URBN - Urban Outfitters: Operational Outperformance To Drive Growth

2023-05-17 02:00:35 ET

Summary

- Urban Outfitters has delivered strong operational performance despite a tougher macro backdrop.

- While Free People and Anthro continue to grow strong, Urban Outfitters remains a laggard, and the tepid North American market could continue to pressure URBN.

- Free People and Anthro's exposure to higher-end consumers puts them in a relatively better position, as seen historically during an economic crisis.

- Strong momentum in Free People and Anthro, continued traction in Nuuly, valuation comfort, clean inventory, and balance sheet strength.

- We initiate URBN as a Buy with a target price of $32 (at 7x CY23 EBITDA).

Background

Urban Outfitters ( URBN ) ("UO") is a leading specialty retailer offering assorted collection of collections of fashion apparel, accessories, and home goods housing three key brands: Urban Outfitters, Anthropologie, and Free People under its portfolio. It operates over 500 stores for UO and Anthro brands while it also operates over ~190 Free People Stores globally including the US, Canada and Europe. It has outperformed its peers by a huge margin with its share price up over 20% compared to a steep decline in prices observed in its peers. The company has managed to consistently perform well on the back of operational discipline, lean inventory, omnichannel capabilities and a dependable customer loyalty.

Earnings Corner

URBN reported a strong 4% sales growth despite tepid demand macro sentiment driven by comp sales growth of 15% at FP, 9% at Anthropologie offset by a 10% decline at Urban Outfitters. Q4 EPS came at $0.34, slightly softer than consensus estimates of $0.38, primarily as a result of store impairment charges and higher SG&A expenses due to restructuring costs at UO and higher marketing. Nuuly segment continued its exponential growth with sales growing ~150% YoY driven by continued increase in its subscriber base and strong brand follow through. Management reiterated guidance of gross margins jumping by 200 bps for the year, which we feel is achievable and take comfort from the freight tailwinds and improved promotional levels and pricing. Inventory levels increased 3% YoY in the quarter, lower than 4% sales growth (Anthro inventory up 24%, FP up 14% and UO down 5%), which is a significant improvement (inventory was up 19% YoY) in Q3. Leaner inventory levels and ability to bring in products closer to consumer demand would further aid merchandise margins for the coming year. SG&A expense is expected to jump 200 bps higher than sales growth for the year due to new hires, store selling expenses and higher marketing. It guided EPS to be ~$2.5 for 2023, higher than consensus at $2.25.

Will the Growth Continue?

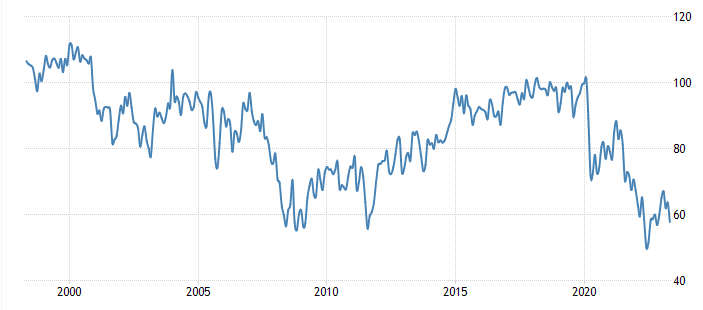

URBN delivered a solid pack of results for the last year, despite a tougher macro backdrop and that has led to its outperformance vs its peers, however should that momentum continue? FP and Anthro's exposure to higher end consumers place them in a relatively better position within the apparel retail landscape. Consumer sentiment has dropped below 60, one of the worst in the decade, and the level that was seen during the 2008 Global Financial crisis and the aftermath of the same.

United States Michigan Consumer Sentiment

{kind=link}

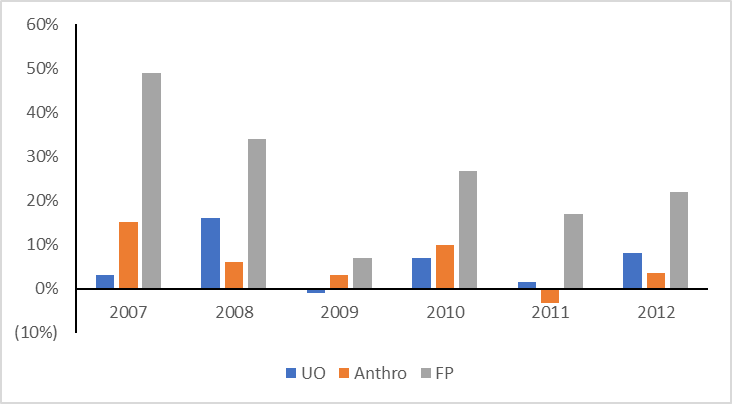

However, despite a challenging macro backdrop, the company's omnichannel focus and exposure to higher end consumers enabled them to ride through the storm, pretty nicely and FP and Anthropologie continued its positive comp growth during the turbulent times and significantly outperformed as the demand recovered.

