CA - Uranium Royalty: A Bet On The High Price Of Uranium And The Lack Of Supply

2023-08-02 14:32:34 ET

Summary

- Despite having "royalty" in its name, only one of Uranium Royalty's assets generates royalty revenue.

- The main sources of income for the company are the sale of assets and the sale of its own shares, which leads to constant dilution of shareholders.

- In our opinion, the value of the company's assets is 30% lower than the current market capitalization. The value of many royalties may be close to zero.

- There are better ways to gain exposure to the uranium price, which we mention further down in the article.

Uranium Royalty Corp. ( NASDAQ:UROY ) is a uranium royalty company focused on gaining exposure to uranium prices. They make investments in uranium interests, including royalties, streams, debt, and equity investments in uranium companies. The company also holds physical uranium at Cameco's Port Hope/Blind River facilities. Through this strategy, the Company seeks interests that provide it direct exposure to uranium prices, without the direct operating costs and concentrated risks associated with uranium exploration, development, and mining.

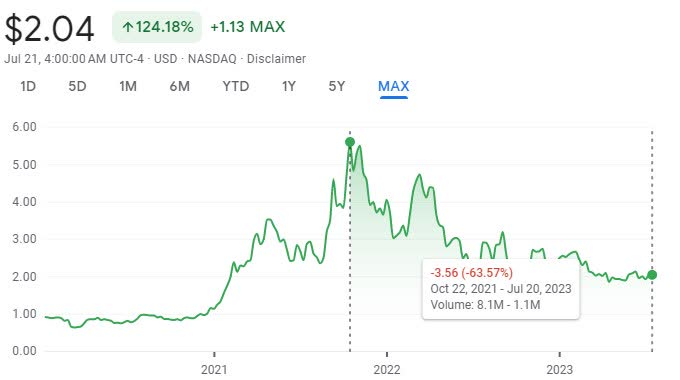

The company is 63% off its highs , so it is a good time to find out what the value of the assets it owns is. For those of you who are impatient, I will reveal that the three main sources where the company's value is hidden are: physical uranium reserves, Yellow Cake shares and royalty streams. I will also tell you that I am bearish UROY stock at the moment. A detailed analysis follows in the sections below.

{kind=link}

Google Finance

Business overview

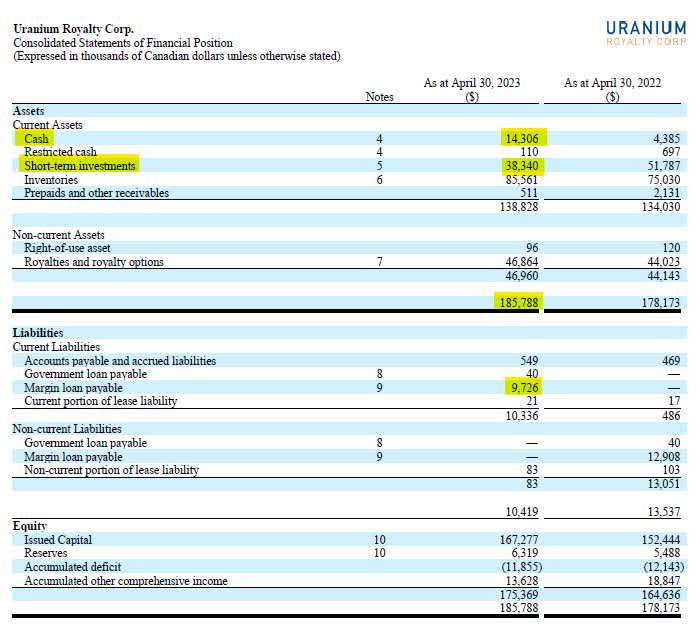

As of April 30, 2023, Uranium Royalty had a portfolio of 20 royalty interests, 5 million ordinary shares of the UK company Yellow Cake (OTCMKTS: YLLXF ), 1,548,068 pounds of U 3 O 8 held in the Company's account at Cameco's Port Hope / Blind River facilities, and cash amounting to CAD14.3 million. Additionally, they had a margin loan of CAD9.7 million secured by a pledge of all the shares of Yellow Cake, which was paid on May 3, 2023. The market cap of the company is CAD268.4 million (US$203.57 million).

