CSGKF - UBS Group AG: Undervalued And Poised For Post-Takeover Upside

2023-05-31 00:01:04 ET

Summary

- UBS released an updated F-4 filing, outlining some positive new insights into the pending Credit Suisse deal.

- The case for pro-forma balance sheet accretion looks compelling, while conservative PPA and legal provisions offer incremental upside.

- UBS stock hasn’t quite recovered following this year’s selldown; at current levels, there’s compelling value on offer.

With the Credit Suisse ( CS ) takeover fast approaching its conclusion, UBS Group AG ( UBS ) has released initial pro-forma financial estimates via an updated SEC F-4 registration statement – a first since the transaction was announced in March this year. While management did caution (multiple times) that any estimates were preliminary and subject to change, the filing marks a key step toward clearing up some of the major uncertainties related to the deal, including with regard to the purchase price allocation ((PPA)), as well as the pro-forma balance sheet and CET1 outcomes post-completion.

On balance, the incremental detail appears positive for the bull case - the breakout of the day-1 PPA charge, for instance, indicates most of the charges relate to accrual assets (e.g., fixed-rate loans and trading assets) that will benefit from a ‘pull-to-par’ effect if held to maturity. Relative to the benefits, the costs seem manageable – even accounting for the larger-than-expected losses CS posted in its latest quarter and potential revenue dis-synergies post-deal, the pro-forma group should have ample buffer to absorb any shocks. With the deal set to close in the coming weeks and UBS equity lingering well below the pro-forma tangible book value (despite double-digit % tangible book accretion potential), patient, long-term-oriented investors should come out ahead.

Updated SEC Filing Adds Color to the UBS/CS Deal Economics

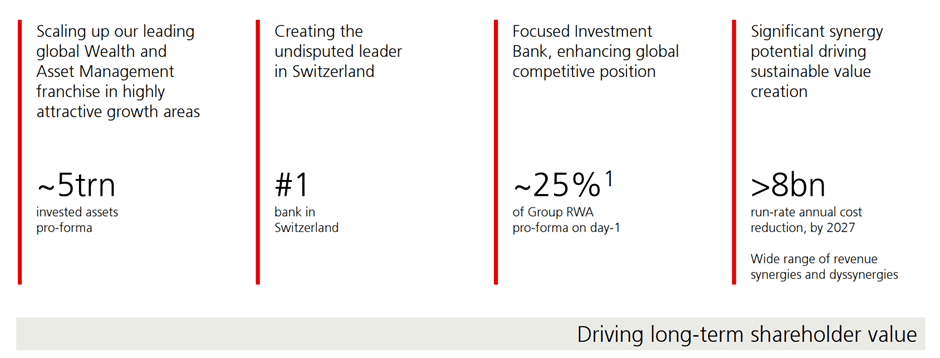

When UBS management last completed a preliminary assessment of a CS deal and the potential pro-forma implications, the conclusion was unanimous that an acquisition was “not desirable.” But since then, a lot has changed. The Swiss banks have been effectively forced into a merger, though this time around, CS’ financial troubles have given UBS a significant upper hand on deal terms. UBS CEO Sergio Ermotti has changed his stance as well, most recently talking up the deal on the Q1 call . The strategic emphasis seems to be on scale - Ermotti guided to ~$5tn of combined invested assets post-deal, making UBS the global #2 wealth manager and enhancing its strategic footprint in growth markets like Southeast Asia, the Middle East, and Latin America. This assumes limited attrition, though, which could prove optimistic given the pace of CS’ AuM attrition thus far (>CHF170bn of outflows over the Q1 2023/Q4 2022 period, mainly in wealth management).

