ULBI - Ultralife: Backlog Increase And FCF Growth Imply Undervaluation

2023-07-31 22:41:29 ET

Summary

- Ultralife Corporation reports an impressive increase in backlog, indicating potential for future net sales growth.

- Communications Systems segment shows significant revenue growth, driven by demand from government, defense, and medical customers.

- Market analysts have positive expectations for Ultralife, with projected growth in net sales, EBITDA, and net income.

Ultralife Corporation ( ULBI ) recently delivered an outstanding increase in backlog thanks to new orders from government, defense and medical customers. I believe that considering the actions announced to deliver sustainable profitable growth, the impressive net sales growth in the Communications segment, and expectations from analysts, ULBI could surprise even more in the coming years. I saw risks from raw materials’ inflation, cybersecurity attacks, or a reduction in the budget made by the U.S. Government. With that, my DCF model implied certain undervaluation in the stock price.

Ultralife Corporation Reported An Impressive Increase In Revenue In The Communications Systems Segment

Ultralife Corporation offers products and services, including power solutions to communications and electronics systems, to clients in the government, defense, and commercial sectors.

Source: Ultralife Corporation

The list of products offered by Ultralife is long. It includes rechargeable and non-rechargeable batteries, charging systems, communications and electronics systems as well as accessories. With many products in different markets, I believe that the net revenue is diversified, which may lower future net sales volatility.

Source: All Products | Ultralife Corporation

Ultralife uses several trade channels, including original equipment manufacturers and distributors to the industrial and defense sectors. The company also reports sales, operations, and product development facilities at an international level in North America, Europe, and Asia.

Ultralife reports two operating segments: Battery & Energy Products, which offers Lithium 9-volt, cylindrical, and thin cell, and the Communications Systems segment, which includes RF amplifiers, power supplies, and cable and connector assemblies.

The Battery & Energy Products segment appears to be most relevant in terms of revenue, however the revenue from the Communications Systems segment is growing at a large pace. In the quarter ended June 30, 2023, the revenue from the Communications Systems multiplied by more than four as compared to the same quarter in 2022.

Source: 10-Q

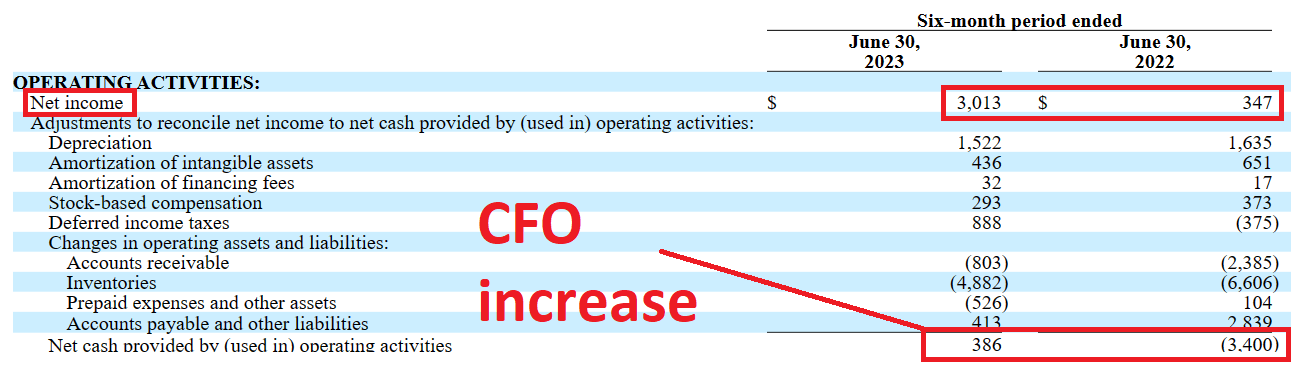

It is also worth noting that in 2023, market participants saw a significant increase in the net income. In the six months ended June 30, 2023, ULBI reported close to ten times more net income than that in the same period in 2022. Additionally, ULBI reported a significant increase in the cash flow from operations, which would most likely have an impact on the recent beneficial stock price performance.

{kind=link}

The beneficial results came from surging demand from government/defense and medical customers. With that, management also pointed out certain improvements in gross margin and disciplined spending, which, in my view, may continue to have beneficial impact in the coming quarters.

