SPGI - Unveiling Moody's: The Untold Story Behind Berkshire's Investment

2024-01-18 12:54:58 ET

Summary

- The article delves into Berkshire Hathaway's investment in Moody's, tracing its evolution from a 15% ownership in 2000 to the present.

- I try to reverse-engineer Buffett's investment case in Moody's to see whether it still makes sense or not.

- Then, I explain my strategy regarding this stock.

Introduction

A promise is a promise. A few weeks ago, I shared my research on S&P Global ( SPGI ), but I actually explained how my research process started from reverse-engineering Warren Buffett's investment in Moody's ( MCO ). As some SA readers may know, I happen to spend a bit of my time studying Warren Buffett's main investments through Berkshire Hathaway ( BRK.A , BRK.B ). After sharing why Mr. Buffett invested in BNSF and calculating what returns Berkshire has earned from this investment so far, I feel it is time to look at another big investment of Berkshire in a completely different industry.

How Moody's Became Part of Berkshire's Portfolio

First and foremost, before we look at the company, let's look at how Moody's became part of Berkshire's portfolio. It all started after Moody's spun off of Dun & Bradstreet . At that time, Berkshire held 24 million shares, bought in late 2000 for $499 million. This translated into a total ownership of 15% of the company. In 2005 , Berkshire reported 48 million shares, or 16.2% of the company. Of course, the share count doubled due to a stock split. By the end of 2008 , due to yearly buybacks, Berkshire owned 20% of the company. A year later, in 2009, Berkshire was raising cash to buy BNSF. Therefore, it sold some of its stake in Moody's to pursue this new investment. This sale was criticized by many because, if considered it by itself, it seems a big mistake of Buffett's. In fact, Berkshire sold at a low and missed out on big gains. However, if we put this sale in the right context, Buffett did jump in on a big opportunity which did pay off. So, we should consider the opportunity cost of this sale and balance the missed gains with the earned ones.

In 2012, Berkshire reported a 12.7% stake in Moody's, with 28.4 million shares for $287 million, while the market value at that time was $1.43 billion. In 2013 , Berkshire trimmed its stake to 24.7 million shares, owning around 11.5% of the company.

Since then, Berkshire has not changed anything else to its stake. But still, the magic of compounding has produced its effects: on one side, Moody's buybacks have increased Berkshire's equity in the company; on the other, the stock has increased its value year after year. However, since 2013, neither in Berkshire Hathaway's annual reports nor in Warren Buffett's shareholder letters, do we read anything in particular about Moody's.

So, I went and read the transcripts of Berkshire's annual meetings to gather more insights into this investment. In 2000 , Buffett, for example, was asked what he thought about Moody's moat. This was his reply:

I would say that the moat is, just in our view, far wider, deeper, and infested with far more poisonous characters, in the case of Moody’s, than in the case of the operating company. We’ve had experience — just in terms of making decisions about how you either obtain credit information, in the case of the operating company, or if you want to obtain ratings on securities or something — I think you’d conclude that Moody’s is a much stronger franchise than the operating company.

And Charlie Munger added a few significant words: "Moody’s is a little like Harvard. It’s a self-fulfilling prophecy. You know, I hate to think of how much you could mismanage Harvard now and still have it work out pretty well".

In 2010, of course, Buffett was asked about his sale of Moody's shares and whether or not his investment case had changed. To this, he answered in the following way:

I would say this. The ratings agencies have had, and still have, under current conditions, an incredibly wonderful business. I mean, it takes no capital at all, you know, the pricing power is significant. And certain parts of the world feel they need rating agencies. [...] It’s not a business that we rely on, but we do recognize that if the sort of, the social model doesn’t change, it still remains a phenomenal business

Apart from these last quotes, I haven't been able to find much more. This makes sense because Mr. Buffett has often been quite reluctant when having to shed some light on his stakes in marketable securities.

And yet, though we would like to have more insights, two facts stand clear before us. First of all, our social and economic model makes it almost impossible for a business to escape paying its toll to Moody's; secondly, Moody's pricing power is immense.

So, after my analysis of Moody's main competitor S&P Global, here we are with a summary of my research on Moody's itself.

