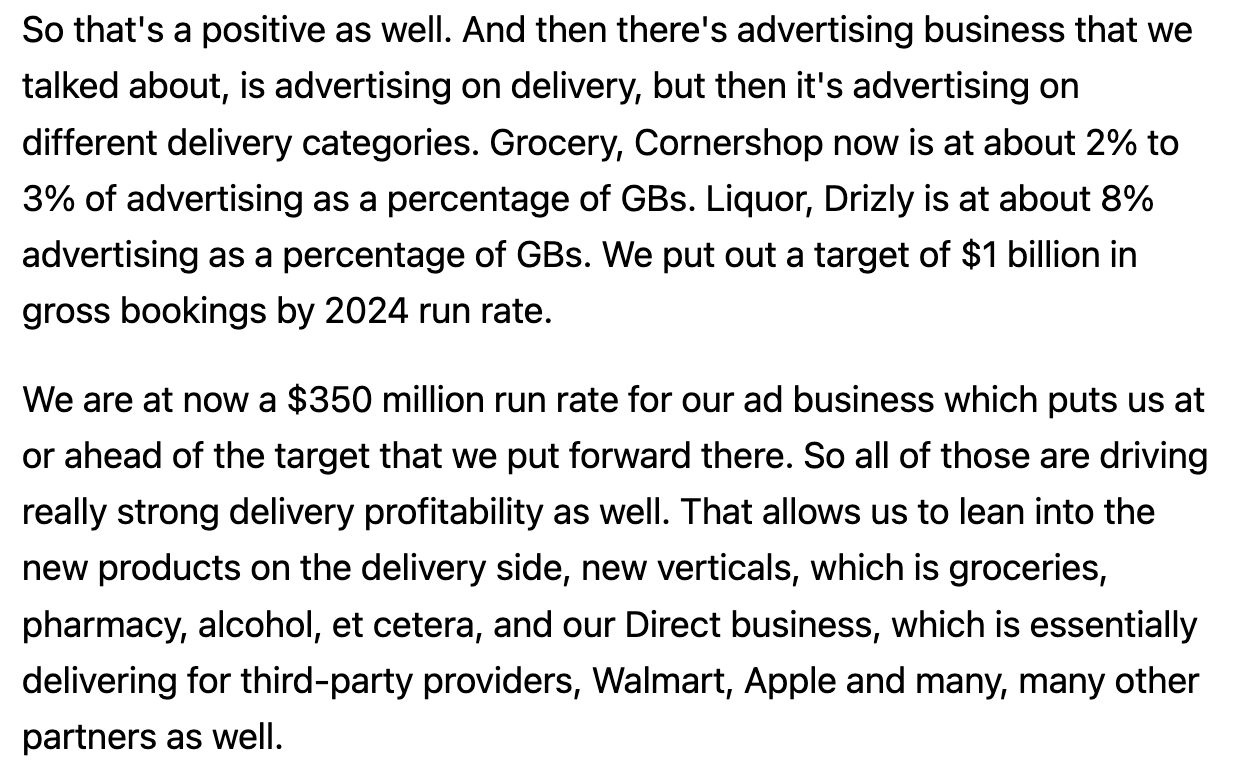

While the economic benefits of autonomous driving and ghost kitchens are likely 3-5 years away, Uber will realize a more immediate benefit from its advertising business. As we sit today, Uber is generating $350 million in annual run rate revenue from offering advertising both on its mobile apps (allowing restaurants to pay for preferred app real estate) and outdoor advertising (mini billboards on cars). The company has guided to $1 billion in advertising (with high incremental margins) looking out to 2024.

