URBN - Urban Outfitters: Limited Margin Of Safety At Current Levels

2023-10-18 02:59:29 ET

Summary

- Urban Outfitters reported record Q2 sales driven by strong performance in its Free People, Anthropologie, and Nuuly segment.

- Importantly, this momentum is likely to continue into Q3, and the company expects further margin expansion as it benefits from fewer markdowns and higher full-priced selling.

- That said, while its ex-UO segments continue to perform well & Anthropologie excelled again, I don't see enough margin of safety to justify chasing the stock above $35.00.

Roughly two years ago, I wrote on Urban Outfitters ( URBN ), noting that while the stock reported record Q2 results and was benefiting from wardrobe refreshes post-COVID-19, the stock looked close to fully valued at $36.00. Since then, the stock has suffered a 50% drawdown and has seen limited upside despite solid results year-to-date and continued to see solid growth in its Free People, Anthropologie, and Nuuly segments. In fact, its Anthropologie segment grew sales by ~33% on a two-year basis and the company has ambitious goals for Free People Movement (active-wear, beyond-the-gym staples, and wellness essentials). In this update, we'll dig into the recent results, dig into how the stock looks positioned heading into H2, and whether the stock looks worthy of investment at current levels.

{kind=link}

Fiscal Q2 2024 Results & Recent Developments

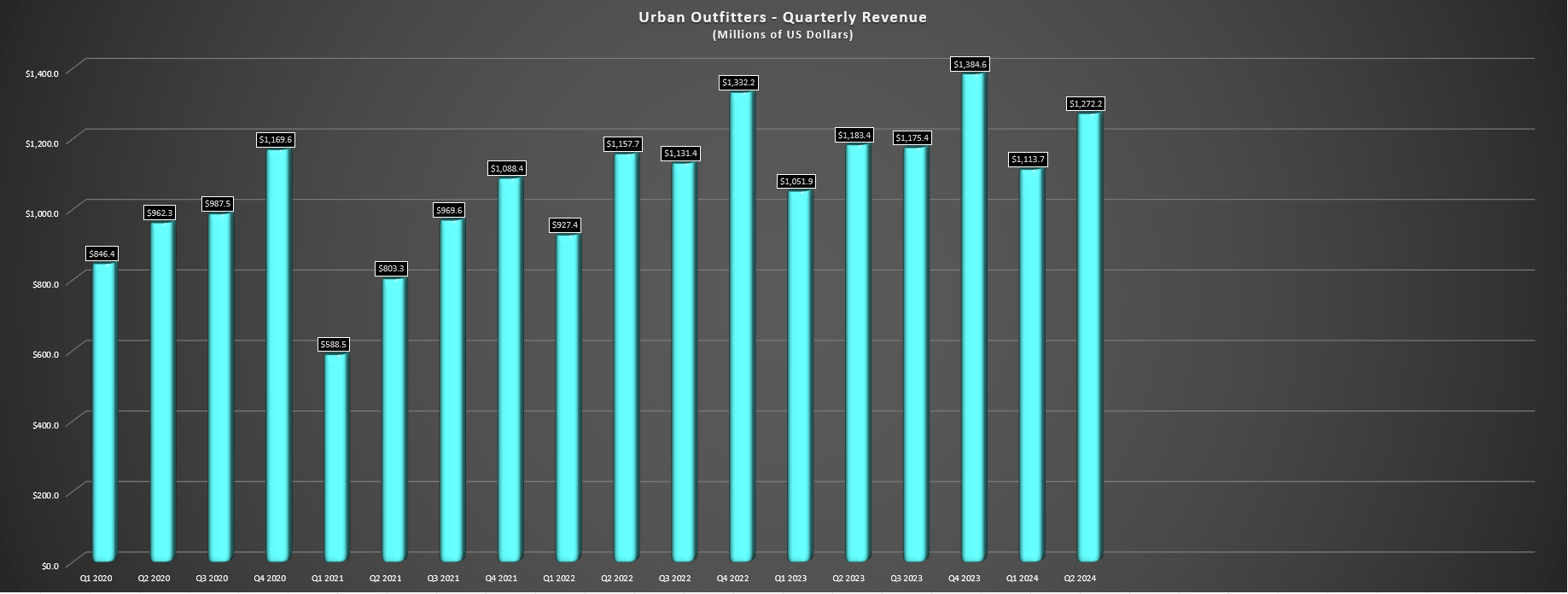

Urban Outfitters released its fiscal Q2 2024 results in August and was one apparel brand next to Abercrombie & Fitch ( ANF ) and Lululemon ( LULU ) that outperformed expectations, proving the right assortment could overcome a tough macro backdrop. This was evidenced by record fiscal Q2 sales of ~$1.27 billion (+8% year-over-year) driven by strength in North America and exceptional quarters from its Free People, Anthropologie and Nuuly segments. And while its OU brand couldn't complete the quadfecta of positive comp sales, the company still managed to post 5% consolidated comp retail sales year-over-year as its other segments more than offset the softness at OU. And from a development standpoint, the company opened 9 net new stores in the period, including 5 Free People stores.