{kind=link}

UBS Group AG

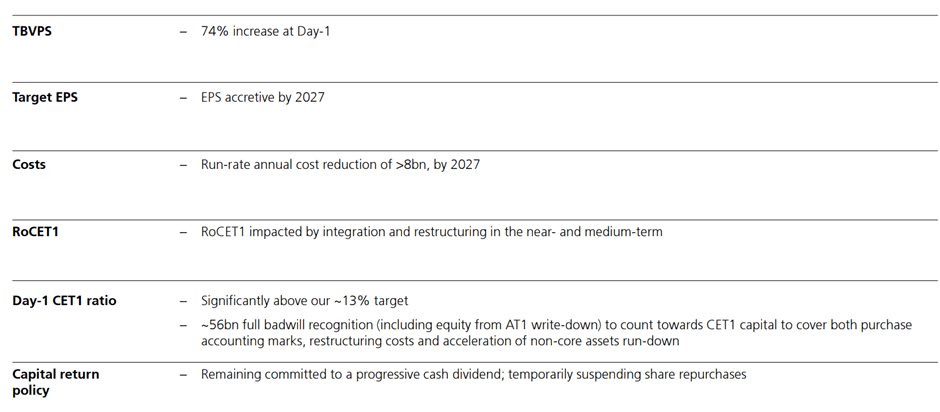

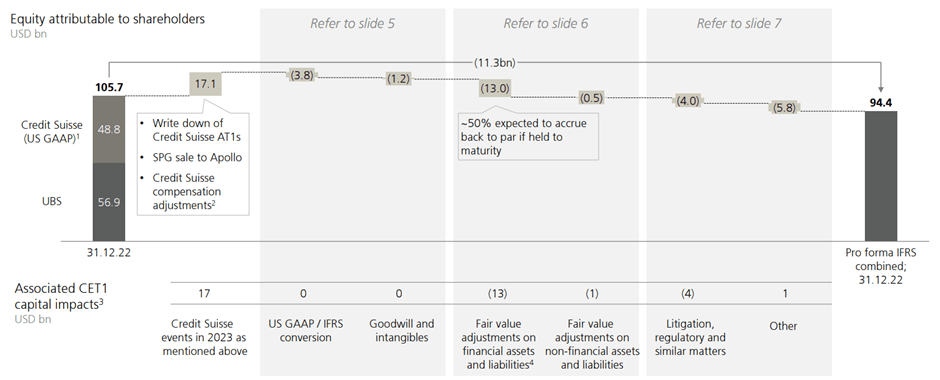

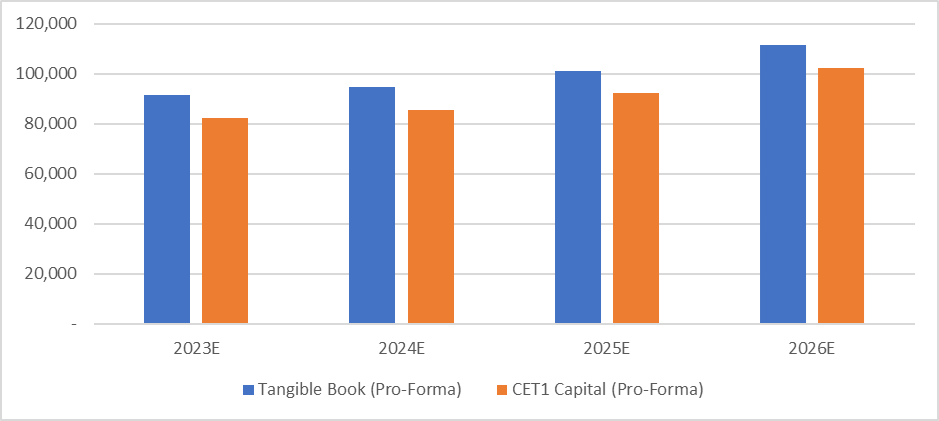

Post-Q1, UBS has shed light on the financial case as well, most recently filing an updated F-4 registration statement with plenty of helpful insights on the pro-forma balance sheet and P&L. The projected +74% increase (vs. stand-alone UBS) in day-one tangible book value remains intact, implying a pro-forma value of $28.3/share (or $93bn after accounting for 178m of new shares being created). The new filing also clarifies the assumptions embedded in this pro forma guide, including a full AT1 write-down, compensation adjustments (as communicated to CS by Swiss regulators), and the sale of CS’ Securitized Products Group to Apollo Global Management ( APO ). Despite the larger equity haircut (vs. initial guidance), the day-one CET1 of >14% still implies an >$7bn buffer relative to UBS’s current ~13% CET1 target. Hence, the pro-forma entity should comfortably absorb any additional charges post-closing. A word of caution, though – these estimates are based on an outside view of trailing balance sheet figures and may thus be subject to sizeable revisions over the coming months.

{kind=link}

UBS Group AG

‘Pull To Par’ and More Sources of Incremental Upside

Another key highlight from the F-4 disclosure was the size of the purchase price allocation (i.e., charges relating to IFRS requirements for recording acquired assets and liabilities at their fair values post-deal closing). Of the $13.5bn estimated markdowns, ~$13bn is solely from financial assets/liabilities, with ~50% expected to ‘pull to par’ (i.e., converge to par value) if held to maturity. Assuming the pro-forma balance sheet is as robust as projected, UBS should have no trouble realizing these gains over time. The ~$4bn of additional litigation provisions also seem conservative in light of CS’ Q1 disclosure of “reasonably possible” losses (excluding those covered by existing provisions) amounting to ~$1.3bn. Some of the delta is likely conservatism, though accounting differences (e.g., contingent liabilities treatment under IFRS vs. US GAAP) related to risk assessment are a key contributor as well.

{kind=link}

UBS Group AG

The most notable omission from the filing was details on the state guarantees (via the SNB) UBS will receive, a key source of downside protection for the pro-forma entity. Early details have been positive, though - UBS’ Q1 commentary pointed to legally enforceable liquidity guarantees from the SNB that should protect UBS from major deposit flights post-takeover. The market hasn’t yet given the bank much credit for this option, with UBS stock still trading well below day-one pro-forma tangible book. Assuming no execution mishaps and the jittery sentiment on banking stocks eventually eases, the stock has a clear re-rating path from here.

{kind=link}

JP Research

Undervalued and Poised for Post-Takeover Upside

With the UBS-Credit Suisse merger/takeover entering its final stages, the latest SEC F-4 registration statement filing was timely. The new disclosures were especially positive for the bull case, validating the potential ‘pull-to-par’ upside from the PPA, as well as the strength of the pro-forma balance sheet. Strategically, the cost-benefit of combining the Swiss banks’ assets remains uncertain – the ~CHF5bn loss for stand-alone CS in Q1 indicates more dis-synergies than synergies, though the pro-forma CET1 and the SNB liquidity guarantee offers a sizeable safety margin. The P&L accretion will be trickier, given the likely attrition at CS in the initial years, though cost-out initiatives should help as well.

The biggest source of upside, in my view, is the valuation. Despite a favorable ROTE and tangible book value accretion outcome, UBS is currently being priced at a wide discount to its pro-forma tangible book value; thus, investors have many ways to win from here. Key upside catalysts over the coming months include incremental detail on the post-deal profitability roadmap (and the resumption of buybacks), as well as updated listing plans for the Swiss business.

For further details see:

UBS Group AG: Undervalued And Poised For Post-Takeover Upside