LHX - Up To 50% Undervalued - Why L3Harris Has Become My Favorite Dividend Growth Stock

2023-09-06 05:56:47 ET

Summary

- I've recently increased my L3Harris Technologies position by 55% due to my strong belief in its undervaluation.

- The challenges faced by L3Harris are primarily external, such as supply chain issues and inflation, rather than internal performance issues, as indicated by its robust backlog and revenue guidance.

- With diverse business segments, high space exposure, and the potential for aggressive dividend growth, L3Harris is my top choice for a dividend growth stock.

Introduction

I wasn't planning on writing this article. However, recent developments and a re-assessment of my investment have caused me to increase my L3Harris Technologies (LHX) position by 55%.

On July 27, I wrote an article titled L3Harris Has Become A Strong Buy After Stellar Q2 Earnings . Since writing that article, the stock has fallen roughly 7%, resulting in me to re-assess my view.

The conclusion of my re-assessment is why I'm writing this article.

I believe that LHX is up to 50% undervalued based on a number of factors.

Not only is the company benefitting from rising global defense demand and easing supply chain issues, but it is also positioning itself for outperforming growth in space, the go-to segment for the next few decades.

Thanks to a number of strategic M&A deals like the takeover of Aerojet Rocketdyne, the company is a huge player in the space segment.

While the market is ignoring LHX due to (somewhat justified) inflation fears and (related) ongoing pressure on margins, I believe the market is presenting us with one of the best opportunities I've seen since the pandemic wrecked the stock market in 2020.

Hence, I added 55% to my LHX position, making it one of the largest investments in my portfolio. I also bought it for several portfolios that I advise.

In this article, I'll update my thesis and explain why LHX is currently my favorite dividend growth stock.

So, let's dive in!

Why L3Harris Is Struggling

Throwing good money after bad money is one of the biggest risks on the stock market. For example, a lot of people were convinced that certain crypto coins or nonfungible tokens were the future. It resulted in a massive disaster for a lot of retail investors.

The same goes for a wide range of overhyped investments like fake meat companies, high-flying tech stocks, or companies that simply lost their competitive edge.

So, my strategy to become an even more aggressive buyer once my favorite stocks show weakness can only excel if I'm a good stock picker.

Given that I mainly focus on proven dividend growth stocks, I eliminate a lot of risks. I eliminate even more risk when I can identify why certain stocks are down.

For example, in 2020, I was an aggressive buyer of energy stocks. All the good stocks were down as if the world was ending. However, that was caused by the obvious pandemic and overblown fears that fossil fuels might be a thing of the past.

What followed was higher economic growth, a vaccine, and evidence that oil demand isn't going anywhere.

The L3Harris situation is different, yet a bit similar.

All evidence suggests that L3Harris is not down because of poor earnings or management making poor decisions. There's no data that backs up the thesis that LHX has serious issues.

No. L3Harris is down because of a mix of factors it cannot impact.

As I explained in the aforementioned article, LHX is firing on all cylinders - at least when it comes to its topline.

In the second quarter, its orders rose by 17%, pushing its total backlog to $25 billion. The company has a funded book-to-bill ratio of more than 1.0x in every single segment, with Communication Systems seeing a 1.38x book-to-bill ratio. Please note that this indicates that for every $1.00 in finished work, the company gets $1.34 in new orders.

L3Harris Technologies

Thanks to these developments, the company raised its revenue guidance across the board. It also hiked operating income guidance in two of its three segments.

L3Harris Technologies

This is what the company said with regard to the IMS segment, which saw lower operating income guidance:

This, along with some operational challenges on fixed price development programs at a couple of our remote sites permeated and had an impact within the quarter. Jon Rambeau and our IMS team are addressing these issues. They are predominantly related to talent and learning loss inefficiencies and we expect the results of these actions to have a positive impact as we progress towards the end of the year. - LHX 2Q23 Earnings Call

