DASH - Uber Technologies: Finally Gaining Traction

Summary

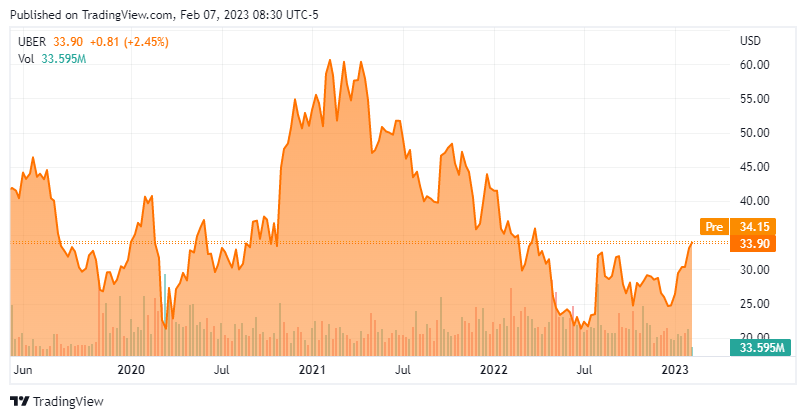

- Shares of Uber Technologies are up over 35% to start 2023 as the market grows increasingly confident in its ability to reach its FY24 Adj. EBITDA goal of $5.

- On an Adj. EBITDA basis, the pioneer in ride sharing will post its first-ever, full-year positive result when it releases earnings on February 8, 2023.

- With a business model resilient to economic downturns (save pandemic-induced global lockdowns), this busted IPO’s push towards profitability merited a closer examination.

- A full investment analysis follows in the paragraphs below.

The one thing that unites all human beings, regardless of age, gender, religion, economic status, or ethnic background, is that, deep down inside, we all believe that we are above-average drivers .”? Dave Barry

Today, we take a deeper look at one of the best known 'Busted IPOs' in the market, Uber Technologies ( UBER ). This one time unicorn has given shareholders a wild ride since coming public in mid-2019. The shares are off to a hot start in 2023 and the company seems to be gaining traction in several areas of the business. The company's fourth quarter earnings report should be out shortly. Below is an analysis on where the company stands prior of a fresh set of new data.

{kind=link}

Company Overview:

Uber Technologies, Inc. is a San Francisco based transportation platform moving individuals, food, and freight from point A to point B. It is currently responsible for nearly two billion trips every quarter provided primarily to its ~124 million active users. Having pioneered the notion of ride-sharing, the company operates in over 70 countries, originates approximately one-quarter of its rides within the U.S., and nearly one-quarter of them in five metropolitan areas: Chicago, Miami, New York, Sao Paulo, and London. It also has equity stakes in other mobility and delivery concerns valued at ~$4.4 billion (as of September 30, 2022). Uber was founded in 2009 and went public in 2019, raising net proceeds of $8.0 billion at $45 per share. The stock trades around $34.00 a share, translating to a market cap just north of $67 billion.

November Company Presentation

Operating Segments

The company disaggregates its operations into three segments: Mobility; Delivery; and Freight.

Mobility consists of customers downloading the Uber app and requesting transportation to a designated location, provided by drivers operating on the same platform. Rates charged are algorithmically based on the current competitive landscape, customer’s personal preferences, and (in some instances) government mandates. Uber receives a cut (~20%-25%) of the gross booking charge for matching driver and passenger. Contingent upon the geography, competition includes Lyft ( LYFT ), Ola ( OLAC ), DiDi ( DIDIY ), Grab ( GRAB ), and other taxi services (including its own Yandex JV) in what it estimates to be a $5 trillion plus total addressable market ((TAM)). It vies for passengers based on price and speed to pick up. That said, it is the undisputed leader, having commanded 46% of global gross ride-share bookings in FY20. Mobility accounted for segment Adj. EBITDA of $2.29 billion on revenue of $9.89 billion during the first nine months of 2022 (YTD22).

Launched approximately seven years ago, Delivery allows consumers to order food, alcohol, and other items from ~870,000 merchants for pick up or delivery. Best known for its Uber Eats app, it competes with similar offerings from DoorDash ( DASH ) and Amazon ( AMZN ) (amongst others), generating segment Adj. EBITDA of $310 million on revenue of $7.97 billion in YTD22.

Freight connects carriers with shippers available on Uber’s platform with the touch of a button and competes with DHL, XPO Logistics ( XPO ), and many other freight brokers. It was responsible for segment Adj. EBITDA of $8 million on revenue of $5.41 billion in YTD22.

Geographically, approximately five-eighths of the company’s top line is derived from the U.S. and Canada, with slightly more than one-fifth generated out of the EMEA.

