UPLD - Upland Software In No Hurry To Improve Go-To-Market Changes (Rating Downgrade)

2023-12-05 18:00:13 ET

Summary

- Upland Software, Inc. beat revenue and earnings estimates for its Q3 2023 financial results.

- The company provides work management software to businesses worldwide.

- Upland Software management appears to not be in any hurry to implement its change in go-to-market approach until the end of 2024.

- Given declining revenue and worsening operating losses, my outlook on Upland Software, Inc. shares is to Sell.

A Quick Take On Upland Software

Upland Software, Inc. ( UPLD ) reported its Q3 2023 financial results on November 2, 2023, beating both revenue and consensus earnings estimates.

The firm provides work management software to businesses worldwide.

I previously wrote about UPLD with a Hold outlook on management’s focus on creating sales and marketing efficiencies to improve financial results.

Management is now saying it won’t fully implement its change in go-to-market approach until the end of 2024.

Given declining revenue and an apparent lack of urgency in improving its sales approach and cost structure, my outlook on Upland Software, Inc. stock is to Sell.

Upland Software Overview And Market

Texas-based Upland has developed a suite of work management tools for primarily small and midsize businesses.

UPLD is led by Chairman and CEO Jack McDonald, who was previously Chairman and CEO of Perficient.

The company’s primary offerings include software covering these functional areas:

-

Business Operations

-

HR & Legal

-

Sales and Marketing

-

Contact Center

-

IT

-

Product Management.

Upland seeks new customers through its inside sales, direct sales and marketing teams and partner referrals.

Per a 2021 market research report by Grand View Research, the worldwide market for customer relationship management was an estimated $43.7 billion in 2020 and is expected to reach $98 billion by 2028.

This represents a forecast CAGR (Compound Annual Growth Rate) of 10.6% from 2021 to 2028.

The primary reason for this forecasted growth is a growing demand for integrated software suites to automate engagement with customers and prospective clients.

Below is a historical and projected future growth trajectory for the CRM industry in the U.S. from 2016 to 2028 by solution type:

Grand View Research

Major competitive or other industry participants include:

-

Salesforce

-

Zoho

-

Microsoft

-

SAP

-

Oracle

-

Adobe Systems

-

Zendesk

-

ServiceNow

-

BMC

-

Ivanti

-

Atlassian

-

HubSpot

-

Sage

-

Others.

Upland Software’s Recent Financial Trends

Total revenue by quarter (blue columns) has trended lower; Operating income by quarter (red line) has remained negative in recent quarters:

Seeking Alpha

Gross profit margin by quarter (green line) has grown in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have trended higher more recently, a negative result as revenue has declined.

Seeking Alpha

Earnings per share (Diluted) have been volatile and remained well into negative territory:

Seeking Alpha

(All data in the above charts is GAAP.)