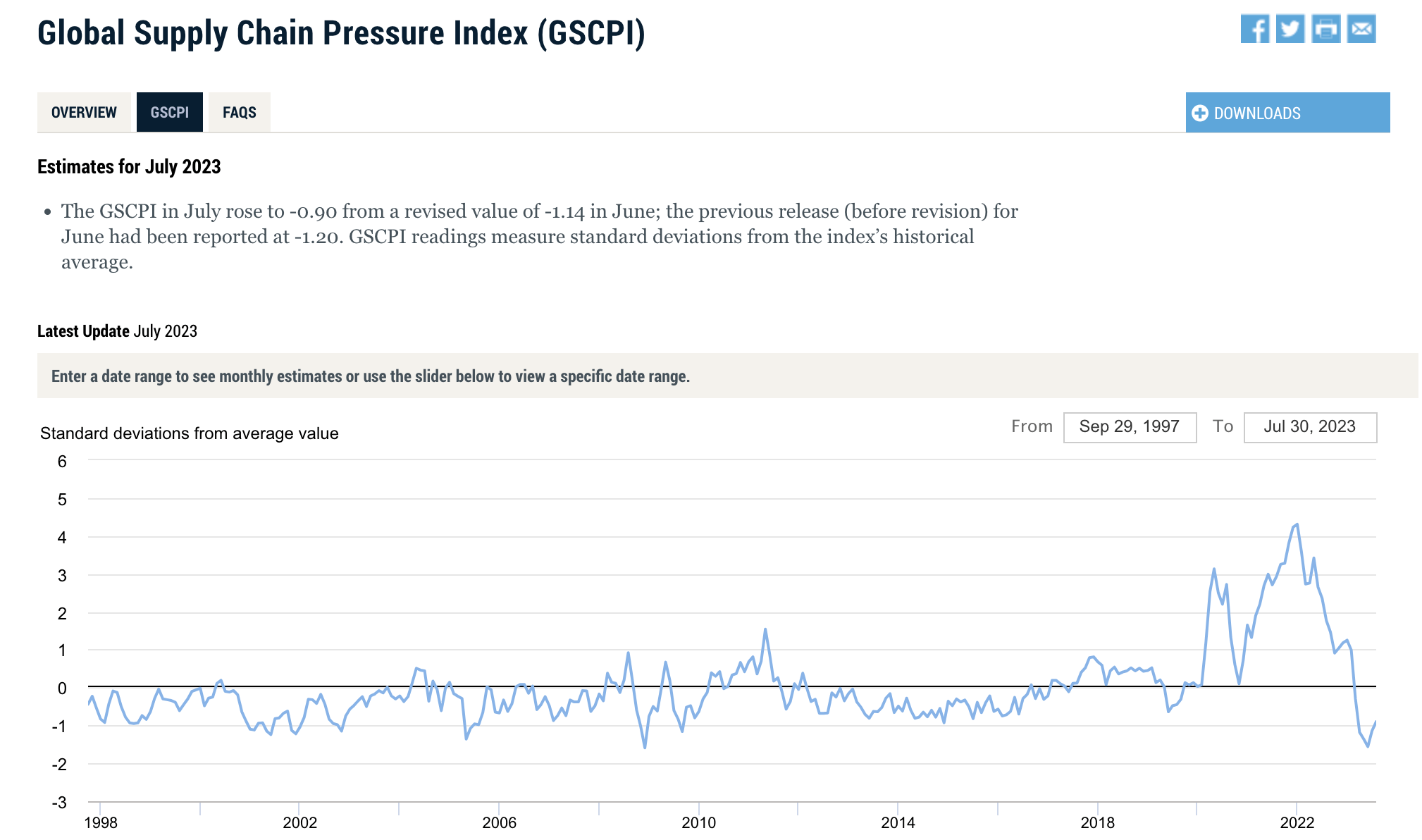

The good news is that supply chain issues are quickly fading.

Using New York Fed data, we see that the Global Supply Chain Pressure Index has normalized. While some high-tech components still see shortages, I expect that defense companies will see full normalization in early 2024.

Federal Reserve Bank of New York

{kind=link}

I would even make the case that a recession would accelerate that process, as defensive giants will have less competition for certain supplies if cyclical companies reduce procurement spending.

Inflation, unfortunately, remains an issue. As most of my readers will know, I've been in the group that expects sticky inflation to last for a long time.