The value of 1,548,068 pounds of physical uranium held at Cameco at the current market price is CAD113.79 million CAD (US$86.3 million).

{kind=link}

Trading Economics

During the year ended April 30, 2023, the Company purchased 300,000 pounds of physical uranium at a weighted average cost of US$53.59 per pound and sold 200,000 pounds of physical uranium at US$50.80 per pound to fund the repayment margin loan. So, they bought a pound for US$53.59 and sold it for US$50.80, a loss of almost US$3 on a pound.

The current value of short-term investments, comprising 5.0 million shares of Yellow Cake (OTCMKTS: YLLXF) is around CAD35.7 million (US$27 million). There are also stream and option agreements on physical uranium which may have some value if the price of uranium increases:

- Uranium Royalty Corp. (URC) has the option to acquire up to US$21.25 million (US$2.5 million to US$10 million per year) of uranium until January 2028 from Yellow Cake. If URC exercises this option, Yellow Cake will, in turn, exercise its rights under the Kazatomprom Agreement to acquire the relevant quantity of U 3 O 8 from Kazatomprom and sell such quantity of U 3 O 8 to the Company at the same price at which Yellow Cake acquires the U 3 O 8 .

- Supply Stream with CGN Global Uranium Limited - a greement to purchase 500,000 pounds of U 3 O 8 for delivery at Cameco from 2023 through 2025 at a weighted average price of US$47.71 per pound.

