X - United States Steel: Iron Hot As Rumors Of A Buyout Fuel The Flames Of Speculation

2023-12-14 02:35:27 ET

Summary

- United States Steel Corporation is receiving multiple bids valuing the company at over $40 per share, representing a premium of about 23% compared to the initial offer made by Cleveland-Cliffs.

- ArcelorMittal is rumored to be offering an all-cash deal with a bid of up to $45 per share, a 38.3% premium over Cleveland-Cliffs' initial offer.

- Steel Dynamics is also a top contender, with high profitability and the ability to generate significant synergies from United States Steel's assets, making this potential tie-up interesting.

When it comes to investing, I truly do believe that a contrarian approach is more often than not the best in the long run. But this is not always the case. Sometimes, going with the flow can be incredibly profitable. A great example of this so far can be seen by looking at United States Steel Corporation ( X ). Back in August of this year, news broke that competitor Cleveland-Cliffs ( CLF ) was willing to acquire the firm in exchange for $32.53 per share, valuing the business at $9.50 billion on an enterprise value basis. It didn't take long for the management team at United States Steel to shut down the offer as being inadequate. But the firm did make clear that it was interested in strategic alternatives and that it would begin accepting offers from potential suitors.

A short time after that occurred, I opened a small but speculative long position in the stock. I had a little cash left over at that time and felt that a speculative M&A candidate would be a better place to have the money than a high-yield account earning less than 6% per annum. As time went on, I became more confident that something would occur that would boost the share price of United States Steel. And in anticipation of that special something, which I was certain would take the form of a buyout, I added significantly to my position. Fast forward to today, and I am up about 19.8% on my stake in the firm. The share price’s move higher, combined with my decision to continue building a stake in the enterprise whenever the stock pulled back, has led to United States Steel bringing my second largest holding representing 15.7% of my overall portfolio. Since the publication of that article , the S&P 500 is up a meager 6.1%.

Now, it seems as though we are rapidly approaching the moment of truth. We understood weeks ago that there were multiple bidders interested in acquiring United States Steel or making some sort of major transaction with it such as a purchase of some assets. Allegedly, the Board of Directors of the firm with slated to meet on December 13th, though that did not necessarily mean that an announcement would be made shortly thereafter. In my view, a deal will definitely be announced. And while there are reasons why Cleveland-Cliffs would want to purchase up the enterprise, I would argue that there are two other companies that would be more likely candidates to come out on top if they are willing to pay the price.

The big picture

As of this time, nobody knows exactly what will transpire except perhaps a select few who are involved in the picture. But currently, there are rumors that United States Steel has received multiple bids valuing the company in excess of $40 per share. To put this in perspective, this represents, at the low end, a premium of about 23% compared to the initial offer made by Cleveland-Cliffs earlier this year. Supposedly, Cleveland-Cliffs is one of the companies still in the running, with its offer north of $40 and consisting of a combination of cash and stock. According to reporting, there might even exist a reverse termination fee that would demonstrate to the market the confidence of management that the transaction will clear any antitrust hurdles. But this isn't the only firm that is rumored to be in the mix.

Another leading contender is ArcelorMittal ( MT ), which is supposedly offering an all-cash deal. The rumors circulating are that it has financing in place to bid up to $45 per share. That would be a 38.3% premium over the initial offer made by Cleveland-Cliffs back in August. There have been at least three other companies that have been mentioned in this process. One of these is Nucor Corporation ( NUE ) which, with a market capitalization of $40.5 billion, is nearly double in size to the next largest of the suitors. Though the rumor circulating is that it might only be interested in one particular asset. What this asset is could be anybody's guess. However, the current rumors circulating suggest that it might partner with Stelco ( STZHF ) in a transaction. And lastly, there is Steel Dynamics ( STLD ). But specifics regarding it and its potential level of interest have not been revealed.