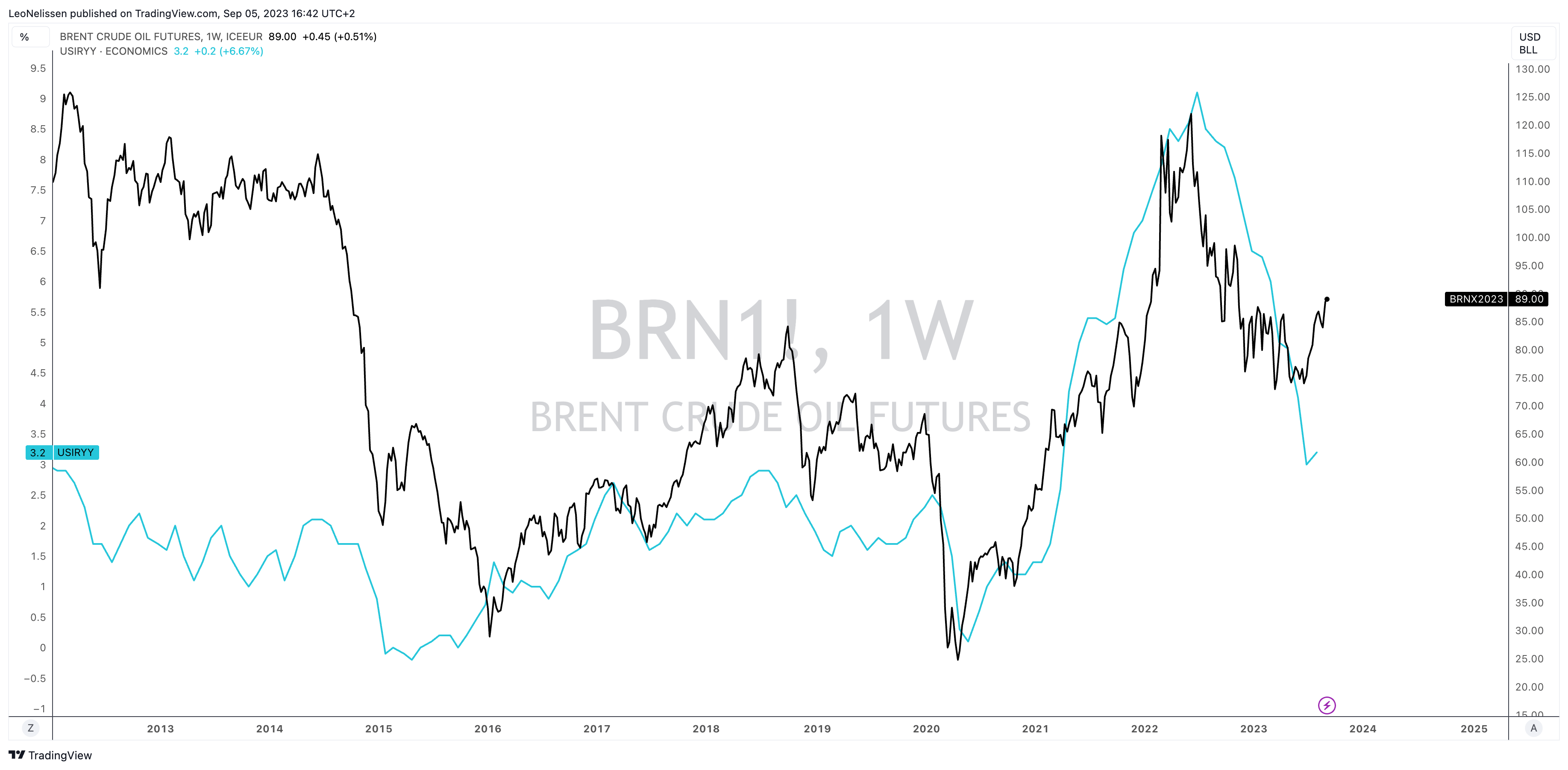

Right now, we're seeing rising oil prices, with Brent crude oil closing in on $90 again.

This is very inflationary, as the comparison between oil and year-on-year inflation below shows.

TradingView (ICE Brent, Y/Y Inflation)

