UBER - Uber: Entering The Black

2023-04-11 08:24:16 ET

Summary

- Uber finally become profitable on an adjusted operating income basis backing out R&D.

- Price to sales is still a bit rich, but lower than many recent tech IPO comps.

- The world is open, the apps are improving and revenue is growing.

Uber growth

I love the trend lines below for Uber (UBER). When you have trend lines for revenue or earnings making a dramatic cross over the price trend lines to the upside, it is certainly eye-catching. Let's look at the following points:

- Year over year growth in revenue of 82.6%

- Trailing 5 year revenue CAGR of 25% per year.

- All time total return per share of -24.36%

Uber IPO'd around $42 a share in 2019 and now sits in the low $30 a share range. The company has made enormous strides since going public with only downside price action. The stock is a buy and one that is on the verge of having a wide moat.

Price to sales

Price to sales is typically how we locate value in pre-profit companies. The price of Uber is actually down post-IPO while revenue is up. This has resulted in a lower and lower price-to-sales ratio which is now under 2 X.

Revenue sources as of 12/31/2022, Courtesy of FactSet:

| Mobility |

| 44.01% |

| Delivery |

| 34.2% |

| Freight |

| 21.79% |

Uber is unique compared to Lyft in that they have a diversified revenue stream that is not 100% based on ride-sharing. The Uberization of the taxi industry has already happened. On a recent business trip, I had the luxury of both using taxis and Uber.

Taxis were in terrible shape, the drivers had no interest in speaking to me and they were not even there waiting in the designated line upon arrival at the airport. An attendant had to call a taxi over, which was a first. To me, that was the last remaining advantage taxi services had over ride-sharing, they were always there waiting for you. Not so much anymore.

The Uber app just keeps improving. SeaTac airport had designated car parking spaces in the garages where the driver would be waiting to get you. That way you know exactly where to walk to and the app reflects it. The Uber drivers were happier than I had encountered in the past before Covid and the subsequent reopening of travel worldwide. I did not hear any complaints about not being paid enough or being raked over the coals by Uber regarding their tips. It seems Uber is starting to evolve and instead of them subsidizing their drivers, they've now been able to pass the increased fare along to us, the consumer.

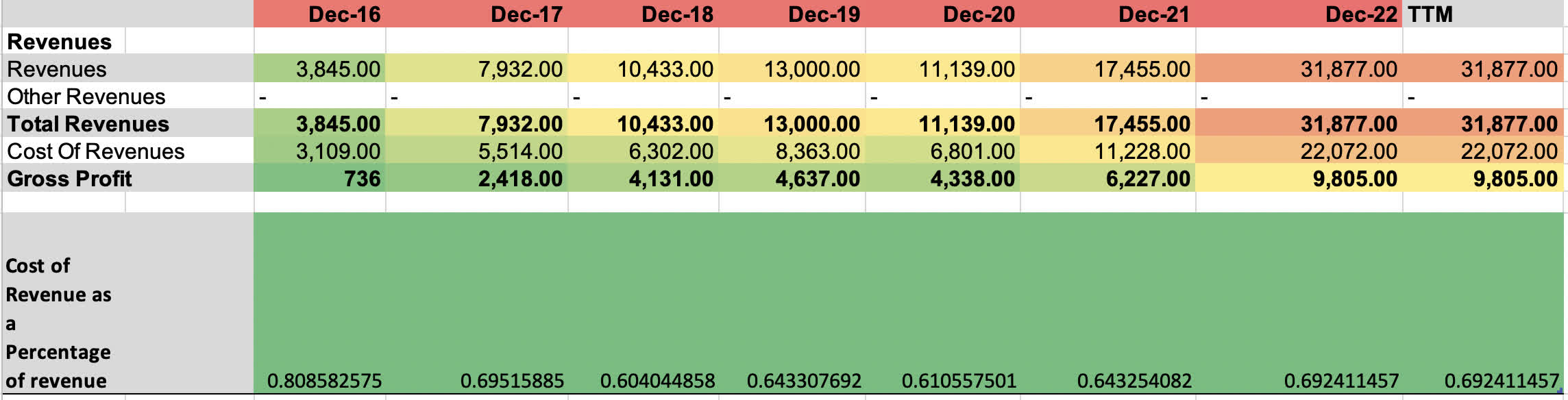

Uber cost of revenue progression:

My Own Excel. Data Via Seeking Alpha

{kind=link}

Taking a look at the progression of cost of revenue as a percentage of revenue, we see it starting at around 80% pre-IPO. It then began to dip and hit a low of 61% in 2020. From the low point to the current, Uber has added greatly to their freight and food delivery businesses, whereas they only had ride-sharing prior.