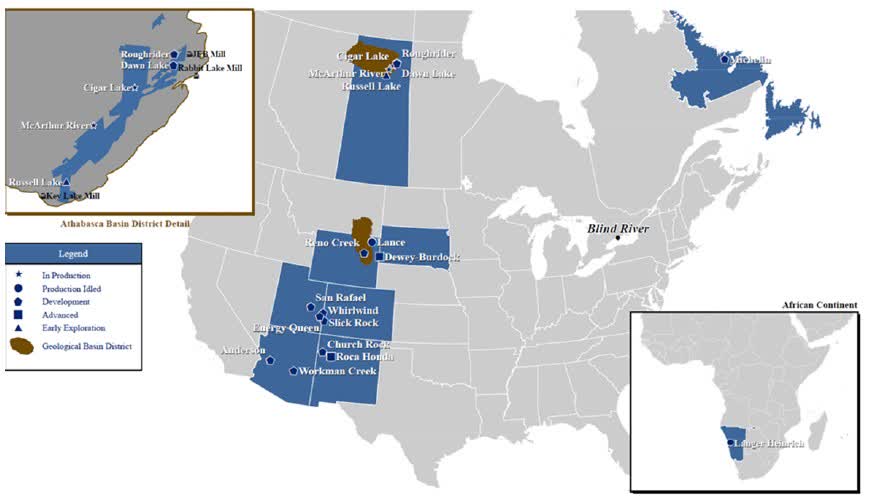

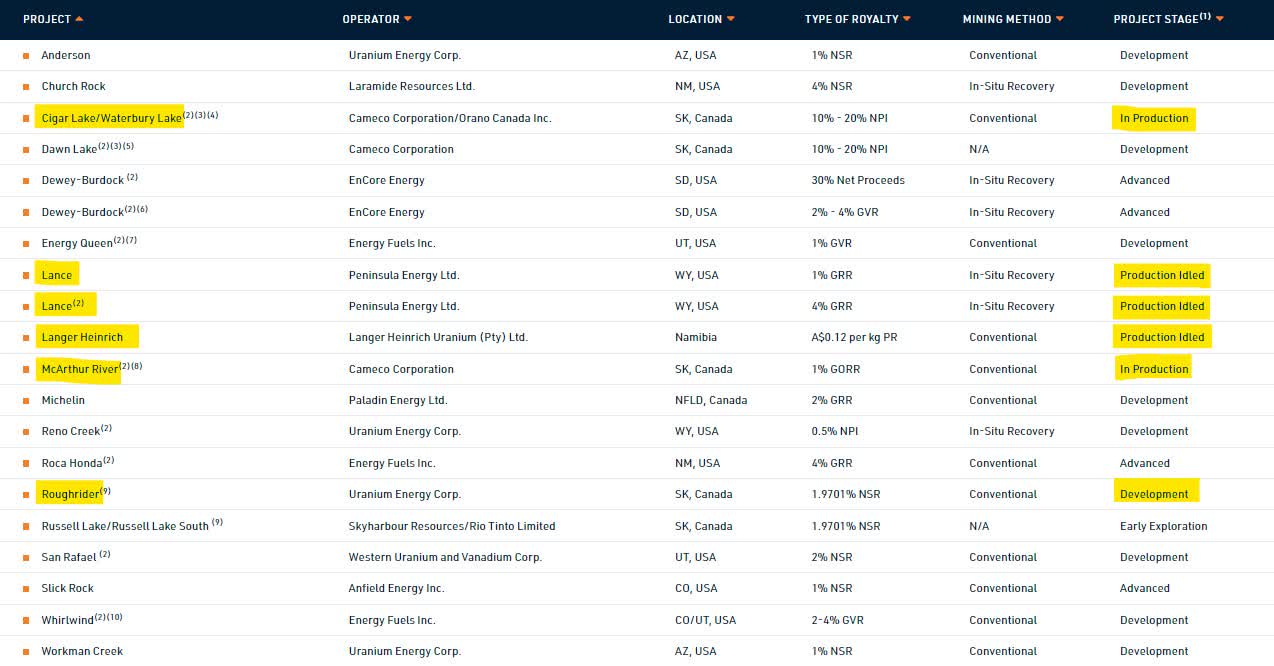

The company’s portfolio consists of 20 royalty interests , which currently do not generate revenues to the Company. Only the McArthur River and Waterbury Lake / Cigar Lake mines are in production. The production was idled at three royalties and the rest are in different stages of development. The portfolio is concentrated in USA and Canada, with the exception of one project in Namibia.

{kind=link}

Uranium Royalty Corp.; 40-F Form

We have decided to assess the value of the assets currently in production, assets with idled production, and one asset in development. The most valuable assets are McArthur River and Waterbury Lake / Cigar Lake.

{kind=link}

UROY web page

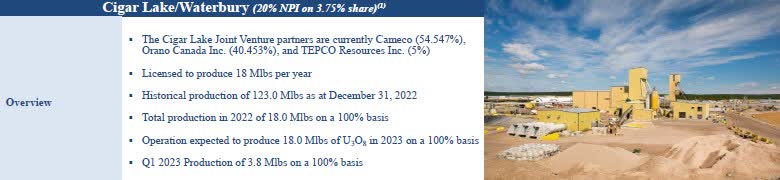

Cigar Lake project is project currently owned by a joint venture of four companies: Cameco (54.547%), Orano Canada Inc. (40.453%), and TEPCO Resources Inc. (5%). As of December 31, 2022, Cameco disclosed estimated mineral reserves of 154.8 Mlbs of U 3 O 8, and the mine had already produced 123 Mlbs by end of 2022. The yearly production is estimated to be 18 million pounds with operating costs of US$15.98 per pound.

{kind=link}

Uranium Royalty Corp.; Corporate Presentation

The Cigar Lake Royalty is a sliding scale 10% to 20% Net Profit Interest (NPI) on a 3.75% share of the overall uranium production, derived from Orano's current 40.453% production interest. After the mine reaches a production of 200 million pounds (Mlbs), the royalty percentage will decrease to 10%. As a profit-based NPI interest, this royalty is calculated based on generated revenue, with deductions for certain expenses and costs, including development costs. Given the significant amount of expenditures for development, the royalty will only generate revenue for the company after these significant cumulative expenses are exhausted.

So, let us value this asset. If we assume uranium price at 55 USD/lbs, yearly production of 18 Mlbs, net profit at 39 USD/lbs (U$55 price of U 3 O 8 less U$16 costs), exhaustion of cumulative expenses by end of 2027, and a 5% discount rate, we arrive at an NPV of 6.65 million USD, which we believe is a very optimistic valuation. In 2028, the royalty will be 10% NPI, and the remaining mineral reserves will be 65 Mlbs, which gives us less than 4 years of mine life. This royalty is more of a bet on high uranium prices than an investment.