The company

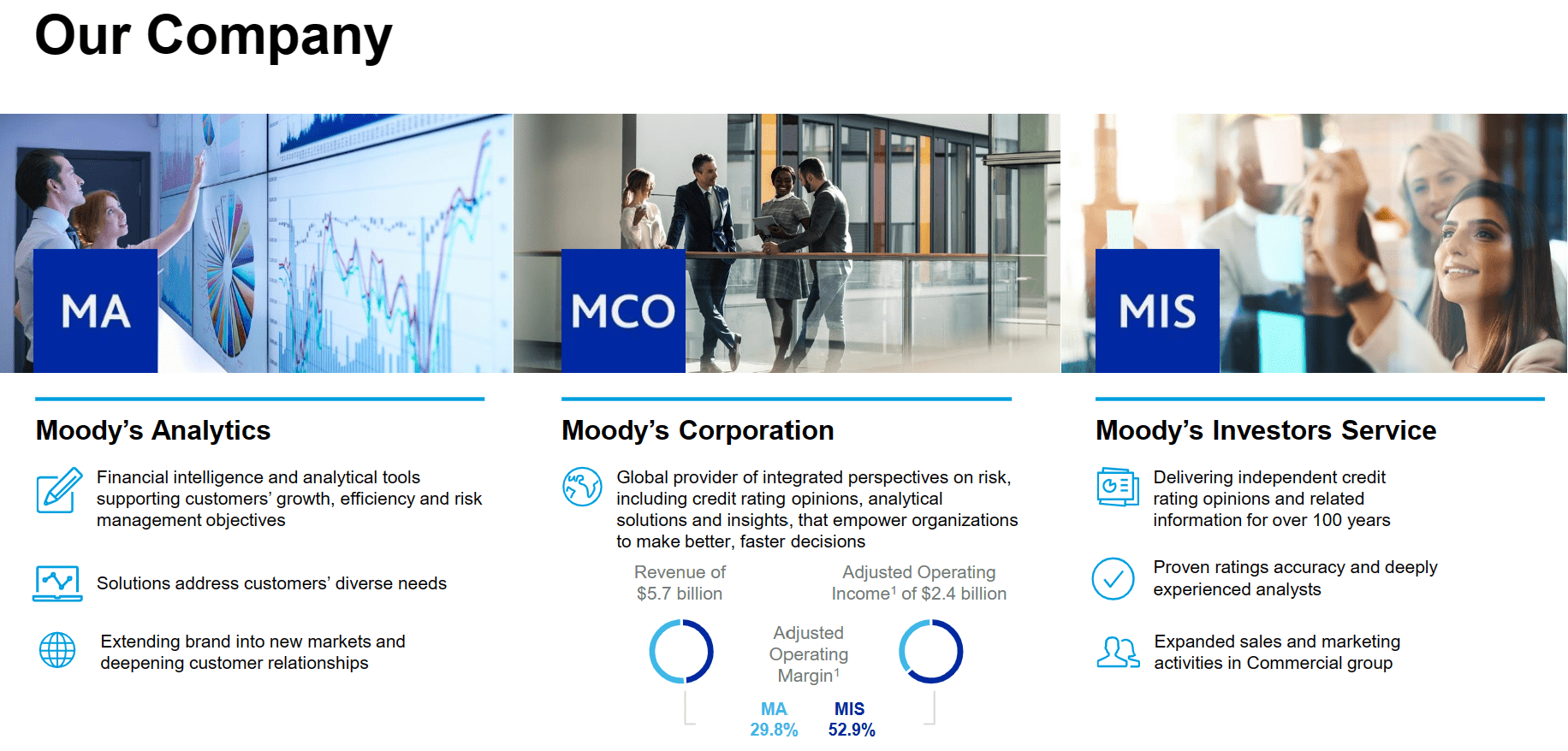

Let's start from the start. How does Moody's explain itself? In its last available annual report (the new one will be up shortly) we read the following company overview: "Moody’s is a global-integrated risk assessment firm that empowers organizations and investors to make better decisions. Moody’s reports activities in two segments: MIS and MA". MIS stands for Moody's Investors Service, while MA stands for Moody's Analytics, as we can see below.

{kind=link}

So, we have a surprise right away. We usually think of Moody's as a ratings agency, but in the way the company represents itself, there is no immediate mention of this activity.