New businesses always need some sort of subsidization, but Uber, even with the two new businesses, has kept the cost of revenue at 69% or below. This is progress as the ride-sharing business is becoming more profitable, evening out the returns from the other businesses. If we were to segregate just the ride-sharing business, the cost of revenue would probably be down in the low 50% range at this point.

Trigger point

Like Amazon and others in the category of high revenue growth, pre-GAAP income plays, the trigger point of purchase for many comes at one seminal moment. The moment of a glimmer of hope and a possibility of possible operating margins. You see, this possibility lets one imagine what could be one day if growth initiatives were curbed. The R&D line in operating income provides a pre-tax growth engine that allows certain companies in tech to get ahead of the competition. If used wisely.

Some use it sparingly and some like Amazon ( AMZN ), Google ( GOOGL )( GOOG ), Meta ( META ), Microsoft ( MSFT ), etc.. have used it to their advantage to blow away the competition. Although UBER is nowhere near the revenue size of the latter-mentioned techno uncles, this aspiring nephew is learning the ropes and starting to gain its footing. After having a negative adjusted operating margin and operating income since IPO, the sprouts in the garden are starting to emerge. If the revenue continues to grow at the current pace, the self-sustainability of the business should only grow greater and greater along with it. Dara Khosrowshahi is starting to get the hang of it.

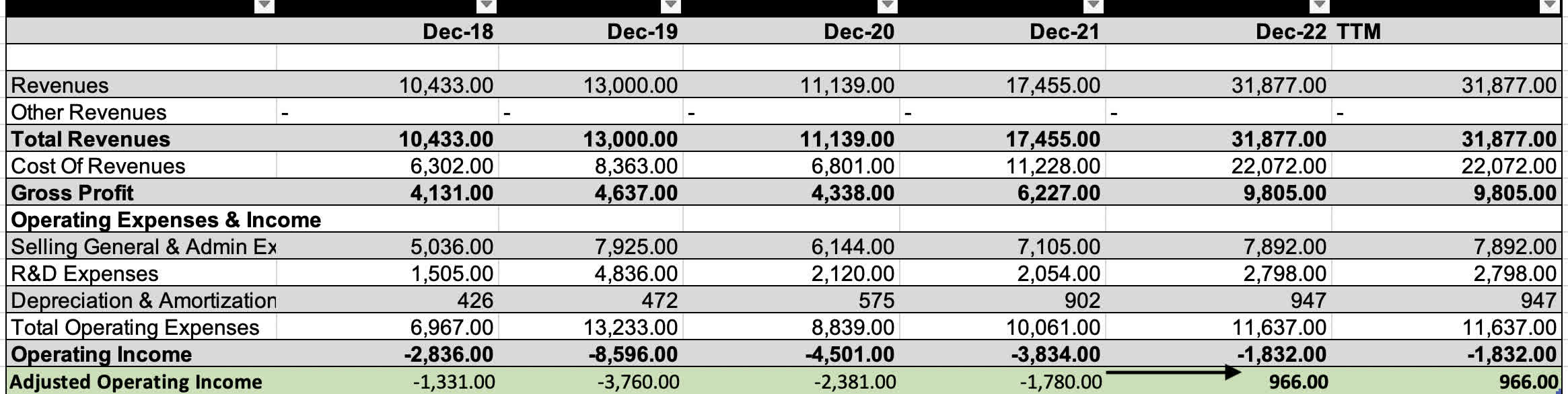

Backing out the R&D

{kind=link}

To quote a great cinematic hero, Egg Shen from Big Trouble in Little China:

"See? That was nothing. But that's how it always begins. Very small."

At just under $1 Billion in adjusted operating income when adding back the R&D line, the number is not huge, but the company is now showing that the top line is trickling down to the bottom line. This is just what I like to see and wait around for in companies with high revenue growth. This is when the magic begins, it might take time for the market to see it, but several case studies would tell you this is important.

Compared to Lyft

{kind=link}

Adding R&D back into the Lyft ( LYFT ) operating income, the company is still in the red to the tune of $548 million. Not huge, but what stands out the most is the revenue. Uber by revenue comparison is on the order 7 X larger than Lyft. I've seen many Lyft vs Uber articles on here, but frankly speaking, the two companies scale-wise have little comparison.

Post profitability, yes, small companies can be good investments alongside large ones, like Walgreens ( WBA ) vs. Walmart ( WMT ). Old established industries where profit margins are available to everyone and it's not a zero-sum game. However, in new industries, it's normally those who fight and win the scale battle that ends up the victors.