Uber CEO commentary on Advertising (September Goldman Sachs conference transcript from Seeking Alpha)

{kind=link}

Valuation & Conclusion

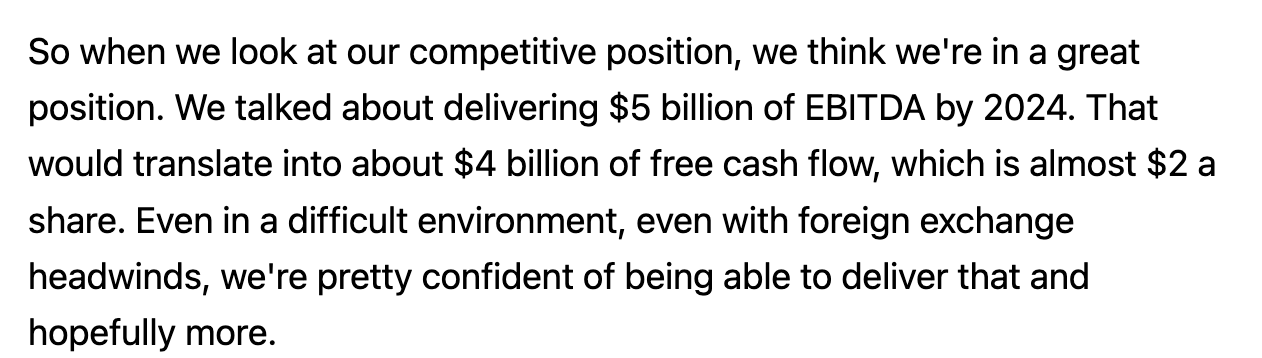

Uber is already generating positive EBITDA ($516 million in 3Q22 with guidance for $600-630 million in 4Q22) and has guided to $5 billion in EBITDA in 2024. The driver of getting from 4Q22 run rate EBITDA ($2.5 billion annualized) to $5 billion is a 7% incremental margin from total bookings (higher for mobility) as well as a high incremental contribution from the expected addition of $650 million in advertising revenue.

CEO guides to nearly $2/share in free cash flow per share in 2022 (September Goldman Sachs conference transcript from Seeking Alpha)

{kind=link}

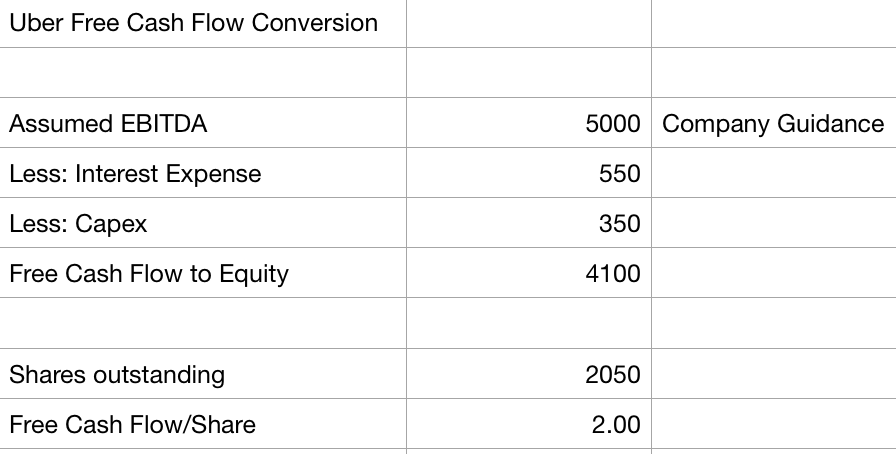

Importantly, Uber is an asset-light business and requires little in the way of capital expenditures. Equally important is that because Uber has generated an accumulated loss of ~$23 billion, the company has accrued massive tax loss carry-forwards which will shield the company from paying taxes for several years. As shown below, I expect Uber to generate nearly $2 per share in free cash flow in 2024.

Uber 2024 Free Cash Flow Estimate (Company Disclosure; Author Estates)

{kind=link}

Importantly, I expect free cash flow will continue to grow at a high rate beyond 2024, in part due to the benefits of ghost kitchens and autonomous driving but also due to underlying growth in ride share and delivery bookings (and improved incremental margins). Assuming 10-15% annual bookings growth at a 7-8% incremental margin gets me to $3.50 in 2026.

I believe that Uber is worthy of a premium multiple given its dominant market position, sustainable competitive advantages, and compelling long-term growth opportunities. Applying a 25x multiple on my 2024 free cash flow estimate, I get a value of $50 per Uber share which represents a 100% upside from the current price.

I see Uber as one of the most compelling opportunities available to long-term investors.

For further details see:

Uber: 12.5x 2024e FCF With Significant Growth Ahead