Urban Outfitters Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

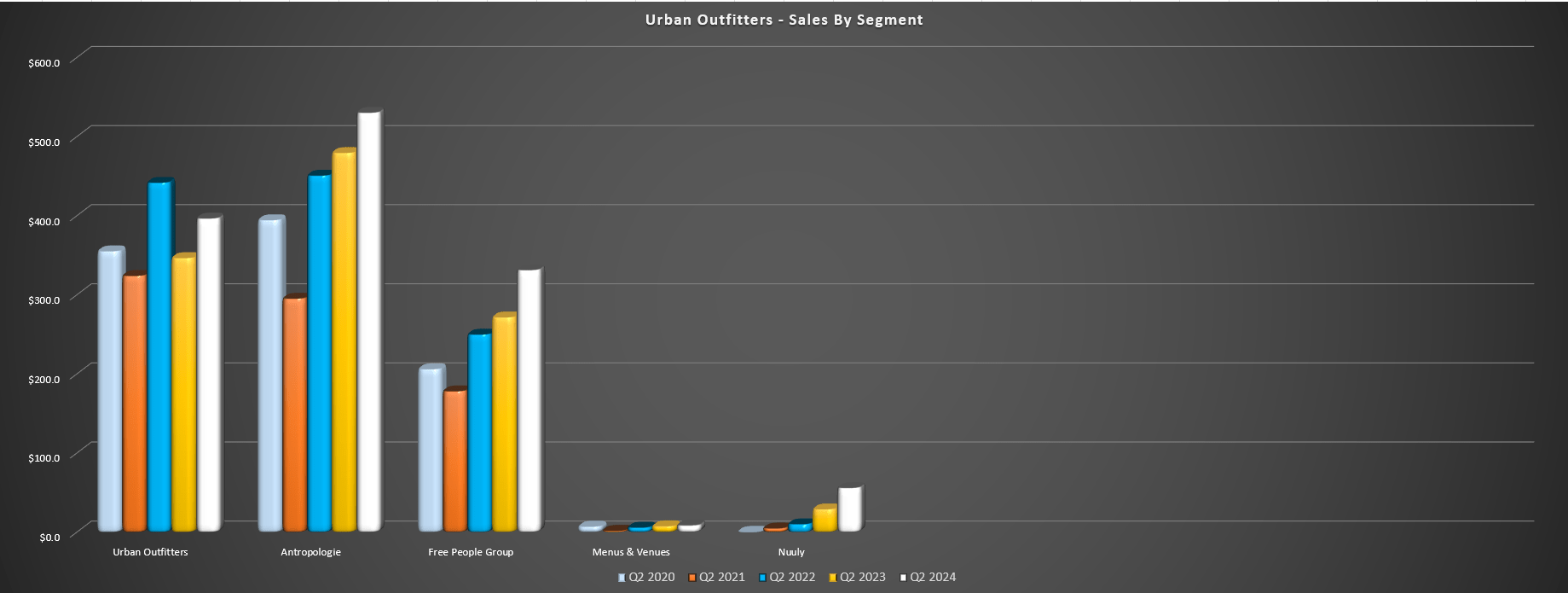

Digging into the results a little closer, Urban Outfitters reported 26.9%, 10.6%, and [-] 14.1% comp sales growth at Free People, Anthropologie, and OU, respectively, with total Free People increasing 22% year-over-year to ~$331 million with traffic, transactions, conversion rates and AUR all up, besides strength in digital. Urban Outfitters noted it believes there's the potential for Free People Movement to potentially be a $1.0 billion brand in five to six years, and while it's an ambitious goal, American Eagle certainly proved that this was the case with Aerie under Jennifer Foyle, exceeding even its own expectations. In addition, it was certainly encouraging to hear commentary that the customer is "favoring fashion over price ", suggesting that if the right assortment is there that its customers will pay up.

