REIT - Urgent Warning To REIT Investors

2023-09-23 09:00:00 ET

Summary

- REITs are currently facing widespread dislike among investors.

- The negative sentiment towards REITs is due to the high-interest rates.

- I explain why I believe that most investors are misguided and highlight some opportunities to consider.

After recovering a good bit in July, REITs ( VNQ ) came right back down in August:

The focus remains on rising interest rates and it is scaring off investors.

There just doesn't seem to be much appetite for REITs in a world with >5% interest rates. Here are a few comments that I received on my public articles in the past weeks:

"No sense in owning something yielding 5.5% when I can get 5.2% from a money market fund."

---

"When you can get 5.2% risk free in a money market fund why take future market risk with a REIT that has lost value to the extent higher interest rates will translate into lower FFO growth going forward."

---

"I think the bonds are the better choice for the short term. Up to 2025. Yields are higher than dividends."

Moreover, these comments appear to be gaining "likes" from other like-minded investors.

But here's my warning to you: REITs are NOT bond replacements.

Many people appear to think that just because REITs offer a lower dividend yield than money market funds, they should be avoided.

But this is very shortsighted because REITs are not just income investments. They are total return investments and the dividend yield is just one component of the total return.

Take the example of VICI Properties ( VICI ), which is the owner of trophy casinos such as the Caesars Palace in Las Vegas:

VICI Properties

It offers today a 5% dividend yield and so according to this logic, you should avoid it at all costs.

But in addition to this dividend payment, VICI is expected to grow its cash flow (on a per-share basis) by 10% in 2023. It is growing so rapidly because its leases enjoy annual rent hikes and it retains a large chunk of its cash flow and raises more capital to buy additional properties.

So you get a 5% dividend yield + 10% FFO per share growth, and that gets you to a 15% annual total return, assuming that its valuation multiple remains intact. This is nothing exceptional for the REIT as this is more or less what it has achieved since going public:

YCHARTS

But even assuming that its long-term growth rate drops down to just 5%, a historically low figure for VICI, it would still offer very attractive total return potential:

5% dividend yield + 5% FFO per share growth = 10% average annual total on a constant multiple basis.

(Note that a 5% growth rate should be very doable for VICI given that it uses relatively little leverage, which is true for most REITs, its leases include CPI-based rent escalations, and it also retains 35% of its cash flow to reinvest in growth. In that sense, its cash flow yield is actually 7.7%, but VICI retains 2.7% for growth and pays a 5% dividend yield.)

Would you rather earn a 5% yield on a money market fund, which will result in a 2-3% annual real return after inflation, or would you prefer to earn a 10% average annual total return owning REITs?

If you are petrified by volatility and have a short investment horizon, then sure, go for the 2-3% real return. You won't get ahead by much but you will sleep better at night.

But if you have a long investment horizon and enough discipline to ignore the volatility, then favoring REITs, which offer a ~3x higher annual real return, is really a no-brainer to me.

And it gets better, a lot better!

Today, REITs are priced at historically low valuations because of the high-interest rates.

But what if these high-interest rates aren't here to stay after all?

Investors are quick to extrapolate recent trends far into the future, but, in my opinion, the reality is that today's high interest rates are simply the result of the surge in inflation that resulted from the pandemic and Russia's brutal invasion of Ukraine.

Now, this inflation is already gone. The last CPI reading was just 3% and if you adjust for its lagging shelter component, the real-time CPI is already down to the Fed's target rate of 2%.

Therefore, the high-interest rates really aren't needed anymore. They served their purpose in cooling down the inflation, but how long will it take before they are cut again?

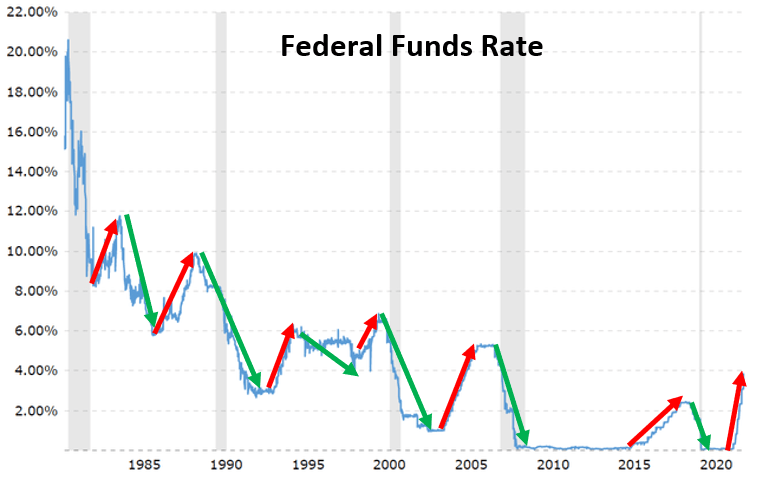

Many are today assuming that the high rates are here to stay, especially following the Fed's recent comments , but if you look back at the last 40 years, you will see that every period of rising rates has ended shortly after with major rate cuts:

