LYFT - Uber Q3 Earnings: Still A Buy On Track To Reaccelerate Gross Bookings

2023-11-07 17:05:00 ET

Summary

- We maintain our buy rating on Uber Technologies, Inc.

- Uber Q3 2023 results and outlook for next quarter confirm that Uber is on track to reaccelerate its gross bookings into 1HFY24.

- We believe the company will continue to drive profitable growth scaling across mobility and delivery segments and expect this to boost top-line growth in 2024.

- Additionally, we see an improved position for Uber in the advertising business into 2025.

- We expect Uber stock to outperform through 1H24.

We remain buy-rated on Uber Technologies, Inc. ( UBER ). We understand investor concerns regarding top and bottom lines falling below estimates during Q3 , but we're not too concerned. We see a longer-term outperformance for Uber driven by reacceleration in its gross bookings.

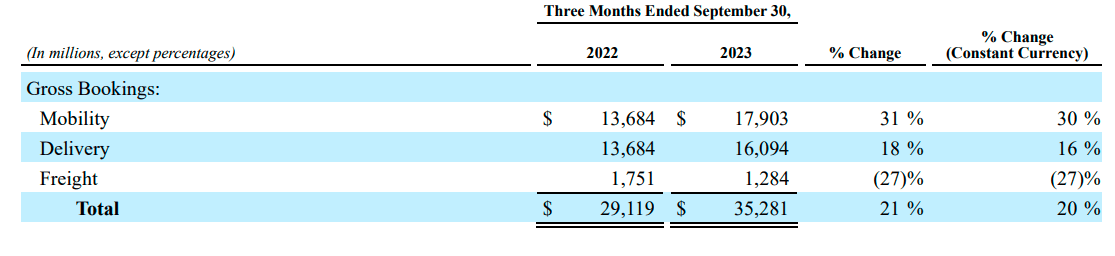

Consistent with our expectations, mobility and delivery segment gross bookings increased substantially this quarter, by 31% and 18% Y/Y to $17.0B and 16.09B, respectively. We think lower revenue this quarter is due to macro headwinds and business model changes negatively impacting revenue margin. We believe the company will continue to drive profitable growth scaling across mobility and delivery segments and expect this to boost top-line growth in 2024. We think investors overreacted to the estimate miss this quarter, considering that gross bookings growth exceeded expectations. We expect Uber stock to outperform the peer group through 1H24.

The following outlines Uber's performance against Lyft, Inc. ( LYFT ) and the S&P 500 (SP500, SPY).

YCharts

We think the 3Q23 results and outlook for next quarter confirm that Uber is on track to reaccelerate its gross bookings into 1HFY24-management guides for gross bookings of $36.5-37.5B and adjusted EBITDA of $1.18-1.24B. We see more upside for the stock as management scales its delivery and mobility segments. The following outlines the gross bookings this quarter.

