UIS - Unisys: Revenue Constrained Stable Margins With AI Prospects

2023-07-19 08:42:26 ET

Summary

- Unisys reported a 15.6% year-on-year increase in revenue for Q1-2023, the highest rate since June 2021.

- It becomes important to assess whether such a pace can be sustained especially that second quarter financial results are expected on August 1.

- Unisys' capabilities in cybersecurity, data analytics, and artificial intelligence are leading to valuable project engagements but exposure to the financial sector for its cloud business is currently problematic.

- Any improvement in sector performance or AI-related sales could improve growth expectations for the fiscal year 2023.

Unisys' ( UIS ) revenue for the first quarter of 2023 (Q1-2023) represented a year-on-year surge of 15.60% which is the highest rate since the June 2021 quarter and yet, there was no equivalent level of market enthusiasm.

Thus, given that second-quarter (Q2-2023) financial results are expected on August 1 , the underlying reasons for this growth must be understood in order to assess whether the company can sustain these figures in order to improve on its revenue expectations for the full year which ends in December. This is especially the case in a macroeconomic environment characterized by customers exercising caution on new IT spending. This thesis will also highlight AI-led growth and margin improvement prospects for this IT service provider.

IT Spending and Segmental Revenue Growth

According to a report by the IDC or International Data Corporation dated April 5 this year, global IT spending continues to slow down in reaction to the weak economy. Still, despite being less than in 2022, the amount spent on everything from PCs, servers, IT security, and cloud deployments this year should go up by 4.4% and total $3.25 trillion.

Going deeper, investments by hyperscalers like Amazon (NASDAQ: AMZN ) and other cloud-related implementation projects should be more resilient, sometimes, at the expense of on-premises data centers. The reason for this is that as wage inflation remains high (compared to 2021) and setting up IT infrastructures implies more upfront investment, CIOs are more readily inclined to deploy applications in an as-a-service mode and pay only for what is consumed every month.

Now with a market cap of $349 million, Unisys is no hyperscaler like Microsoft nor a big IT service provider like Accenture ( ACN ). Instead, with a history as a server manufacturer with the Unisys brand and later on with Clear Path, I would rather compare it with International Business Machines ( IBM ) which also provides cloud services by partnering with hyperscalers.

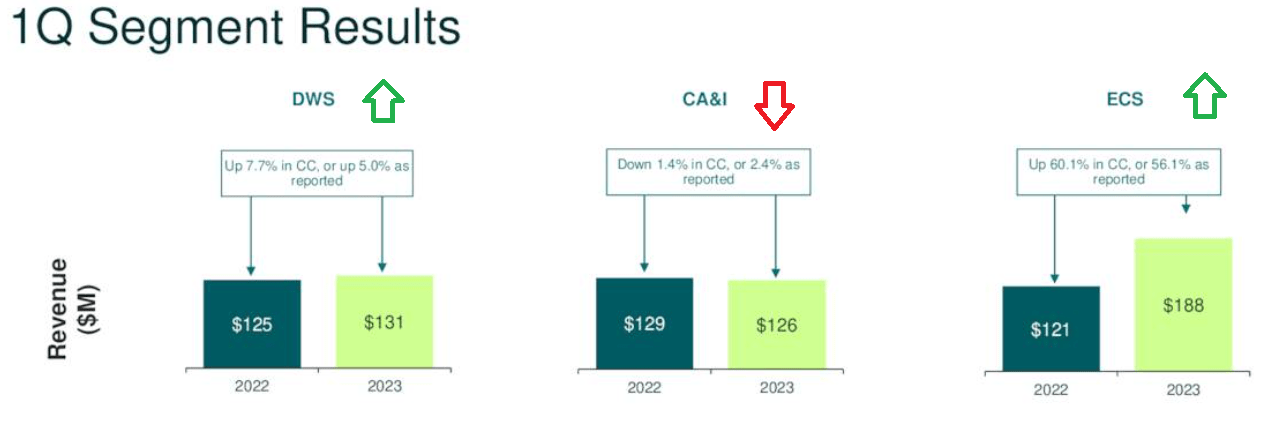

While Unisys does not have the scale of IBM, it also provides more or less the same category of services, in response to the post-Covid requirements for decentralized work environments as well as to cater for IT cybersecurity and analytics services. For this purpose, it is structured into three segments as shown below whose topline performances for the first quarter of 2023 (Q1-2023) are highlighted in green and red.

Q1 Results Earnings Call Presentation (seekingalpha.com)

{kind=link}

Going into details, as part of the DWS (Digital Workspace Solutions), it offers workspace solutions that saw a 5% YoY revenue growth attributed to new business wins, existing customers expanding their TCV (total contracts value), and price increases.