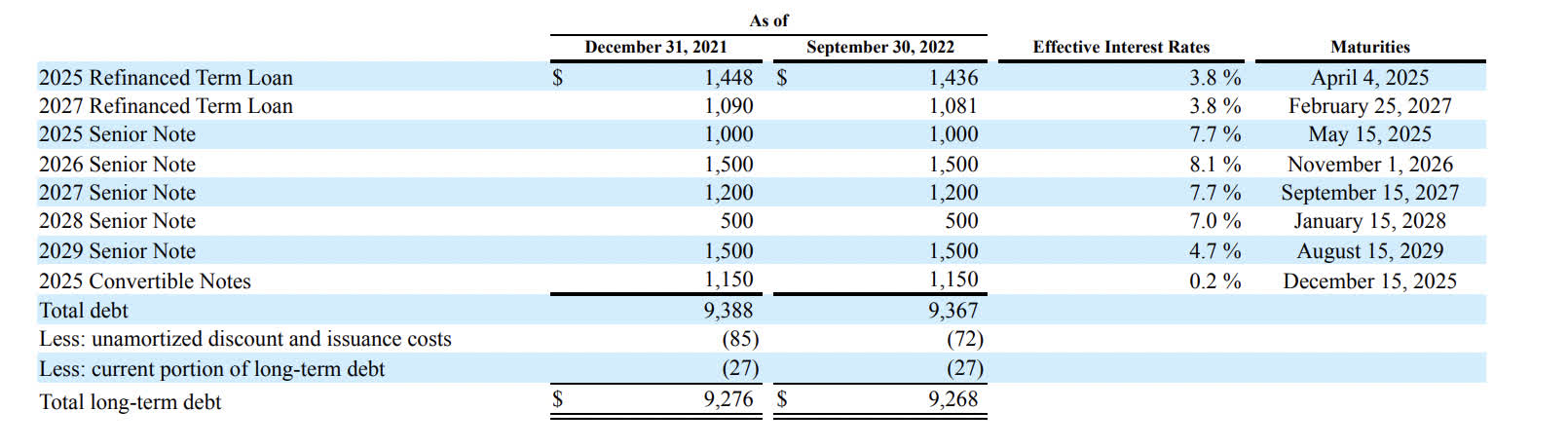

Balance Sheet

{kind=link}

Getting into the TTM data for Uber, we can see a slowdown in total debt accumulation when compared with 2019-2020, plus a slowdown in share dilution. These are all positive items showing greater self sustainability of the business.