{kind=link}

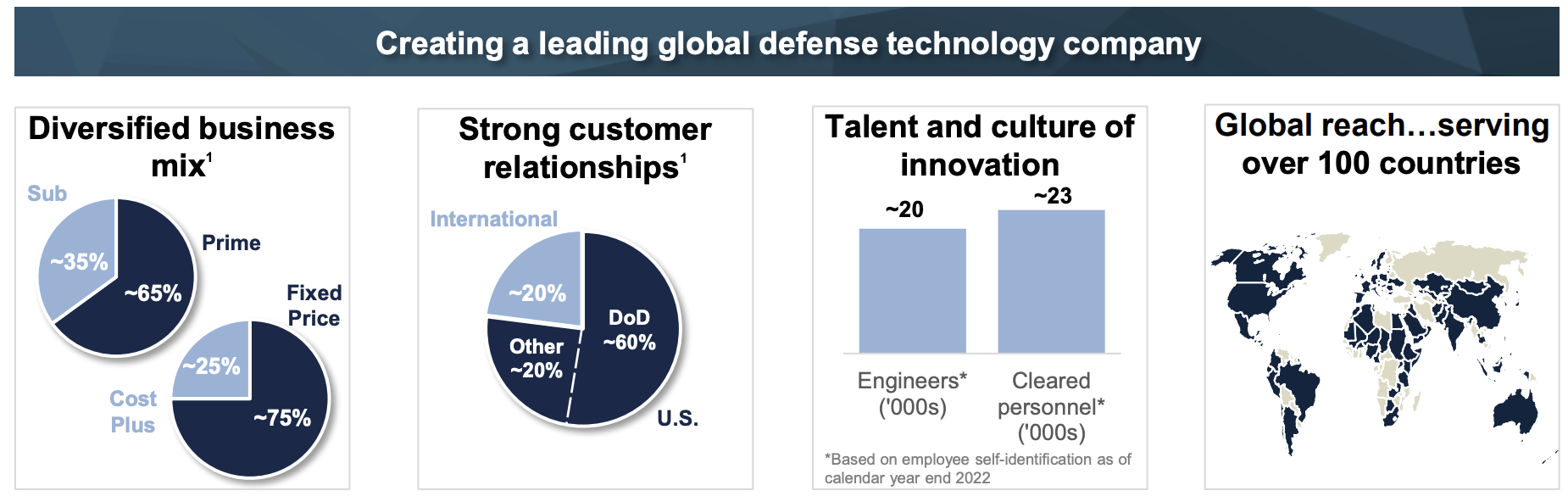

As we can see below, 75% of the company's contracts have a fixed price. This is less-than-perfect for an inflationary environment.

{kind=link}

With regard to these pricing issues, the company says that it is taking actions, like selective bidding (emphasis added):

They have a lot of fixed price contracts , probably some fixed price development programs, which I think I've publicly said we're really going to be selective on bidding going forward , especially when the customer is asking for a fixed price production or low rate production , simultaneous with development, that's just bad business and makes no sense and we're going to continue to push back and not bid those because very hard to price something that you haven't developed. - LHX 2Q23 Earnings Call

The good news is that fixed pricing isn't the end of the world. The government knows that it needs to use defense spending to adjust for inflation. After all, if it neglects to incorporate inflation protection in fixed-price contracts, it could seriously hurt the stability of the defense supply chain - as weird as that may sound given the size of the defense budget.

While the defense budget is steadily rising, one major issue is the inconsistency and risks of continuing solutions until spending agreements have been reached. When adding persistent inflation, investors tend to ignore companies like LHX.

{kind=link}

According to the U.S. Department of Defense:

" Support for the top line is great ," McCord said. "Timing and timeliness of that support matter just as much. One thing that is not so great is this pattern of recurring, lengthy, persistent, continuing resolutions . These negatively impact our mission."

[...] "It's also our job to continue to help remind people and enable our service chiefs and secretaries to remind people on the harm that this dynamic does for us ," he said. "And speaking of communicating, we can't succeed if we're not communicating with Congress - both our priorities and hearing their concerns, not just ... transmitting. We have to listen."

While the mix of budget uncertainty and sticky inflation isn't great, it comes with a great valuation and plenty of long-term potential.