If we are going to talk about the capacity to make a transaction, it's clear that Stelco on its own would be wholly inadequate to make any sort of deal happen. From a balance sheet perspective, it might actually be the healthiest of the players with cash in excess of debt totaling $250.3 million. This means it has a tremendous capacity to bring on debt. But with a market capitalization of $1.9 billion, it would essentially be absorbed by United States Steel instead of the other way around. Of course, if it does partner up with some other player to take away a piece of United States Steel, that could be interesting. But from everything that has been going on regarding the rhetoric and rumors, it seems as though United States Steel would be far more interested in a transaction involving the entire firm. So I would make the case that Stelco is currently the least likely of the five suitors to succeed in anything substantive.

{kind=link}

At first glance, Nucor actually makes a great deal of sense. Given its immense size, with the aforementioned $40.5 billion in market capitalization, the firm could easily absorb United States Steel. The company also has other things going for it as well. For instance, it is the only one of the five besides Stelco that has cash that exceeds debt. Admittedly, it's only by $50.5 million. But this means that the company could easily take on the debt needed in order to make a transaction happen. I would like to draw your attention to the table above. In it, you can see certain profitability metrics regarding not only the five suitors but also United States Steel.

Conceptually, Nucor has a lot to gain from buying United States Steel. Of the five firms, it has the highest net profit margin, the highest adjusted operating cash flow margin, and the highest EBITDA margin. This is based on trailing 12-month data ending as of the most recent quarter for each firm. And with the exception of Stelco, it has the highest return on assets and the highest return on equity. A big reason to acquire other competitors is to generate synergies. There can be revenue-related synergies and I have no doubt that exist here. However, most synergies take the form of cost reduction. Clearly, Nucor runs a tight ship and the firm has plenty of wiggle room from a profitability perspective between what United States Steel generates and what it generates to create potentially a lot of value for shareholders. To put this in perspective, a 1% improvement in the net profit margin for United States Steel would translate to an extra $182.5 million in net income. The same thing applies to adjusted operating cash flow and EBITDA. A 1% improvement in return on assets would be worth $209.4 million, while for return on equity, it would be $111 million. It wouldn't be unthinkable that the company may be able to squeeze a few percentage points out as time goes on.