With backlog increasing to $110.9 million and durable demand across our diverse end markets, the near-term highest priority remains to recapture gross margin through continued execution of price realization activities, qualification of alternate component suppliers, and lean manufacturing initiatives. Source: Ultralife Corporation Reports Second Quarter Results

Beneficial Expectations From Market Analysts

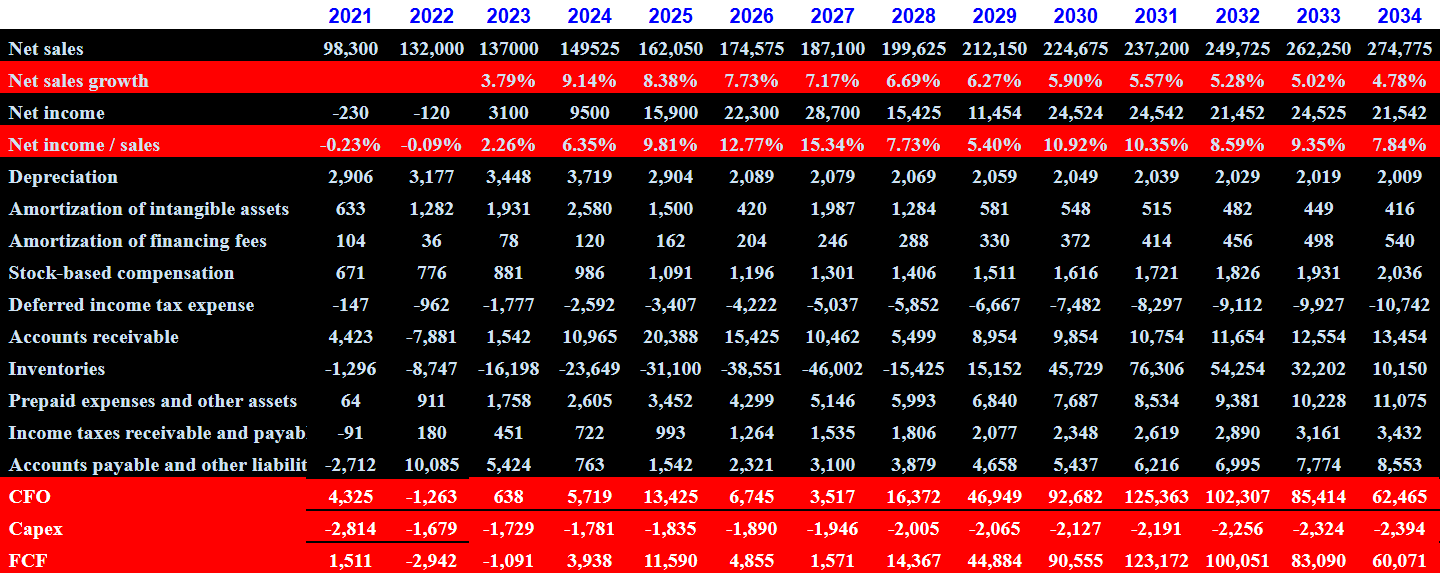

I believe that there are a lot of market analysts who like Ultralife Corporation. Future estimates for 2023 and 2024 include net sales growth, EBITDA growth in 2024, and net income growth. More precisely, 2024 net sales would stand at $149 million, with 2024 EBITDA of $15.5 million, 2024 EBIT close to $12.5 million, 2024 net income of about $9.5 million, and EPS of close to $0.61 per share.

Source: Market Screener

Balance Sheet

The quarter ended on June 30, 2023 surprised investors with an increase in total assets driven by increases in cash, increases in trade accounts receivable, and increases in inventories. I believe that we can explain some part of the outstanding spike in the stock price by the very decent balance sheet reported. In recent days, the stock price increased from around $5 per share to close to $7-$8 per share.

Source: SA

More in particular, the company reported cash worth $8 million, trade accounts receivable of $28 million, inventories worth $46 million, and prepaid expenses and other current assets close to $4 million. Total current assets stood at $87 million, significantly higher than the total amount of current liabilities. Liquidity may not be a problem in the near future for Ultralife.

The list of long term assets included property, plant, and equipment worth $21 million, goodwill close to $37 million, deferred income taxes of about $11 million, and total assets worth $175 million. The asset/liability ratio is larger than 3x, so I believe that the balance sheet stands in good shape.