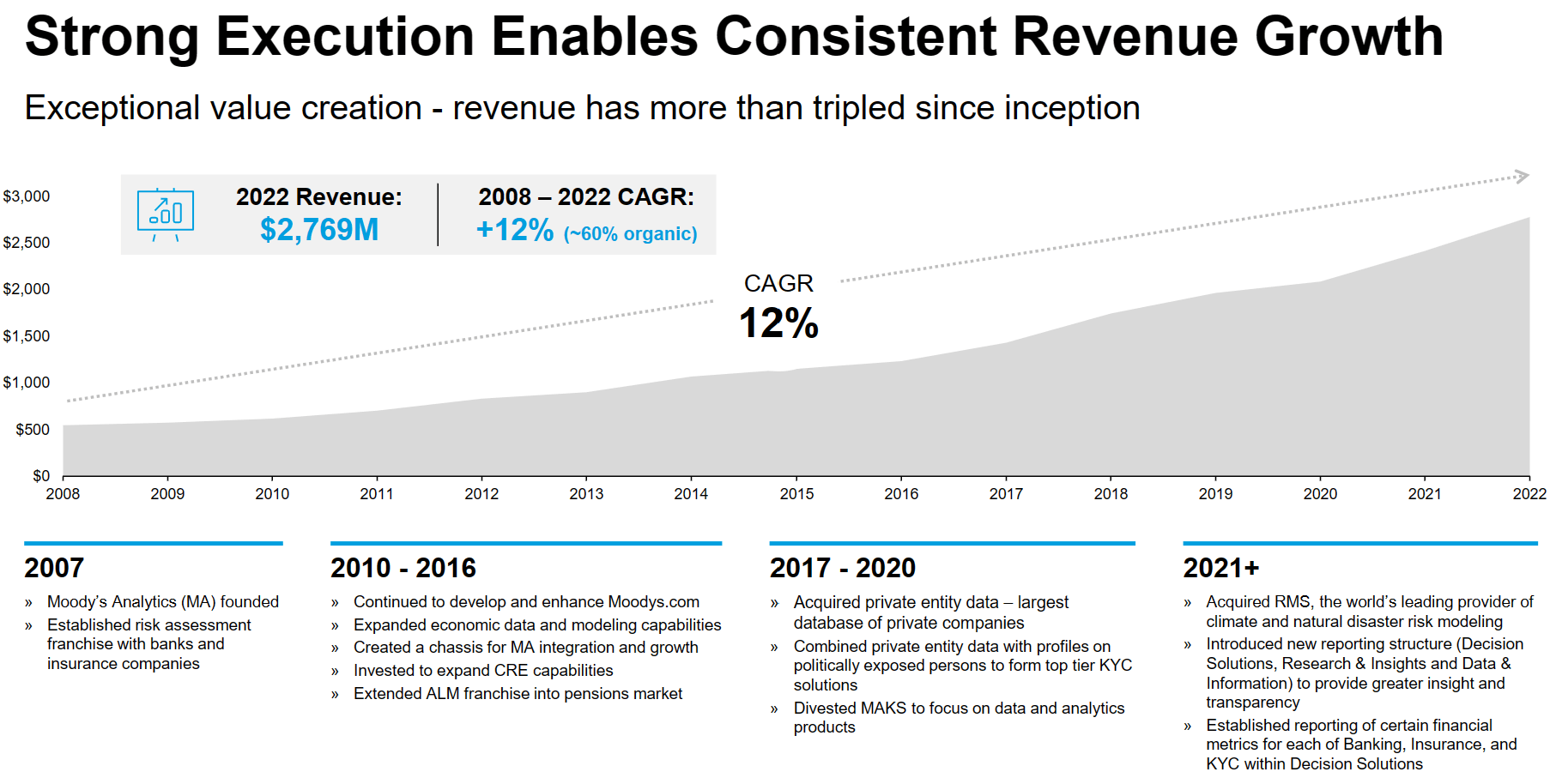

Why is that? Since 2007, Moody's started expanding beyond ratings, establishing MA, a risk assessment franchise serving at first banks and insurers. From 2017 to 2022 Moody's built out its data and analytics capabilities, complementing its risk management software business with private company information. Starting in 2023, Moody's wants to position itself to serve as wide a range of risk assessment markets as possible. What makes this accomplishment interesting is the proprietary data Moody's owns, which gives it a one-of-a-kind competitive differentiator.

If we sum up all of these steps, we see how Moody's has been able to continually foster its constant growth at a 12% CAGR since 2008. Quite remarkable for a company whose market cap is almost $70 billion.