Why I Like LHX So Much

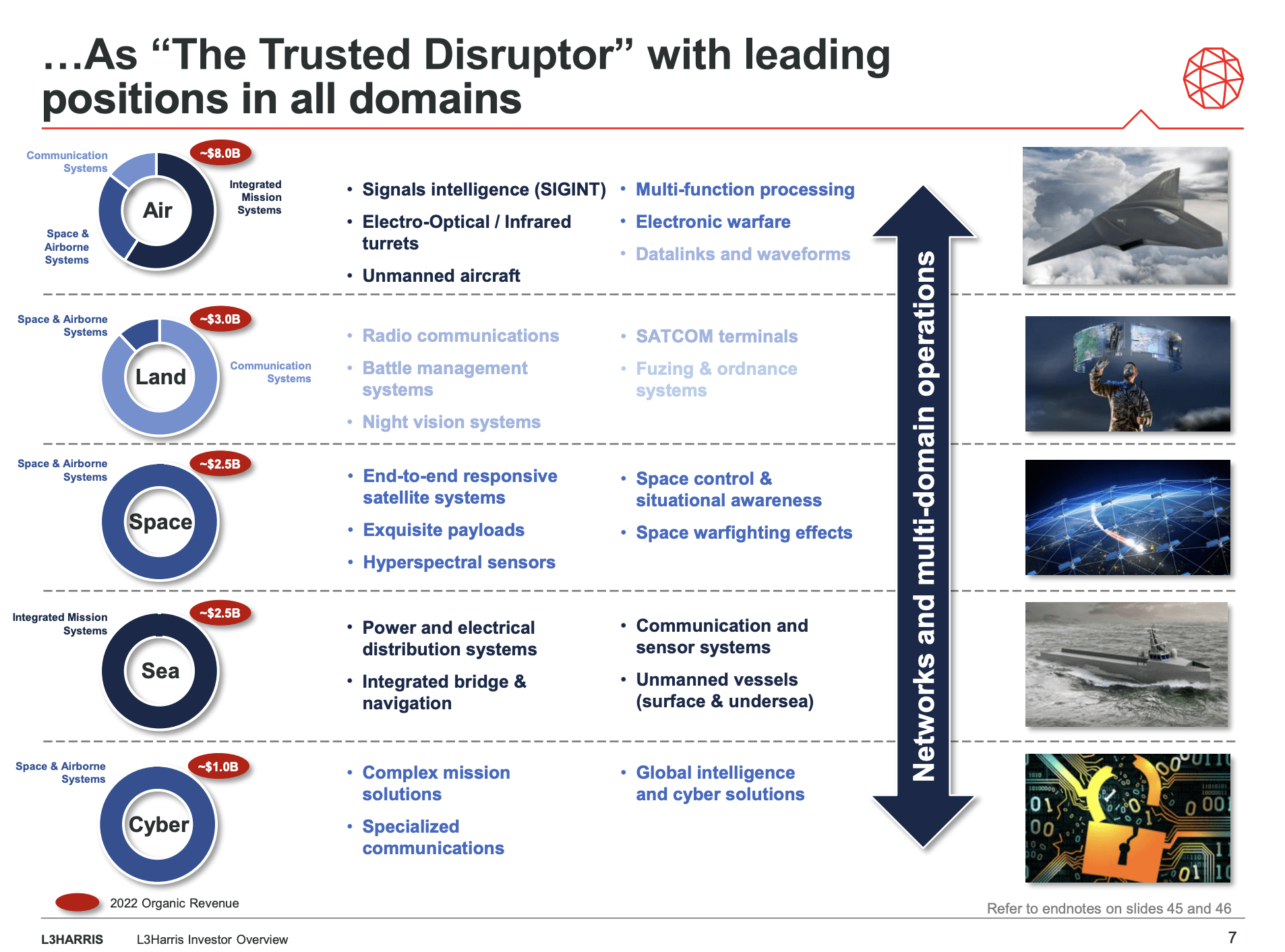

Despite current struggles, L3Harris is one of the best-diversified defense contractors. The company has three strong business segments that give the company leading positions in all domains. This includes air, land, space, sea, and cyber. The company's products and services in these domains are almost countless.