{kind=link}

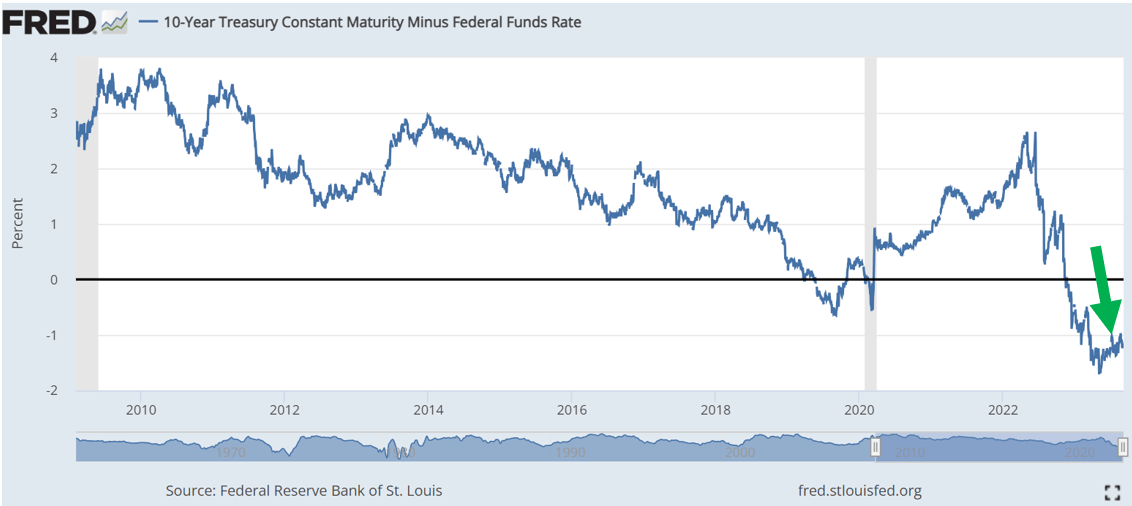

Eventually, the economy will inevitably feel the pain of higher interest rates and this will likely push it into a recession. The Fed is doing its best to manage expectations and talking about "higher for longer", but the debt market is already pricing significant rate cuts with the yield curve more inverted than ever and this indicator has a near-perfect track record of predicting recessions:

{kind=link}

Therefore, I think that it is likely that today's policy of high-interest rates won't last for long.

It seems much more likely that it was a temporary policy to a temporary crisis.

The Fed is of course playing tough as it wants to manage expectations to avoid a second spike in inflation, but as the economy dips into a recession, and the fears of inflation turn into fears of deflation, interest rates will likely again return to lower levels.

China is already dealing with deflation, which is a much bigger threat than inflation to highly leveraged economies, and today's deflationary forces are stronger than ever:

- Governments are heavily indebted

- The population is aging rapidly

- New innovations such as AI are resulting in lower costs

These deflationary forces explain why interest rates have been trending lower for 40+ years and they are today stronger than ever. The likes of Elon Musk are predicting that we are going into an age of abundance in which everything will be "ridiculously cheap" as a result of AI and robotics.

But I digress.

My warning here is simply that today's high-interest rates likely won't last forever so selling at today's low levels based on this single factor is a big mistake in my opinion.

Today, REITs are priced as if the high-interest rates were here to stay, which gives us great margin of safety in case we were wrong. REITs are priced on average at just 13.5x FFO even as the S&P500 ( SPY ) is priced at 25.5x earnings after its recovery:

YCHARTS

But as interest rates return to lower levels, it will be REITs' turn to profit.

A REIT like VICI may deserve to trade at 16-18x FFO, but today, it is priced at just 13x FFO.

Taking a more extreme example: Crown Castle ( CCI ) traded at 26x FFO before the recent crash. Today, it is priced at less than half of that:

Another good example would be Alexandria Real Estate ( ARE ). It was priced at around 24x FFO, but you can now buy it at just 12x FFO:

Even getting back just halfway to their previous peaks would unlock about 50% upside from here and those valuations wouldn't be excessive by any means. These are investment-grade-rated blue-chip type REITs with exceptional track records and attractive long-term growth prospects.

And so if you now expect this recovery to play out over the next 3-5 years, then your annual total returns would surpass 20% when you add the repricing upside on top of the yield and the growth.

~5% dividend yield + ~5% annual growth + >10% annual repricing upside = >20% average annual total return

This may seem a little far-fetched to you, but it really isn't in my opinion.

REITs have crashed countless times throughout their history, but they have always fully recovered because good real estate is growing in demand and limited in supply:

NAREIT

Moreover, whenever REITs have been priced at such low valuations, they have typically been especially rewarding in the following years.

In fact, you will note that the returns that we are forecasting are actually quite a bit lower than the historic performance of REITs following such crashes:

{kind=link}

Finally, REITs are today priced at these historically low valuations despite having the strongest balance sheets ever and enjoying solid rent growth. The only reason for the discount is the high-interest rate policy but as this is removed, I expect REITs to again push new all-time highs. After all, rents are higher than ever and so are property replacement values.

Therefore, it seems very shortsighted to avoid REITs simply because their dividend yields are often lower than the yields of money-market funds.

REIT dividend yields are low because they retain a lot of their cash flow for growth. Even with very reasonable assumptions, you can forecast very compelling returns for REITs in the coming years.

So you can choose between earning today a safe 5% yield, which is really only about 2-3% after inflation, and even this may not last for long as interest rates will likely return to lower levels, exposing you to significant reinvestment risk.

Or you could invest in REITs at historically low valuations and position yourself for ~10% annual expected total returns from the yield and growth alone, plus some additional upside when interest rates return to lower levels.

The choice is not complicated for me and so my thoughts haven't changed and I expect to keep accumulating a lot more REITs in the coming weeks.

For further details see:

Urgent Warning To REIT Investors