{kind=link}

On the other side, MIS does indeed focus on credit ratings and assessment services on debt obligations.

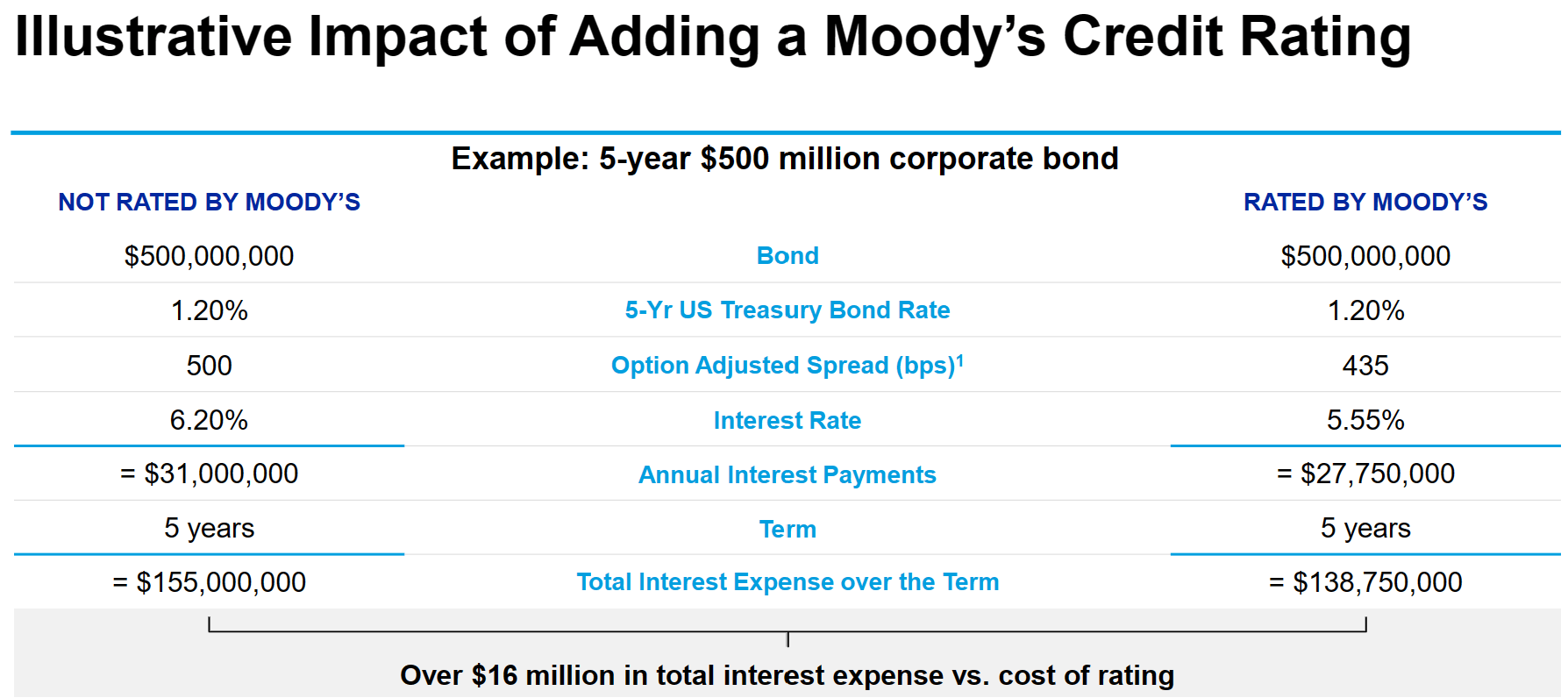

Now, one may wonder why a business needs to obtain a rating from Moody's. The answer is quite clear: a rating from Moody's facilitates access to debt capital at a lower interest rate. This leads to big savings in the long run. For example, as we can see below, a $500 million bond rated by Moody's sees an interest rate of 5.55%. The same bond would have an interest rate of 6.20% if not rated by Moody's. Over five years, this leads to more than $16 million of extra total interest expense, which is 3.2% of the money borrowed at first.

{kind=link}

Currently, MIS rates almost 34k organizations, for a total rated debt outstanding of $73 trillion. MIS prospects for growth are linked to strong secular trends, which include an expanding global GDP (the more it grows, the more debt issuance there will be), ongoing increase in refunding walls, and disintermediation of credit.