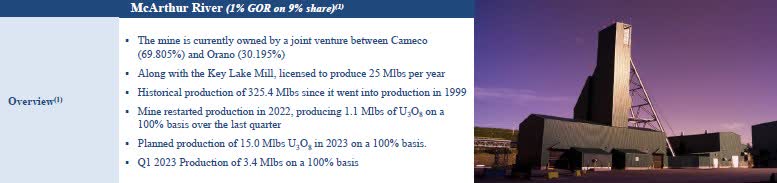

McArthur River is a project operated by Cameco. As of December 31, 2022, Cameco disclosed estimated reserver of 394 million pounds (Mlbs) of U 3 O 8 and they plan to achieve a production rate of 18 million pounds per year by 2024. This gives us 22 years of mine life with the current production plans. The project was suspended by 2022 and produced 1.1 million pounds in 2022. It is expected to produce 15.0 million pounds in 2023.

{kind=link}

Uranium Royalty Corp.; Corporate Presentation

The McArthur River Royalty is a 1% GORR (gross overriding royalties) on a 9.063% share of uranium production. URC can also choose to receive physical uranium as payment, which they did in 2022. This is probably the best royalty of the company. If the production targets are met, URC will receive 13.6 thousand pounds (klbs) of U 3 O 8 in 2023 and 16.3klbs of U 3 O 8 from 2024. At the current uranium price of 55 USD/lbs, the cash flow for the company is US$748k in 2023 and US$896.5k from 2024. This represents an NPV of 11.66 million USD (using a 5% discount rate).

The Lance Project is located in Wyoming, USA and operated by Peninsula Energy. The mine is expected to produce 14.4 million pounds (Mlbs) of U 3 O 8 over a 14-year mine life, with All-In Sustaining Costs of US$39.08/lbs. According to Peninsula's quarterly activity report for March 2023, commencement of commercial production was expected in mid-year 2023. Uranium Royalty Corp. holds two separate royalty interests on the Lance Project: 4% of the gross income from the underlying property and 1% gross revenue royalty interest. The Net Present Value using production of 1.0 Mlbs from 2024, a uranium price of 55 USD/lbs, and a 5% discount rate is US$11.2 million with a yearly cash flow of US$1.19 million.

The Langer Heinrich mine, located in Namibia, Africa, is operated by Langer Heinrich Uranium (75% owned by Paladin). The mine has been under care and maintenance since mid-2018. Paladin stated that the project is on track and on budget (US$118 million) for first production in the first quarter of 2024. Proved and probable reserves are estimated to be 83.8 Mlbs of U 3 O 8 with a 17-year mine life and C1 costs of US$27.40/lbs. The royalty is comprised of a production royalty ((PR)) of A$0.12 per kilogram of yellowcake. When we assume yearly production of 4.94Mlbs from 2024, a uranium price of 55 USD/lbs, and a 5% discount rate, we get a yearly cash flow of US$180k and an NPV of US$1.94 million, which we believe is an optimistic valuation.

The Roughrider Project is a development-stage project in Saskatchewan, Canada. The operator is Uranium Energy Corp., which acquired it from Rio Tinto in 2022 for $150 million. The Company owns a 1.9701% NSR (net smelter return) royalty in the project. As the project was only recently impaired by Rio Tinto, we were interested in their opinion on this asset. This is what Rio Tinto wrote in their 2022 Annual report : “On 17 October 2022, we completed the sale of the Roughrider uranium undeveloped project located in the Athabasca Basin in Saskatchewan, Canada for US$150 million (US$80 million in cash and US$70 million in shares of Uranium Energy Corp.). The project was fully impaired during the year ended 31 December 2017 due to significant uncertainty over whether commercially viable quantities of mineral resources could be identified at a future date .” Therefore, our valuation for this asset is zero. Just a quick reminder, Rio Tinto acquired this asset in 2012 for US$550 million and sold it last year for $150 million. This illustrates how volatile and unpredictable the mining business can be.