Weakness in Cloud and Competition

However, there was weakness in CA&I (Cloud Applications and Infrastructure), where sales regressed by 1.5%, which somewhat contradicts IDC’s optimism for this particular area of IT spending. This is partly explained by cautious spending by its financial services clients which contributed to more than 15% of the segment’s revenues in Q1-2023. However, going forward, the pipeline (or the dollar value of potential sales opportunities) for CA&I has increased by 17% on a sequential basis, but, for this to translate into more income, the company should execute deals, and this is what potential investors should be paying attention to during the earnings call in about two weeks' time.

Shifting to a positive note, there was strength in ECS (Enterprise Computing Solutions) which includes high-intensity computing and where sales increased by 60% YoY. As the largest segment accounting for $188 million (42%) of revenues in Q1-2023, it was mainly responsible for the 15.6% topline growth.

Looking at the industry, Unisys faces competition from system integrators and IT consultancies both in the U.S. and internationally. The reason is that the barrier to entry into everything from Infrastructure-as-a-Service to intelligent AI-as-a-Service or Analytics-as-a-Service has been lowered thanks to these being available through the cloud infrastructures of hyperscalers. Therefore service providers no longer have to invest tons of money in setting up infrastructure instead, they just need to partner up with hyperscalers to service their customers.

This also implies that to win new customers and generate sales, the company may have to sacrifice profitability, which is evidenced by the lower gross profit margins of 11.9% and 13% for DWS and CA&I respectively. This weakness is also explained by the charge Unisys incurred when subcontractors did not deliver according to performance. Still, margins are expected to improve as the company taps into lower-cost job markets and uses a higher degree of automation.

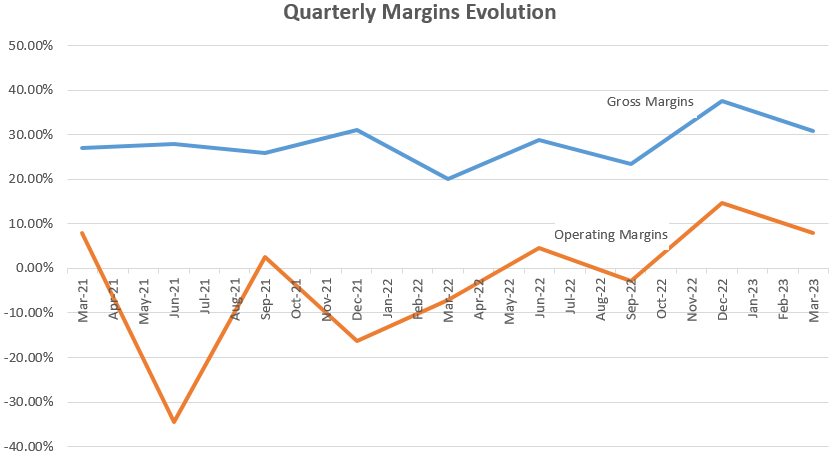

In this context, overall gross margins came out at 30.8% in Q1-2023 versus 19.6% in the prior year. This is also explained by the considerable weight of the ECS segment. Also, this segment's gross margin was 66.7% or an increase from 52.1% for the prior year's quarter. Therefore, if sustained, at the 30.8% level throughout subsequent quarters, margins could benefit with the blue chart further rising comfortably above the 30% mark. At the same time, this improvement could prop up the operating margins which have been mostly under the 10% threshold and even dipped below zero in the 2021-2022 period.

Chart Built using data from (seekingalpha.com)

{kind=link}

Therefore, progress has been made in managing costs on a quarterly basis, but, given its weight in both sales and margins, a lot depends on the performance of the ECS segment.

The ECS Segment, Regressing Sales but Stable Margins

Looking deeper into ECS, it includes Unisys ClearPath Forward Dorado mainframes which are custom-made servers for supporting high-volume transaction processing for the most demanding workloads. This is about number crunching and in this field, there are not many competitors , with two constituted by IBM's Z Systems or Fujitsu's (FJTSY) GS21. This means more pricing power for Unisys given that Dorado can also integrate with VMware's ( VMW ) virtualization software for private cloud solutions and can also be made available in a public cloud format.

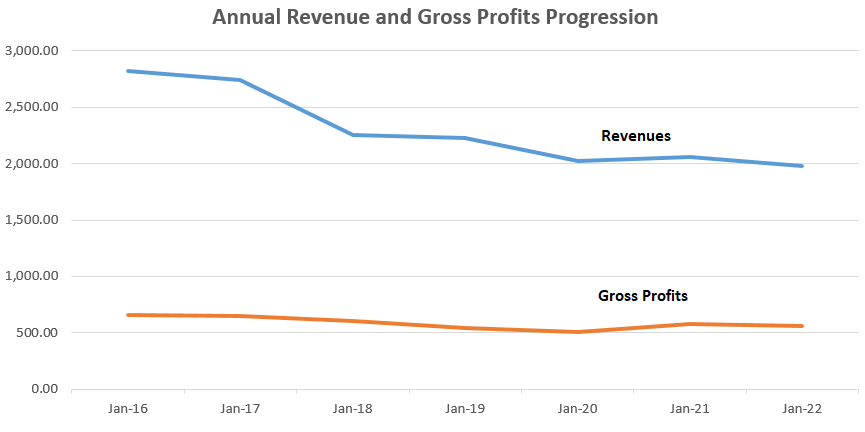

However, coming back to the possibility of the company again achieving the same degree of growth as in Q1-2023, this was largely achieved on the back of license and support revenues, and as per the executives, “renewals levels are expected to be lower on a YoY basis for the three remaining quarters”. Also, for the full year, they expect a revenue regression. If this projection materializes, it means that the blue chart below will continue on its downtrend.