Going back to MA, whose business has grown in recent years, we have to think about it as a provider of data and information, research and insights, and decision solutions figured out to help customers navigate risks of any complexity. MA is a great business which really shows Moody's scale. While rating debt, Moody's acquires a lot of information, which then can be re-assembled and analyzed to assess risks with an expertise almost no one can match. As a result, MA leverages MIS's proprietary data and delivers new solutions to its customers. In addition, MA runs on a subscription-based model, generating recurring revenue with little sensitivity to cyclical changes in debt issuance volumes. MA currently has over 15k customers and operates in more than 165 countries. As of Q3 2023 , MA produces over $300 million of annualized recurring revenue.

MA, on its side, is a compounding machine thanks to a few factors such as strong customer retention rates, cross-selling, upgrades and pricing, continued SaaS transition, and increased distribution capacity.

Another factor to consider about the company's health comes from a quick look at its executive officers. They have all spent a long time at Moody's. This means the company is able to grow its talents up to the point it doesn't need executives from outside.

If we look at Moody's global revenue ($5.5 billion at the end of FY 2022), we see how it is almost evenly split between the U.S. and non-U.S. customers. This gives quite a bit of geographical diversification to Moody's revenues. Moreover, almost 70% of Moody's revenues are recurring, with the remaining 30% falling under the transaction category.

MCO 2022 Annual Report

As far as Moody's revenue stream goes, around 56% of it comes from MIS, while the rest comes from MA.

Moody's is also a very capital-light business. Its operating expense is about $1.6 billion, which amounts to less than 30% of the company's revenues. Adding up another $1.5 billion of SG&A expense, we find out that Moody's runs its business with an operating margin of 34.4%, which is considered very low by the company.

Please consider what I have just written: Moody's is a company that thinks a 34.4% operating margin is low. There are companies whose best operating margin is not even a double-digit one!

