UIS - Unisys Sees Tepid 2023 While It Pursues Next-Gen Solutions Growth

2023-03-20 14:25:59 ET

Summary

- Unisys Corporation reported its Q4 2022 financial results on February 22, 2023.

- The company provides digital workplace and various cloud computing solutions to organizations worldwide.

- 2023 will continue to be a transition period as Unisys Corporation seeks to focus on higher-margin Next-Gen Solutions.

- I'm on Hold for Unisys Corporation in the near term.

A Quick Take On Unisys

Unisys Corporation ( UIS ) reported its Q4 2022 financial results on February 22, 2023, beating revenue and EPS consensus estimates.

The company provides a variety of enterprise software, computing and cloud infrastructure services to enterprises worldwide.

I view 2023 as a continued transition year, as management seeks to reorient the company toward growth in its Next-Gen Solutions while trying to keep L&S churn at a minimum.

For the time being, I’m on Hold for Unisys.

Unisys Overview

Blue Bell, Pennsylvania-based Unisys was founded in 1986 and provides a range of information technology solutions to organizations worldwide.

The firm is headed by Chairman and CEO Peter Altabef, who was previously president and CEO of MICROS Systems, president of Dell Services, and president and CEO of Perot Systems.

The company’s primary offerings include:

-

Digital Workplace Solutions

-

Cloud Applications and Infrastructure

-

Enterprise Computing Solutions.

The firm acquires customers through its direct sales and marketing efforts as well as through partner referrals and channels.

Unisys’ Market & Competition

According to a 2021 market research report by Grand View Research, the market for digital workplace solutions and software was an estimated $27.3 billion in 2021 and is forecast to reach $167 billion by 2030.

This represents a very strong forecast CAGR of 22.3% from 2022 to 2030.

The main drivers for this expected growth are increased demand for hybrid workplaces as the outbreak of the global pandemic forced many organizations to adopt more flexible working arrangements.

Also, the chart below shows the historical and projected future growth of the digital workplace market in the U.S.:

U.S. Digital Workplace Market (Grand View Research)

Major competitive or other industry participants include a wide variety of firms serving various market segments. An abbreviated list is shown here:

-

IBM

-

Accenture plc

-

Atos SE

-

Trianz

-

Capgemini

-

HCL Technologies

-

Infosys

-

Tata Consultancy Services

-

Mphasis.

UIS’ Recent Financial Results

-

Total revenue by quarter has proceeded with the following trajectory:

Total Revenue History (Seeking Alpha)

-

Gross profit margin by quarter rose sharply in the most recent reporting period:

Gross Profit Margin History (Seeking Alpha)

-

Selling, G&A expenses as a percentage of total revenue by quarter have trended lower in recent quarters:

Selling, G&A % Of Revenue History (Seeking Alpha)

-

Operating income by quarter has turned markedly positive in Q4 2022:

Operating Income History (Seeking Alpha)

-

Earnings per share (Diluted) have produced their first positive result in Q4 2022:

Earnings Per Share History (Seeking Alpha)

(All data in the above charts is GAAP.)