Taking into account the fact that it takes at least 10 to 15 years to bring a mine online , one has to ask oneself how long they are willing to wait to realize the value in these development assets and what it takes to bring them online. In our view, we would need a uranium price above $100 USD/lbs and a significant supply disruption lasting years to keep the prices above US$100/lbs. Such a black swan event would be if the biggest uranium producer, Kazatomprom, went offline. It could create a supply gap of more than 25 Mlbs of uranium annually, which may bring the uranium price to new all-time highs above US$148/lbs. However, the probability of such an event is, in our opinion, low, and as investors, we should not rely on low probability events.

World Nuclear Association

So the question is: Is it possible to bring new 25 Mlbs of uranium annually to the market, and how long will it take? If we look at Cameco, they have three suspended operations : Rabbit Lake (7.5 Mlbs annual production), Crow Butte (2 Mlbs annual production), and Smith Ranch-Highland (3 Mlbs annual production). At the same time, they would lose production of 3.32 Mlbs from their JV with Kazatomprom, so they may add a new supply of 9.18 Mlbs of uranium annually in a relatively short time. The Lance and Lager projects mentioned above may bring an additional 5.94 Mlbs from 2024. So, we see that three operators may bring 15.12 Mlbs to the market in 1 to 3 years. The remaining operators probably also have some operations that can start production in several years, but they will not be able to produce at US$55/lbs for U 3 O 8 .

A look at the Financials

The last annual report (form 40-F) was published in July 2023. We will go over income statement and balance sheet and highlight some items.

{kind=link}

Uranium Royalty Corp; Form 40-F, 2023

As of April 30, 2023, the Company had cash of US$14.3 million, compared to US$4.4 million on April 30, 2022. The increase in cash, amounting to US$9.9 million, was primarily due to the net proceeds received from the sale of uranium inventory, totaling US$13.9 million, and the net proceeds from the sale of a portion of its shares in Yellow Cake and all of its shares in Sprott Physical Uranium Trust. However, this increase was partially offset by a cash payment of US$2.2 million for the acquisition of royalties, cash paid for the purchase of 300,000 pounds of U3O8 for US$21.4 million, and an equity investment in Sprott of US$2.9 million. Additionally, there was a net repayment of margin loan principal and interest, amounting to a total of US$5.5 million.

The increase in total assets from US$178.2 million to US$185.8 million as at April 30, 2023 was primarily attributed to the increase in cash received from the sale of the shares, amounting to US$14.2 million. However, this increase was partially offset by a net repayment of margin loan principal and interest, totaling US$5.5 million.

The margin loan was subject to an interest rate of the Adjusted Term SOFR Rate (5.06%) plus 5.50% per annum, and the unutilized portion of the facility was subject to a standby fee of 2.50% per annum. However, I must clarify that this loan was fully settled and extinguished on May 3, 2023.