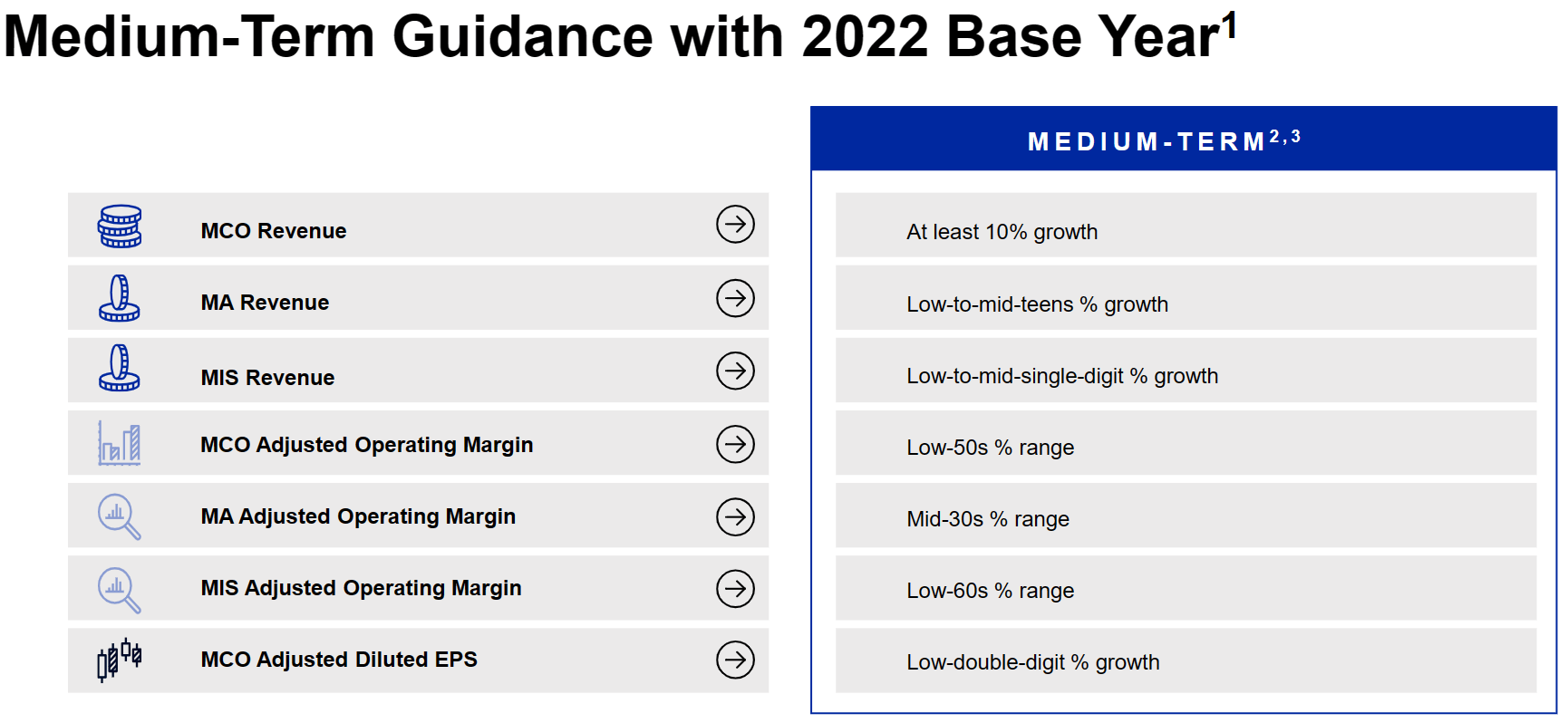

What's even more interesting is that Moody's is not shy about its future goals. The company expects to keep growing at least 10% per year, with margins between the mid-30s and the low-60s, depending on the business segment.