{kind=link}

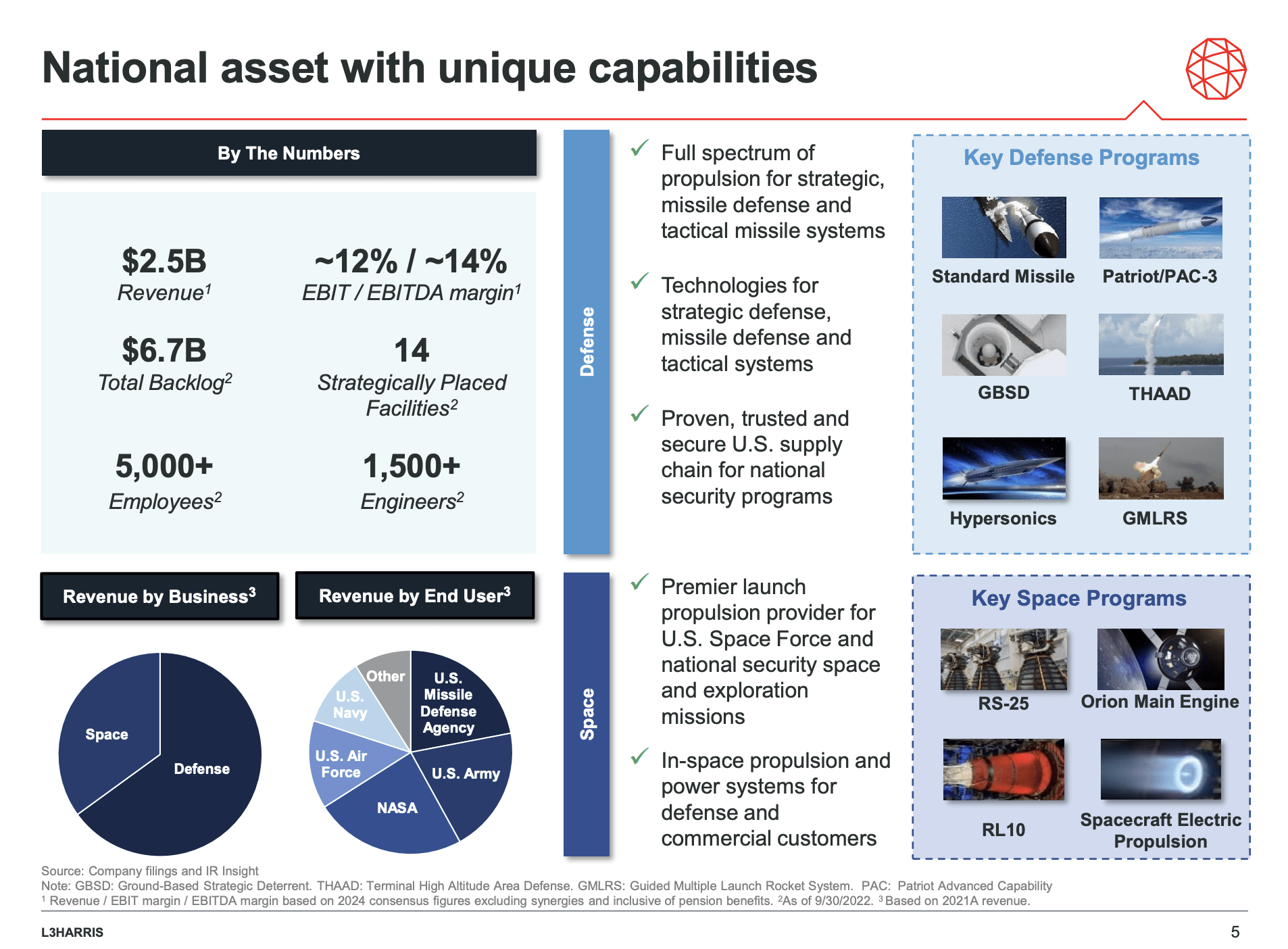

While all of these areas have strong secular growth, I care a lot about its space exposure. I believe the acquisition of Aerojet Rocketdyne was one of the smartest deals I've seen since I started covering investment opportunities.

{kind=link}

Not only is the company now an even more important supplier to all American defense contractors, but it expanded its space exposure. In addition to producing propulsion solutions for all modern rockets, including the Patriot System, THAAD, and GMLRS, the company is a supplier of space engines like the RS-25 (pictured below).

L3Harris Technologies

Thanks to this deal, the company pushed its total space exposure to 15% of its total sales, making it one of the biggest space players that also comes with a strong non-space business - the same cannot be said about speculative micro-cap stocks in this industry.

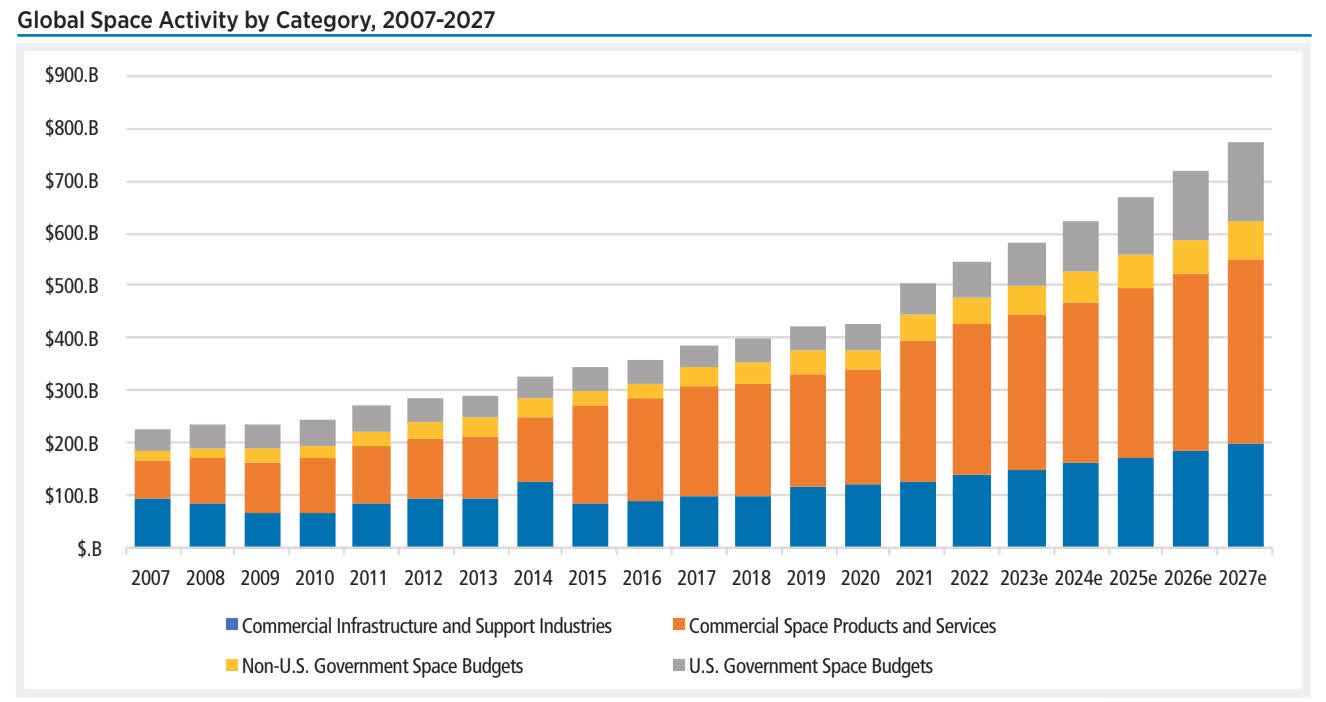

The space industry is huge.