{kind=link}

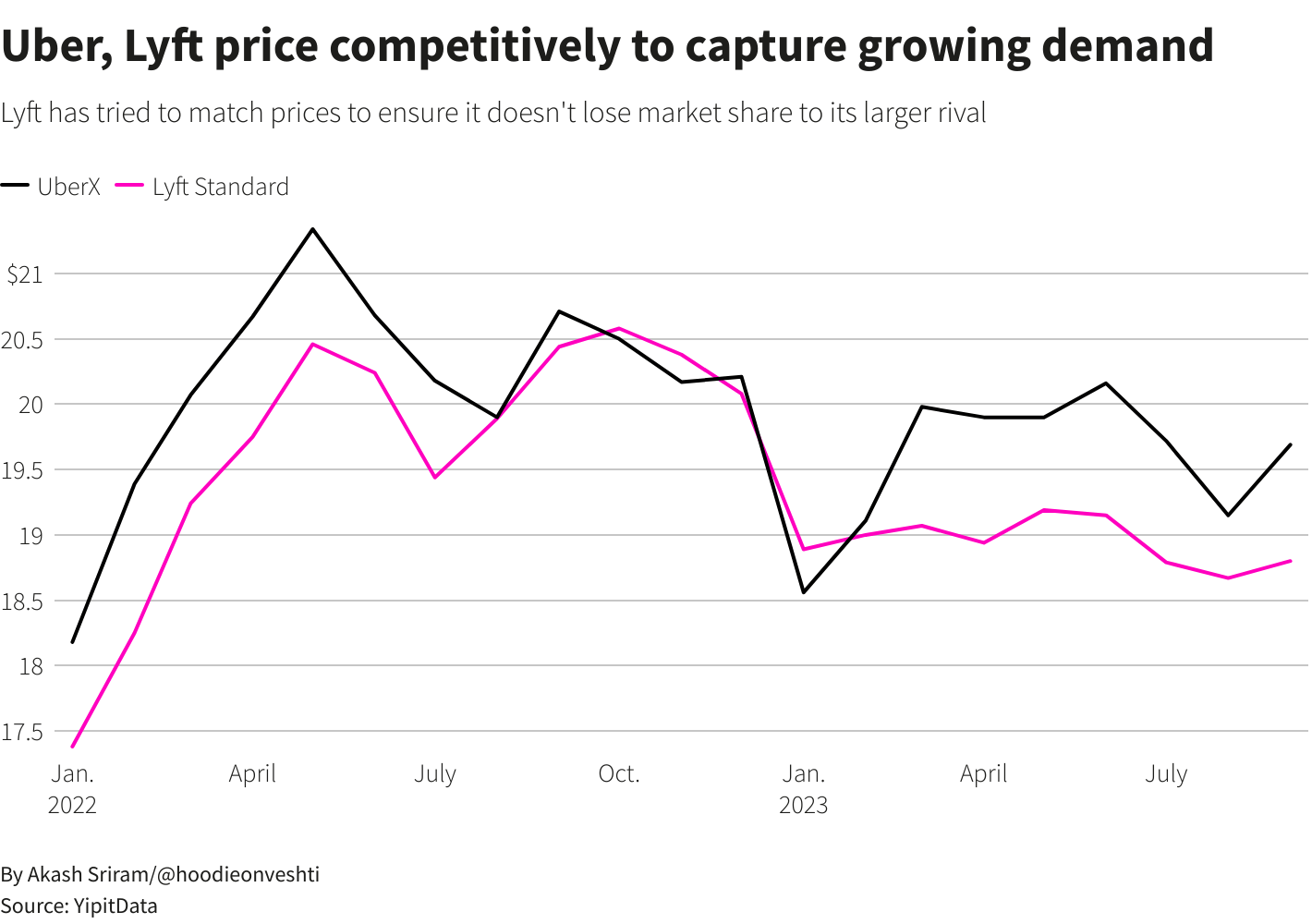

We think Uber's higher double-digit growth in mobility also helps put investor concern over competition with Lyft to bed for the time being. Lyft cut prices earlier this year; the average price of a Lyft ride as of September end was "more than 4% cheaper than Uber's similar service, according to data analytics firm YipitData." In comparison, both companies were charging roughly the same price in February. We think the ride-sharing market is becoming increasingly competitive in regard to pricing, but we believe 3Q23 results highlight Uber's relative resilience in spite of Lyft's price cuts due to diversification across delivery and freight. The following outlines Uber and Lyft's competitive pricing.

{kind=link}

Additionally, we expect growth to be supported by a recovery in the spending environment; we see this playing on two fronts. The first is a recovery in travel spending; we're seeing better-than-expected results across the sector, with Booking Holdings Inc. ( BKNG ) growing top line growth ahead of estimates and Airbnb, Inc. ( ABNB ) exceeding estimates. The second is a rebound in ad spending, which we expect to bode well for Uber's advertising opportunities.

Valuation

The stock is fairly valued, in our opinion, granted that margins continue to improve. On the P/E basis, the stock is trading at 45.1x C2024 EPS $1.07 compared to the peer group average of 20.4x. The stock is trading at 2.4x EV/C2024 Sales versus the peer group average of 2.5x. We think Uber stands to fare better than stocks within the same sector that are trading at higher multiples; the main case in point is Airbnb, Inc. ((ABNB)). We recently upgraded the stock to a hold based on a more balanced risk-reward profile as travel spending rebounds, but we don't see any near-term catalyst driving outperformance. Meanwhile, Uber is seeing a trend of stronger mobility and delivery growth into 2024. We recommend investors explore entry points into the stock at current levels.

The following chart outlines Uber's valuation against the peer group average.

TSP

Word on Wall Street

Wall Street shares our bullish sentiment on the stock. Of the 47 analysts covering the stock, 45 are buy-rated, and the remaining are hold-rated. We think investor confidence in Uber will continue to push the stock higher into 1H24. The stock is currently priced at $48. The median and the mean sell-side price-targets are $58, with a potential upside of 19-20%. The following charts outline Uber's sell-side ratings and price targets.

TSP

What to do with the stock

We remain buy-rated on Uber Technologies, Inc. shares. We think 3Q23 results and outlook for next quarter confirm that gross bookings will reaccelerate toward 2HFY24. We see management achieving profitable growth driven by the scaling strategy for mobility and delivery. Additionally, we expect to see an improved position for Uber in the advertising business into 2025. We see the stock trading higher into 2024 and recommend investors add on the pullback.

For further details see:

Uber Q3 Earnings: Still A Buy, On Track To Reaccelerate Gross Bookings