{kind=link}

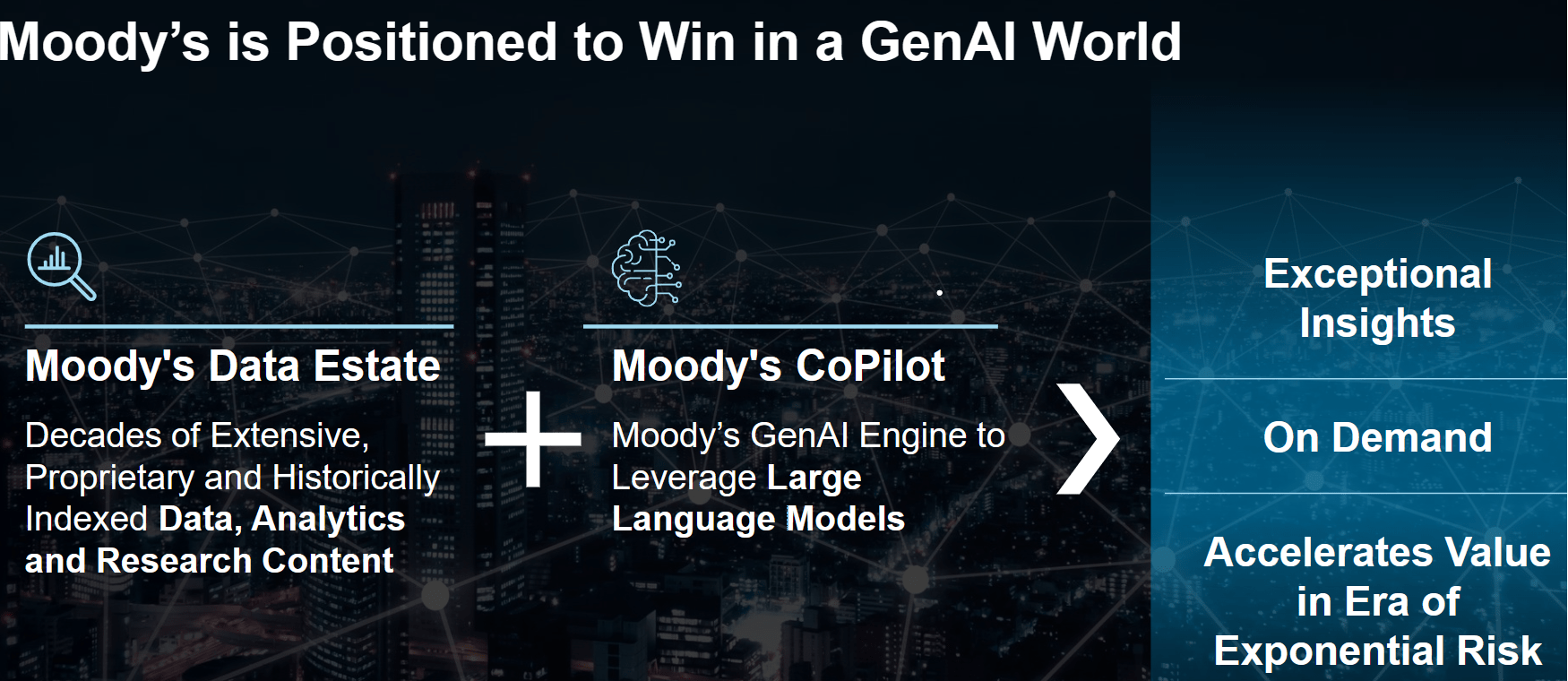

On top of this, we need to consider how Moody's runs a business bound to win as AI develops and becomes part of our lives.

In fact, as Moody's shows below, the company is positioned to win in this major shift because Moody's owns data, analytics, and research content which can be screened through Moody's CoPilot.

{kind=link}

All in all, Moody's shows itself as a true powerhouse, protected by a huge and ever-growing moat.

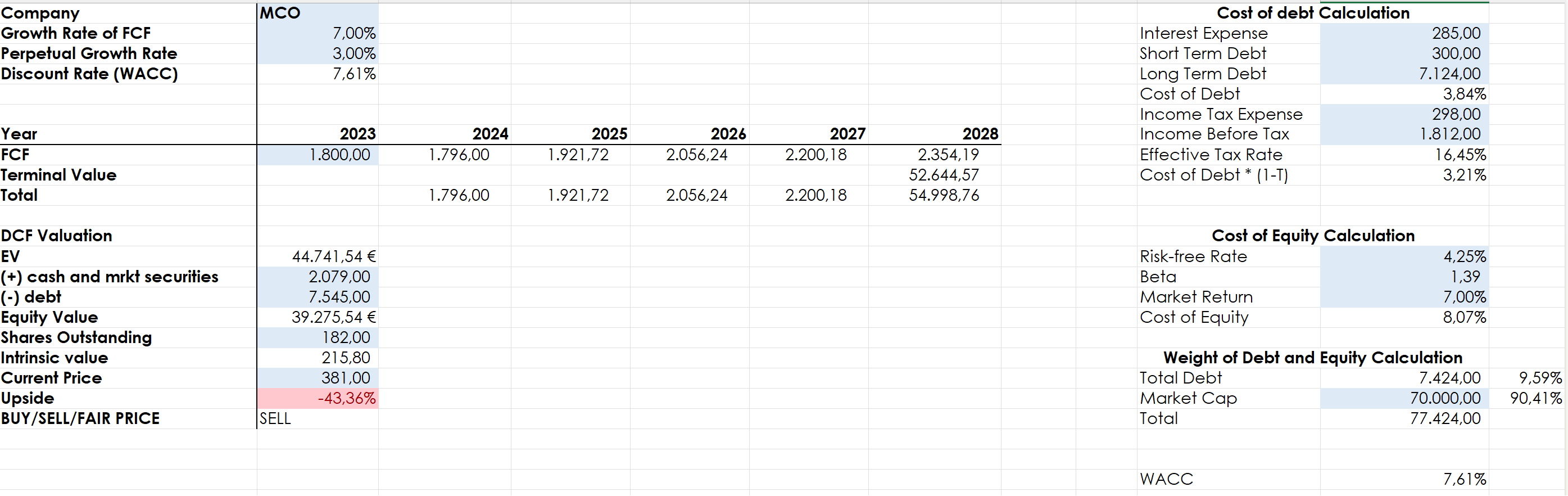

If I run my discounted cash flow model, assuming a FCF growth rate of 7% for the next five years and plugging in the latest TTM financials, this is what I get.

{kind=link}

The result is that Moody's seems to be overvalued. However, as I tried to explain above, Moody's premium may well be justified due to its incredible moat and its enduring pricing power. No doubt, Moody's is a wonderful business. But its current share price, though not insane, is not exactly a fair price.

After all, the stock does currently trade at a forward PE of 38 and a forward P/FCF of 34.5. These metrics do confirm Moody's is a bit expensive right now.

So, while I have it on my watchlist, I am not currently going to initiate a position. Yet, I believe every investor seeking high-quality companies whose compounding trajectory is clear should keep a close eye on this stock. In case of a sudden drop or a dip, this is one of the first ones to buy.

For further details see:

Unveiling Moody's: The Untold Story Behind Berkshire's Investment