Urban Outfitters Quarterly Revenue by Segment - Company Filings, Author's Chart

{kind=link}

Elsewhere at Anthropologie, Urban Outfitters shared it was the 10th consecutive quarter of positive retail comps, and that it surpassed pre-pandemic traffic, conversion and comps both in store and online. The company called out apparel, accessories and shoes as areas of strength, and also noted that profit increased materially because of fewer markdowns, with momentum continuing into August. Urban Outfitters also shared that it has hired a new president of Anthropologie Home to improve its growth rates in this business, which has been an area of strength for off-price retailers like TJX Stores ( TJX ). And elsewhere at the company's smallest but rapidly growing Nuuly segment, sales grew 94% year-over-year on 85% subscriber growth, with this being Urban Outfitters' new segment, a clothing rental and resale marketplace. In addition, the segment is getting closer to profitability with a DC in Kansas that will improve delivery times and reduce delivery costs to consumers.

Unfortunately, we saw SG&A increase to 25.4% (+100 basis points) because of incentive-based compensation and increased marketing and creative expenses, and its UO brand still struggled despite the higher expenses. Urban Outfitters noted that this was the one disappointing segment with sales down over 10% on a two-year basis and that its comp improvement came up shy of its goals. And Urban Outfitters also shared that the turnaround could take longer than it expects at its UO brand with this news dampening what was otherwise a very impressive report for its other segments. The silver lining was that at least full-priced sales have improved and it's seen lower mark down rates, a trend that's consistent across its segments, which led to higher gross profit.

Earnings Growth & H2 2024 Outlook

Digging into earnings growth and the company's H2 2024 outlook, margins came in strong during fiscal Q2, with gross profits up 410 basis points, and the company also did a solid job controlling inventory which fell 16% to ~$586 million. The sharp increase in margins helped to push quarterly earnings per share [EPS] to $1.10 vs. $0.64, and FY2024 annual EPS estimates are now sitting at $3.24, pointing to 3% growth vs. the difficult comps from FY2022 (wardrobe refresh post-lockdowns) and a near doubling of annual EPS year-over-year. Notably, this earnings breakout (new multi-year high for annual EPS) appears to have further momentum, with FY2025 and FY2026 annual EPS estimates sitting at $3.45 and $3.60, respectively. So, while some brands are struggling to grow earnings and are struggling to hold on to market share like Gap ( GPS ), Urban Outfitters is executing better than I expected.

{kind=link}

As for the company's H2 2023 outlook, I would normally be quite cautious with personal savings rates continuing to trend lower with the added impact of higher gas prices. However, Urban Outfitters certainly proved in its recent results that its better segments are performing well with double-digit growth and it's doing an excellent job executing while some other apparel brands are stumbling. Hence, although it might have been more sensitive if it was more heavily reliant on UO, the growth in its other segments now ~2.3x the size of UO vs. ~1.7x in fiscal Q2 2020. Plus, Urban Outfitters remains confident in further margin improvement in H2 of this year, suggesting that the fiscal Q3 results were not an anomaly if it can continue similar to momentum to what it's enjoyed year-to-date, suggesting the potential to beat fiscal Q3 estimates of $1,264 million. Let's dig into the valuation to see if the stock is offering a margin of safety:

{kind=link}

Valuation

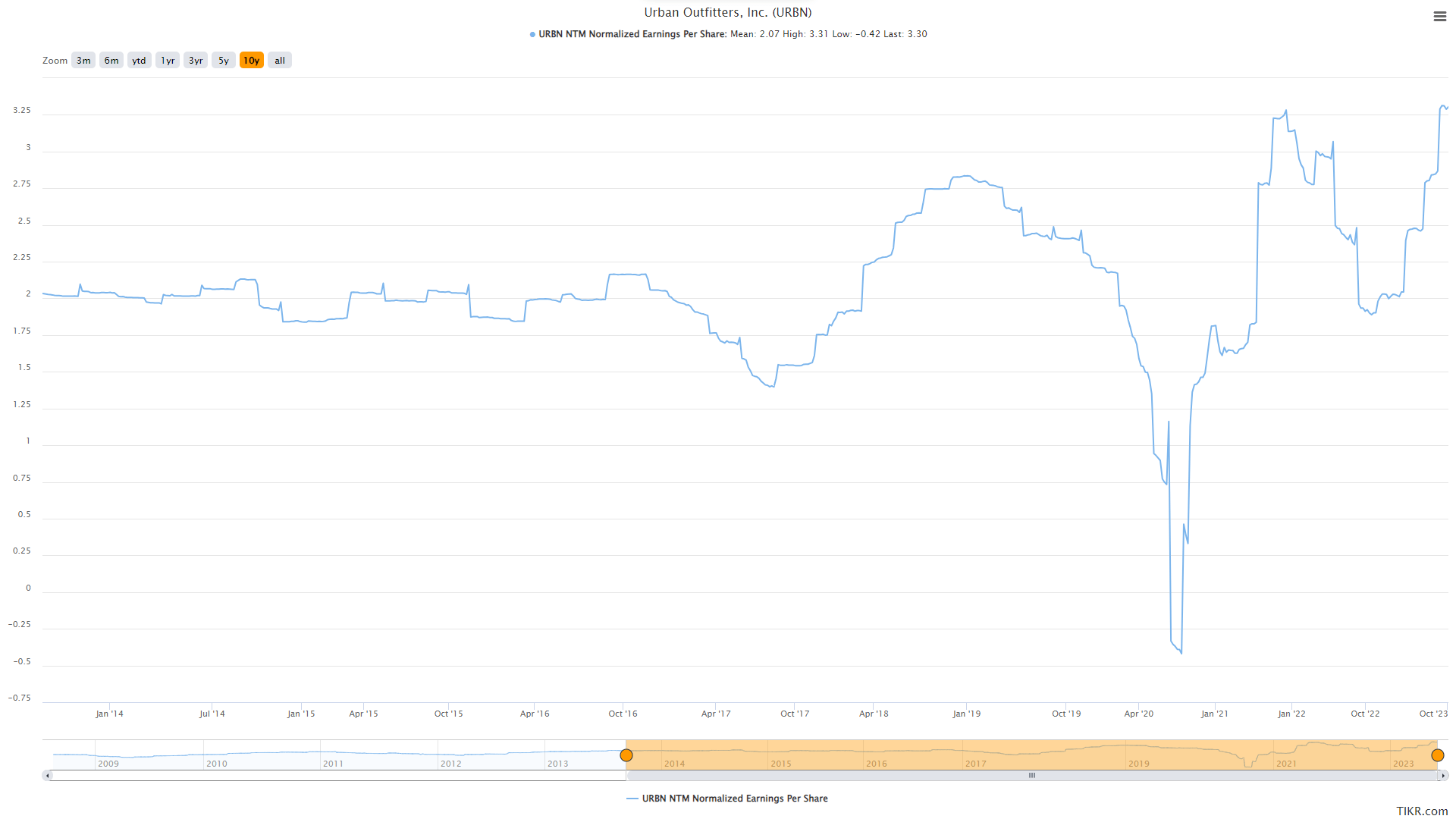

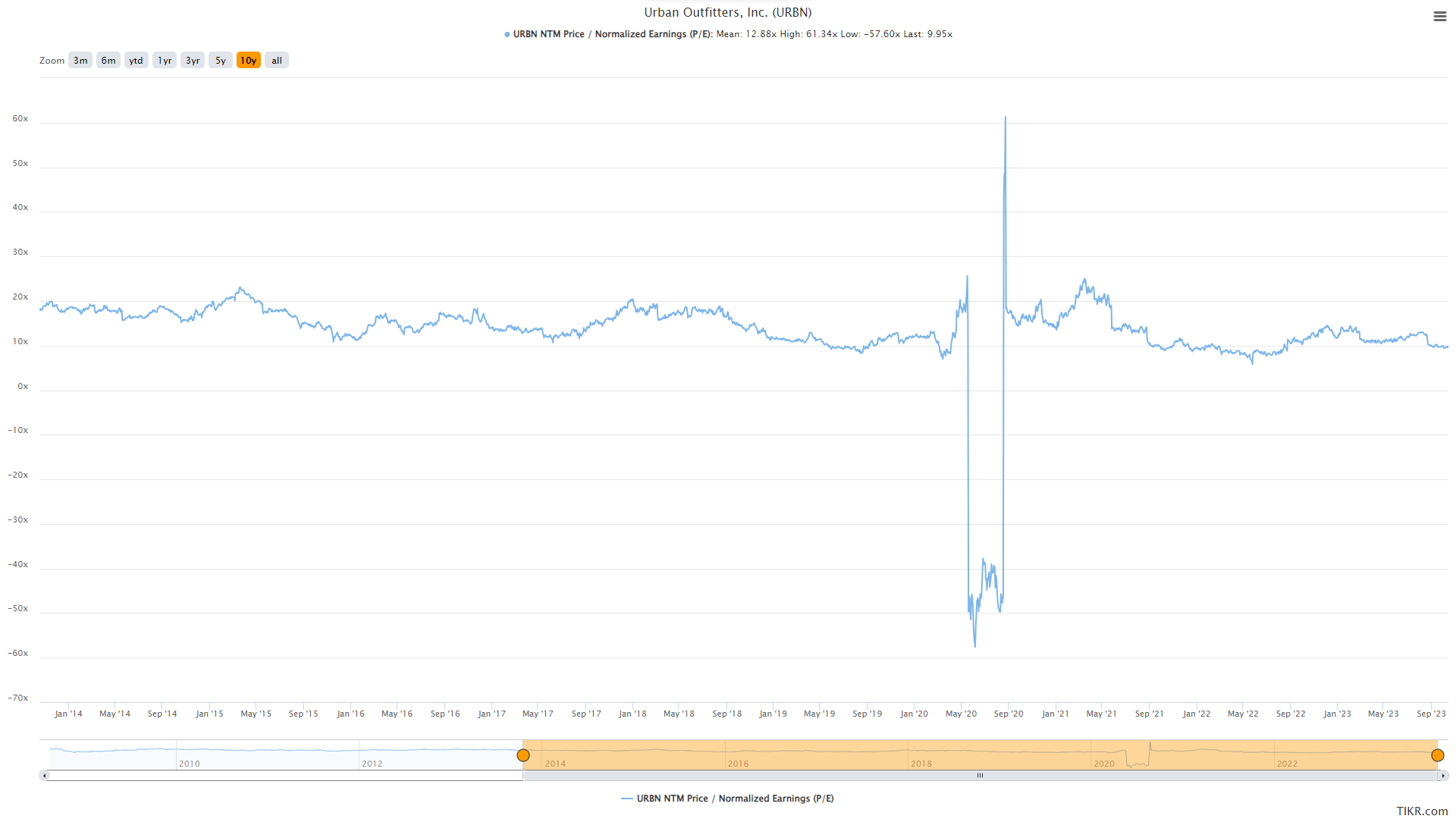

Based on ~93 million shares and a share price of $35.00, Urban Outfitters trades at a market cap of ~$3.26 billion and an enterprise value of ~$3.77 billion. This makes it one of the higher capitalization names in the Retail/Apparel industry group, ahead of names like Boot Barn ( BOOT ) and Foot Locker ( FL ), and having a similar capitalization to American Eagle. However, with the stock now up ~95% off its Q2 2022 levels, I no longer see a margin of safety in place. This is because the stock is trading at ~18.0x free cash flow on an EV/FCF basis using FY2025 estimates, which leaves the stock close to fully valued (in my view), especially in the current interest rate environment where we've seen considerable multiple compression across most sectors. Meanwhile, the stock is trading just shy of its average earnings multiple of ~12.9 (10-year average), sitting at ~10.8x FY2024 earnings estimates ($3.24).

Urban Outfitters - Current & Historical P/E Ratio - TIKR.com

{kind=link}

Using what I believe to be a more conservative multiple of 11.0x earnings and FY2025 annual EPS estimates of $3.45, I see a fair value for the stock of $37.95, pointing to a 9% upside from current levels. However, while this might interest some investors, I am looking for a minimum 25% discount to fair value for mid-cap stocks to ensure an adequate margin of safety. And if we measure from an estimated fair value of $37.95, this points to an ideal buy zone of $28.50 or lower, suggesting URBN is nowhere near a low-risk buy zone following its gap-up and steady trend higher after its fiscal Q1 results. So, while the stock may be nowhere near as overbought as Abercrombie & Fitch, which is trading in nosebleed territory and vulnerable to a sharp correction, I think there are better places to park one's capital currently.

Summary

Urban Outfitters put together a solid fiscal Q2 report and, judging by the better than expected retail sales and positive commentary on fiscal Q3 trends, the company is likely to have another solid report when it announces its results in November. That said, I prefer to buy names that are hated or significantly priced (and ideally both), and while Urban Outfitters is very reasonably priced if it can turn its UO brand around, I don't see enough margin of safety to bet on the stock just yet. Hence, if I were looking to put capital to work in the Retail Sector ( XRT ), I think there are better bets elsewhere like Pet Valu ( PET:CA ) on dips.

For further details see:

Urban Outfitters: Limited Margin Of Safety At Current Levels