Chart Built using data from (seekingalpha.com)

{kind=link}

However, on a more positive tone, the slight recovery in gross profits (as per the above orange chart) shows that the cost of revenues has been more contained as of 2021 and is probably due to the company starting to become choosy when selecting projects, with profitability in mind.

Moreover, with its cloud solutions, the company remains "well-positioned" to play a prominent role in artificial intelligence, data analytics, and cybersecurity. This has already enabled it to bag more contracts as well as expand upon existing ones, but, as I touched upon earlier, it is important to assess whether exposure to the financial sector continued to constitute an area of uncertainty for Q2-2023's financial results.

What to Look for during the Earnings Call

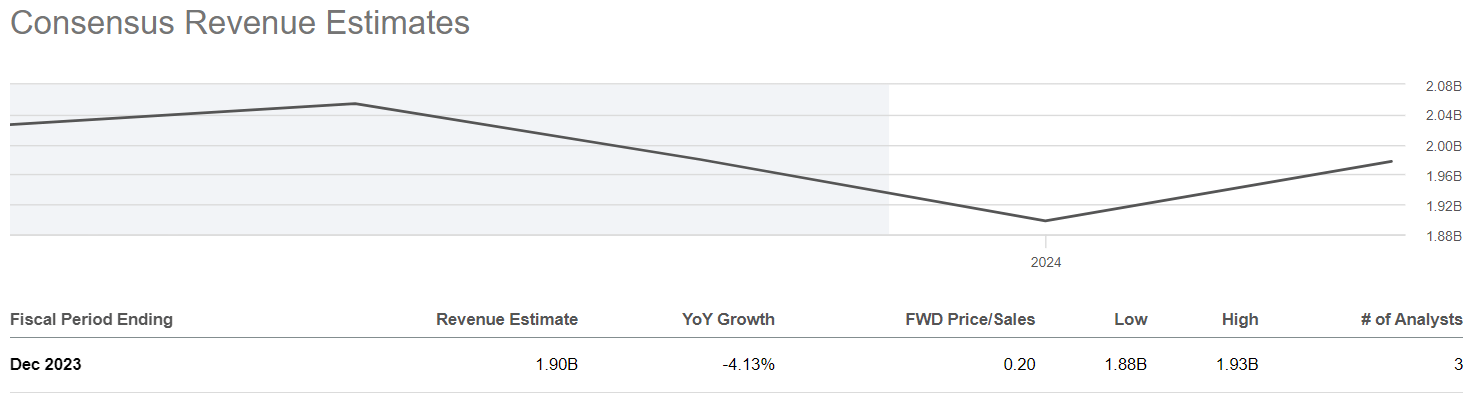

This is especially in a period when more interest rate rises by the Federal Reserve may adversely impact the current resiliency of the U.S. economy in general and the financial sector in particular. Consequently, any improvement coming from this sector and bagging AI-related contracts could translate into the reduction in YoY growth being less pronounced than the expected 4% .

Consensus Revenue Estimate for Fiscal Year 2023 (seekingalpha.com)

{kind=link}

Pursuing further, with its price-to-sales of 0.18x, it trades at a discount of nearly 94% relative to the IT sector. This explains my Hold position while the company improves its balance sheet given the debt-to-equity ratio of over 980% , which remains well above peers. In this respect, its net debt of $139.8 million at the end of Q1-2023 is less than the receivables of $461 million meaning that in case it is able to accelerate the pace of getting paid by customers for the work done, it can increase cash infusion in the business and reduce debt. For this matter, its cash and equivalents of $392 million imply less likelihood of requiring additional financing.

In conclusion, by going through the business segments, this thesis has shown that the exceptional revenues enjoyed in the first quarter are not likely to be replicated in the balance of this year. Still, due to favorable market positioning, AI could drive further growth, and one should be on the lookout for related sales during the next earnings call.

Along the same lines, given the company's emphasis on profitability, the use of machine learning within existing business processes could lower costs and, for this matter, any improvement in gross margins (which remain relatively stable as per the margin chart), could reduce the EPS loss of $-0.40 expected for the second quarter. Finally, in this regard, potential management comments relating to leveraging internal talent instead of relying on subcontractors or external hiring should be scrutinized.

For further details see:

Unisys: Revenue Constrained, Stable Margins, With AI Prospects