{kind=link}

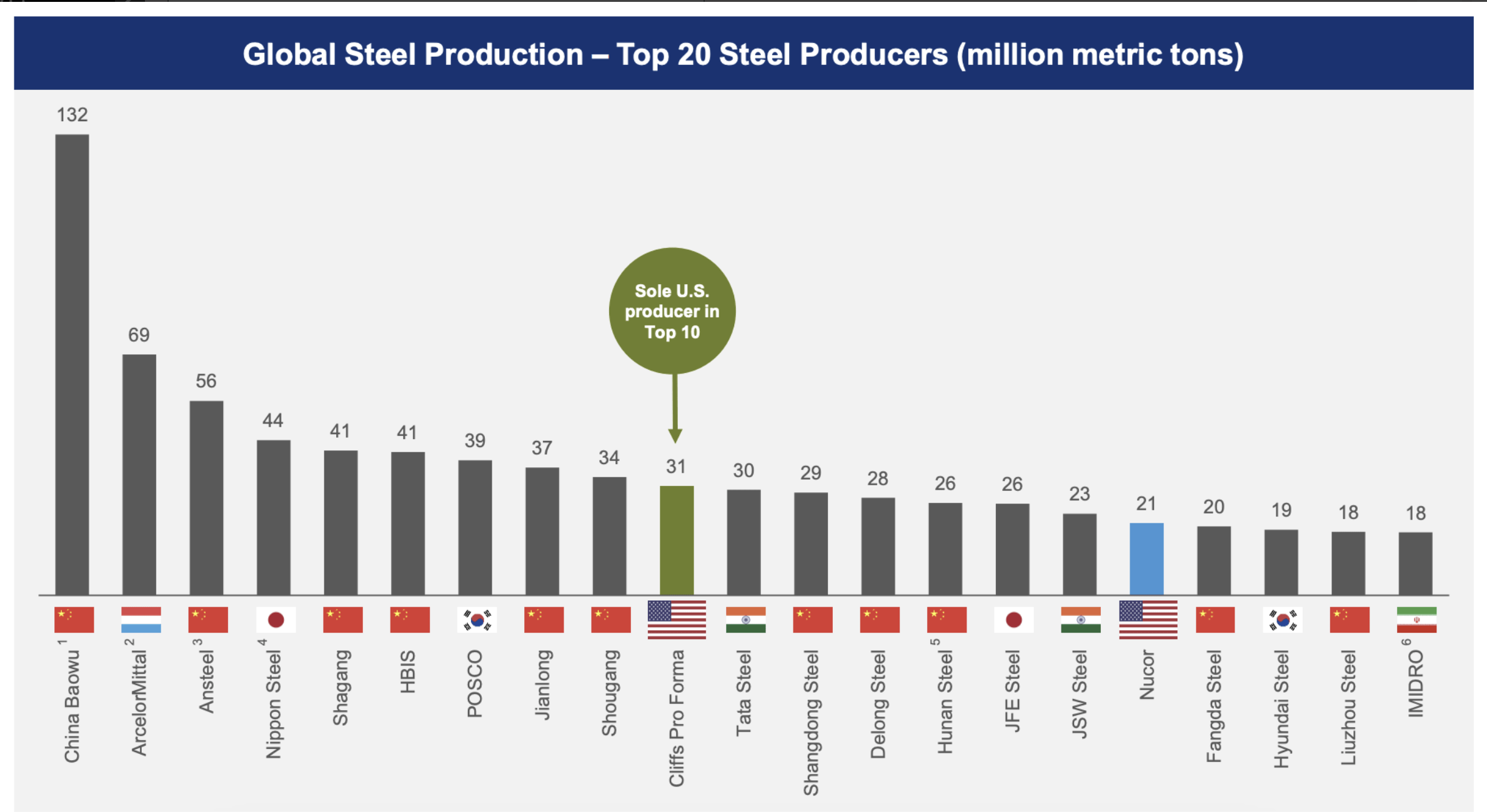

But there is one big problem with the idea of Nucor acquiring United States Steel. And that is its immense size. The business is already one of the 20 largest global steel producers on the planet. It's also the largest in the US, responsible for 21 million metric tons of output per annum. Combined, United States Steel and Cleveland-Cliffs would be responsible for 31 million metric tons, and when the offer from Cleveland-Cliffs came out regarding a potential transaction, it immediately set off alarm bells that the deal, if agreed upon, would face tremendous regulatory scrutiny. I'm not saying that a transaction between United States Steel and Nucor can't or won't happen. It could. But I would be awfully surprised if anything significant could occur on that front.

Filtering out those two firms, we are left with Cleveland-Cliffs, ArcelorMittal, and Steel Dynamics. I won't dig into any details regarding Cleveland-Cliffs because I feel like I have covered as much as I could for what information is publicly available in the article that I wrote about its offer back in August. A higher bid would likely mean lower synergies if it involves cash because of the debt the company would need to bring on in order to make that transaction possible. And of the five companies, Cleveland-Cliffs has the highest net leverage ratio at about 1.88. This is not outrageous, but it is high enough that I have to wonder about how attractive a much larger deal than what was initially expected would ultimately be. Of course, as the aforementioned table shows, you also have the fact that Cleveland-Cliffs is actually less profitable than United States Steel, so it might ultimately hope to piggyback off of the success of its target in order to boost its own margins. And that might be enough incentive to convince management to pay top dollar. You also have the union support behind it. But I don't think that's enough to solidify a transaction.

At the end of the day, this brings me to ArcelorMittal and Steel Dynamics. There are a couple of reasons why I think that ArcelorMittal might end up winning the prize. For starters, the high bid rumor so far is a $45 all-cash bid from it. There's no guarantee the rumor is true. But the fact that it's circulating suggests that the company is truly serious about a potential purchase. Second, United States Steel does have more attractive profit margins than ArcelorMittal does, so the company likely sees this as an opportunity to boost its own profitability by capturing synergies just like Cleveland-Cliffs did. However, because of how much closer profit margins are, it remains to be seen how much synergies could actually be realized. At this time, ArcelorMittal also has a much lower net leverage ratio than Cleveland-Cliffs does of 0.54. This gives the company a greater ability to take on debt in order to seal the deal. The firm also has about an extra $986 (minus $35 million that it donated) million that just came in from the sale of certain assets and Kazakhstan. However, some of that payment will occur over time. Though those who follow the company closely also understand that it is dealing with some issues involving that country because of a horrific incident that resulted in the deaths of 46 workers this October.