{kind=link}

Uranium Royalty Corp; Form 40-F, 2023

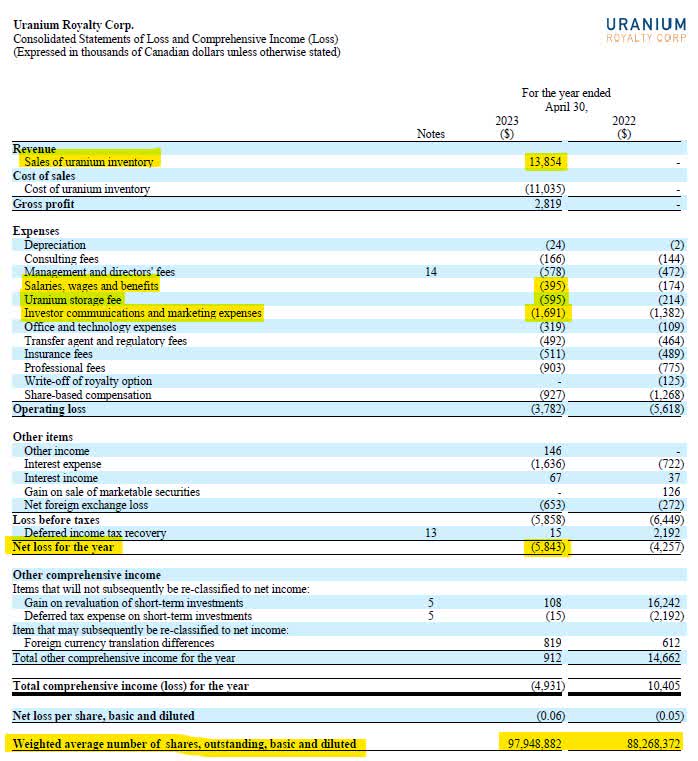

The increase in net loss for the year ended April 30, 2023, was primarily attributable to various factors. These include increases in uranium storage fees amounting to US$0.4 million, investor communications and marketing expenses totaling US$0.3 million, salaries, wages, and benefits increasing by US$0.2 million, and interest expenses rising by US$0.9 million.

The company's only sources of cash are the sale of assets or the sale of its own shares. It is appreciated that the high-interest loan was fully settled and extinguished on May 3, 2023. However, it's worth noting that while the uranium inventory increased by only 100,000 pounds, the storage fees have quadrupled. This indicates that management should focus on controlling storage costs, as the expenses of holding uranium have significantly risen. Therefore, further sales of uranium inventory may be a suitable source of cash for the company.

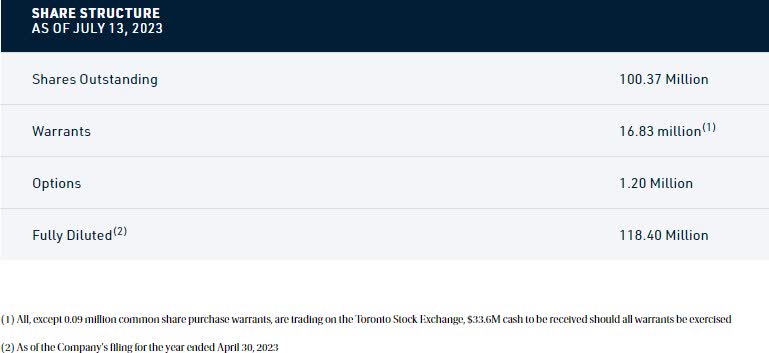

What we don`t like is 2.27-fold increase in wages and very high marketing expenditures. These indicate that the company may focus on raising additional funds through the sale of shares, potentially leading to shareholder dilution. Observing the graph below, the trend appears clear with no sign of change.

Data from Seeking Alpha (by April of each year); Graph: author

Since April 2023, the number of shares has already increased . This confirms the concern about potential shareholder dilution due to the company's focus on raising additional funds through the sale of shares. It's essential for investors to closely monitor such developments and assess their impact on the company's financial health and shareholder value.

{kind=link}

company`s web page

What we would like to see is a decrease in costs, especially a significant reduction in marketing expenses, which will lower the need for additional funding. The main source of cash should be the sale of U 3 O 8 from inventory, supplemented by the sale of shares, but only if there are significant investment opportunities. However, it's crucial to recognize that there is a high risk that suspended operations and development projects may not begin production for 10 years, if at all. In general, URC is a bet on high uranium prices and a lack of supply. The question to consider is how long you are willing to wait for it.

Valuation

| Asset |

| value (US$ million) by July 2023 |

| physical uranium |

| 86.3 |

| Yellow Cake shares |

| 27 |

| Cigar Lake project |

| 6.65 |

| McArthur River project |

| 11.66 |

| Lance project |

| 11.2 |

| Langer Heinrich project |

| 1.94 |

| Cash* |

| 3.48 |

| URC value |

| 148.23 |

Our optimistic valuation of the company is US$148.23 million while the market cap is US$203.57 million. It`s no-brainer for us. Uranium Royalty Corp. is a SELL .

Some other ways how to get exposure to Uranium

As we promised at the beginning of this article, we provide also several other ideas how to get exposure to uranium price. We believe that all of these possible investments are better than Uranium Royalty Corp.