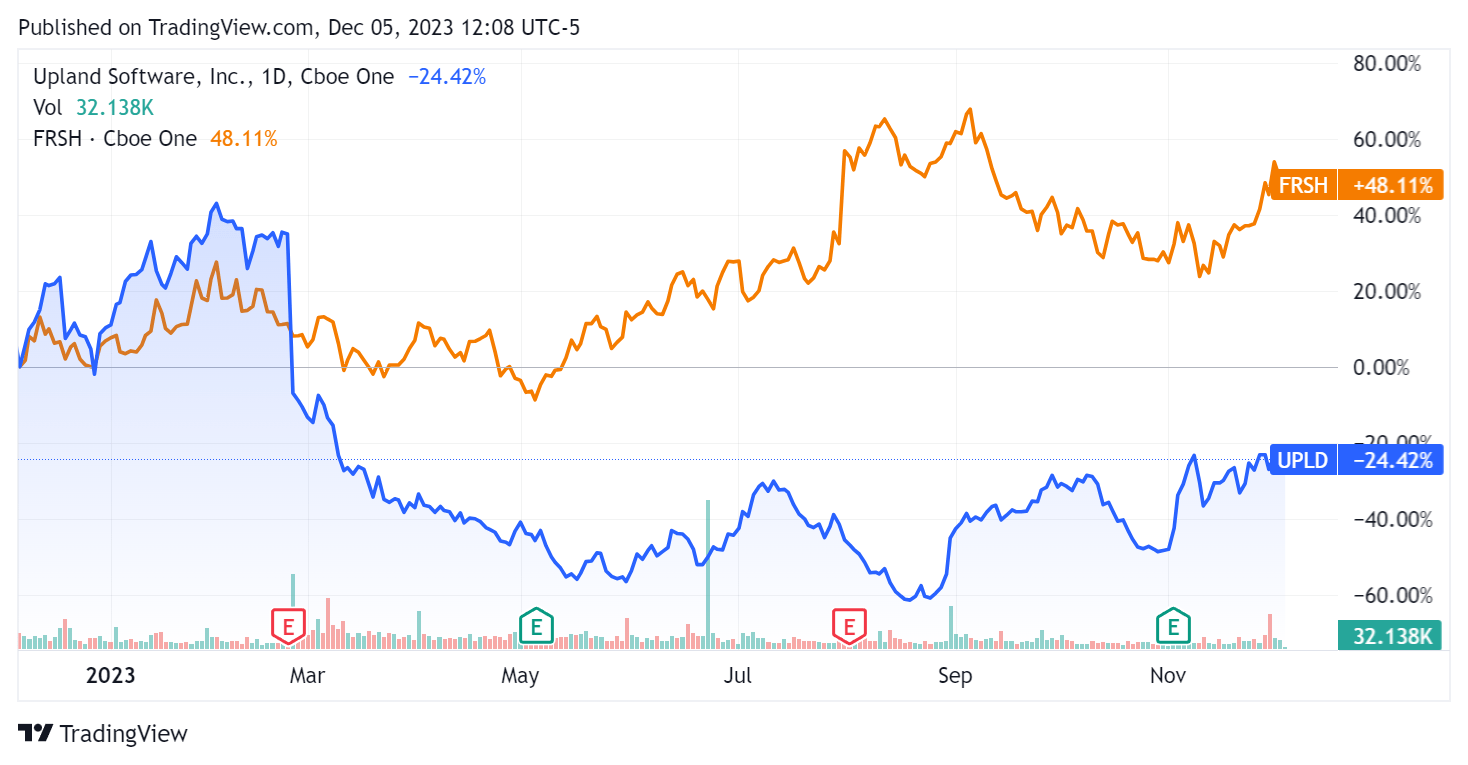

In the past 12 months, UPLD’s stock price has fallen 24.42% vs. that of Freshworks Inc.’s ( FRSH ) gain of 48.11%:

{kind=link}

For balance sheet results, the firm ended the quarter with $239.6 million in cash and equivalents and $477.5 million in total debt, of which $3.1 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was a solid $45.8 million, during which capital expenditures were only $1.2 million. The company paid $25.8 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Upland Software

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 1.7 |

| Enterprise Value / EBITDA |

| 10.9 |

| Price / Sales |

| 0.5 |

| Revenue Growth Rate |

| -3.1% |

| Net Income Margin |

| -61.3% |

| EBITDA % |

| 15.5% |

| Market Capitalization |

| $155,380,000 |

| Enterprise Value |

| $514,980,000 |

| Operating Cash Flow |

| $47,000,000 |

| Earnings Per Share (Fully Diluted) |

| -$5.95 |

| Forward EPS Estimate |

| $0.80 |

| Free Cash Flow Per Share |

| $1.42 |

| SA Quant Score |

| Hold - 3.39 |

(Source - Seeking Alpha.)

