UBER - Uber's Starting To Look Like An Early Amazon

2023-04-11 08:46:25 ET

Summary

- Uber is a logistics software company that readily uses its technology to enter new business lines.

- Its relatively new subscription service, Uber One, already has 12 million people signed up and comes with a host of benefits for the business.

- Furthermore, it is trading cheaply relative to its true sector comparison: Information Technology. This is sensible as it is actually a software company, albeit one that works with physical goods.

- In this article I outline the logic of all of this and why Uber is starting to look like Amazon.

Overview

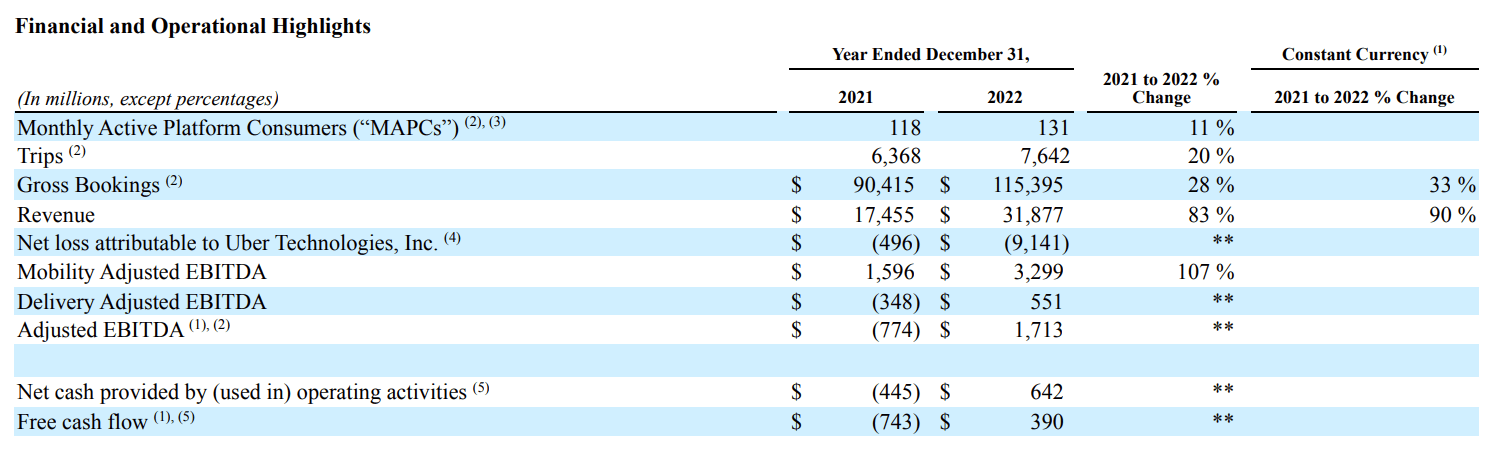

Uber ( UBER ) has long been a polarizing stock, with significant skepticism on the part of some investors as to whether the business model can even work. The results for 2022 went a long way towards proving that it can. Operating cash flow, adjusted EBITDA, and free cash flow all in came in positive – a first in the company’s operating history. All this came along with very significant revenue growth: 83% year-over-year.