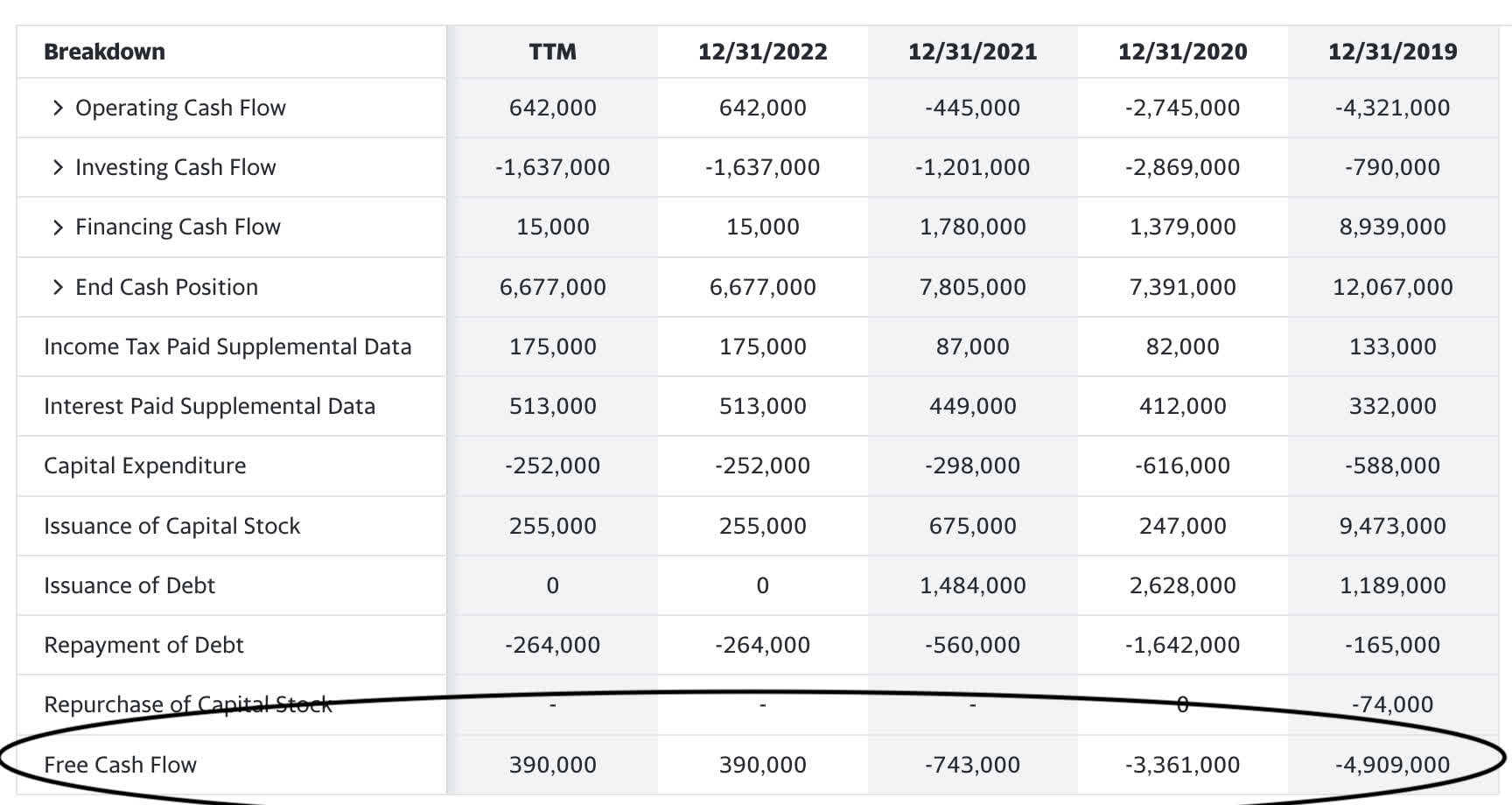

{kind=link}

We can also observe that Uber has pivoted into positive free cash flow. This is another great sign of self-sustainability without having to ratchet up debt or excessively dilute investors.

My decision tree of a tech spec buy

Harkening back to some great Charlie Munger quotes about decision-making in valuation and evaluation, I enjoy the quote he made equating investing to bridge:

“The right way to think is the way Zeckhauser plays bridge. It’s just that simple.”

Richard Zeckhauser himself has been interviewed to expound upon that same notion of decision-making as it relates to bridge, but basically, it all boils down to your list of probabilities and creating a decision tree. Below are some probability trigger points and commonalities I have found in books relating to early investments in Amazon and Costco before they became what they are today. These are part of my decision tree in stocks like Uber:

- Revenue increasing, share price flat to decreasing.

- Positive adjusted operating income, adjusted EBIT or EBITDA.

- Business scaling and growing.

- Low price-to-sales ratio.

The balance sheet is the one negative probability out of the deck of cards with a higher than normal debt to equity ratio for a tech company. The other probabilities line up nicely with a company scaling quickly, using R&D effectively, and getting to self-sustainment before their competition.

Risks

Global pandemic lockdowns and interest rates. Geopolitical worries are not an extreme threat as China has taken that market back a long time ago and would be the one market subject to travel slowdowns. There shouldn't be any revenue from China from my understanding as DiDi Global ( DIDIY ) was given the ride sharing market by the Chinese government and Uber was given the boot quite some time ago.

{kind=link}

Some maturities are coming up in 2025, two are low-interest 3.8% issuances to the tune of $2.5+Billion and the other are convertible notes at $1.15 Billion. Some dilution through conversion of the convertible notes is to be expected. I would also expect Uber's interest expense to double in 2025 for the 3.8% notes if they are refinanced at a long duration. The near-term increase in interest might be in the neighborhood of an extra $100 million or so per annum post-2025. Now that Uber is generating positive free cash flow, they can also dampen the blow a bit with some debt repayment.

Catalysts

Another new segment that is intriguing would be same-day package delivery. Hiring drivers to deliver packages from point A to point B locally seems extremely logical and another business that could scale up quickly. I could imagine one day that the delivery business could begin to service logistics centers with a similar vehicle leasing program as Amazon. This could easily be a new and large area for top-line growth to look out for along with strides in the freight segment.

Speaking of freight and knowing someone who has a small trucking business, it seems about as easy as buying and getting licensed for a big rig, collecting a shipping container at point A, and bringing it to point B using the Uber app. This business is allowing individuals to be full-time employed business owners running a legitimate freight company. For all those that dreamed of traveling the country, liberating themselves from a 9-5, and maybe winning a few arm wrestling competitions like Stallone in Over the Top, this is an amazing opportunity.

Conclusion

Uber is my main focus currently for a pre-GAAP profit, revenue growth company. I have a few others on my list that are within my price-to-sales range, but not yet turning a profit on an adjusted EBIT, EBITDA, or operating income basis. Uber has buy rating by Bank of America Securities, CFRA, and Morningstar. The revenue growth is amazing and there isn't much competition in this space as Uber is quickly becoming a wide-moat industry leader.

The balance sheet is the only area leaving me from slapping a strong buy on the stock. All my other boxes are checked for companies in this growth stock category. I am not expecting, or hoping this stock takes off this year. I'd hope it gets closer to $25 at which the price-to-sales ratio would be closer to 1.5X. This is a stock I intend to hold forever and will be accumulating throughout the year. The only thing that will impede me is a large price break out to the upside. Uber is a buy here.

For further details see:

Uber: Entering The Black