Source: 10-Q

I am not concerned about the total amount of long term debt and short term debt because the company is showing positive free cash flow generation and net income growth. In my view, if management needs some new financing, banks will be ready to offer it. Accounts payable stood at $18 million, with the current portion of long-term debt worth $2 million, accrued compensation and related benefits of $2 million, and long-term debt close to $22 million. Total liabilities were equal to $55 million.

Source: 10-Q

My Discounted Cash Flow Model

In my financial model, I assumed that the actions that we saw in the recent quarter will most likely continue to play a beneficial role and may enhance FCF generation from 2023. In addition, I assumed that further strengthening of relationships with key customers and growth in new markets could also accelerate net sales growth. The company is clearly reporting more net sales growth in foreign jurisdictions. With know-how accumulated in the United States, I would expect further net sales in Europe or Asia

These actions position us to deliver high-quality, sustainable profitable growth for 2023 generating incremental cash flow to pay down our acquisition debt and further invest in our businesses. Source: Ultralife Corporation Reports Second Quarter Results

Source: 10-k

The RF amplifiers and other products that Ultralife Corporation sold are acquired by U.S. military and foreign defense organizations. The fact that we saw an increase in the sale of these products to defense organizations appears quite beneficial. These groups have large budgets and very serious due diligence assessments before acquiring products. In my view, if they bought once, they will most likely buy more. Additionally, I believe that the fact that the U.S. military is buying products will most likely enhance the interest from other foreign defense organizations.

The military systems include RF amplifiers, power supplies, power cables, connector assemblies, and amplified speakers. We market these products to all branches of the U.S. military and foreign defense organizations that we are permitted to sell our products to, as well as U.S. and international prime defense contractors. Source: 10-k

From 2023 to 2034, my financial model includes a median net sales growth close to 6% with a median net profit margin of 8.9%. I believe that the net sales growth assumed is in line with the market growth expected for the global power markets.

The Global Power Electronics Market was worth USD 22.58 billion in 2020 and is poised to amass a valuation of USD 35.72 billion by 2027, registering a CAGR of 5.9% over the forecast duration of 2022-2029. Source: The Global Power Electronics Market to Show Positive Growth at CAGR of 5.9%

The global market for RF Power Amplifiers estimated at US$6.4 Billion in the year 2022, is projected to reach a revised size of US$16.6 Billion by 2030, growing at a CAGR of 12.7% over the analysis period 2022-2030. Source: RF Power Amplifiers - Global Strategic Business Report

{kind=link}

My financial model also included amortization of intangible assets growth, stock based compensation growth, some account receivable growth, and growth in changes in inventories. In sum, cash flow from operations would grow from around $5 million in 2024 to close to $62 million in 2033-2034.

More precisely, I assumed 2034 net sales worth $274 million, 2034 depreciation of $2 million, stock-based compensation close to $2 million, changes in accounts receivable worth $13 million, and changes in inventories close to $10 million. Besides, with changes in accounts payable and other liabilities worth $8 million, 2034 CFO would be about $62 million, and with capex of -$3 million, 2034 FCF would be $60 million.