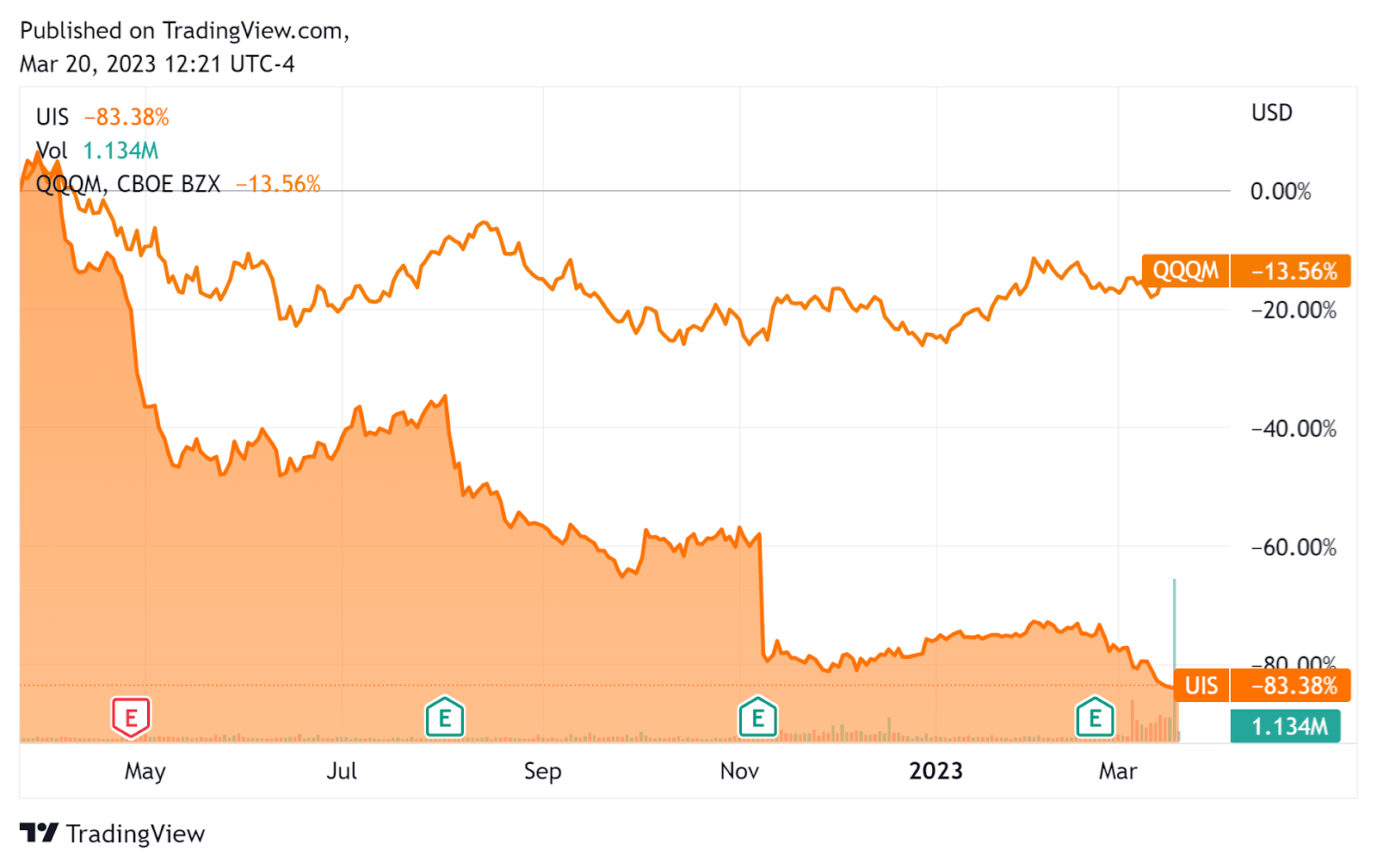

In the past 12 months, UIS’s stock price has fallen 83.4% vs. that of the Nasdaq 100 Index’s drop of 13.6%, as the chart indicates below:

{kind=link}

As to its Q4 financial results, total revenue rose 3.3% year-over-year and gross profit margin jumped seven percentage points to 38%.

Operating income turned sharply positive, as did earnings per share.

For the balance sheet , the firm ended the quarter with $391.8 million in cash and equivalents and $495.3 million in long-term debt.

Over the trailing twelve months, free cash used was $18.3 million, of which capital expenditures accounted for $31.0 million. The company paid $20.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For UIS

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 0.2 |

| Enterprise Value / EBITDA |

| 3.7 |

| Price / Sales |

| 0.1 |

| Revenue Growth Rate |

| -3.6% |

| Net Income Margin |

| -5.4% |

| GAAP EBITDA % |

| 6.2% |

| Market Capitalization |

| $231,910,000 |

| Enterprise Value |

| $445,410,000 |

| Operating Cash Flow |

| $12,700,000 |

| Earnings Per Share (Fully Diluted) |

| -$1.57 |

(Source - Seeking Alpha.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

UIS’ most recent GAAP Rule of 40 calculation was 2.5% as of Q4 2022’s results, so the firm is in need of significant improvement in this regard, per the table below:

| Rule of 40 - GAAP |

| Calculation |

| Recent Rev. Growth % |

| -3.6% |

| GAAP EBITDA % |

| 6.2% |

| Total |

| 2.5% |

(Source - Seeking Alpha.)

Future Prospects For UIS

In its last earnings call ( Source - Seeking Alpha ), covering Q4 2022’s results, management highlighted the "macroeconomic and geopolitical uncertainty" against which the firm contended during all of 2022.

Management believes their approach to transitioning to higher margin software products "is working."

Leadership is focused on growing its non-L&S offerings, which it broadly lumps into what it calls "Next-Gen" solutions.

In total, in Q4 2022, its next-Gen Solutions TCV (Total Contract Value) "grew by more than 80% and ACV [Average Contract Value] more than doubled year-over-year."

Looking ahead, while its L&S business relationships are "sticky," management provided only tepid forward guidance, although it is entering 2023 from a better pipeline standpoint.

One question is whether the newfound operating profitability is just a one-off event due to cost-cutting initiatives or whether the company will be able to grow meaningfully in 2023.

Also, its defined benefit retirement plan funding requirements vary based on a variety of factors, including actuarial assumptions, investment returns and ‘very specific and complex IRS funding rules.’

But, "currently, no cash contributions for these pension plans are expected for 2023 and 2024."

Despite this happy forecast, its large L&S segment "will be challenged" in 2023, although the company says that 90% of its L&S revenue has a customer retention rate of "95% plus."

So, I view 2023 as a continued transition year for Unisys Corporation as management seeks to reorient the company toward growth in its Next-Gen Solutions while trying to keep L&S churn at a minimum.

For the time-being, I’m on Hold for Unisys.

For further details see:

Unisys Sees Tepid 2023 While It Pursues Next-Gen Solutions Growth