{kind=link}

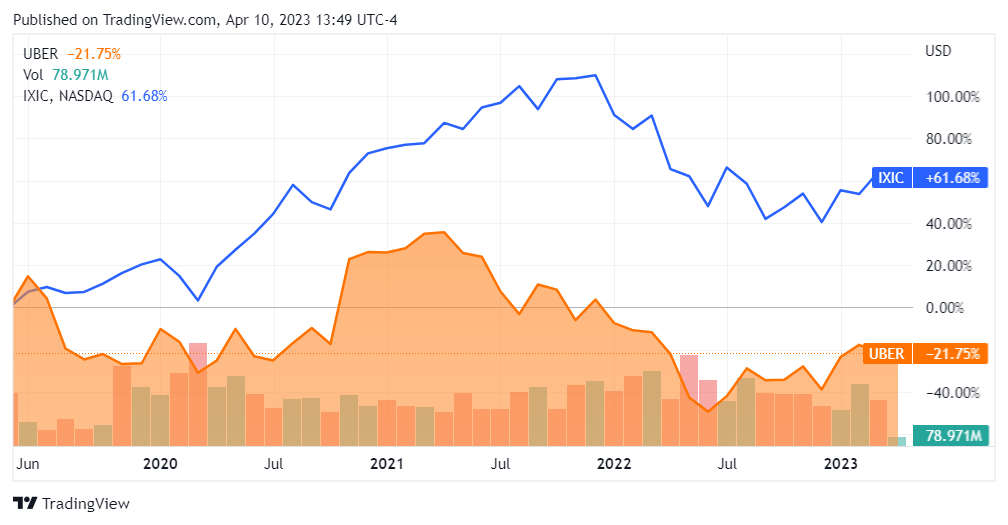

Yet, the stock hasn’t taken off as a result. Indeed, Uber stock is still trading at a discount to its IPO price as well as significantly trailing the price performance of the NASDAQ Composite. While some of this can be attributed to the ongoing dilutive effect of share-based compensation, this is far from the full story. Simply put, not enough investors are putting money into the stock. This continues to be the case even as the company has maintained a relatively high institutional ownership percentage ( 73.77% as of this article ).

I think a lot of this is due to Uber being a misunderstood business and thus a misunderstood stock. In this article I’m going to highlight why this may be the case and what I believe makes this company interesting.

{kind=link}

Valuation

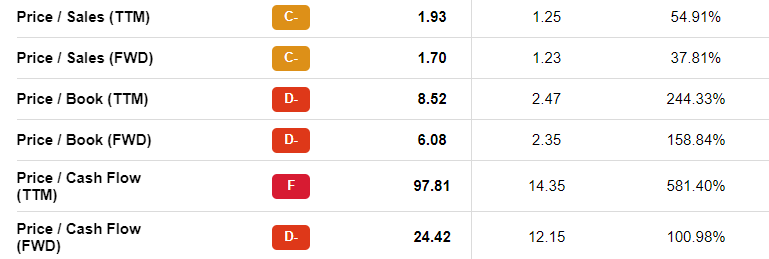

Let’s start with valuation. Upon first glance, Uber looks to be fairly expensive. The company trades at a premium to its sector across the board, especially so when we look at its operating cash valuation.

However, I wouldn’t be so quick to accept this at face value. The company is classified as part of the Industrials GICS Sector and the Passenger Ground Transportation industry, where valuations tend to be low.

Uber, however, isn’t really like other companies in the Industrials Sector; it’s actually a software company. It doesn’t operate or own cars - or any heavy machinery in general. Rather, it uses algorithms to route these physical assets as well as their human operators.

{kind=link}

As such it makes more sense for us to compare its valuation to the Information Technology sector instead. Here, we see a different picture emerge.

| Metric |

| UBER |

| IT Sector Median |

| % Diff to Sector |

| Price/Sales TTM |

| 1.93 |

| 2.77 |

| -30.32% |

| Price/Sales FWD |

| 1.70 |

| 2.67 |

| -36.33% |

| Price/Cash Flow TTM |

| 97.81 |

| 19.65 |

| 397.76% |

| Price/Cash Flow FWD |

| 24.42 |

| 18.56 |

| 31.57% |

| YoY Revenue Growth |

| 82.62% |

| 14.32% |

| 476.96% |

Source: Author's Spreadsheet, Data from Seeking Alpha

While still expensive on a TTM cash flow basis, we must keep in mind that Uber has just crossed the threshold as to becoming a cash flow positive company last year. As to its revenue multiple, Uber is actually discounted to the overall sector by roughly a third. This is the case even as it is posting YoY growth rates that are 476% that of the IT sector’s median. The forward-looking cash multiple has it trading at a premium, but this is only one year out.

Overall I think this valuation is closer to the reality of Uber’s business and makes the company look that much more attractive for prospective investors.