This is not to say that the company won't face any pushback from regulators. It very well could. In fact, the company is currently the second-largest steel producer on the planet, accounting for 69 million metric tons of output per annum. But its exposure to the US market is quite small. Only 11.1% of its revenue last year involved the US. That compares to 91.3% coming from Cleveland-Cliffs. In fact, Cleveland-Cliffs generates about 2.4 times the amount of revenue from the US market than ArcelorMittal does. So it might very well fare better from a regulatory perspective than a domestic player.

The other company that I think is at the top of the list is the one that has been perhaps the least discussed. Even rumors suggest that it might only be interested and may not have submitted a bid. And that firm is Steel Dynamics. The fact of the matter is that there are a lot of reasons why this particular candidate might make the most sense. It boasts the highest return on assets and the highest return on equity of any of the five companies that have been listed. It also has the second-highest net profit margin, adjusted operating cash flow margin, and EBITDA margin of the five. This means it has the potential to generate significant synergies from the assets of United States Steel. On top of this, the company has a rather high market capitalization of $18.5 billion, making it almost as large from that perspective as ArcelorMittal. Its net leverage ratio is a very modest 0.21, which means that it could easily take on debt needed to make the deal go through.

In addition to market size and capability, it also has a large set of operations. Based on data from last year, it has steel making and steel coating capacity of around 16 million tons. It's engaged in the steel recycling business and has made investments in other areas such as a $2.5 billion project that was announced in July of 2022 for the construction of a 650,000 metric ton aluminum flat rolled products mill in Mississippi. The company focuses especially on what it considers to be value-added products, which might go a long way toward explaining its impressive margins. Of course, it will face the same kind of regulatory scrutiny that Cleveland-Cliffs would. But when you consider its larger size and ability to make a transaction, plus its higher profitability, it seems to me to be a more logical prospect.

Author

Now, for those worried that a deal might not go through because of how high a price United States Steel might demand, I would say that any concern on this front is unwarranted. In the table above, you can see the implied equity value and the implied enterprise value of United States Steel at various buyout prices ranging from $35 per share all the way up to $50 per share. You can also see in the table below, using estimates for 2023, the price to earnings multiple, the price to operating cash flow multiple, and the EV to EBITDA multiple of the company at each of those buyout prices. That second table also shows the same trading multiples for each of the five firms that have been named as potential suitors.

{kind=link}

*Fundamental data from Cleveland-Cliffs , ArcelorMittal , Nucor , Stelco , and Steel Dynamics .

Cells that are highlighted in red indicate scenarios where those suitors are trading at levels outside of the range of pricing that United States Steel is trading at in the table. Cells that are highlighted in blue indicate scenarios where those firms have trading multiples within the range of what the table shows. And cells that are highlighted green show scenarios where firms are trading cheaper than what the range shows. I think it's also interesting to point out that the two leading candidates that I put forth are in an interesting position when it comes to this. For instance, ArcelorMittal is actually trading at multiples lower than this range. Generally speaking, it's undesirable for a company to acquire one that's more expensive than it is. But if we are talking about a transaction that is all cash, the leveraged nature of it, including the potential tax shield, could still make the transaction accretive. Steel Dynamics, meanwhile, is trading at levels within the range shown for two of the three metrics, so it wouldn't necessarily be out of the question for it to pay a similar price to what it's trading for or a slight premium if synergies warrant in order for a transaction to come through.

Takeaway

Based on all the data provided, I think that a deal involving United States Steel and one of its suitors is imminent. I'm glad I bought shares when I did and my only regret is not buying more. It's unclear who the winner will be. However, I would say that the two most likely candidates would be Steel Dynamics and ArcelorMittal in that order. I would place Cleveland-Cliffs in 3rd place, followed by Nucor and then Stelco in last. Regardless of who the buyer is, it does seem likely that additional upside is on the table. And because of how quickly this transaction will likely be announced, I would argue that the rapid short-term upside warrants a ‘strong buy’ rating for United States Steel.

For further details see:

United States Steel: Iron Hot As Rumors Of A Buyout Fuel The Flames Of Speculation