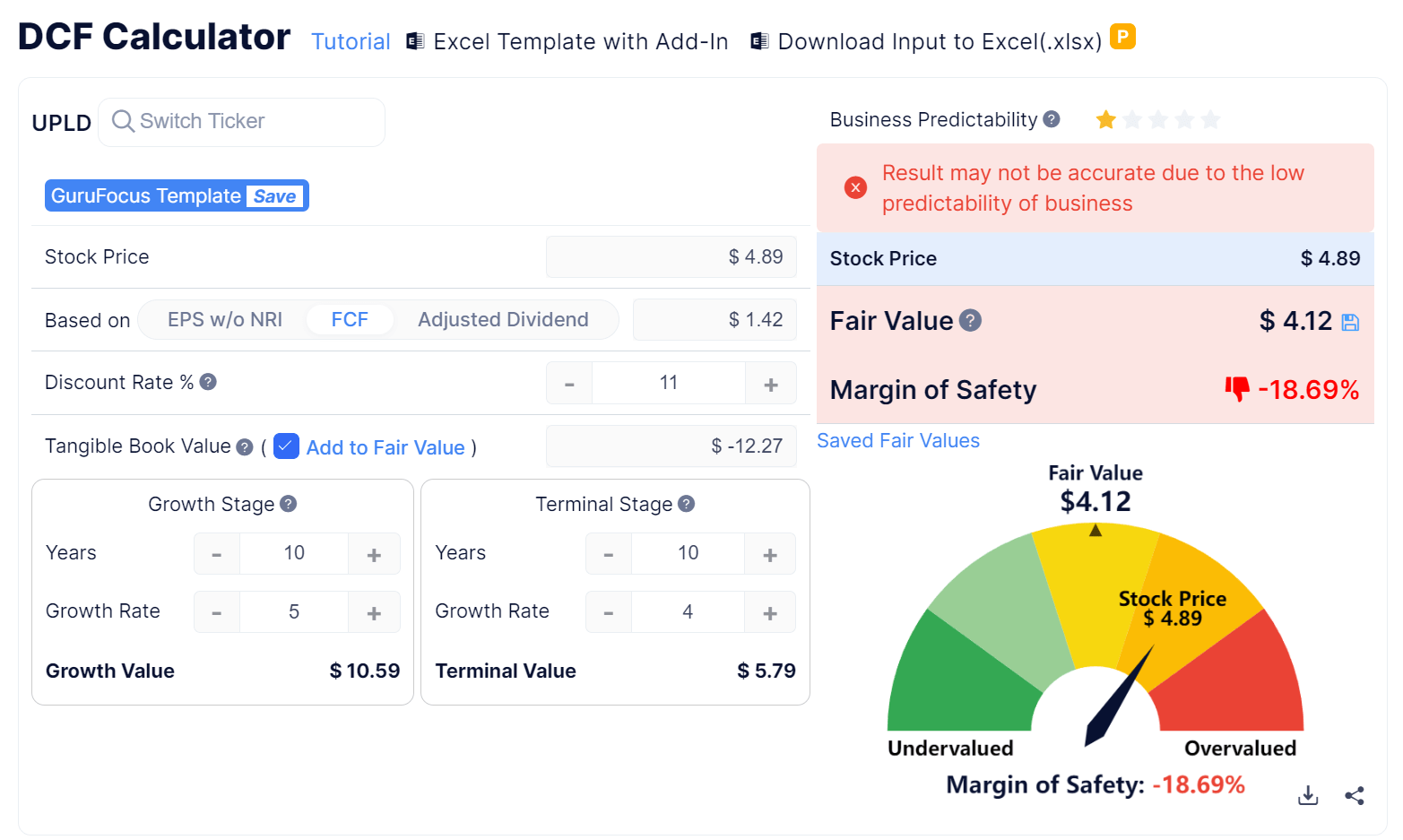

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

{kind=link}

Based on the DCF, the firm’s shares would be valued at approximately $4.12 versus the current price of $4.89, indicating they are potentially currently overvalued.

As a reference, a relevant partial public comparable would be Freshworks:

| Metric (Trailing Twelve Months) |

| Freshworks |

| Upland Software |

| Variance |

| Enterprise Value / Sales |

| 8.7 |

| 1.7 |

| -80.6% |

| Enterprise Value / EBITDA |

| NM |

| 10.9 |

| --% |

| Revenue Growth Rate |

| 21.1% |

| -3.1% |

| --% |

| Net Income Margin |

| -28.9% |

| -61.3% |

| 111.7% |

| Operating Cash Flow |

| $62,480,000 |

| $47,000,000 |

| -24.8% |

(Source - Seeking Alpha.)

UPLD’s most recent unadjusted Rule of 40 calculation was negative (13.0%) as of Q3 2023’s results, so the firm’s performance has worsened, per the table below:

| Rule of 40 Performance (Unadjusted) |

| Q4 2022 |

| Q3 2023 |

| Revenue Growth % |

| 5.1% |

| -3.1% |

| Operating Margin |

| 15.8% |

| -9.9% |

| Total |

| 20.9% |

| -13.0% |

(Source - Seeking Alpha.)

Commentary On Upland Software

In its last earnings call (Source - Seeking Alpha ), covering Q3 2023’s results, management’s prepared remarks highlighted beating the midpoint of its previous guidance range for revenue and adjusted EBITDA.

New customers, which totaled 162 during the quarter, were distributed across industry verticals and products and included 26 large customers.

The firm repurchased 783,000 shares of common stock under its September 2023 stock repurchase program authorized by the Board.

Analysts asked leadership about go-to-market changes, capital allocation and its growth strategy.

Management replied that it doesn’t expect all the go-to-market changes to be fully implemented until the end of 2024.

The firm will continue to repurchase stock and has the option of using excess cash to pay down its debt load.

Leadership also said its 2024 revenue growth guidance will be fairly conservative, likely less than its "aspirational" goal of 5% for 2024.

For the quarter’s results, total revenue for Q3 2023 fell by 6.8% year-over-year, while gross profit margin grew by 1.4%.

However, Selling and G&A expenses as a percentage of revenue rose by 6.0% YoY, indicating reduced efficiencies in generating revenue.

Operating losses were $7.3 million, the second-worst result in the last nine quarters.

The company's financial position is reasonably good, with plenty of liquidity, a meaningful amount of long-term debt but solid free cash flow.

UPLD’s Rule of 40 performance has deteriorated well into negative territory.

Management didn’t disclose any revenue or customer retention rate metrics and said it usually does so after the year is concluded.

Looking ahead, full-year 2023 revenue expectations are for a decline of 6.2% versus 2022.

If achieved, this would represent a reversal to revenue decline versus 2022’s growth rate of 5% over 2021.

In the past twelve months, the firm's EV/Sales valuation multiple has dropped by a net of 13.7%, as the chart from Seeking Alpha shows below:

{kind=link}

A potential floor to the stock could include continued stock buybacks by the company.

However, I’m not particularly impressed by management’s apparent lack of urgency in shifting to a more efficient go-to-market model.

While the stock may be supported by a potential lower cost of capital environment in 2024 resulting in an improved valuation multiple, the stock looks overvalued here amid declining revenue.

My outlook on UPLD is to Sell the stock.

For further details see:

Upland Software In No Hurry To Improve Go-To-Market Changes (Rating Downgrade)