{kind=link}

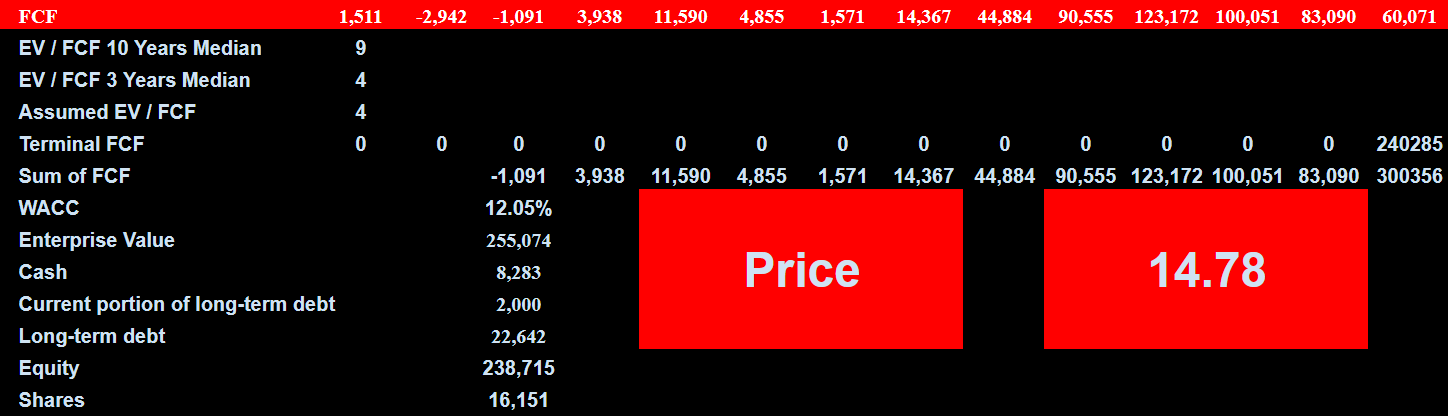

Taking into account that the EV/FCF 10 years median is close to 9.055x, I believe that assuming a terminal EV/FCF of 6.055x is reasonable.

Source: YCharts

If we assume a WACC of 12.055%, the implied enterprise value would be about $255.55 million. If we add cash worth $8 million, and subtract the current portion of long-term debt close to $2 million and long-term debt of about $22 million, the implied equity would be $238.05 million, and the fair price would stand at close to $15.

{kind=link}

Risk Factors

I believe that ULBI would most likely suffer from rapid cost inflation of raw materials, which may lead to lower gross margins and lower FCF growth. Management noted initiatives to increase the price of products, however we cannot really know whether ULBI will be fully successful.

Going forward, to reduce this lag, we are initiating more frequent customer price increases closely aligned to cost increases, subject to our customers’ willingness to accept of the price increases. Source: 10-k

It is also worth noting that there is one customer, L3Harris Technologies, which was responsible for a significant part of the revenue. It is a clear risk as negotiations with this customer may lead to lower FCF margins. Besides, if L3Harris Technologies decides to leave ULBI, the decline in sales would most likely lead to significant stock price declines.

We have one customer, L3Harris Technologies, a large global defense primary contractor, which comprised 17% of our total revenues in 2022. Source: 10-k

In 2022, the company reported that 29% of the total amount of revenue came from sales made directly or indirectly to U.S. and foreign militaries. A significant reduction in the budget and appropriations decisions made by the U.S. Government may have a detrimental impact on future sales growth. The communications business segment appears to sell a lot of products to militaries. I believe that a deterioration in the relationship with these buyers would lower future sales growth.

Cyber-security appears to be a serious risk for ULBI. In 2023, the company noted an attack from a third-party, known for ransomware attacks. In this regard, I believe that the cyber-security insurance of $100,000 signed by ULBI appears too small. In my opinion, attackers may cause economic damages and reputational damages that exceed $100k.

On February 7, the Company received an electronic communication allegedly from a third-party, known for nefarious ransomware attacks, claiming responsibility for the incident, and discussions with that third party commenced through experienced cyber-security professionals engaged by the Company. The Company’s deductible for its cyber-security insurance is $100,000. Source: 10-k

I believe that many analysts became extremely optimistic about ULBI after taking a look at the impressive increase in total backlog seen on June 30, 2023. Many may expect double digit backlog growth also in 2024 and 2025, which could lead to significant stock price appreciation. ULBI may deliver lower growth than expected, which would most likely have a detrimental impact on the stock price.

Our total backlog at June 30, 2023 was $110,875 representing a 40.1% increase over the comparable $79,147 for the same period last year. Source: 10-k

A Lot Of Competitors Are Large

Competition in both segments appears to be intense with many domestic and global actors. Competition is based on design flexibility, performance, price, reliability, and customer support.

I believe that the company offers superior technologies and services than many other peers, which would explain the recent increase in revenue. With that, there are larger companies with more resources and more personnel, which may offer better designs, and adapt their offerings faster than ULBI.

Conclusion

Ultralife Corporation recently delivered an impressive increase in backlog, which may most likely accelerate net sales growth in the coming years. The Communications Systems segment is experiencing significant net sales growth thanks to growing demand from government, defense, and medical customers. I would also expect further improvement in the CFO and FCF margins thanks to announced actions to deliver sustainable profitable growth. Even taking into account recent increases in the stock price, my DCF model implied significant upside potential in the stock price.

For further details see:

Ultralife: Backlog Increase And FCF Growth Imply Undervaluation