According to Payload Space , the Space Foundation believes the space industry is poised to generate more than $800 billion by 2028, in part because of the surge in launch activities.

The commercial space sector accounts for the largest portion of the current space economy right now-78%, by the Space Foundation's tally.

In 2022, commercial space companies pulled in $426.6B, up nearly 8% from the year prior. Breaking that down even further, space products and services accounted for about two thirds of 2022 commercial revenue, and infrastructure initiatives made up the remaining third.

This is what this trend could look like:

{kind=link}

Furthermore, while I just reported that defense spending is causing some insecurity, this cannot be said about the space component of defense spending.

This is what Space News reported in March (emphasis added):

President Biden's $842 billion budget request for the Defense Department for fiscal year 2024 includes $30 billion for the U.S. Space Force, the largest funding request to date for the military space branch.

The $30 billion request is $3.7 billion more than what Congress enacted for the Space Force in 2023.

" The largest space budget ever ," DoD said in budget documents released March 13 on the Biden administration's funding request for the coming fiscal year that begins Oct 1. The proposed budget "procures and modernizes capabilities to secure the use of space in the face of increasing threats to U.S. national security space systems ," the Pentagon said in budget documents.

Most of the increase proposed for the Space Force is for the development and procurement of missile-warning satellites, and for launch services.

Being on the front row, L3Harris plans to capitalize on this.

During its 2Q23 earnings call, the company highlighted its Trusted Disruptor strategy, which focuses on being more innovative and agile.

This strategy has been particularly successful in the space sector.

Over the past four years, they have seen a remarkable 10x increase in satellite contracts.

They have also achieved a significant milestone with two classified operational constellations, a clear indication of their disruption in the market.

The company's investments in research and development and satellite manufacturing facilities have contributed to its growth, with revenue in the space sector alone increasing by over 50% since the merger between L3 and Harris in 2019.

{kind=link}

Meanwhile, challenges with suppliers have been addressed collaboratively.

Looking ahead, the company has several launches scheduled for October, and the space team is well-prepared for upcoming opportunities.

In general, the company's outlook is stellar, which makes its valuation so attractive.

Dividends & Valuation

LHX is also a dividend growth stock, which is why I bought it in the first place (I'm a dividend growth investor).

The company currently yields 2.6%. Over the past three years, annual dividend growth has averaged 11.2%. It also has bought back a ton of stock. For this, the company used proceeds from post-merger divestitures.

However, buybacks have slowed down, and the most recent hike, on February 24, 2023, was just 1.8%.

This is due to the Aerojet merger. The company will reduce its debt before returning to (what will likely be aggressive) buybacks and dividend growth.

L3Harris aims to maintain a net-debt-to-adjusted EBITDA ratio of under 3.0x in the long run. If this target is exceeded, the company intends to prioritize debt repayment to ensure it maintains a solid investment-grade credit rating. This can be achieved through a reduction in share repurchases and by potentially selling non-core assets to generate proceeds for debt repayment.

Analysts expect the company to achieve its debt target next year, which means we are close to the return of aggressive dividend growth.

Given that the yield is now at 2.7%, potentially aggressive dividend growth will have a major impact on the yield on cost of long-term investors.

This brings me to the valuation.