Historical Operating Performance

Before the pandemic, Uber was growing like a weed, with gross revenue expanding at a 63% CAGR from $2.0 billion in FY15 to $14.2 billion in FY19. In an effort to penetrate markets and corral share, it also lost money hand over fist, generating negative $6.81 a share (GAAP) and negative Adj. EBITDA of $2.7 billion in FY19.

With the advent of the pandemic, available drivers for Mobility plummeted – although Delivery did provide somewhat of an in-built hedge – and revenue fell to $11.1 billion in FY20. That said, Uber began to operate more efficiently, with Adj. EBITDA improving slightly to negative $2.5 billion that same year.

FY21 saw a return to growth with a 57% surge in revenue to $17.5 billion while Adj. EBITDA improved to negative $774 million. Of note, Delivery exited FY21 more than three times larger than at the onset of the pandemic (4Q21 gross bookings of $54 billion versus 4Q19 gross bookings of $17 billion).

Anticipating this return to growth, the market rallied shares of UBER 367% off its pandemic sell-off lows to an all-time high of $64.05 in February 2021. That market cap of ~$119 billion represented a price-to-FY21 revenue of 6.8 – somewhat outrageous for a business with no profitability in sight. As such, with the macroeconomic backdrop uncertain and inflation taking a bite out of high-growth no-profit concerns, Uber’s stock retreated 69% to an intraday low of $19.90 a share on the final trading session of 1H22. That said, it has caught a bid to begin 2023, up 37% YTD.

3Q22 Earnings & Outlook

And it would appear that some of that enthusiasm is rooted in the belief that Uber is heading towards profitability, with evidence provided on its 3Q22 financial report of November 1, 2022. On that date, it posted a loss of $0.61 a share (GAAP) and Adj. EBITDA of positive $516 million on revenue of $8.3 billion versus a loss of $1.28 a share (GAAP) and Adj. EBITDA of positive $8 million on revenue of $4.8 billion in 3Q21, representing a 72% improvement at the top line (and 83% on a constant currency basis). [GAAP earnings, which include the change in value of its equity stakes in other like businesses, is not terribly meaningful. Non-GAAP earnings are not provided by the company.]

November Company Presentation

Strength was seen across the board with Mobility generating segment Adj. EBITDA of $898 million on a 73% year-over-year surge in revenue to $3.8 billion; Delivery contributing segment Adj. EBITDA of $181 million on a 24% increase in its top line to $2.8 billion; and Freight delivering $1 million of segment Adj. EBITDA on revenue of $1.8 billion, up 336% over 3Q21.

November Company Presentation

On a global basis, the number of drivers has returned to pre-pandemic highs, although only ~80% of the 2019 level in the U.S., where drivers earn ~$36 an hour.

November Company Presentation

The company stated that October was tracking to be its best month ever for both Mobility and total company gross bookings.

November Company Presentation

Longer-term, as the company further distances itself from the pandemic, it has its eyes on generating Adj. EBITDA of $5 billion on gross bookings of ~$170 billion in FY24 (based on range midpoint), suggesting a gross bookings CAGR of 22%-25% (FY21 to FY24).

Balance Sheet & Analyst Commentary:

Furthermore, cash flow from operating activities YTD22 was $886 million (free cash flow: $693 million), placing Uber in the position to make either significant reinvestments into its business, repay debt, or return capital to shareholders. As of September 30, 2022, the company held unrestricted cash and equity positions of $9.3 billion against a similar amount of debt.

November Company Presentation

Street analysts are overwhelmingly constructive on Uber, registering approximately 30 buy or outperform ratings against only one hold rating by KeyCorp. Their median twelve-month price objective is $54. On average, they expect the company to lose $0.18 a share (GAAP) on revenue of $8.5 billion in its final stanza of 2022, bringing the year to a loss of $5.06 a share (GAAP) on revenue of $31.8 billion. In FY23, Uber is expected to lose $0.29 a share (GAAP) on revenue of $36.8 billion, representing 16% growth at the top line.

Verdict:

Given its history of losses, its challenging to evaluate the ride-share pioneer on traditional metrics, only on perceived progress and what-if scenarios. Despite declarations to the contrary, Uber is resilient to the macroeconomic backdrop – another global pandemic shutdown notwithstanding – as more people may elect to hail rides as opposed to repairing or replacing an old vehicle. People who opt not use its ride service to patronize nice restaurants due to poor personal financial condition may choose to use its delivery service to order in cheaper food.

With its sturdy model, Uber has momentum, and it is on its way to achieving its FY24 goals. However, assuming achievement of $5 billion in Adj. EBITDA in FY24, that would put it at a current ‘forward’ EV/Adj. EBITDA of ~13, which is not a bargain. With a 37% run up already in 2023, the recommendation is to wait for a better entry point below $30 a share. Investors will get another set of data points when the company reports fourth quarter results tomorrow.

Americans will put up with anything provided it doesn't block traffic .”? Dan Rather

For further details see:

Uber Technologies: Finally Gaining Traction