Uber's Business: Starting to Look Like Amazon

Uber’s business is also relatively unique and has synergies that may not be appreciated off the bat. I actually find Uber to be reminiscent of Amazon in several respects. This may sound like a stretch, but allow me to explain.

Digitized Logistics

The first element of this is that Uber, like Amazon, is at its core a digitized logistics business: it uses software to move real world assets. Just like Amazon was a pioneer in using algorithms to control its supply chain, so is Uber. Uber actually takes it a step further by not owning the physical assets that it controls. While Amazon leverages algorithms to control its inventory, Uber leverages algorithms to control assets that are technically not its inventory. This makes it even more of a ‘pure software’ company. As mentioned, it doesn’t own cars and it doesn’t employ drivers – it simply routes them using software.

Diversification & Marginal Diversification

The next element of this is that Uber is well-diversified and continues to become even more so. Since its core competency is routing physical goods using software, it is able to establish any logistics-oriented business line rapidly and at a lower marginal cost.

While starting out with just rides, it entered the food delivery business and has already turned it into a positive adjusted EBITDA business. It has also been delivering groceries. Uber has been delivering alcohol since acquiring Drizzly in Q1 2021. Around that time, it also started delivering prescriptions. Uber can deliver just about anything, since that’s what its core network and algorithms allow it to do; perhaps this is starting to sound familiar. This technology has also been readily ported to routing freight trucks through Uber freight.

Subscription Offering

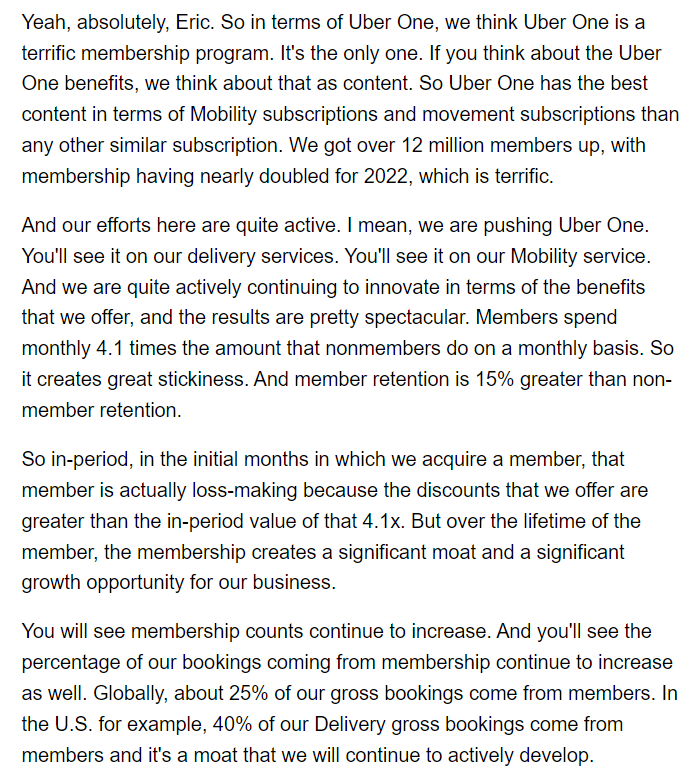

Just like Amazon Prime changed the game for Amazon, Uber One has changed the game for Uber. This subscription service already has 12M users signed up and comes with the same economic benefits as Amazon Prime has had for Amazon: improved consumer retention, higher spending per user, and smoother revenues. I think Uber One will continue to drive results across each of those metrics and further cement Uber’s moat.

{kind=link}

Conclusion

As you can see, there is more than meets the eye with Uber. This company has a robust business that’s growing rapidly, both in terms of revenues as well as the diversity of its offerings. Because of its unique core competency - logistics software - it is able to grow both vertically and horizontally quite readily. Additionally, Uber has been getting strong traction in ensuring users stick with it through Uber One. All of this comes along with a valuation that’s much better than it seems. I am handedly reiterating my belief that this stock is a buy.

For further details see:

Uber's Starting To Look Like An Early Amazon