Historical Retail Comp Sales Growth by Brand

{kind=link}

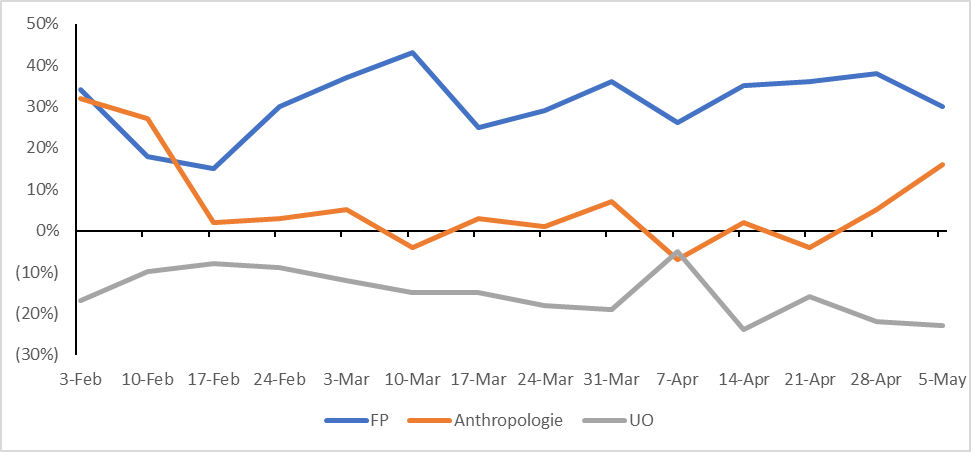

Despite a dip in foot traffic dragged by UO in QTD, according to data from placer.ai, web traffic has been strong, primarily driven by FP and Anthropologie brands. FP has shown strong traction in its spring trends and is expected to perform strongly in Q1 offset by weakness in the wholesale segment as a result of the department store's struggles. Anthropologie continued on its momentum with its occasion wear continuing to thrive along with complimentary growth observed in casual wear products with its key products of dresses, pants, jackets, and shoes witnessing steady growth and acceptance from consumers. It further witnesses strong reception to its Spring category as the brand brought in Spring receipts earlier than previous years.

Weekly Traffic Change YoY

{kind=link}

UO is expected to be under pressure due to the continued impact of North American macro environment. However, the supply chain has significantly eased with UO heavily reliant on ocean as means of transportation and improving trends in Europe could have an outsized impact on the brand reviving it back to profitability.

Nuuly Rentals also continues to grow strongly having amassed 150k subscribers already within 3 years and generating $130 mn in sales last year, a whopping ~150% jump YoY and expected to top $200 mn in current year. It is also opening a second warehouse in Kansas, double the size of the first, that will be able to handle over 600k subscribers over the coming years. Apart from that, the rentals are expected to lure lower to middle income consumers whose purses are tightened amidst the current inflationary pressures and will be able to perfectly complement growth to URBN in general (FP and Anthropologie exposure to mainly high end consumers). Management further expects Nuuly to record a profitable quarter in the second half of the year which we believe reasonable as a result of higher active subscribers which would benefit from the economies of scale.

Valuation

We believe UO is trading cheaply at just 5x 2023 EBITDA despite a strong operational management, continued earnings outperformance, cleaner balance sheet and improved inventory yields to a favorable risk reward. We rate this as Buy with a target price of $32 per share (at 7x EV/ 2023 EBITDA, a slight premium to its peers).

URBN has 19.2 mn shares remaining under its share repurchase program. We expect URBN to deliver about $400 mn in free cash flows over the next two years and expect them to repurchase about 9 mn shares which would further lead to an EPS accretion by ~$0.30.

Quant ratings also points to a strong buy rating and further upside in share price due to strong momentum and growth along with valuation comfort.

Seeking Alpha Seeking Alpha

Risks to Rating

Risks to rating include 1) deterioration in macro environment and consumer spending which can impact sales and margins 2) competitive pressure due to slowing sales could lead to an increase in promotional activities which could pressure margins 3) any challenges in inventory management would negatively impact sales and margins 4) supply chain disruption could negatively impact UO which is heavily reliant on sea transport and impact inventory availability 5) Nuuly's subscriber growth slows and continue to lose money (Rent the Runway is twice the size of Nuuly but is still unprofitable).

For further details see:

Urban Outfitters: Operational Outperformance To Drive Growth