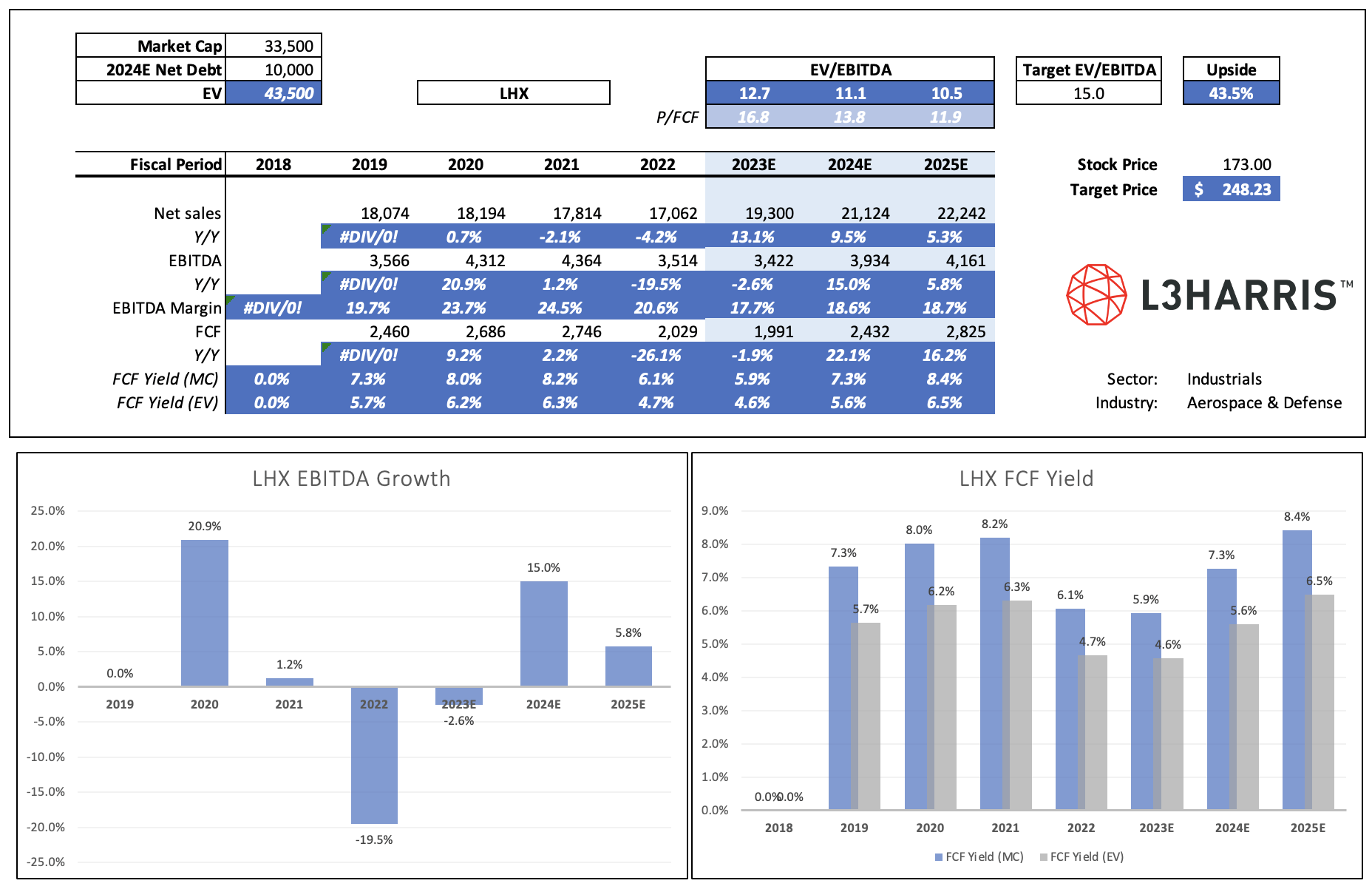

Looking at the data below, LHX is expected to maintain strong EBITDA growth. While the company isn't expected to see pre-2022 margins, EBITDA margins are expected to gradually rebound to 19%.

Leo Nelissen (Based on analyst estimates)

{kind=link}

Moreover, free cash flow is expected to see very strong growth, growing 22% in 2024 and 16% in 2025. This could boost the free cash flow yield to more than 8%.

This is one of the highest numbers among any of my dividend growth investments. It also explains why the company is expected to hit its leverage target next year and why I expect aggressive growth in shareholder distributions after this year.

With regard to the valuation, LHX has traded close to 19x EBITDA after the 2019 merger. If I apply a lower 15x valuation, the company could have between 40% and 50% upside over the next two years. The current consensus price target is $232, which is roughly $16 below my target.

I believe a 15x multiple is fully warranted for a stock with such strong EBITDA and free cash flow power.

So, while this stock price decline isn't fun, I have become an aggressive buyer, deploying a significant part of my war chest. I expanded my LHX position by more than 50% and will continue to average down if the stock keeps dropping.

I have little doubt that LHX will be one of the best performers in my portfolio over the next 10+ years.

Given its secular tailwinds, dividend growth potential, and valuation, LHX is currently my favorite dividend growth stock.

Takeaway

My decision to increase my investment in L3Harris Technologies by 55% is driven by a belief that the market is undervaluing this powerhouse of a company. While there are challenges, such as inflation concerns and supply chain issues, LHX's strong performance, diversified business segments, and strategic moves in the space industry make it a compelling choice.

The space sector, in particular, holds enormous potential, and LHX's acquisition of Aerojet Rocketdyne positions it as a key player. With a favorable outlook for defense spending in this arena, LHX is well-prepared to capitalize on these opportunities.

Moreover, as a dividend growth investor, I appreciate LHX's track record of annual dividend growth and its commitment to shareholder value, even amidst recent adjustments due to the Aerojet merger.

Considering the company's growth prospects, attractive valuation, and potential for aggressive dividend growth in the near future, I see LHX as a long-term winner in my portfolio.

This stock decline has presented an excellent buying opportunity, and I am confident that LHX will be one of my top performers in the years to come.

For further details see:

Up To 50% Undervalued - Why L3Harris Has Become My Favorite Dividend Growth Stock