{kind=link}

Barchart.com

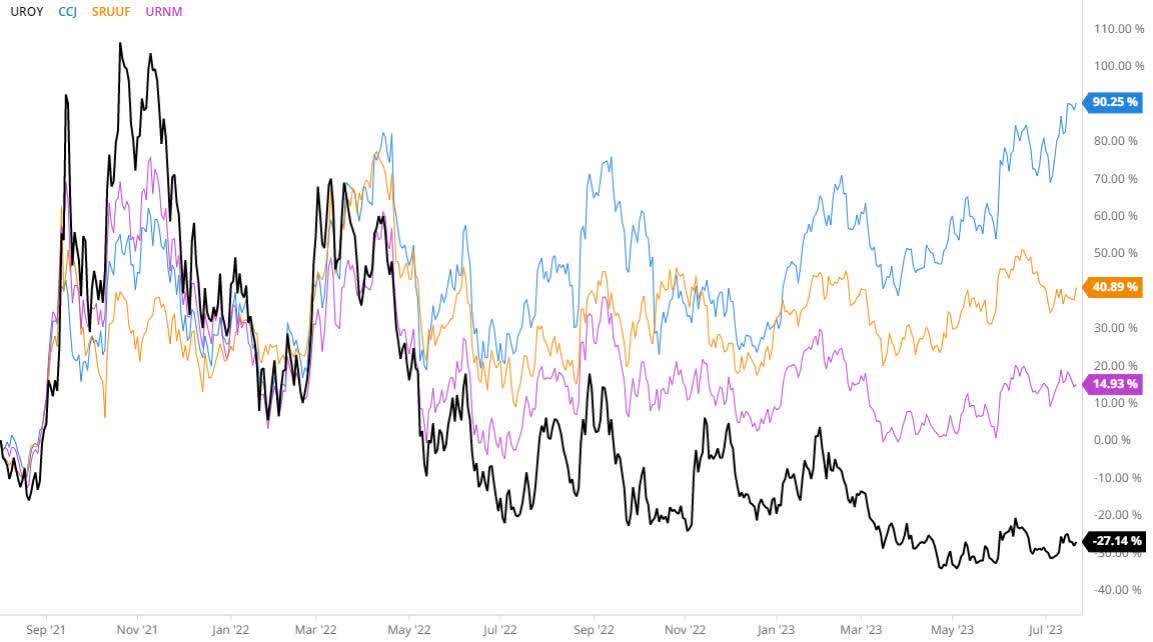

First one is Sprott Physical Uranium Trust (OTCMKTS: SRUUF), which holds substantially all of its assets in uranium in the form of U 3 O 8 . It is Closed-End trust with management fee 0.70% which currently trades with discount to NAV of -12.12% and has outperformed Uranium Royalty Corp. ( UROY ) by 68% in the last 2 years.

{kind=link}

Sprott.com

Second is Sprott Uranium Miners ETF ( URNM ), if you want to have exposure to uranium miners. Management fee is 0.85% and the ETF has 37 holdings including physical uranium. The fund has outperformed Uranium Royalty Corp. ( UROY ) by 41% in the last 2 years. Below are its top 10 holdings which represent almost 75% of net assets.

{kind=link}

Sprott.com

And the last one, if you feel comfortable to invest in single stocks, is Cameco ( CCJ ), which has clearly outperformed Uranium Royalty Corp. and Sprott Uranium Miners ETF and Sprott Physical Uranium Trust in last two years. Cameco is the world's largest publicly traded uranium company, based in Saskatoon, Saskatchewan, Canada. In 2015, it was the world's second largest uranium producer, accounting for 18% of the world production. It is not a goal of this article to analyze the value of Cameco, so we suggest readers to refer to other articles about the company on Seeking Alpha.

Conclusion

Uranium Royalty Corp. is a company without stable cash flows, relatively high cash burn rate, questionable value of the royalties (especially those in development stage) and constant shareholder dilution. Market cap of the company is in our opinion 30% higher than the value of the assets. For us, Uranium Royalty Corp. is a SELL . We believe there is a better way to get exposure to the price of uranium.

For further details see:

Uranium Royalty: A Bet On The High Price Of Uranium And The Lack Of Supply